3 Singapore blue chip dividend stocks yielding above 4% in June 2026. What to watch before buying for income

Stocks

By Ng Hui Min • 20 Jun 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

We look at 3 Singapore blue chip dividend stocks yielding above 4% in June 2026, and whether their payouts appear sustainable for income investors.

What happened?

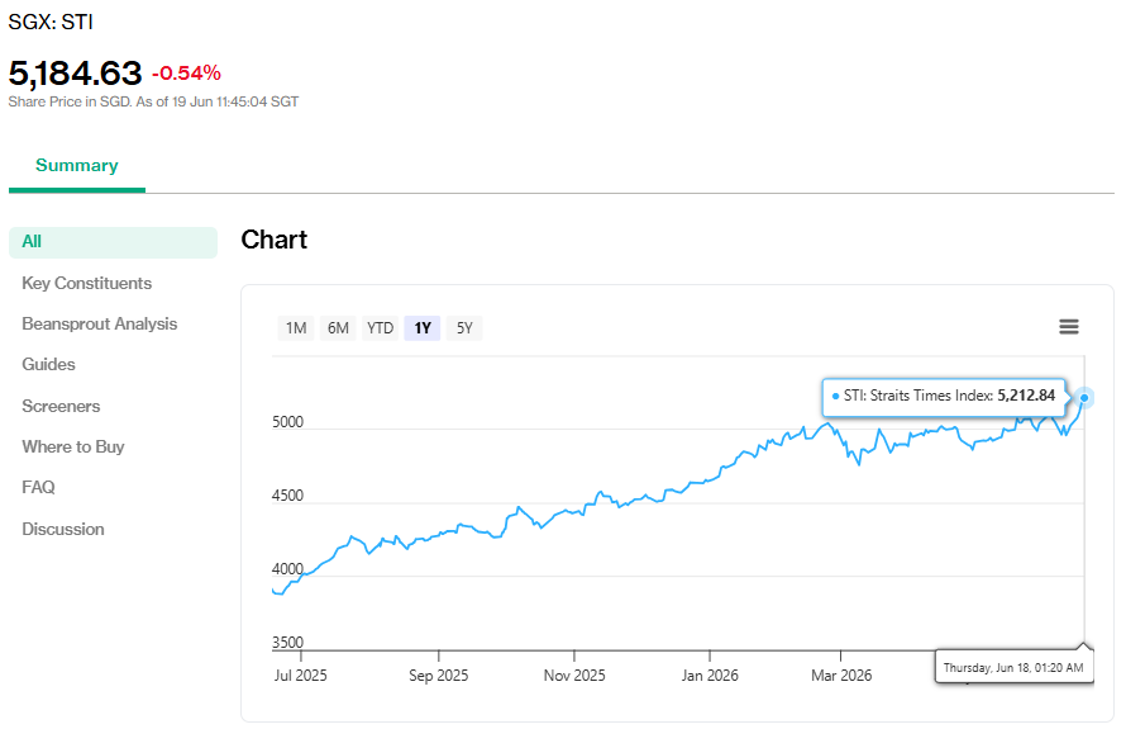

The Straits Times Index (STI) reached another all-time high of 5,212.84 on 18 June 2026.

However, not every blue chip and dividend stock has kept pace with the rally. Some names have lagged the rally, which have pushed their dividend yields higher.

Earlier, we looked at why investors should look beyond Singapore REITs to blue chip stocks for income, especially as quality dividend stocks may offer more resilient payouts across market cycles.

We also analysed the 3 best-performing Singapore blue chip stocks in May 2026, where names like DBS and SATS rallied on earnings momentum.

Last month, we also looked at three Singapore blue chip stocks with forward yields above 6%.

Since then, we have seen questions from the Beansprout community on whether there are blue chips with dividend yields above 4% worth considering.

In this article, we look at whether SIA, StarHub and CapitaLand Investment offer a genuine income opportunity, or if their higher yields reflect concerns about weaker earnings ahead.

3 Singapore blue chip dividend stocks yielding above 4% in June 2026

#1 - SIA (SGX: C6L)

Singapore Airlines, or SIA, is Singapore’s national carrier. The Group operates the full-service Singapore Airlines brand and low-cost carrier Scoot, serving 135 destinations across 35 countries as at June 2026.

Recent operating data remains healthy.

In May 2026, SIA Group’s passenger traffic rose 4.9% year-on-year, while capacity increased 5.3%.

Passenger load factor stood at 86.0%, with Singapore Airlines at 84.6% and Scoot at 91.2%. Scoot also launched passenger services to Belitung, Indonesia during the month.

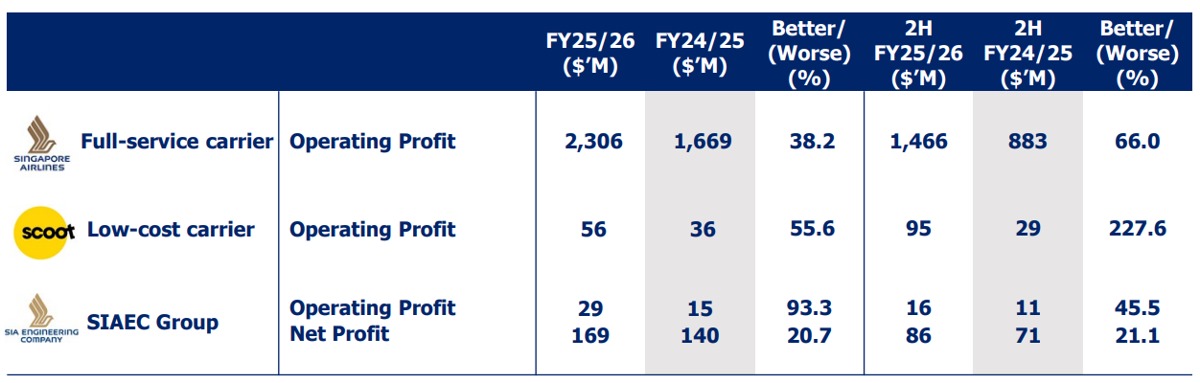

For the financial year ended 31 March 2026, SIA delivered a strong operating performance.

Revenue rose 5.0% year-on-year to a record S$20.5 billion, while SIA and Scoot carried a record 42.4 million passengers, up 7.7% from the previous year. Passenger load factor also improved to 87.7%.

Operating profit increased 39% to a record S$2.4 billion, supported by healthy travel demand, higher yields and lower net fuel costs.

However, net profit fell 57.4% to S$1.18 billion. This was mainly because the previous year included a large one-off gain from the Air India-Vistara merger, which did not repeat.

SIA also began recognising Air India’s full-year losses, which weighed on reported earnings.

From a dividend perspective, SIA has several positives.

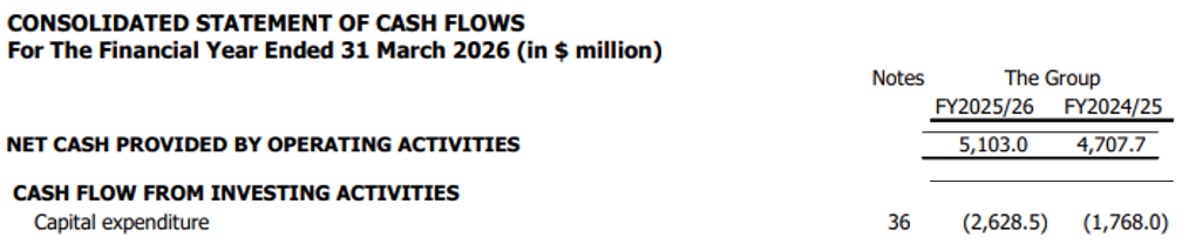

Free cash flow, which is operating cash flow minus capex, remains positive. This means the company is still generating cash after paying for major spending needs such as aircraft and other investments.

However, SIA has guided for capex to increase over the next two financial years as it continues with fleet renewal.

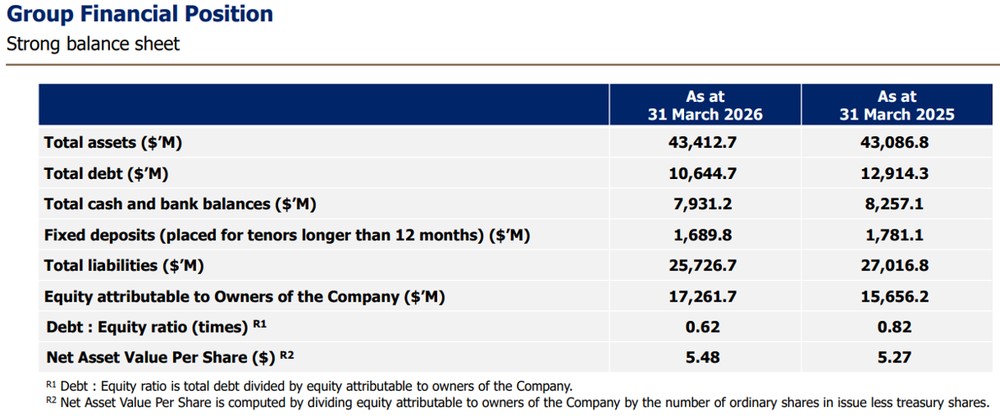

Its balance sheet also looks relatively strong compared with many other airlines.

Total debt fell from S$12.9 billion to S$10.6 billion, while net debt-to-equity stood at about 0.16 times. This gives SIA more financial flexibility to support dividends through the cycle.

SIA declared total FY2025/26 dividends of 37 cents per share, comprising ordinary dividends of 27 cents and special dividends of 10 cents. The payout ratio was around 70.7% based on ordinary dividends, and about 96.9% if special dividends are included.

The board has also committed to paying special dividends of 10 cents per share in FY2026/27 and FY2027/28, providing some near-term dividend visibility.

Based on Factset’s consensus FY2026/27 dividend per share of S$0.304, SIA offers a forward dividend yield of about 4.2% based on 17 Jun closing price of S$7.21.

However, investors should remember that airlines are cyclical businesses. SIA remains exposed to fuel prices, travel demand, geopolitical disruptions and the performance of Air India. Fleet renewal also means capex will remain a recurring requirement.

Overall, SIA offers an attractive yield and strong near-term dividend visibility, but it is not a defensive income stock. Investors considering SIA for dividends should be comfortable with earnings volatility and the risks that come with the airline cycle.

Find out how much dividends you would have received as a unitholder of SIA in the past 12 months with the calculator below.

Related links:

#2 - StarHub (SGX: CC3)

StarHub is one of Singapore’s three main telcos, offering mobile, broadband, entertainment, enterprise connectivity and cybersecurity services.

Telco services are generally recurring in nature. Consumers and businesses are unlikely to stop using mobile or broadband services even when economic conditions weaken. This gives StarHub a relatively stable revenue base.

We recently spoke with StarHub CEO Nikhil Eapen on staying the dividend course through headwinds.

Singapore’s mobile market remains highly competitive. Low-cost mobile plans continue to put pressure on average revenue per user, weighing on StarHub’s consumer business.

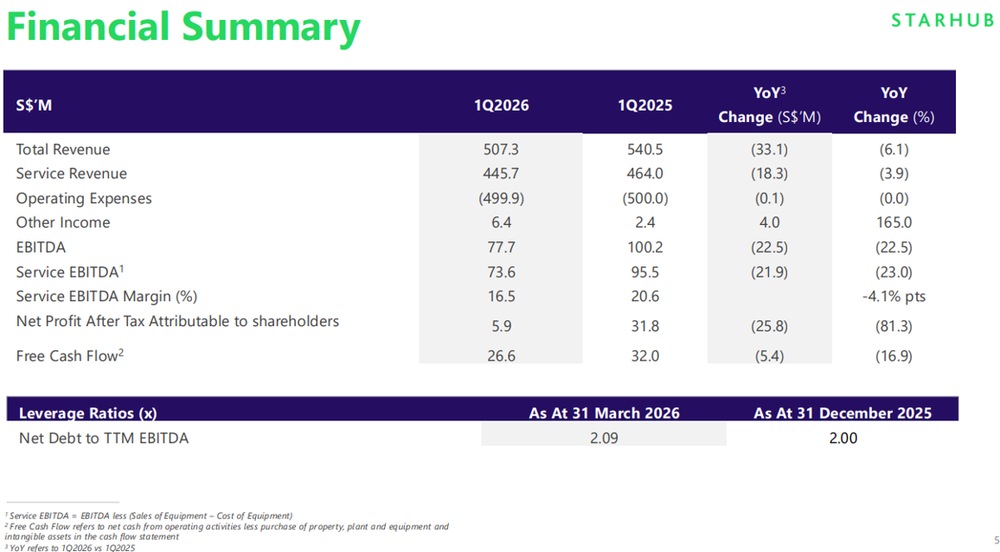

StarHub’s 1Q2026 results reflected these challenges.

Service revenue fell 3.9% year-on-year to S$445.7 million, with declines across consumer mobile, broadband and entertainment.

Earnings Before Interest, Taxes, Depreciation and Amortisation (EBITDA) fell 22.5% to S$77.7 million, while net profit attributable to shareholders dropped 81.3% to S$5.9 million. This was due to lower gross profit, higher depreciation and higher finance costs.

The enterprise business was mixed.

Cybersecurity revenue from Ensign grew 22.4% year-on-year (YoY), and StarHub’s regional enterprise orderbook rose by more than 50%.

However, managed services revenue declined due to project timing, which dragged overall enterprise revenue lower.

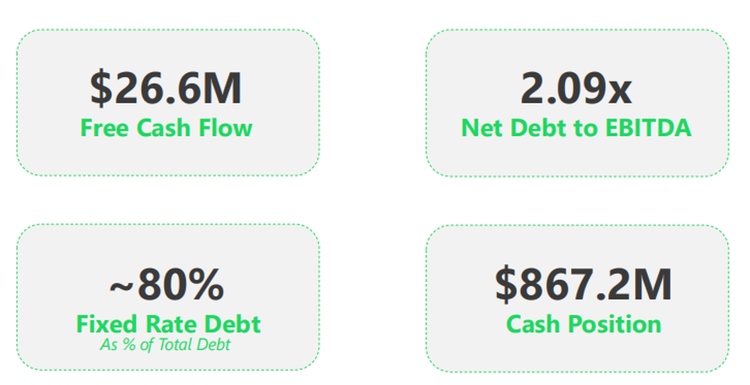

On free cash flow, StarHub generated S$26.6 million in 1Q2026.

For FY2025, underlying free cash flow was S$163 million, excluding the one-off S$188 million spectrum payment, which would have been negative otherwise.

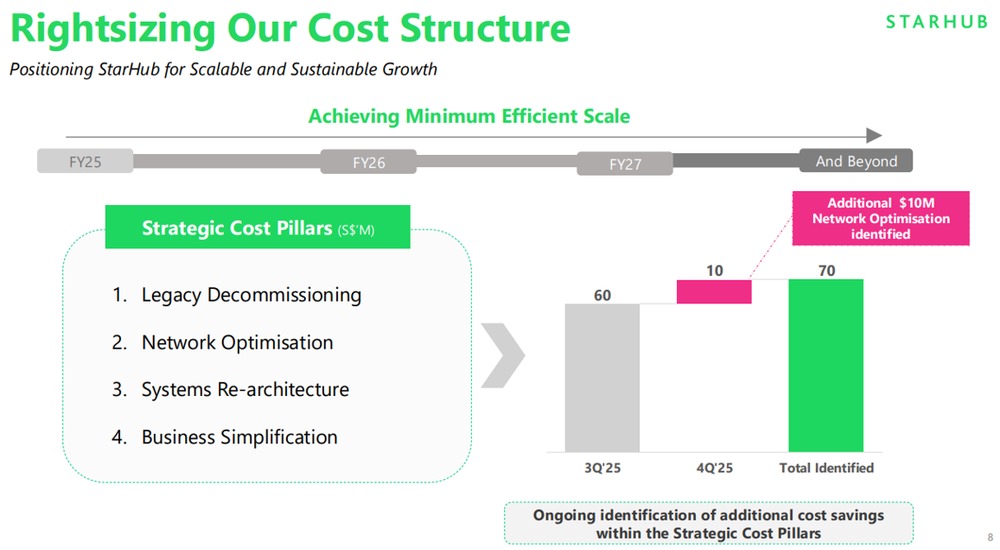

Management expects positive free cash flow trends to resume in FY2026, supported by its cost optimisation programme, which targets S$60 million to S$70 million in savings through 2028.

StarHub has also taken steps to strengthen its balance sheet.

In April 2026, the Group sold a 16.81% stake in Ensign for S$121 million in cash proceeds, while retaining a 38.92% stake. Its net debt to equity stands at 1.6 times as of 31 Dec 2025.

From a dividend perspective, StarHub has paid dividends for 19 consecutive years.

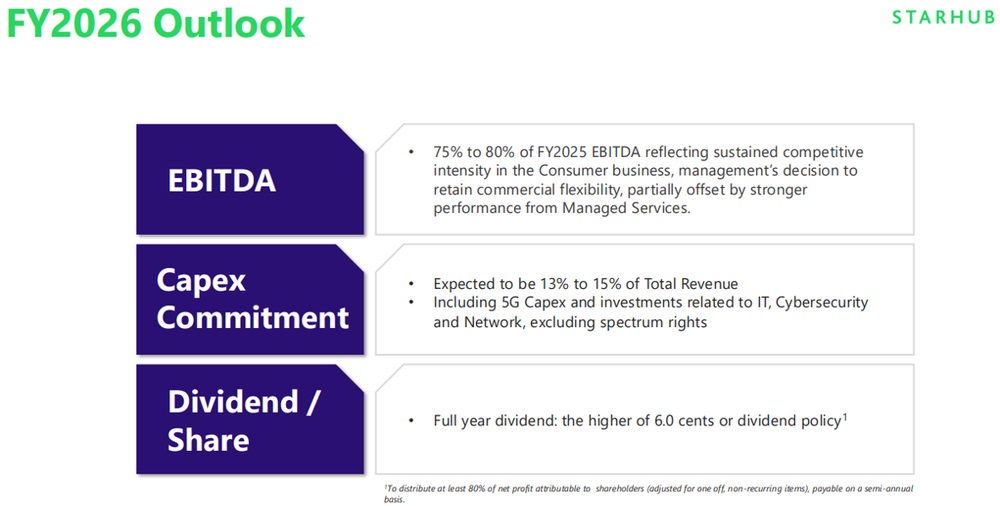

However, dividends have been declining, from 7.2 cents per share in FY2024 to 6.2 cents in FY2025, with consensus expecting around 6.0 cents in FY2026.

Based on StarHub’s closing price of S$1.05 on 17 June 2026, this translates into a forward dividend yield of about 5.7%.

The key concern is dividend sustainability.

StarHub’s payout ratio based on reported earnings was above 100% in FY2025, at around 133%. This means dividends exceeded reported net profit.

However, free cash flow coverage looks more reassuring, as underlying free cash flow remained positive.

Overall, StarHub offers an attractive dividend yield and a recurring telco business model. However, earnings are under pressure, and dividends have been reduced over the past two years.

We would want to see EBITDA margins stabilise and the enterprise orderbook convert into recognised revenue before gaining more confidence in StarHub’s dividend outlook.

Find out how much dividends you would have received as a unitholder of StarHub in the past 12 months with the calculator below.

Related links:

- StarHub latest valuation, share price and analysis

- StarHub dividend history and forecast

- kopi-C with StarHub CEO: Staying the dividend course through headwinds

#3 - CapitaLand Investment (SGX: 9CI)

CapitaLand Investment, or CLI, is a global real asset manager with S$125 billion in funds under management as at end-2025.

The Group manages eight listed REITs and a wide range of private real estate funds across sectors such as retail, logistics, data centres, lodging and credit.

CapitaLand Investment is shifting from owning properties on its balance sheet to a more fee-based, asset-light model.

This means earning recurring income from fund management, commercial management and lodging management, rather than relying mainly on property ownership or development gains.

The Group has set a target to grow its funds under management to S$200 billion by 2028.

CapitaLand Investment’s latest results show a mixed picture.

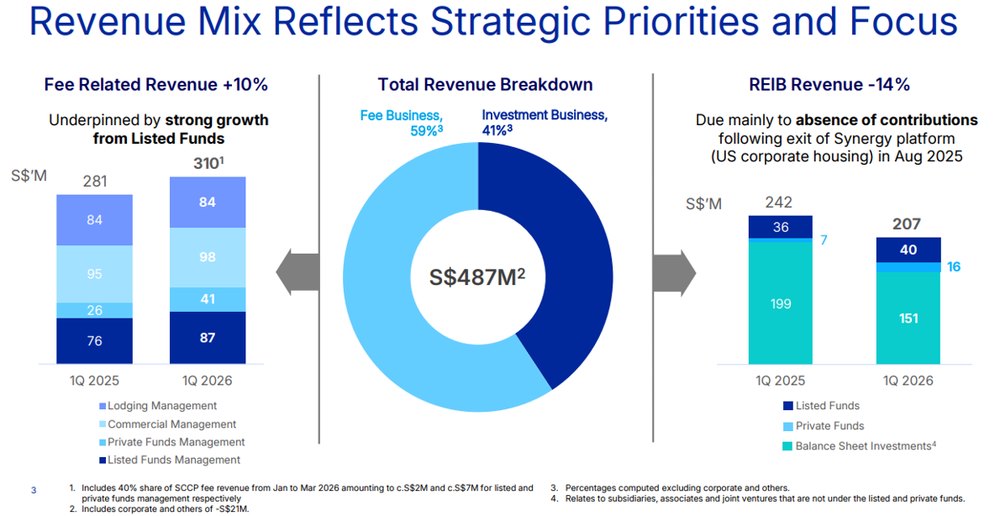

In 1Q2026, fee-related revenue grew 10% year-on-year to S$310 million, supported by its listed funds and private funds platform.

However, total revenue fell 2% to S$487 million, as revenue from the real estate investment business declined following asset divestments.

For FY2025, operating Profit After Tax and Minority Interest (PATMI) rose 6% to S$539 million. This is the better measure of underlying earnings, as it strips out more volatile revaluation items.

Reported PATMI, however, fell 70% to S$145 million, mainly due to revaluation losses from CapitaLand Investment’s China portfolio. This remains the key risk, as China property weakness can continue to create volatility in reported earnings.

On the positive side, CapitaLand Investment continues to recycle capital actively.

It won a S$2.4 billion real estate mandate from Income Insurance, raised S$2.5 billion in fund equity year-to-date, deployed S$7.2 billion and divested S$3.4 billion.

This reinforces CapitaLand Investment’s shift towards becoming a capital-light real asset manager.

From a dividend perspective, CapitaLand Investment’s asset-light model is a positive.

Fund management businesses generally require less capex and can generate more recurring fee income over time.

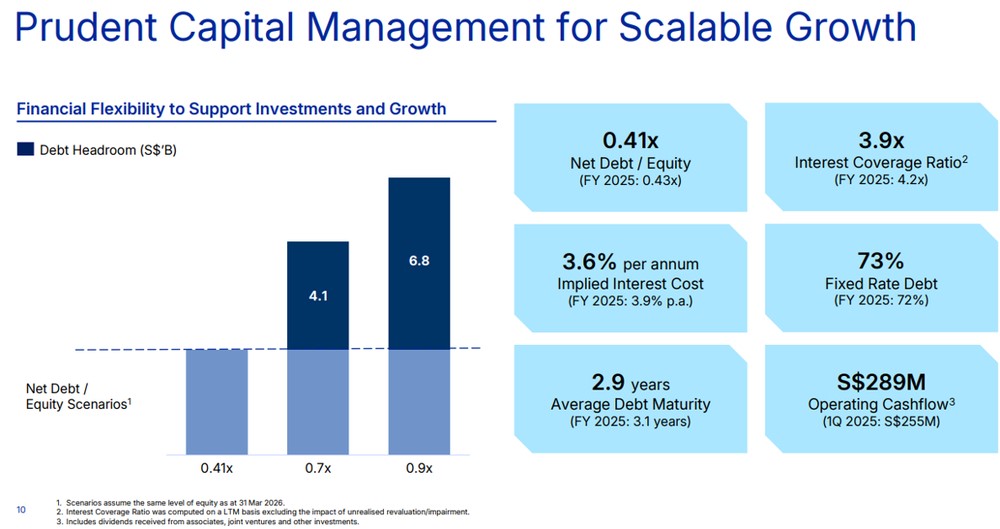

As of 31-Mar-26, free cash flow coverage of the dividend is close to 1 time, and should improve if the fee business continues to scale.

Net gearing stood at 0.41 times, with around S$4.1 billion of debt headroom before reaching 0.7 times.

CapitaLand Investment’s dividend track record is also its clearest strength.

The Group has maintained its dividend at 12 cents per share every year since FY2021, despite COVID recovery, higher interest rates and China revaluation losses.

Consensus also expects dividends to remain at 12 cents per share in FY2026.

At a share price of around S$2.58 based on 17 June 2026 closing, this translates to a forward dividend yield of about 4.7%.

Overall, CLI looks like the most dependable income stock among the three. Its fee business is growing, its Fund Under Management (FUM) target provides a clear longer-term growth path, and the dividend has been maintained through a challenging real estate cycle.

Investors still need to be patient with China-related revaluation risks, but the underlying income stream looks relatively resilient.

Find out how much dividends you would have received as a unitholder of CapitaLand Investment in the past 12 months with the calculator below.

Related links:

- CapitaLand Investment latest valuation, share price and analysis

- CapitaLand Investment dividend history and forecast

- Interview with Ervin Yeo from CapitaLand Investment: Why some malls thrive and others don't? What investors should look out for

What would Beansprout do?

If I am investing in a stock for dividend, I would not look at yield alone.

I would also check whether the company has healthy free cash flow, a stable business, a consistent dividend track record, and a yield that is meaningfully above the risk-free rate.

Among the three, CapitaLand Investment looks like the most dependable income stock to me.

Its yield of around 4.7% is not the highest, but its dividend has been steady at 12 cents per share since FY2021.

Its shift towards a fee-based, asset-light real asset management model could also support more recurring income over time. Learn more about CapitaLand Investment Limited here.

SIA offers a forward dividend yield of about 4.2% and better near-term dividend visibility, supported by committed special dividends for FY2026/27 and FY2027/28.

However, it remains a cyclical dividend stock, with earnings exposed to travel demand, fuel prices, geopolitical risks and higher aircraft capex. Learn more about SIA here.

StarHub offers the highest yield at about 5.7%, but also carries more dividend risk.

Earnings are under pressure, dividends have been reduced over the past two years, and its reported earnings payout ratio is above 100%. Learn more about StarHub here.

| Stock | Forward Yield | The Good | Key Risks |

| SIA (SGX: C6L) | ~4.2% |

|

|

| StarHub (SGX: CC3) | ~5.7% |

|

|

| CapitaLand Investment (SGX: 9CI) | ~4.7% |

|

|

Overall, CapitaLand Investment would be our preferred pick for dividend consistency.

SIA may suit investors comfortable with cyclical risk, while StarHub requires more caution until earnings and margins stabilise.

I would focus less on the highest yield and more on whether the payout is supported by recurring earnings, healthy cash flow and a balance sheet that can withstand tougher periods. Find out how to build a more dependable stream of income that can hold up across cycles here.

If you’d like to screen for other Singapore stocks with attractive dividend yields and potential upside, you can explore our Singapore high dividend stocks screener.

Which Singapore dividend blue chip stocks are you watching as the STI reaches new highs? Share your thoughts in the comments below or join the discussion in our Telegram group!

Planning to invest in Singapore stocks? Compare the best Singapore brokers to find the right trading platform, and see the latest promotions and sign-up rewards available.

Follow Beansprout on YouTube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments