T-bill yield rises to 1.55% in latest 16 July auction

Bonds

By Gerald Wong, CFA • 16 Jul 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

The cut-off yield for the 6-month Singapore T-bill rises to 1.55% p.a. in the latest auction on 16 July.

What happened?

The latest 6-month Singapore T-bill auction results are out.

The latest increase brought the 6-month Singapore T-bill yield to its highest level since the start of the year.

This marked the second consecutive increase, after the cut off yield rose to 1.50% in the previous 6-month Singapore T-bill (BS26113X) auction on 2 July.

I have seen on-going discussion in the Beansprout telegram community about how the T-bill compares to the best fixed deposit rates in Singapore as a place to park our cash to earn a higher yield.

In this article, I’ll look at what drove the increase in the T-bill yield, and whether there are better alternatives for investors looking to park their cash.

What we learnt from the latest 6-month Singapore T-bill auction

#1 - Demand for the Singapore T-bill fell slightly

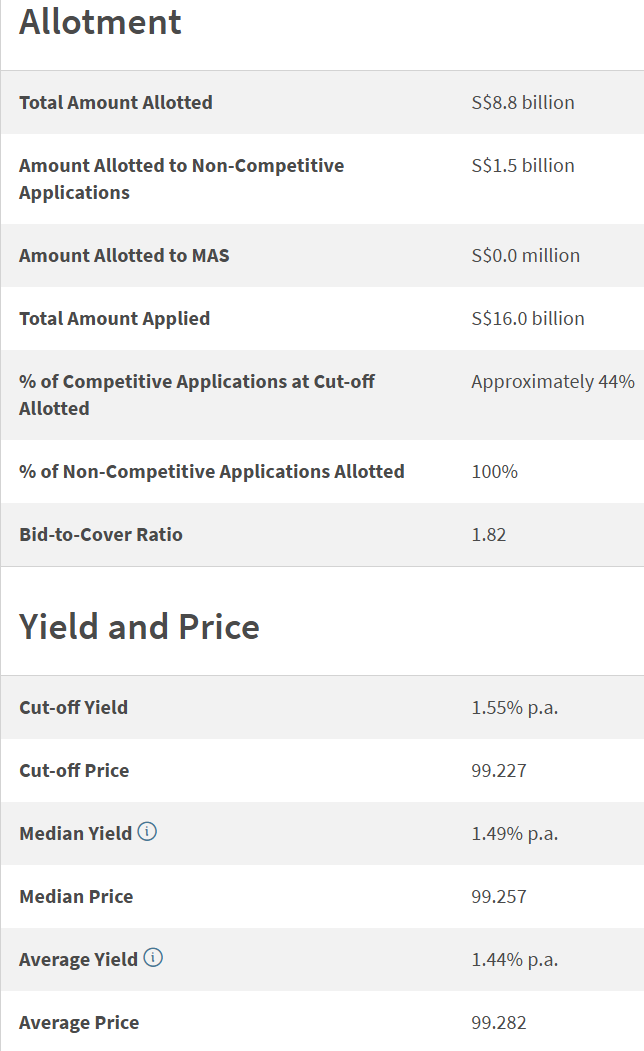

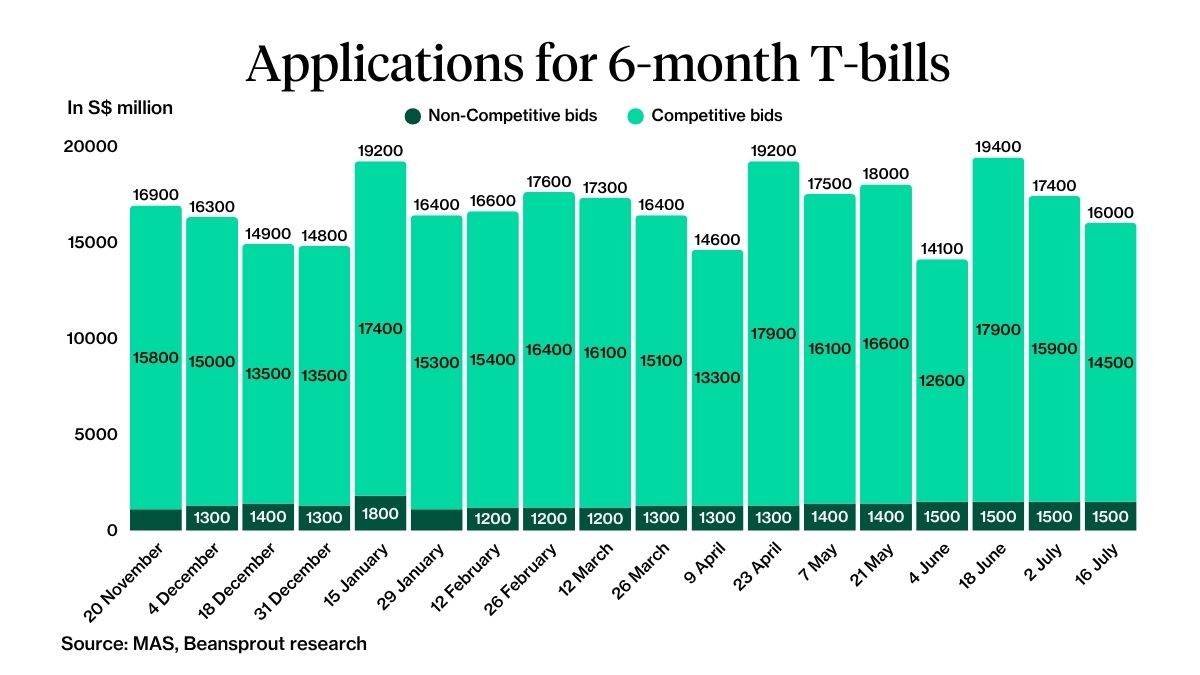

Total applications for the 6-month Singapore T-bill fell to S$16.0 billion in the latest auction on 16 July from S$17.4 billion in the T-bill auction on 2 July.

T-bill applications had previously reached S$19.4 billion in the auction on 18 June, the highest level recorded since the start of the year.

The amount of competitive bids fell to S$14.5 billion on 16 July from S$15.9 billion on 2 July.

If you placed a competitive bid below 1.55%, you would receive 100% of your requested T-bill allocation.

If you bid at exactly 1.55%, the allocation would be around 44%.

The amount of non-competitive bids remained at S$1.5 billion, unchanged from the previous T-bill auction on 2 July.

Since the amount of non-competitive bids was within the allocation limit, all eligible non-competitive bids received full allocation for the T-bill.

#2 - T-bills issued rose slightly

The amount of T-bills issued rose slightly to S$8.8 billion from S$8.7 billion in the previous T-bill auction on 2 July.

In fact, it would mark the highest levels of T-bill issuance since the start of the year, since the previous high in the T-bill auction on 2 July.

With applications falling as issuance increased, the ratio of applications to T-bills issued (bid-to-cover ratio) fell slightly to 1.82x from 2.00x in the previous T-bill auction on 2 July.

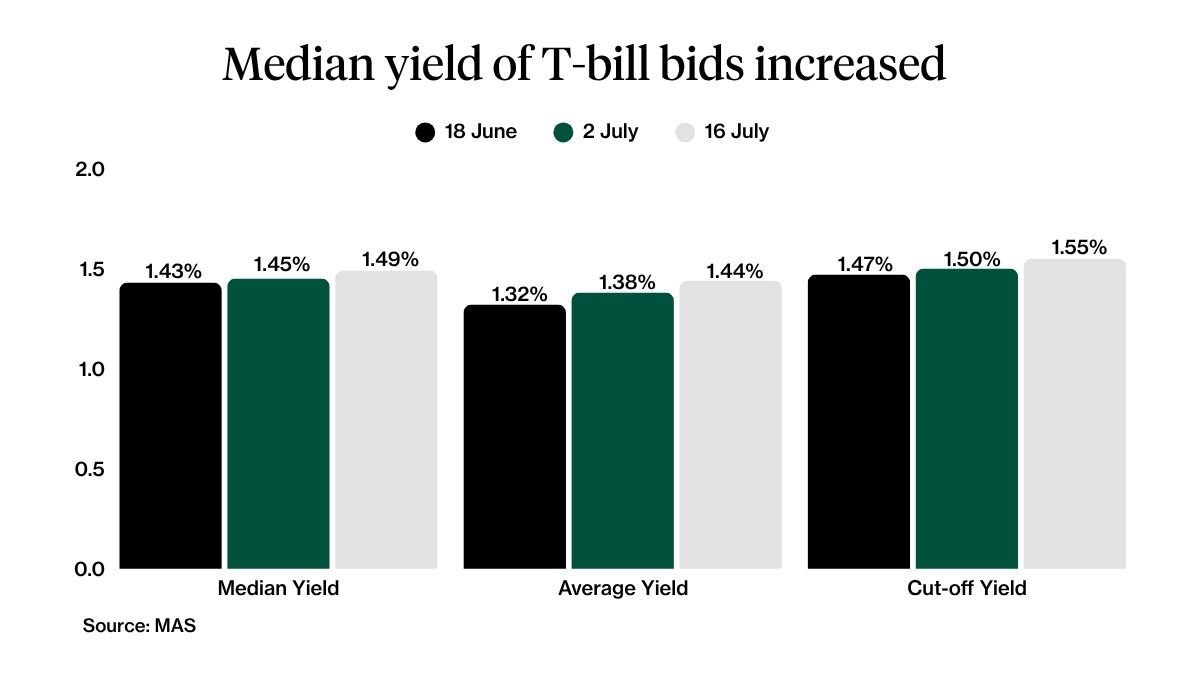

#3 - Median yield of bids submitted rose

The median yield of submitted bids rose to 1.49% from 1.45% in the previous T-bill auction on 2 July.

The average yield of submitted bids also rose to 1.44% from 1.38% in the previous auction.

The increase in both the median and average yields indicates that investors generally submitted bids at higher yields in the latest auction.

Given the median yield and the cut-off yield, this suggests that a substantial number of bids were placed in the 1.49% to 1.55% range, which is higher than the best 6-month fixed deposit rate in Singapore.

What would Beansprout do?

With the 6-month T-bill yield rising to 1.55% in the latest auction, it has become a more competitive option for parking short-term cash.

The higher cut-off yield reflected a combination of slightly weaker demand, a larger issuance size and investors submitting bids at higher yields in the latest auction.

The latest result may appeal to investors seeking higher short-term returns, although I would still compare the T-bill with other cash management options based on the returns and liquidity offered.

With the recent global geopolitical tensions, I have been reviewing my financial plan to make sure it gives me sufficient security and peace of mind.

The first step is to make sure I have sufficient cash put aside for emergency uses through my liquidity pot. Then, I would see how I can earn a higher yield on this pot of emergency cash, while maintaining the liquidity I may need. Learn more about the liquidity pot here.

The T-bill yield of 1.55% is higher than the current best 6-month fixed deposit rate of 1.50% p.a. and the best 3-month fixed deposit rate of 1.35% p.a.

However, investors who can set aside their cash for longer may still find a higher rate of 1.60% p.a. with a 12-month fixed deposit.

Another option to consider is the Singapore Savings Bonds (SSB), which offers a first-year return of 1.46% and average annual return of 2.06% over 10 years, while having the flexibility to redeem prior to maturity.

There are also some savings accounts in Singapore that offer an interest rate of above 1.55% p.a. which are also worth considering if you prefer to keep your cash more accessible.

By finding the best place to park my cash, I can build a stable Liquidity Pot that allows the rest of my portfolio to remain invested through market volatility without being forced to sell at the wrong time.

If you are looking for the best place to park your savings, we compare T-bills to fixed deposits, SSBs and savings accounts to find out how to allow our spare cash to work harder.

For a more structured way to organise your savings, investments and wealth, you can read our guide to the Four Pots of Wealth.

Do you prefer to park your cash in T-bills or fixed deposits? Share with us in the comments below or in our Telegram group!

Enjoyed this insight? Follow Beansprout on Telegram, Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments