Singtel share price falls after record dividend. Is the blue chip stock still attractive?

Stocks

By Goh Lay Peng • 26 May 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

Singtel’s share price fell after FY2026 results despite a record dividend. We look at its dividend yield, earnings and risks.

What happened ?

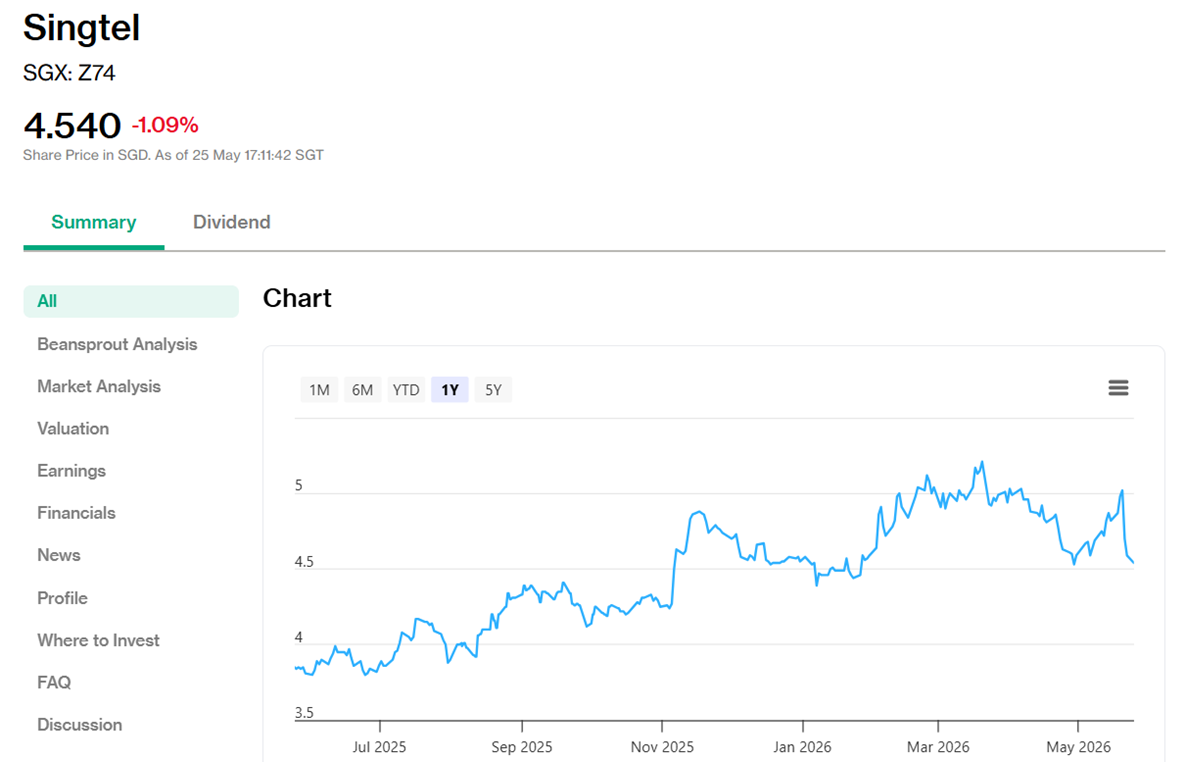

Singtel’s share price has come under pressure.

This marks a sharp reversal from earlier this year, when Singtel was among the Singapore blue chip stocks trading near all-time highs.

After announcing its financial year 2026 (FY2026) results on 21 May 2026, Singtel’s share price fell 9.6% to close at S$4.54 as of 25 May 2026.

This was despite Singtel reporting a record ordinary dividend, stronger underlying profit, and progress in its Singtel28 strategy.

One possible source of selling pressure may have been the ongoing transfer of Singtel Special Discounted Shares (SDS).

The recent correction sparked discussion in the Beansprout community, with some investors asking whether Singtel now looks more attractive as a dividend stock after its share price decline.

In this article, I’ll take a closer look at why Singtel’s share price fell, what stood out from its FY2026 results, and whether Singtel remains attractive as a Singapore blue chip dividend stock.

Why did Singtel share price fall despite stronger FY2026 results?

Singtel’s FY2026 results were strong at the group level.

However, investors may have been concerned about a few areas beneath the surface.

#1- Singtel Singapore earnings remained under pressure

The first concern was Singtel Singapore which is Singtel’s core telco business.

Revenue fell 3.1% year-on-year, while earnings before interest and tax (EBIT) declined 4.6% year-on-year.

EBIT is a measure of operating profit. In simple terms, it gives us a sense of how profitable the business is before interest and tax.

Singtel Singapore’s EBIT margin also fell to 21.5%.

This reflected continued price competition in the consumer telco market, as well as higher spectrum amortisation costs from its 700MHz acquisition.

In other words, the core Singapore telco business is still facing structural pressure.

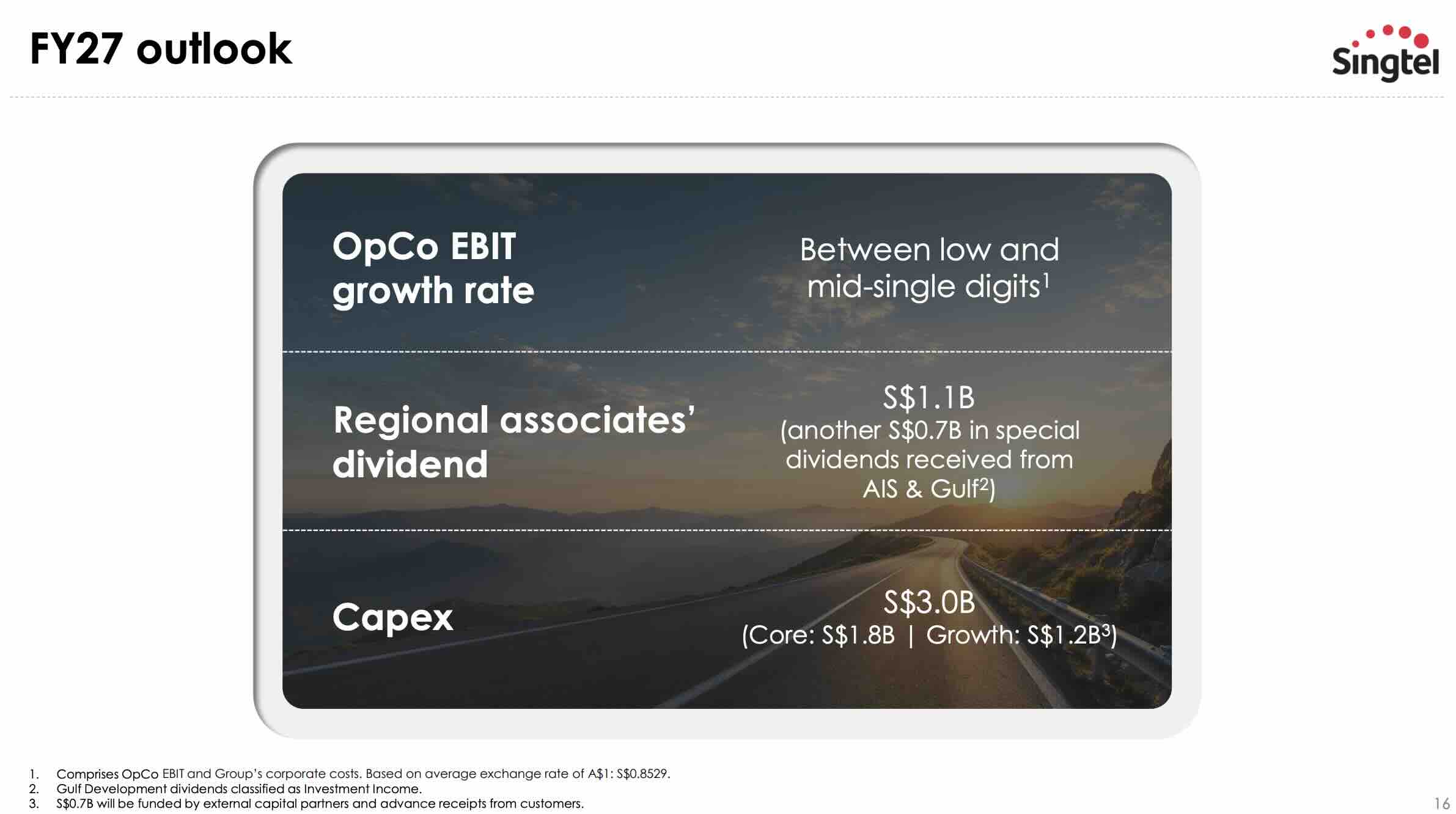

#2 - Singtel FY2027 guidance was more cautious

The second concern was Singtel’s FY2027 guidance.

Management guided for Singtel Singapore’s EBIT growth to be in the low-to-mid single digits.

This would be slower than the 10% growth delivered in FY2026.

The management cited uncertainty from the Middle East conflict and the surprise suspension of the proposed Singapore mobile market consolidation review.

This suggests that while Singtel’s overall strategy may be progressing, earnings growth in the near term may not be as strong as before.

In addition, capex is expected to increase to S$3.0 billion in FY27 from S$2.5 billion in FY26. This include S$1.8 billion of core capex, as well as S$1.2 billion of growth capex.

Notably, the growth capex is expected to be deployed into its graphics processing unit (GPU)-as-a-service business.

#3 - Selling pressure from Singtel Special Discounted Shares (SDS) transfer

Another factor weighing on Singtel’s share price was selling pressure from SDS holders.

The ongoing transfer of Singtel SDS shares from Central Provident Fund (CPF) accounts to Central Depository (CDP) accounts has created a steady flow of selling in the market, with around 120,000 holders choosing to cash out their holdings.

While this does not necessarily change Singtel’s long-term fundamentals, it may have added short-term pressure to the share price.

What stood out from Singtel FY2026 results?

Despite the share price weakness, Singtel’s FY2026 results had several bright spots.

The key question is whether these positives are enough to offset the near-term concerns.

#1 - Singtel Optus showed stronger earnings recovery

Optus appears to be turning around.

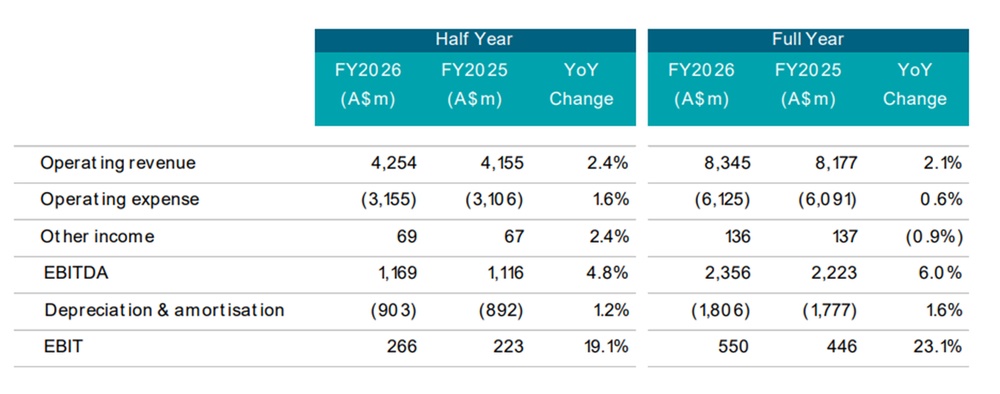

Optus delivered revenue growth of 2.1% to A$8.3 billion, driven by postpaid price increases and customer growth in its value brand amaysim.

More importantly, EBIT surged 23.1% to A$550M as mobile growth and network-sharing revenues from the MOCN (Multi-operator core network) arrangement more than offset higher network and remediation costs.

The improvement signals that Optus' multi-year recovery is taking hold.

#2 - NCS hit record bookings and expanded margins

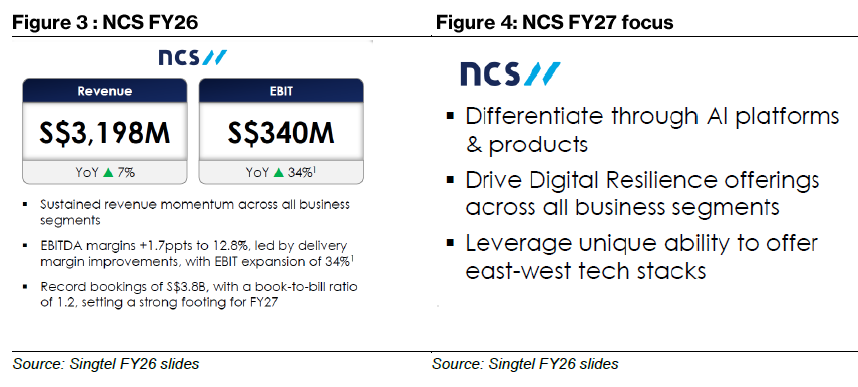

NCS, Singtel’s technology services arm, was another positive area in Singtel’s FY2026 results.

NCS grew revenue 7.4% to S$3.2 billion and expanded EBIT by 33.9%. Excluding a one-off subcontractor credit, EBIT still grew 30%. .

NCS also improved its earnings before interest, tax, depreciation and amortisation (EBITDA) margin by 1.7% to 12.8%, helped by better delivery efficiency.

The most important figure may be its bookings.

NCS reported record bookings of S$3.8 billion, , with a book-to-bill ratio of 1.2 times

A book-to-bill ratio above 1 means that new orders were higher than revenue recognised during the year.

This gives Singtel better visibility over future earnings from NCS heading into FY2027.

#3 — Singtel Singapore under pressure, but enterprise offsets consumer declines

Singtel Singapore remained the weaker part of the results, with revenue down 3.1% and EBIT down 4.6% as price competition and higher spectrum amortisation costs weighed on profitability.

However, there was one encouraging shift.

Enterprise now contributes over 50% of Singtel Singapore 's revenue.

This shows that Singtel Singapore is becoming less dependent on the traditional consumer mobile business.

Instead, the business is moving towards higher-value areas such as business-to-business services, artificial intelligence infrastructure, government contracts and enterprise solutions.

This transition may take time, but it could help make Singtel Singapore more resilient over the longer term.

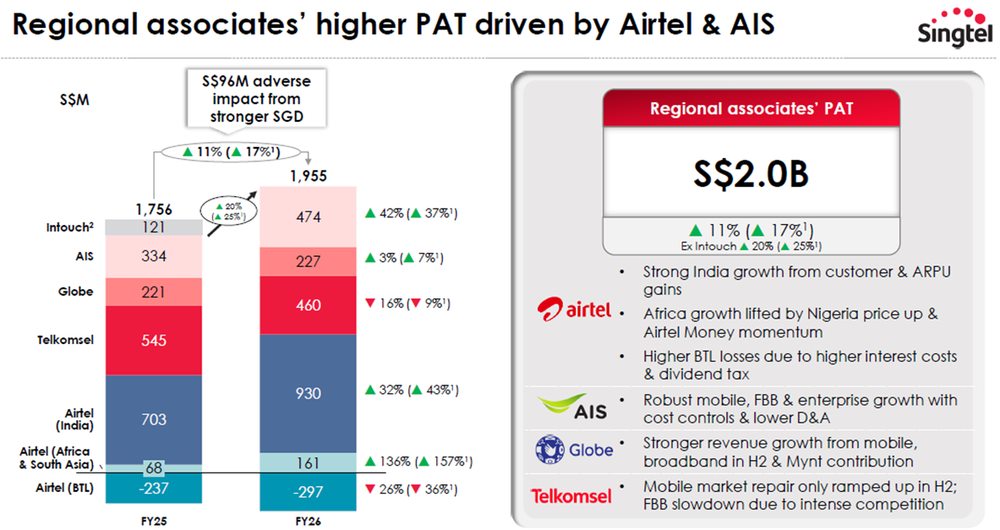

#4 — Singtel regional associates' profit after tax rose 20%, led by Airtel and AIS

Singtel’s regional associates portfolio also delivered stronger earnings.

The portfolio, which includes Airtel, AIS, Globe and Telkomsel, reported net profit of S$2.0 billion, up 20% year-on-year.

Airtel Group delivered stronger earnings driven by sustained growth across its India operations and a robust performance in Africa.

AIS’ contribution rose on the back of robust mobile and fixed broadband growth, disciplined cost management and lower depreciation and amortisation.

Telkomsel was the weaker performer, as Indonesia's mobile market repair only began in the second half.

Overall, the regional associates remain an important earnings driver for Singtel.

This also gives Singtel exposure to regional telecom markets beyond Singapore and Australia.

Note: 1. On constant currency basis.

2. Intouch’s contribution ceased in April 2025, following its merger with Gulf Energy to form Gulf Development, of which Singtel holds an equity interest of 7.7% and has been accounted as a “Fair Value Through Other Comprehensive Income” investment.

#5 — Singtel RE:AI GPU compute business is the new AI growth engine

Singtel is scaling RE:AI, its graphics processing unit (GPU)-as-a-service business that supports artificial intelligence (AI) workloads. The business is separate from its Nxera data centres and gives Singtel another way to tap demand for AI infrastructure.

In FY2026, RE:AI completed its pilot phase, with 1 megawatt (MW) deployed and S$25 million in revenue.

Singtel now plans to scale the business further.

Up to S$600 million in capital expenditure (capex) is planned for FY27, with up to 11MW to be deployed using GB200 and GB300 chips.

Importantly, more than 80% of the target contracted capacity has already been secured before build.

Singtel is targeting comparable EBIT margins to its data centre business and a low-teens unlevered internal rate of return (IRR).

The pipeline of contracts already secured stands at approximately S$600 million over three to five years.

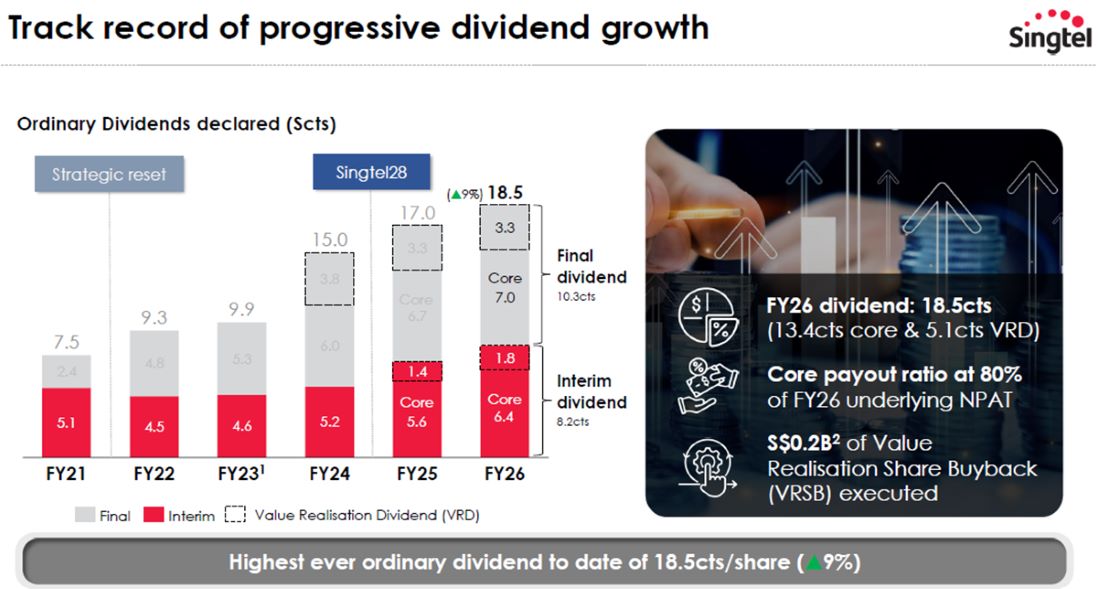

#6 — Singtel dividend reached a record 18.5 cents per share

Another key highlight was Singtel’s dividend track record.

Singtel declared a record ordinary dividend of 18.5 cents per share for FY2026, marking its fifth consecutive year of ordinary dividend growth.

The 18.5 cents per share FY2026 payout comprises two parts.

The first is a core dividend of 13.4 cents per share, based on an 80% payout ratio of underlying net profit after tax (NPAT).

The second is a value realisation dividend (VRD) of 5.1 cents per share, funded by asset recycling.

Asset recycling simply means that Singtel is selling or reducing stakes in some assets, and using part of the proceeds to reward shareholders or reinvest into growth areas.

In FY2026, Singtel recycled S$3.9 billion, mainly from partial Airtel stake sales.

Since April 2024, Singtel has recycled about S$5.8 billion towards its S$9 billion mid-term target.

The board also bought back S$226 million of shares under its VRSB (value realisation share buyback) programme.

Singtel’s shareholder returns are being supported not just by operating earnings, but also by its ongoing asset recycling programme.

1. Excludes 5cts/share special dividend declared in FY23.

2. As at 20 April 2026 before FY26 results trading blackout.

Is Singtel still attractive as a blue chip dividend stock for income investors?

Based on Singtel’s financial year 2026 (FY2026) dividend per share of 18.5 cents and share price of S$4.54, Singtel offers a dividend yield of about 4.1%.

This is higher than the Singapore Government Securities (SGS) 10-year bond yield of 2.1%, giving Singtel a yield spread of about 2.0 percentage points over the Singapore 10-year government bond yield.

The dividend also appears to be supported by more than just asset recycling.

Singtel delivered a strong FY2026 across several key areas, with Optus recovering, NCS expanding margins, and regional associates growing profits.

These helped lift Singtel’s underlying profit by 20.7%, while the group also met its low double-digit return on invested capital (ROIC) target ahead of schedule.

Singtel also has financial flexibility to support shareholder returns and its Singtel28 growth plans.

The group recycled S$3.9 billion of assets in FY2026, and still has a remaining S$3.2 billion of assets targeted for divestment over the next 24 months.

Based on Singtel’s guidance for FY27, it is highly likely that Singtel is able to maintain the dividend per share at the same level.

However, the main watch points for FY2027 would be the cautious EBIT guidance of low-to-mid single digits, reflecting Middle East uncertainty and the paused Singapore mobile consolidation, and whether RE:AI can hit its ambitious commercial ramp and whether Singtel can execute its asset monetisation plans on schedule. .

What would Beansprout do?

In my view, Singtel can still play a role in an income-focused portfolio

Despite the recent rise in bond yields, Singtel’s dividend per share appears relatively resilient. Its FY2026 dividend yield of about 4.1% remains above the Singapore 10-year government bond yield, while the payout is supported by operating earnings, contracted revenue, asset recycling and financial flexibility.

This makes Singtel a potential candidate for the Income Pot, especially for investors looking beyond REITs for Singapore blue chip dividend stocks that can sustain distributions while still investing for growth.

At the same time, I would not view Singtel as an Opportunity Pot idea just because its share price has corrected.

The current macro environment remains uncertain, and this could affect the pace of Singtel’s asset monetisation plans. There may also be delays if Singtel takes longer than expected to IPO or monetise some of its assets.

The near-term outlook also requires some patience. Singtel Singapore’s FY2027 earnings guidance is more cautious, while RE:AI still needs to prove that it can scale into a meaningful growth contributor.

Overall, Singtel still looks attractive as a blue chip dividend stock for income investors who are comfortable with these watch points.

It may not offer the sharpest growth story in the Singapore market, but it offers a mix of defensive dividends, improving core businesses, and new growth optionality through areas such as artificial intelligence infrastructure.

If you’d like to screen for other Singapore stocks with attractive dividend yields and potential upside, you can explore our Singapore dividend stocks screener.

Would you consider Singtel as an income stock after its recent share price correction, or would you wait for more clarity on its FY2027 outlook? Share with us in the comments below or in our Telegram group!

Planning to invest in Singtel? Compare the best Singapore brokers to find the right trading platform, and see the latest promotions and sign-up rewards available.

Follow Beansprout on Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments