Beyond SpaceX IPO: Inside the US$1.8 trillion space economy

Stocks

By Gerald Wong, CFA • 06 Jun 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

We look beyond SpaceX IPO to break down the US$1.8 trillion space economy, from satellites and defence to exposure routes and what investors should consider.

What happened?

Investor attention around the space economy is rising.

Earlier, we looked at how the artificial intelligence boom has lifted demand for chips, data centres, cloud platforms and power infrastructure. The space economy is drawing attention for a similar reason.

The expected SpaceX initial public offering has brought fresh focus to satellite broadband, reusable rockets and the wider commercial space sector.

Reuters reported that space-related exchange-traded funds (ETFs) attracted US$1.3 billion of inflows in the month leading up to 23 May 2026, as investors positioned for a potential SpaceX listing.

But the bigger story goes beyond SpaceX. Just as the internet created new layers of connectivity in the 1990s, satellites are now supporting broadband, navigation, Earth observation, defence and global communications.

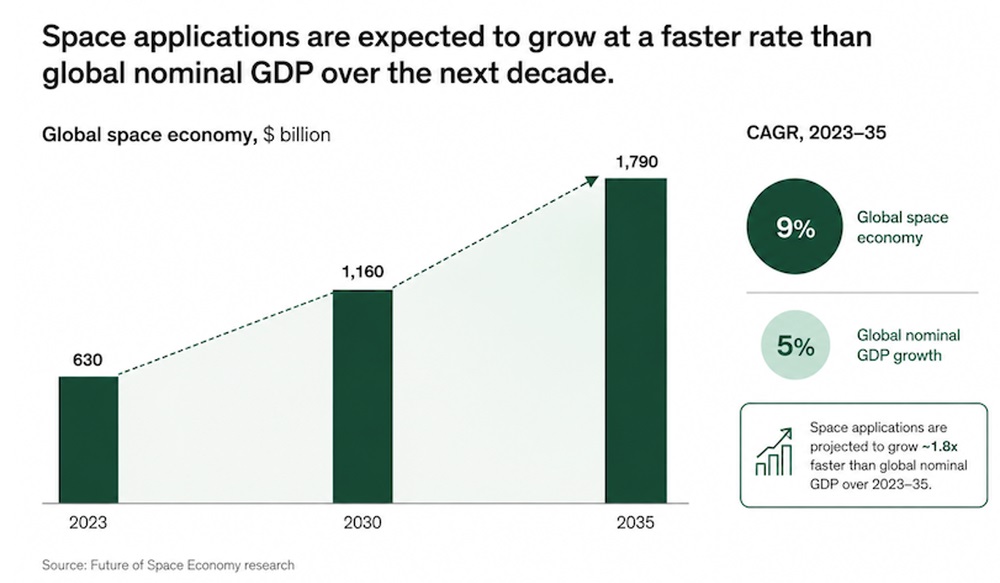

According to the World Economic Forum and McKinsey & Company, the global space economy could grow from US$630 billion in 2023 to US$1.8 trillion by 2035.

In this article, I look at what is driving the space economy, how the value chain works, and the key risks investors should understand.

Why the space economy is becoming a bigger investment theme

For a long time, space was mainly funded by governments. Projects were expensive, highly technical, and often linked to national defence, scientific research or national prestige.

That has started to change.

Reusable rockets, smaller satellites and private capital have reduced the cost of sending equipment into orbit. This has allowed more companies to build satellite networks and commercial space services.

At the same time, demand for space-based services has grown.

Many everyday activities now depend on satellites, even if we do not always notice them. For example, satellites support internet connectivity in remote regions, GPS navigation, financial transactions, aviation systems, weather forecasting, maritime tracking and military communications.

This is why the space economy is increasingly seen as an infrastructure theme.

It is not just about space exploration. It is about the systems that help keep the digital economy connected.

The real investment opportunity of the space economy is infrastructure

When investors think about space, they often focus on moon missions or space tourism. But the more durable investment case may sit elsewhere.

A simple way to understand the space economy is to split it into two layers.

The first layer of opportunity lies in space infrastructure. This includes launch systems, satellites, ground equipment, communications networks and defence-linked systems. These are the foundational technologies that enable the broader space economy to function.

The second layer is space-enabled services. . These are businesses and industries that use satellite data or satellite connectivity. Examples include agriculture, logistics, insurance, maritime operations, aviation, climate monitoring and disaster response.

As these industries expand their use of satellite infrastructure, companies operating in the space ecosystem may benefit indirectly through growing demand for services and data.

There are also more speculative areas such as space tourism, lunar missions, orbital stations and in-space manufacturing.

These areas often attract public attention, but many are still at an early stage of commercial development.

This distinction matters because many headline projections for the “space economy” include industries that merely use satellite data, rather than companies directly operating in space.

As a result, not every company with “space exposure” will necessarily capture the full value of those trillion-dollar forecasts.

It is useful to understand which part of the value chain a company or exchange-traded fund is exposed to.

The six major parts of the space economy value chain

The space sector is broad, and different sub-sectors come with very different risk profiles.

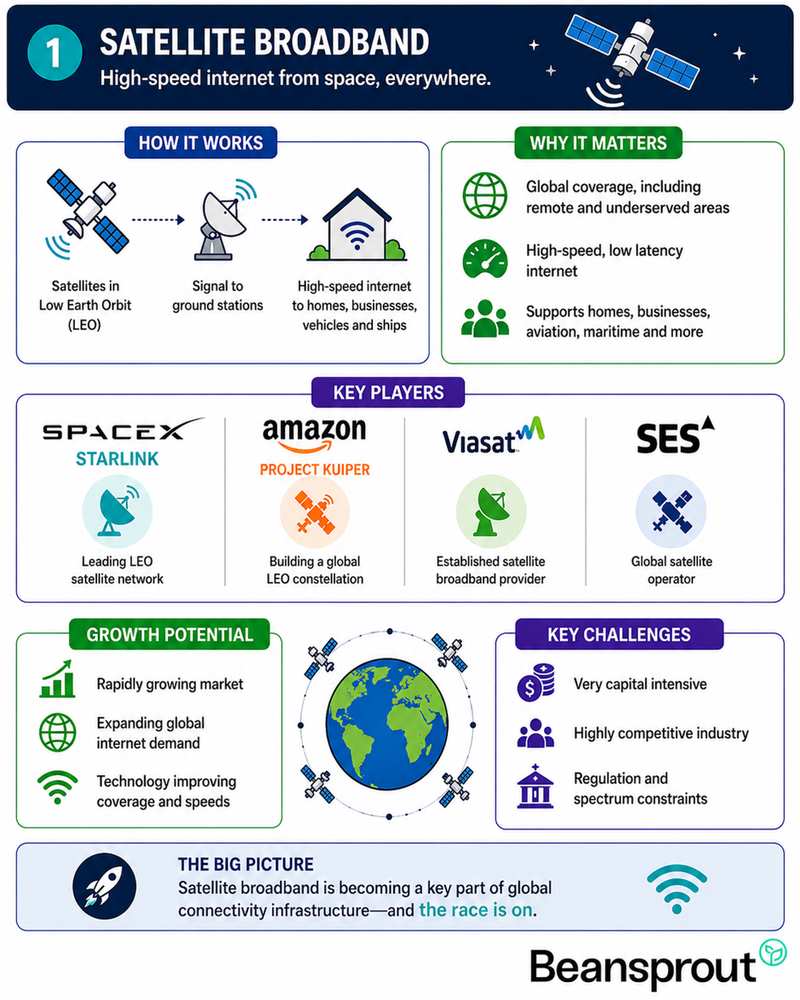

#1 - Satellite broadband

One of the fastest-growing areas is satellite broadband.

Low-Earth orbit satellite networks are expanding internet coverage globally, especially in remote and underserved regions where traditional fibre infrastructure is difficult to build.

Companies such as SpaceX, through Starlink, and Amazon are investing heavily in satellite internet constellations. Traditional satellite operators such as Viasat and SES are also part of this ecosystem.

While growth potential is significant, this segment is extremely capital intensive and highly competitive.

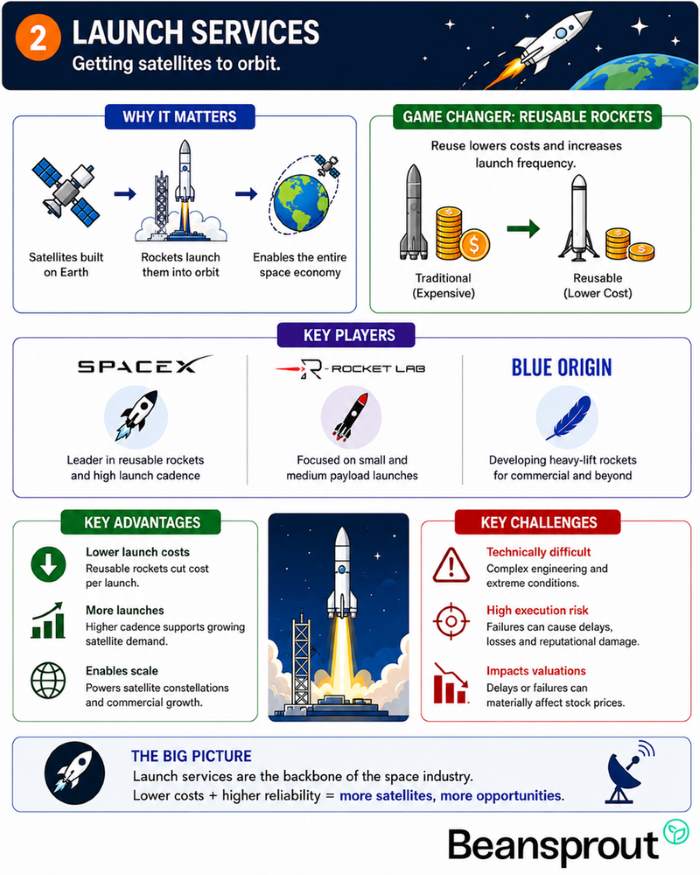

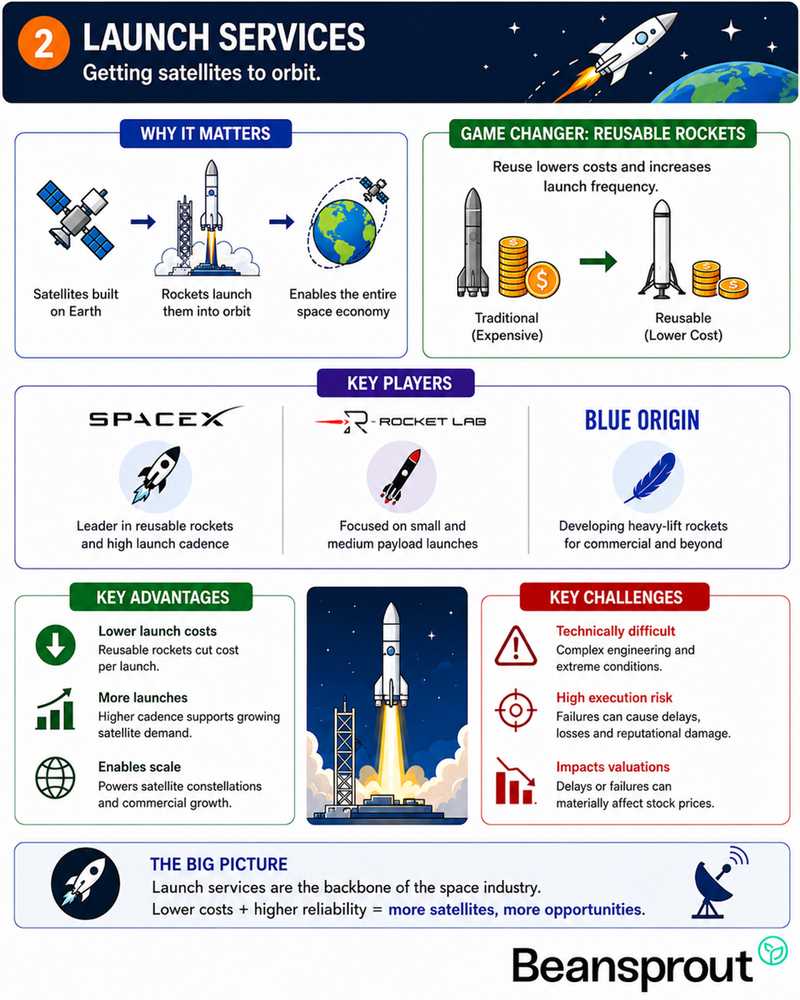

#2 - Launch services

Rocket companies form the backbone of the industry because every satellite still needs to be deployed into orbit.

Reusable rockets have significantly reduced launch costs, helping commercial space activity scale more quickly.

Companies such as Rocket Lab, SpaceX and Blue Origin are key players in this area.

However, launch remains a technically difficult business with high execution risk, where delays or mission failures can materially impact valuations.

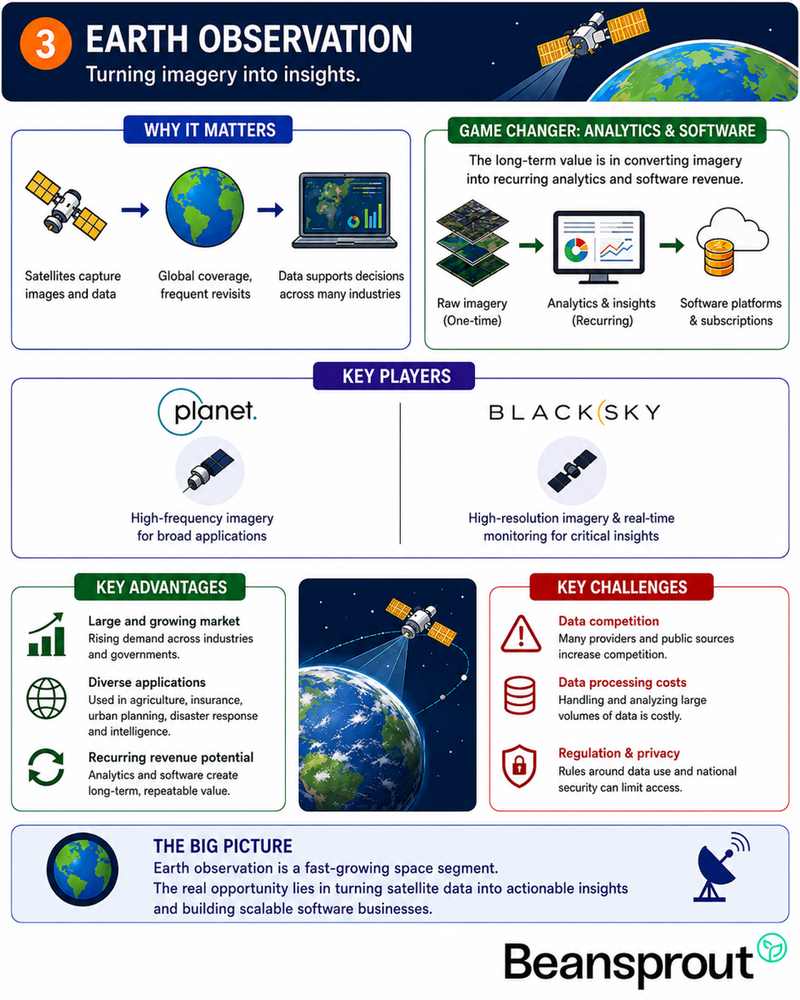

#3 - Earth observation

Earth observation is another growing category. Satellite companies now collect imagery and data used across agriculture, insurance, urban planning, disaster response and intelligence gathering.

The long-term value may not lie purely in taking satellite images, but in converting those images into recurring analytics and software revenue.

Companies such as Planet Labs and BlackSky are examples of listed firms operating in this segment.

#4 - Defence and space security

Defence and space security remain some of the most established parts of the industry.

Governments continue to spend heavily on missile warning systems, military satellites, secure communications and space surveillance capabilities. This gives established defence contractors more predictable revenue streams compared with early-stage space startups.

Companies such as Northrop Grumman, Lockheed Martin and L3Harris are exposed to this trend.

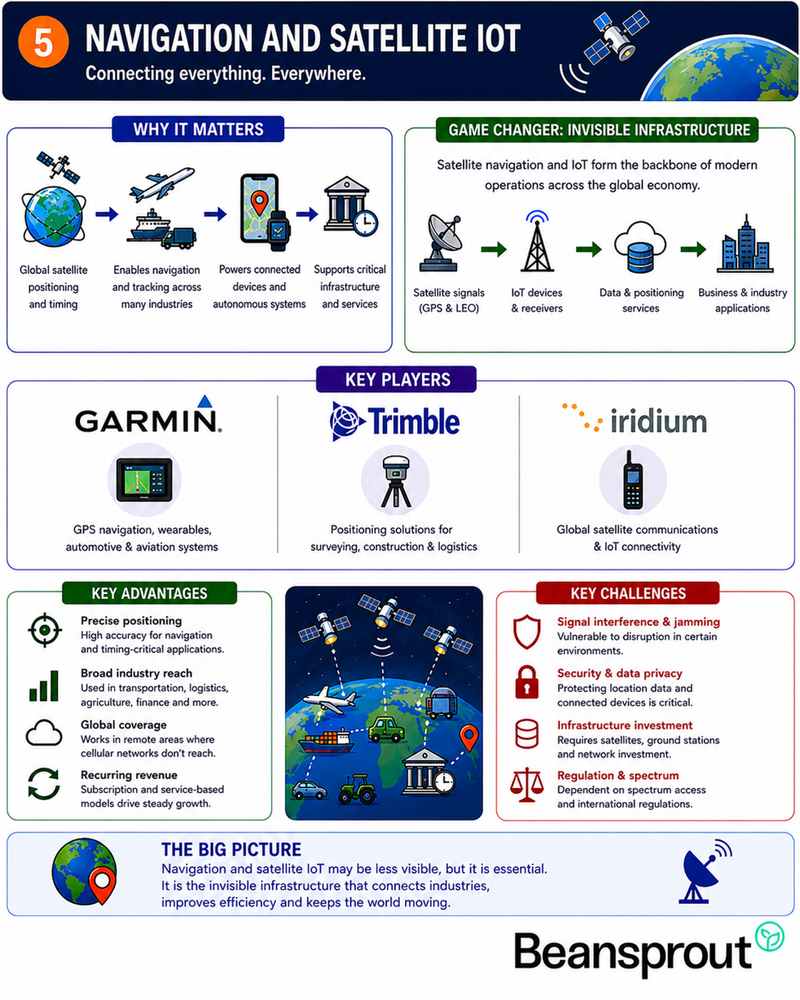

#5 - Navigation and satellite Internet of Things (IoT)

Another important but less visible segment is navigation and satellite-enabled IoT infrastructure. Satellite positioning systems support GPS navigation, aviation systems, logistics tracking, autonomous technologies, maritime operations and even financial transaction timestamping.

While this may appear less exciting than rockets or moon missions, it forms part of the invisible infrastructure powering many modern industries.

Companies such as Garmin, Trimble and Iridium Communications provide exposure to this segment.

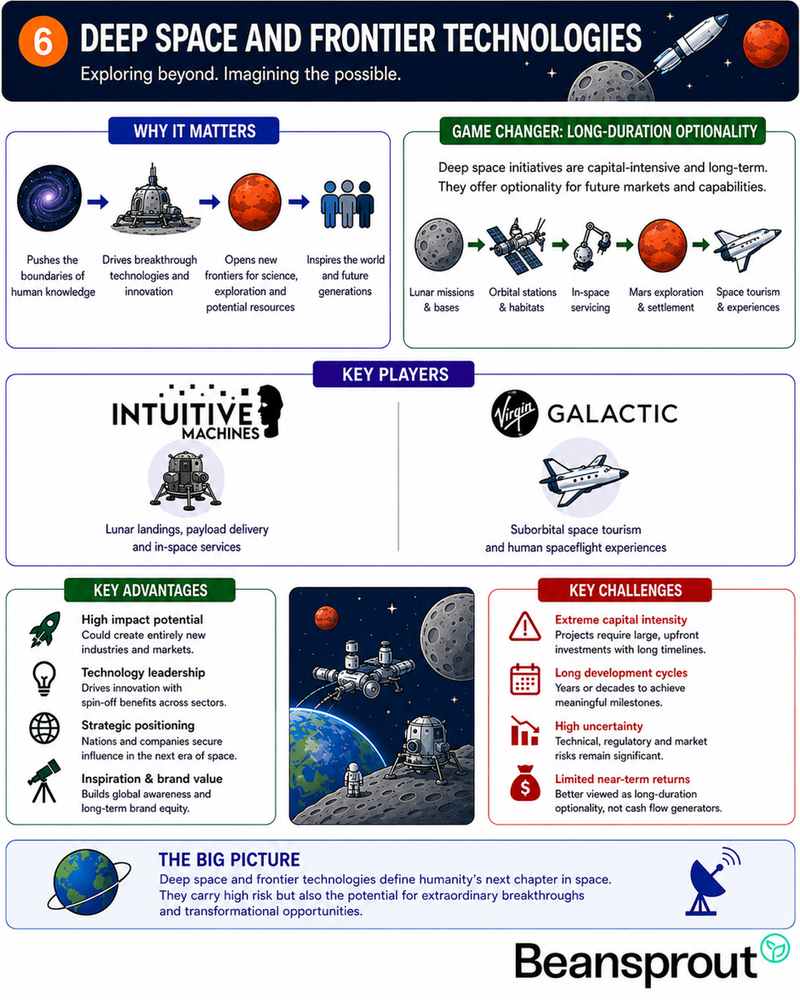

#6 - Deep space and frontier technologies

At the furthest end of the spectrum sits deep space and frontier technologies. This includes lunar missions, orbital stations, in-space servicing, Mars-related projects and space tourism.

Companies such as Intuitive Machines and Virgin Galactic operate in these areas.

While these businesses attract significant public attention, they remain highly speculative and are better viewed as long-duration optionality rather than near-term cash flow generators.

How investors can gain exposure to the space economy theme

For Singapore investors, most investable opportunities are listed in the US market.

One practical starting point may be diversified aerospace and defence ETFs.

For investors who prefer more established businesses, defence contractors may offer a more stable way to gain exposure to the space theme through long-term government contracts and defence spending.

What investors should watch closely before investing in the space economy theme

One important point is that space excitement does not always translate into profits.

The space economy is a long-term structural theme, but investors should be aware of the risks.

The sector includes both mature cash-generating businesses and highly speculative companies.

Some firms already have established government contracts and recurring revenue streams, while others remain dependent on future funding rounds and unproven business models.

Before investing, investors should assess whether a company has a realistic path toward profitability, whether revenue is supported by long-term contracts or recurring demand, and whether current valuations are based on actual cash flow or future expectations.

Government spending also remains a major driver of the industry.

Unlike many consumer technology sectors, large parts of the space economy still depend heavily on defence departments and national space agencies. This can provide long-term funding stability, but it also creates exposure to procurement cycles, political priorities and shifting government budgets.

Finally, investors should recognise that space is likely to remain a long-duration theme rather than a short-term trading story.

Industry growth will probably unfold over many years as launch costs continue falling, satellite adoption expands and downstream applications become more integrated into the global economy.

What would Beansprout do?

The strongest version of the space investment thesis is about infrastructure.

Launch systems, satellites, communications networks, defence systems and positioning technologies are increasingly becoming foundational parts of the modern economy.

At the same time, I would not assume that every space-linked stock or exchange-traded fund will benefit equally from the growth of the space economy.

The more a company depends on future launches, future funding or years of strong growth, the less room there may be for disappointment.

That is why I would keep three principles in mind.

First, separate the theme from the trade. Believing that the space economy can grow over time does not mean every space stock is attractive at any price. I would always ask what growth expectations are already reflected in the valuation.

Second, understand where the exposure comes from, as the risk profile can be very different across these groups.

Third, expect volatility. Space is still a capital-intensive industry, and smaller companies may be affected by launch delays, funding needs, technical setbacks or changes in government spending.

For investors looking at the theme, aerospace and defence exchange-traded funds may offer broader exposure to established companies, while thematic space exchange-traded funds or individual space companies may offer more direct but potentially more volatile exposure.

Space may eventually become one of the defining infrastructure themes of the next decade. But like many emerging industries, separating durable businesses from speculative narratives will matter far more than simply buying into the excitement.

For broad portfolio planning, a long-term structural theme like the space economy would sit closer to the Growth Pot, where the focus is on diversification and participation in multi-year trends.

More concentrated space-related stocks would sit closer to the Opportunity Pot, where position sizing and exit discipline matter more.

The goal is not to decide whether space is the next AI. It is to understand where the real business models are, how much risk is already priced in, and whether the theme fits into a diversified portfolio.

For a broader framework, you can read more about how we build a portfolio across the four pots of wealth through different market cycles here.

Do you think the space economy could become a major investment theme in the years ahead? Share your thoughts in the comments below or join the discussion in our Beansprout Telegram community.

Enjoyed this insight? Follow Beansprout on Telegram, Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments