Oil price surge driving divergence in Singapore stocks: Weekly Review with SIAS

Stocks

Powered by

By Gerald Wong, CFA • 23 Mar 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

We share about how the oil price jump is driving the share price performance of Singapore stocks in the latest Weekly Market Review.

What happened?

In this week's Weekly Market Review in partnership with Securities Investors Association Singapore (SIAS), we discuss key developments in the global equity market with the spike in oil prices, higher inflation expectations, and shifting interest rate outlook.

Watch the video to learn more about what we are looking out for this week.

Weekly Market Review

1:33 - Macro Update

- As we enter the fourth week of the Iran war, geopolitical volatility continues to drive significant uncertainty across global financial markets. Over the past week, US markets experienced a broad pullback, with the S&P 500, Nasdaq, and Dow Jones all falling by approximately 2%. STI remains relatively resilient compared to global peers.

- Oil prices remain a central focus and the primary indicator of investor sentiment. Prices have surged above $110 per barrel amidst concerns over whether oil transport through the Strait of Hormuz will be disrupted.

- Consequently, the narrative of higher for longer interest rates has returned. The Federal Reserve has officially increased its 2026 personal consumption expenditure inflation forecast to 2.7%, up from an earlier estimate of 2.4%. Markets are now pricing in zero rate cuts for the entirety of 2026, causing the US 10-year government bond yield to bounce back to 4.3%.

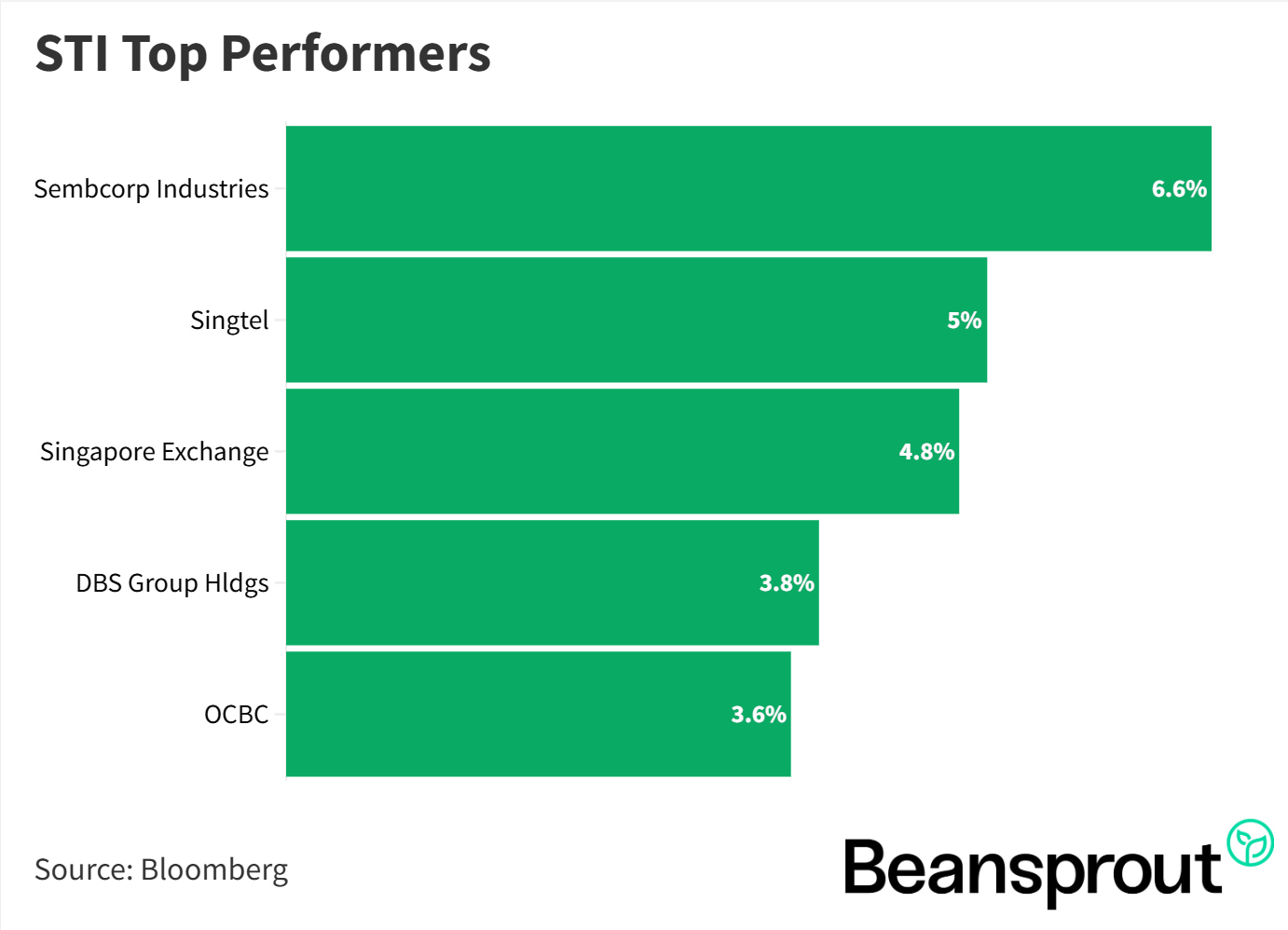

- Despite broader macroeconomic uncertainty, several Singapore stocks demonstrated resilience supported by strong bottom-up drivers. Sembcorp Industries, Singtel, and SGX stood out as key gainers for the week, while local banks like DBS and OCBC also ranked among the top performers, rallying approximately 4%.

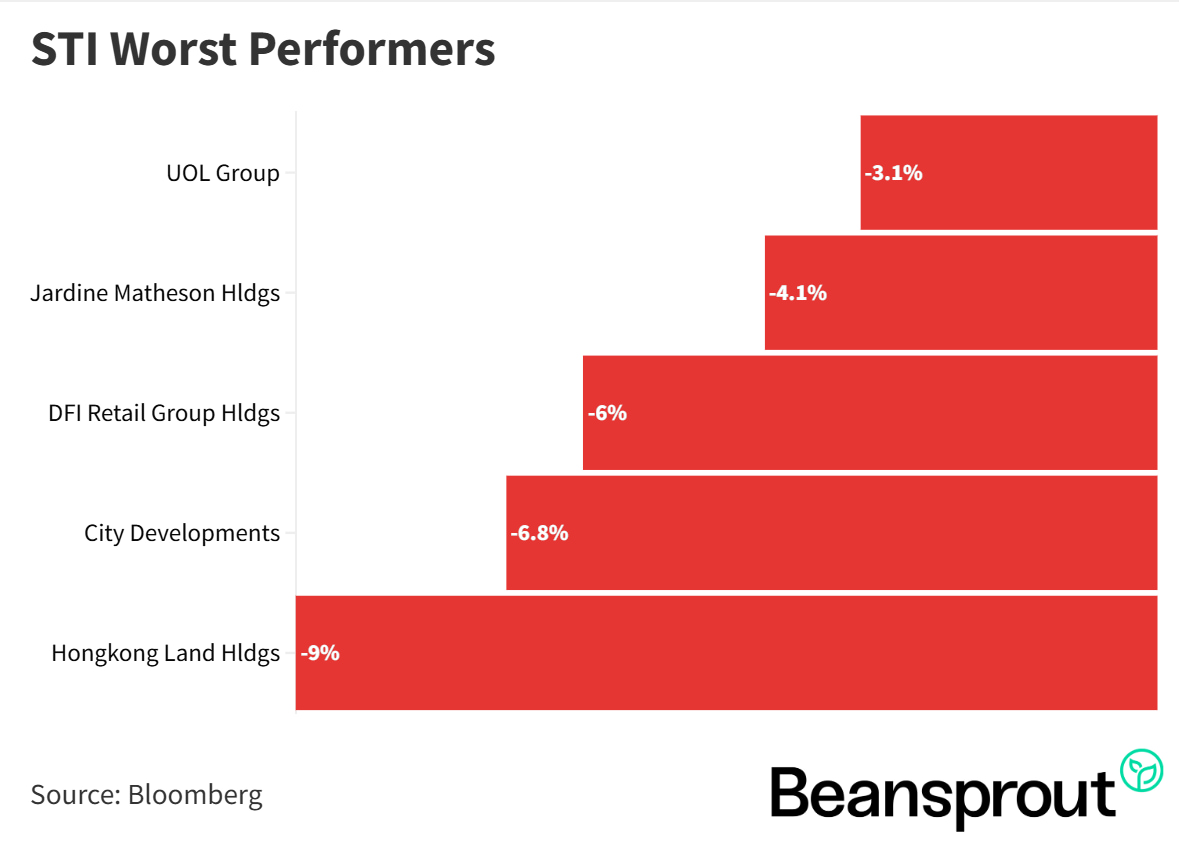

- Conversely, interest-rate-sensitive property stocks and transport names suffered. Property developers like Hongkong Land, City Developments, and UOL saw notable pullbacks, alongside Singapore Airlines which dropped due to fears that surging oil prices will impact its profitability.

STI Top Performers:

STI Worst Performers:

Oil price surge driving divergence in Singapore stocks

- The key macro concern in the market continues to be the situation around the Strait of Hormuz, which remains a critical shipping route for global oil supply.

- Investors are closely watching whether oil transport through this narrow strait could be disrupted, as any disruption may push energy prices even higher.

- With oil prices now above US$110 per barrel, markets are starting to react, and different sectors in Singapore are moving in different directions.

- Oil and gas related names have been relatively resilient, as higher oil prices may lead to increased spending in the offshore and marine sector.

- One example is Seatrium, which has held above S$2.20 per share in March and has shown strength compared to the broader market.

- Higher energy prices have also supported palm oil prices, which has led to renewed interest in plantation-related stocks.

- Wilmar International reached a new 52-week high above S$3.80, supported by stronger crude palm oil prices.

- On the other hand, transport stocks have come under pressure because higher fuel costs may affect profitability.

- Singapore Airlines was one of the names that declined in March, reflecting concerns about rising jet fuel prices.

Read also: Oil jumps above US$110. How Singapore blue chips may be impacted

Fed outlook shifts as inflation expectations rise

- The US Federal Reserve kept interest rates unchanged at the latest meeting, which was widely expected by the market.

- However, the Fed raised its forecast for PCE inflation in 2026 to 2.7%, compared to an earlier estimate of 2.4%, bringing inflation risks back into focus.

- Based on the CME FedWatch Tool, investors are now expecting no rate cuts for the rest of the year, compared to earlier expectations of at least one cut.

- This shift in expectations has pushed the US 10-year Treasury yield back up to around 4.3%, after falling below 4% earlier in the month.

Implications for the Singapore market

- The Straits Times Index (STI) recently reached new all-time highs above 5,000 points, supported partly by expectations of lower interest rates.

- If rate cuts are delayed, the tailwind from lower borrowing costs may pause, which could affect different sectors differently.

Banks may benefit if rate cuts are delayed

- Singapore banks could benefit if interest rates stay higher for longer, as this may support their net interest margins.

- There were signs of stabilisation in margins for UOB and OCBC in the fourth quarter of 2025.

- However, if interest rates remain high for too long and economic growth slows, there is a risk that non-performing loans could increase, which may hurt bank earnings.

REITs and property developers sensitive to bond yields

- REITs had started to recover in the second half of 2025 as interest rates declined, but that recovery is now showing signs of reversing as bond yields move higher again.

- Rising Singapore government bond yields increase financing costs, which tends to put pressure on REIT valuations.

- Property developers may also be affected, as earlier strong sales in late 2024 and 2025 were partly supported by lower mortgage rates.

- If borrowing costs stay elevated, buyer sentiment in the property market could weaken.

Read also: Fed warns inflation may rise. What it means for Singapore blue chip stocks

Technical Analysis

Straits Times Index

- The index is currently trading around 4,861 points after giving back gains from last week when it briefly crossed the 5,000 mark.

- Immediate technical support is located at the 4,790 point level established in late January.

- If current support fails, the index will likely slide toward the 4,700 level and remain in a broad range-bound consolidation.

- Downside pressure is being buffered by the heavy weighting of local banks and energy counters which are benefiting from the current macroeconomic environment.

Learn more about the Straits Times Index (STI) here.

Dow Jones Industrial Average

- The index has officially entered correction territory by dropping 10 percent from its mid-February high of 50,512 points.

- Immediate support rests near the 45,000 level but a break here could trigger a further slide toward the 43,340 support level established last July.

- Momentum is extremely weak as the RSI has broken below the 30-point oversold mark indicating the index is due for a potential technical rebound.

- The index has completely broken below its 200-day moving average confirming the severe downward momentum.

S&P 500

- The broad market index fell 7.5 percent from its late-January high of 7,002 points to current levels around 6,506 points.

- Key support is currently at the November low of 6,500 with a further downside target of 6,360 if Middle East tensions continue to escalate.

- Momentum is severely weakened as the RSI crossed into oversold territory with a highly bearish reading of 29 points.

- Similar to the Dow the index has broken below its 200-day moving average signaling a strong bearish trend.

Learn more about the S&P 500 index here.

Nasdaq Composite Index

- The tech-heavy index has dropped over 10 percent from its January high of 24,019 points to officially enter correction territory.

- The index broke its critical November support at 21,800 points opening the door for a test of the September low around the 21,000 handle.

- Unlike the other major indices the RSI has not yet reached the 30-point oversold level suggesting further downside is highly likely.

- A meaningful technical rebound is unlikely until the index touches the 21,000 level and indicators enter deeply oversold conditions.

What to look out for this week

Monday, 23 March 2026: Singapore Consumer Price Index (CPI) data

Tuesday, 24 March 2026: UOBAM Ping An FTSE ASEAN Dividend Index ETF ex-dividend

Thursday, 26 March 2026: Singapore Savings Bond (SSB) application closing date, LionGlobal Singapore Physical Gold ETF listing date

Friday, 27 March 2026: US PCE Price data

Get the full list of stocks with upcoming dividends here.

Follow us on Telegram, Youtube, Facebook and Instagram to get the latest financial insights.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments