3 best-performing Singapore blue chip stocks in May 2026

Stocks

By Ng Hui Min • 03 Jun 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

We look at the top three Singapore blue chip stocks in May which saw gains of about 8% or more, and what investors should watch after the rally.

What happened?

Singapore blue chips continued to climb in May 2026.

After rebounding in April, the broader market has stayed resilient, but the rally has not been evenly spread across every large-cap stock.

Earlier, we looked at DBS and OCBC hit record highs.

At the same time, we saw Singtel share price fall after record dividend and examined what to look out for as Keppel’s M1-Simba deal falls through.

Investor interest has also moved beyond traditional dividend blue chips, with Singapore tech stocks rallying on the AI boom.

This suggests that the Singapore market has been shaped by several different themes, from AI and data centres to Singapore’s rise as a wealth hub.

In this article, we examine the 3 best-performing Singapore blue chip stocks in May 2026, and whether their latest results, business momentum and dividend outlook are strong enough to support the rally.

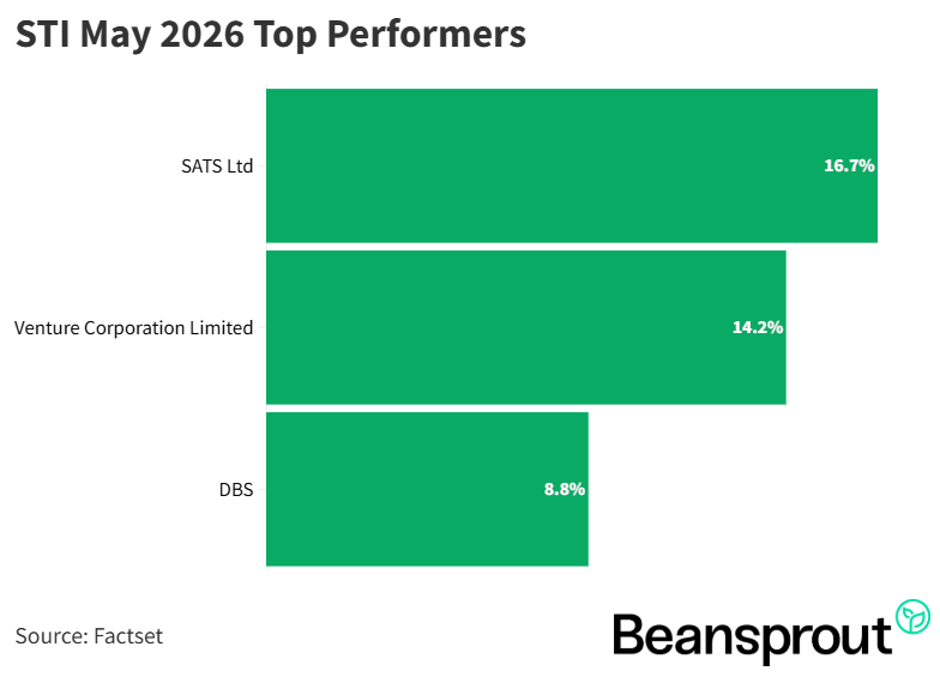

3 best-performing Singapore blue chip stocks in May 2026

#1 - SATS Ltd (SGX: S58)

SATS is a global aviation services company that provides air cargo handling, ground handling and food solutions across major travel and trade hubs.

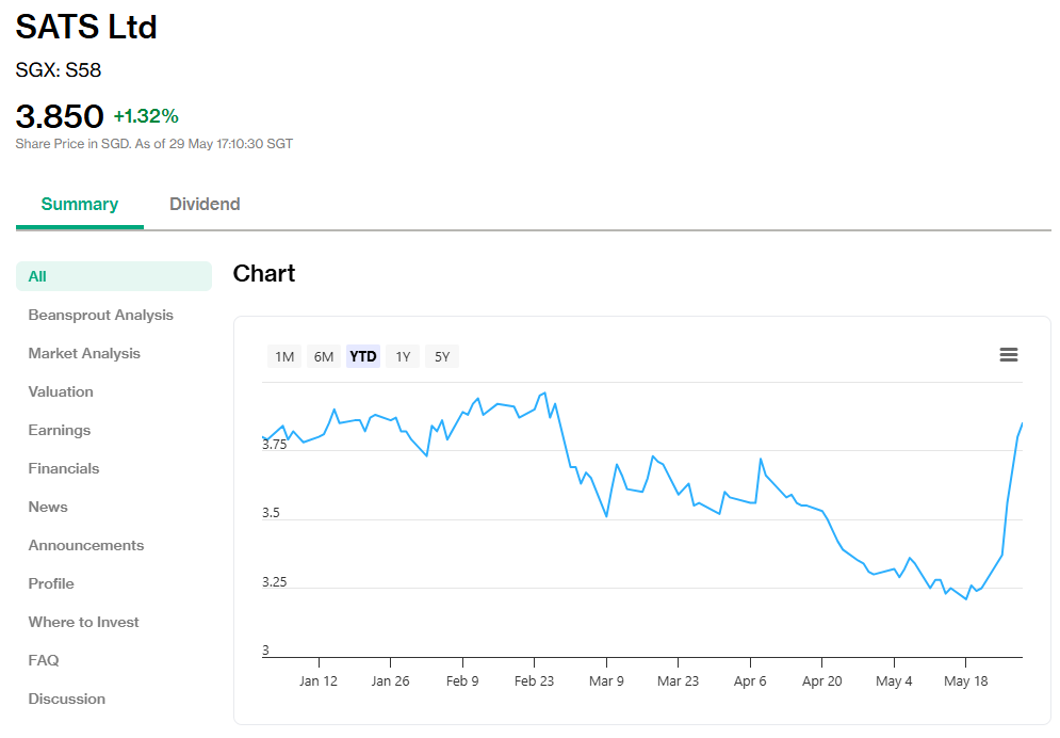

As of 31 May 2026, SATS closed at S$3.85, with its total return rising by about 16.7% in May. This brought SATS close to its five-year high.

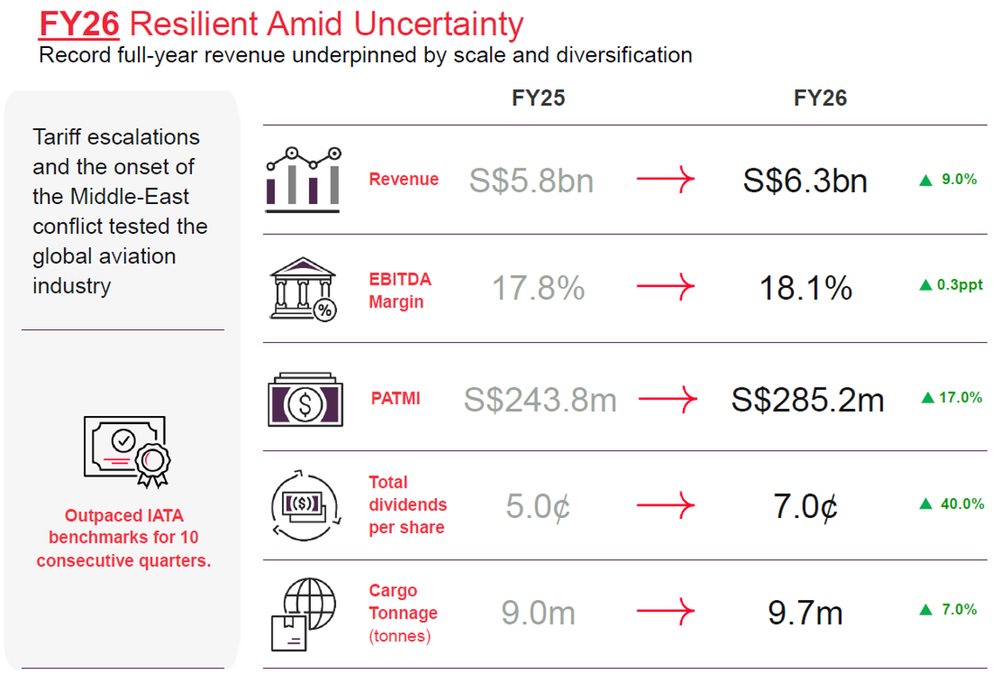

The rally came after SATS reported a stronger set of FY2026 results, showing that its recovery has continued despite disruptions in global aviation and trade flows.

For FY2026, SATS reported record revenue of S$6.35 billion, up 9.0% year on year. EBITDA (Earnings Before Interest, Taxes, Depreciation and Amortisation) rose 10.6% to S$1.15 billion, while profit attributable to shareholders increased 17.0% to S$285.2 million.

The improvement was supported by growth across its enlarged aviation services platform. Gateway Services revenue rose 10.8% to S$4.95 billion, while Food Solutions revenue grew 2.9% to S$1.39 billion.

Profitability also improved, with operating profit rising 14.2% to S$543.3 million. Operating profit margin expanded from 8.2% to 8.6%, reflecting better operating leverage.

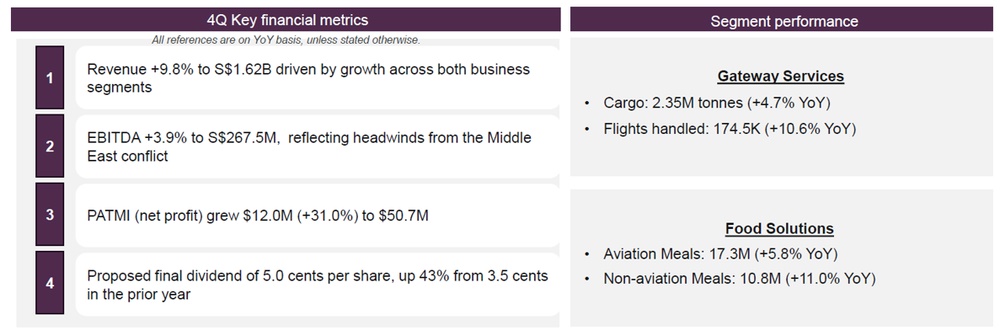

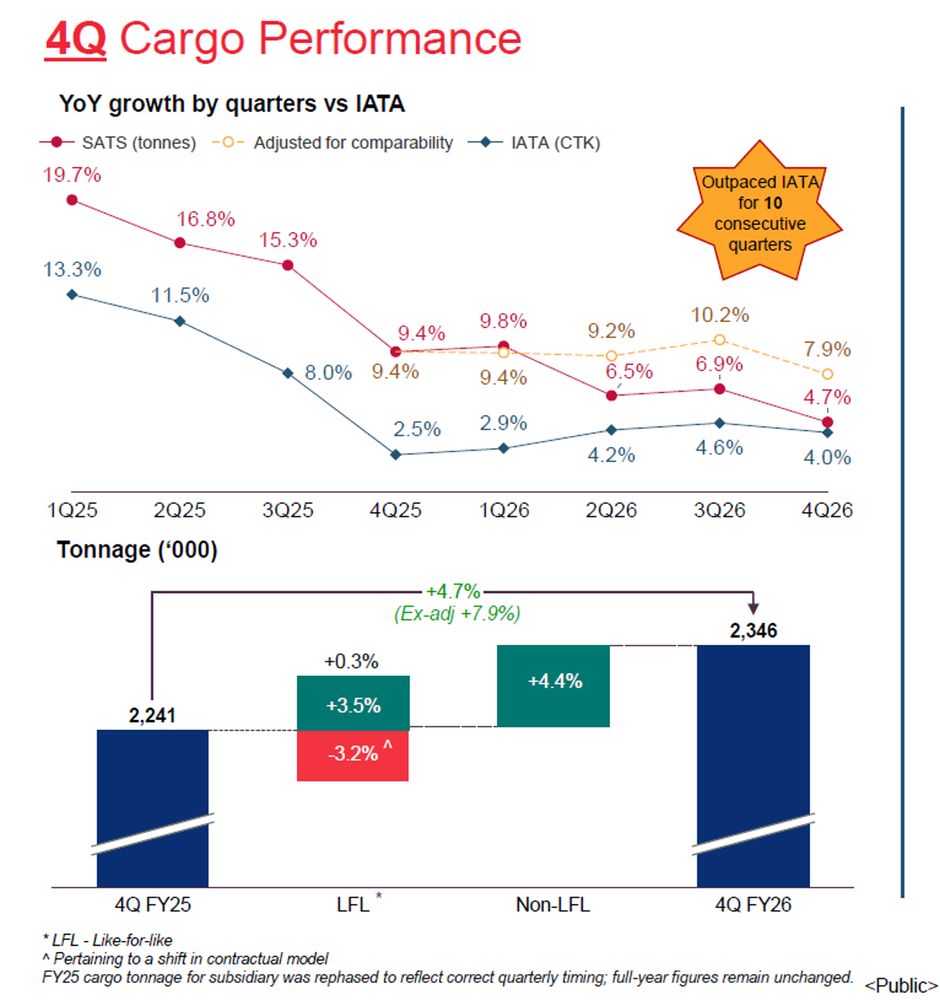

In the fourth quarter, revenue rose 9.8% year on year to S$1.62 billion, while PATMI (Profit After Tax and Minority Interests) grew 31.0% to S$50.7 million. Cargo volume increased 4.7%, flights handled rose 10.6%, aviation meals grew 5.8%, and non-aviation meals increased 11.0%.

Cargo remained the strongest part of SATS’ recovery story.

SATS’ cargo volumes outperformed IATA’s global benchmarks for the 10th consecutive quarter, with growth supported by both organic demand and new wins across its global network.

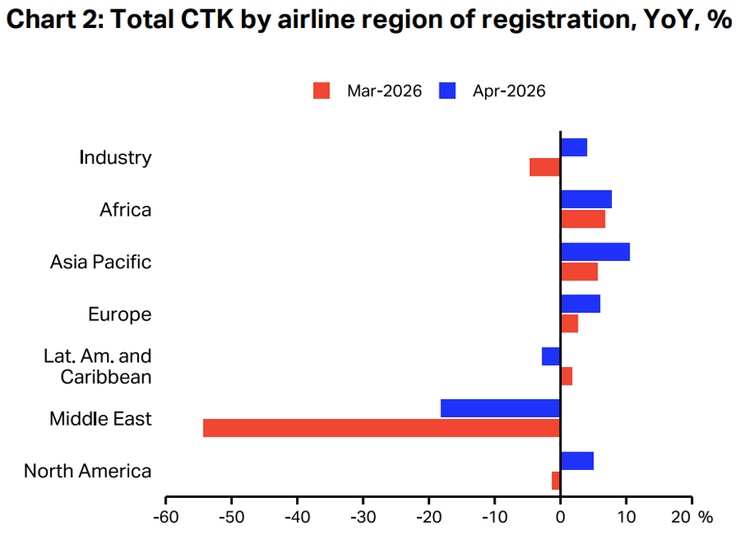

The latest IATA air cargo data points to a more supportive backdrop for SATS.

Global air cargo demand rose 4.0% year-on-year in April 2026, even as capacity declined slightly. More importantly, Asia was the bright spot. Asia-Pacific airlines saw cargo demand grow 10.5% year-on-year, the strongest among all regions.

This matters for SATS because its gateway services and cargo handling businesses are closely tied to air traffic and trade flows through Asia. Key routes also remained resilient, with Europe-Asia cargo demand up 16.2%, intra-Asia up 13.0%, and Asia-North America up 8.3%.

Source: IATA Sustainability and Economics, IATA Information and Data - Monthly Statistics. Data as of 28 May 2026

The higher dividend also signalled that the earnings recovery is starting to translate into better shareholder returns.

SATS proposed a final dividend of 5.0 cents per share, bringing the total full-year dividend to 7.0 cents per share, a 40% increase from the previous year.

Based on SATS’ share price of S$3.85 as of 29 May 2026, the full-year dividend of 7.0 cents would translate to a dividend yield of about 1.8%.

However, the operating environment remains uncertain.

SATS noted that tariff escalations, trade policy shifts and the Middle East conflict had created headwinds, while disrupted flight capacity across Gulf hubs affected traffic flows between Asia, Europe and the Americas.

Still, its global platform may give it more flexibility to capture rerouted cargo flows.

Following the acquisition of Worldwide Flight Services (WFS), the combined SATS and WFS network operates over 225 stations in 27 countries, covering trade routes responsible for more than 50% of global air cargo volume.

For SATS, the key question is whether its enlarged global aviation services platform can continue scaling profitably after the WFS acquisition.

The FY2026 results were encouraging, with record revenue, stronger margins, higher profit and a bigger dividend.

However, I would still watch whether tariff uncertainty, Middle East disruptions and higher input costs affect cargo volumes and profitability in the coming quarters.

Find out how much dividends you would have received as a shareholder of SATS in the past 12 months with the calculator below.

Related links:

#2 - Venture Corporation Limited (SGX: V03)

Venture Corporation is a Singapore-listed technology solutions provider serving customers across areas such as life sciences, medtech, test and measurement, networking and semiconductor-related equipment.

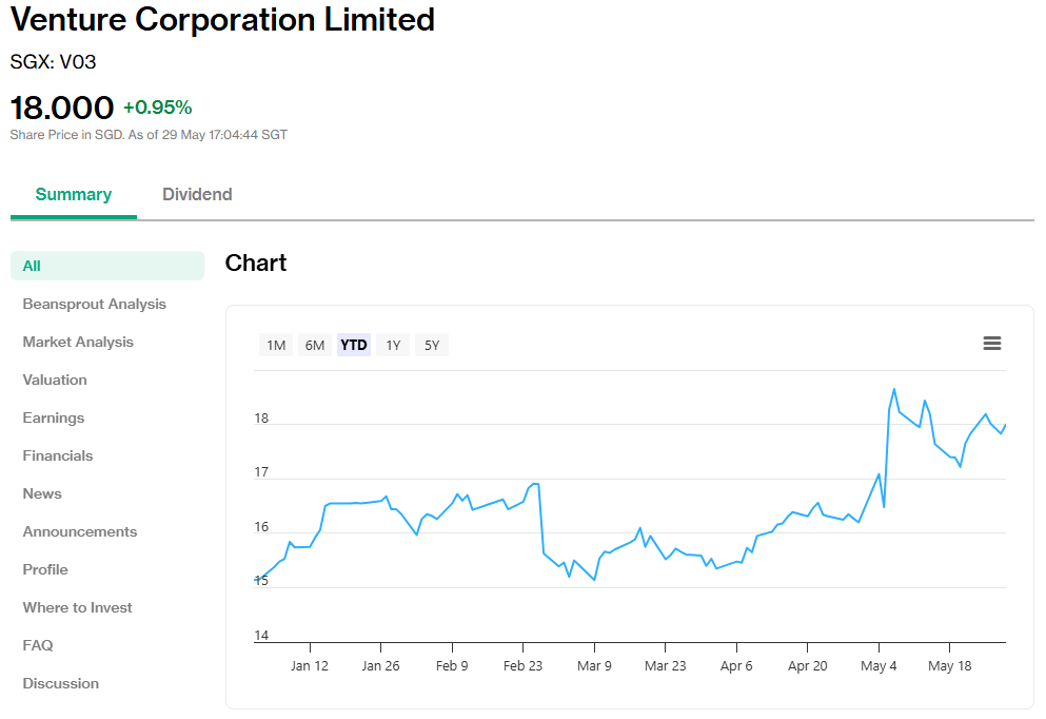

As of 31 May 2026, the stock closed at S$18.00, with its total return rising by about 14.2% in May. This brought Venture closer to its five-year high.

Venture’s share price recovery reflected improving investor confidence in a possible turnaround in technology demand.

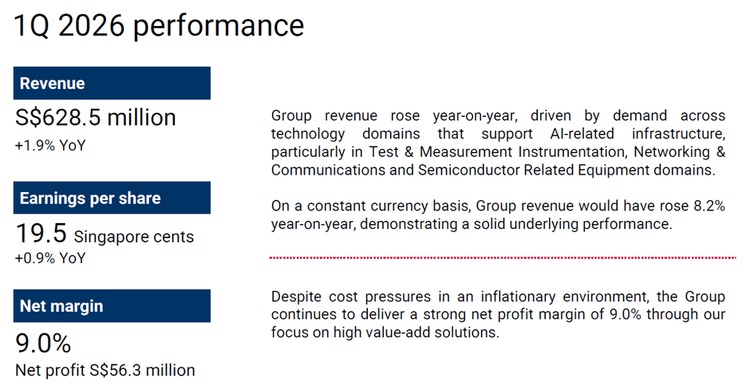

For 1Q2026, Venture reported revenue of S$628.5 million, up 1.9% year on year. On a constant currency basis, revenue would have risen 8.2% year on year.

Net profit came in at S$56.3 million, while earnings per share rose 0.9% to 19.5 Singapore cents.

The headline growth may appear modest, but the revenue mix showed signs of improvement.

Revenue growth was driven by demand across technology domains that support AI-related infrastructure, particularly test and measurement instrumentation, networking and communications, and semiconductor-related equipment.

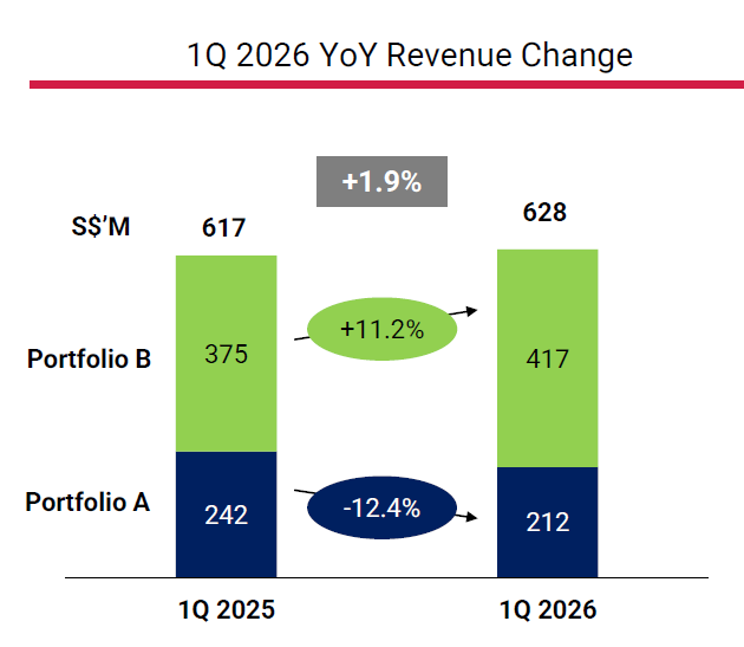

This shift was visible in the performance of its two business portfolios.

Portfolio B, which includes several technology domains linked to AI infrastructure and semiconductors, saw revenue rise 11.2% year on year to S$417 million.

That helped offset weakness in Portfolio A.

Revenue from Portfolio A fell 12.4% to S$212 million, mainly due to lower volumes in the lifestyle consumer domain.

Profitability remained resilient despite the uneven demand environment.

Venture maintained a net profit margin of 9.0%, supported by its focus on higher value-add solutions.

Its balance sheet gives the group room to navigate the cycle.

Venture maintained a net cash position of more than S$1 billion as at 31 March 2026, even after higher dividend payments and share buybacks in 2025.

Working capital also rose to S$868.3 million, as the group increased inventory to support business growth and supply chain resilience.

Venture’s management described the 1Q2026 improvement as a turnaround and said its R&D labs are gaining traction in hyperscale data centres and life science domains.

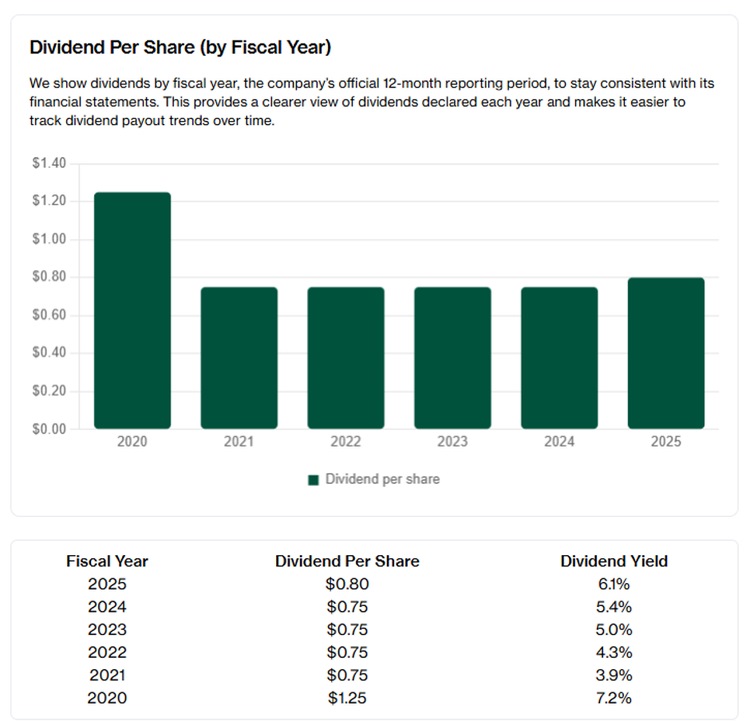

The company’s dividend track record may also have supported investor interest.

Based on Venture’s FY2025 dividend of S$0.80 per share and share price of S$18.00 as of 29 May 2026, this would imply a trailing dividend yield of about 4.4%.

However, I would view Venture as more of a recovery stock than a confirmed growth compounder at this stage.

The next few quarters will be important in showing whether the improvement in Portfolio B can continue, and whether demand can broaden beyond selected technology domains.

Find out how much dividends you would have received as a shareholder of Venture Corporation in the past 12 months with the calculator below.

Related links:

- Venture Corporation latest valuation, share price and analysis

- Venture Corporation dividend history and dividend forecast

#3 - DBS (SGX: D05)

DBS is Singapore’s largest bank, with businesses across consumer banking, wealth management, institutional banking and treasury markets.

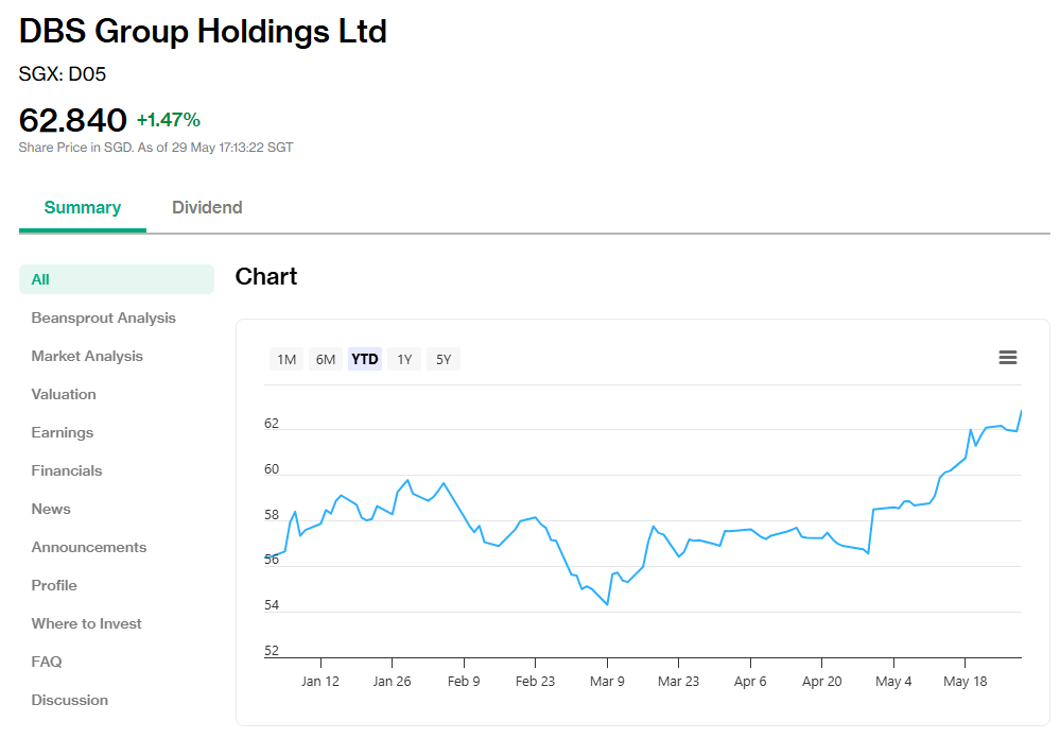

As of 31 May 2026, DBS closed at S$62.84, with its total return, including dividends, rising by about 8.8% in May. This took DBS to a new all-time high.

The gains built on DBS’ resilient 1Q2026 results, where stronger fee income helped offset pressure from lower interest rates.

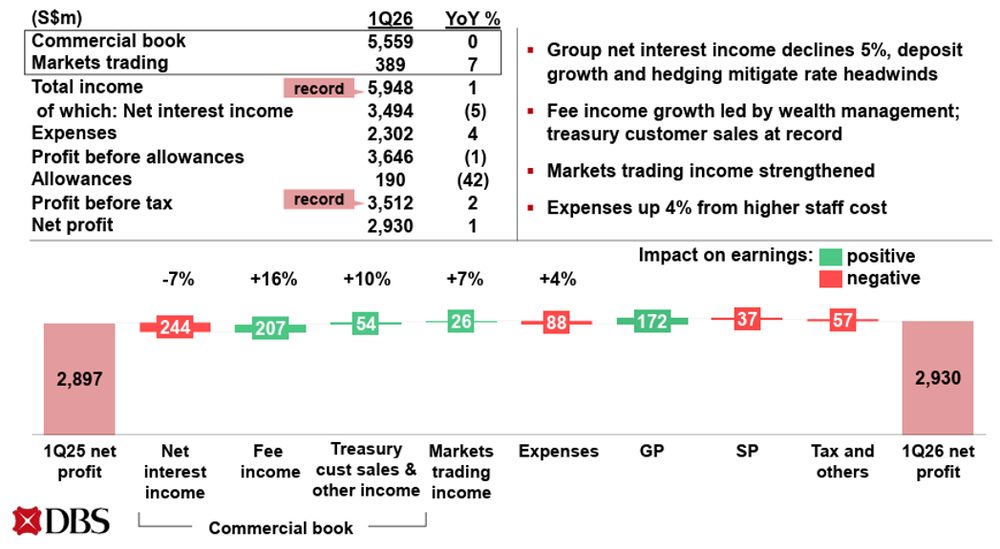

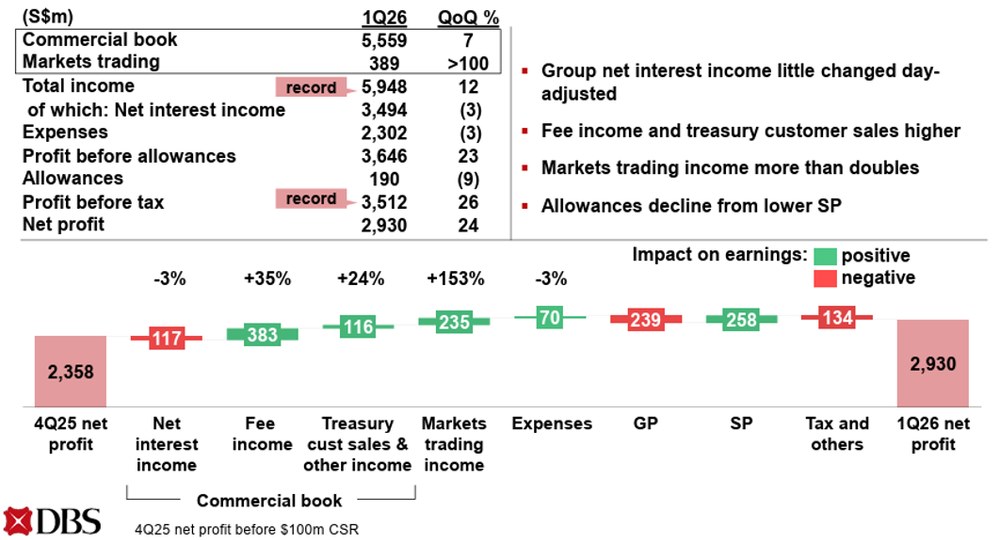

DBS reported net profit of S$2.93 billion in 1Q2026, up 1% year on year and 24% quarter on quarter. Total income reached a new high of S$5.95 billion, while return on equity stood at 17.0%.

The bank is still facing rate headwinds.

Group net interest income declined 5% year on year to S$3.49 billion, while net interest margin narrowed 23 basis points to 1.89%.

However, the impact was partly cushioned by hedging activities, balance sheet growth and stronger deposit momentum.

What stood out most was the strength of DBS’ wealth management and fee income.

Commercial book net fee income rose 16% year on year and 35% quarter on quarter to a record S$1.48 billion.

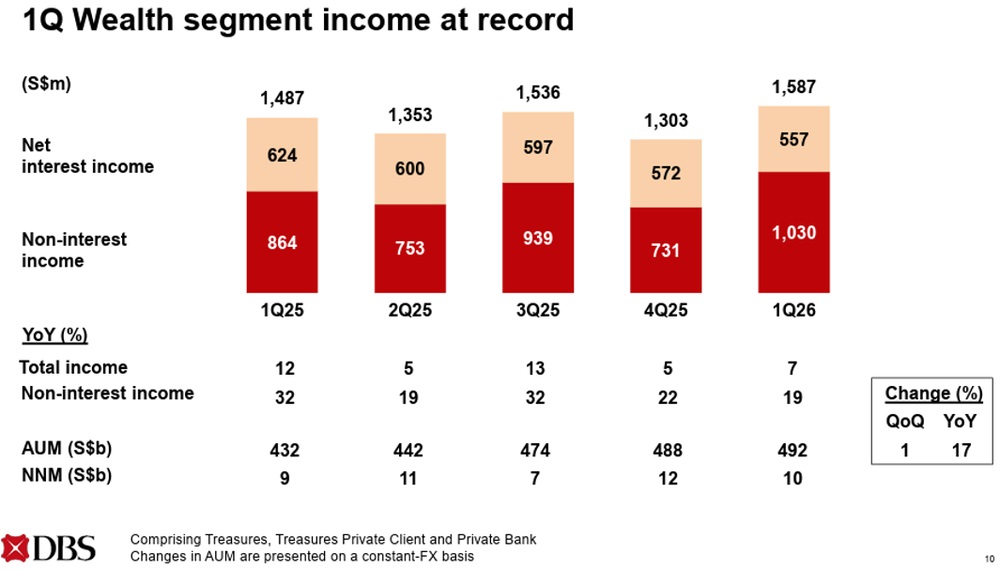

Wealth management fees reached a record S$907 million, driven by higher investment product sales and bancassurance.

This makes DBS less dependent on interest rates alone, a theme we discussed in our earlier article on how wealth management income could provide a larger earnings buffer as net interest income comes under pressure.

Its wealth segment total income reached S$1.59 billion, with assets under management at S$492 billion.

Credit quality also remained steady.

DBS’ non-performing loan ratio stayed at 1.0%, while specific allowances eased to S$157 million, or 14 basis points of loans.

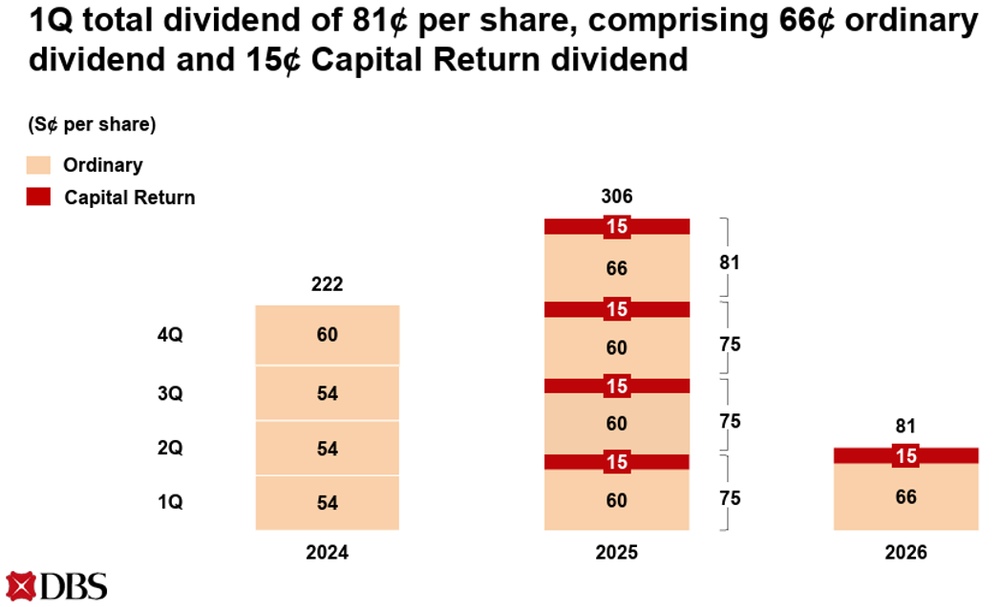

Dividends continue to anchor the DBS investment case for income-focused investors.

DBS declared an ordinary dividend of 66 cents per share and a capital return dividend of 15 cents per share for 1Q2026, bringing the quarterly payout to 81 cents per share. This works out to S$3.24 per share on an annualised basis.

Based on DBS’ share price of S$62.84 as of 29 May 2026, the annualised dividend would imply a dividend yield of about 5.2%.

In our earlier comparison of DBS, OCBC and UOB, DBS stood out for income visibility because the planned capital return dividend of 15 cents per quarter is expected to continue through FY2026 and FY2027.

For DBS, the focus is on whether earnings can stay resilient as interest rates decline.

Its dividend visibility, wealth management momentum and high-quality franchise remain attractive.

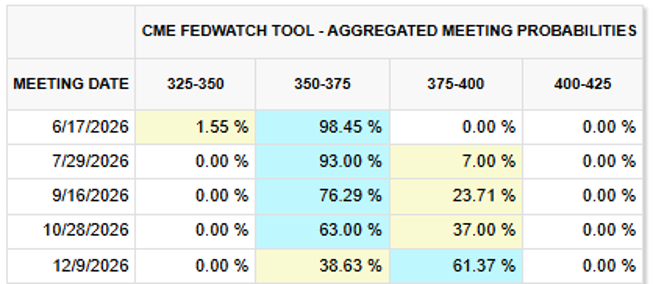

At the same time, expectations for a possible Fed rate hike towards the end of the year could provide support for bank margins if rates stay higher for longer.

In addition, DBS’ AI-driven initiatives could also help improve productivity and customer engagement, potentially supporting a higher ROE over time.

However, after the share price reached an all-time high, valuation has become a bigger consideration, and I would watch whether fee income growth can continue to offset net interest margin pressure.

Find out how much dividends you would have received as a shareholder of DBS in the past 12 months with the calculator below.

Related links:

- DBS latest valuation, share price and analysis

- DBS dividend history and dividend forecast

- DBS profit rises 1% and declares S$0.81 in total dividends in 1Q26: Our Quick Take

- DBS and OCBC hit record highs. How wealth management could support bank dividends

What would Beansprout do?

The strong performance of SATS, DBS and Venture in May shows that Singapore blue chips can still deliver meaningful gains, but the reasons behind the rally were different.

SATS remains a recovery and operating leverage story, supported by stronger air cargo demand. IATA data showed global air cargo demand up 4.0% year-on-year in April 2026, with Asia-Pacific the bright spot at 10.5% growth, though tariff uncertainty, Middle East disruptions and higher input costs remain key risks. Learn more about SATS here.

DBS remains the standout for income, supported by strong wealth management momentum and dividend visibility through FY2027. Rate hikes and AI-driven productivity gains could offer upside, but with the stock at an all-time high, I would add more gradually and watch whether fee income can keep offsetting NIM (Net Interest Margin) pressure. Learn more about DBS here.

Venture looks the most speculative of the three. While early signs of a tech demand recovery are encouraging, especially in AI infrastructure and semiconductor equipment, Portfolio A remains weak and overall growth is still modest. I would want to see a few more consistent quarters before calling this a confirmed upturn. Learn more about Venture here.

Overall, I would assess these stocks based on the role I want them to play in my portfolio, and not simply because they were the best-performing blue chips in May.

For income, DBS still stands out, though I would build positions gradually after the rally. Its dividend visibility remains attractive, but valuation matters more now that the share price has reached an all-time high.

For growth and recovery, I would fall back on Beansprout’s 4-factor Opportunity framework of investability, profitability, earnings growth quality and balance sheet strength.

SATS and Venture may be worth watching as they offer exposure to themes we like in Singapore. SATS benefits from aviation recovery and Singapore’s role as a regional hub, while Venture could ride the AI, data centre and semiconductor equipment cycle.

More broadly, I would look for Singapore stocks aligned with structural themes such as energy security, AI and data centres, the local infrastructure boom, and Singapore’s growth as a wealth hub.

Both SATS and Venture still come with cyclical risks, so I would want to see earnings growth backed by strong fundamentals before adding aggressively.

| Stock | The good | Key risks |

| SATS | ● Record FY2026 revenue of S$6.35 billion, with PATMI up 17.0% to S$285.2 million ● Cargo volumes outperformed IATA’s global benchmarks for the 10th consecutive quarter ● Full-year dividend rose 40% to 7.0 cents per share, with forward dividend yield of about 1.8% | ● Cargo demand remains exposed to tariff uncertainty and global trade disruptions ● Middle East conflict has disrupted traffic flows and raised input cost pressures ● Higher capex and facility expansion may affect free cash flow in the near term |

| Venture | ● 1Q2026 revenue rose 1.9% year on year, or 8.2% on a constant currency basis ● Portfolio B revenue grew 11.2%, supported by AI-related infrastructure demand ● Strong balance sheet, with net cash above S$1 billion and forward dividend yield of about 4.4% | ● Overall revenue growth remains modest, so the recovery is still at an early stage ● Portfolio A revenue fell 12.4% due to weaker lifestyle consumer volumes ● Investors need to watch whether demand broadens beyond selected technology domains |

| DBS | ● 1Q2026 net profit rose 1% year on year to S$2.93 billion, while total income reached a record S$5.95 billion ● Wealth management and fee income provide a stronger earnings buffer as interest rates decline ● Highest forward dividend yield among the three at about 5.2% | ● Net interest income remains under pressure from lower interest rates ● Valuation has become more demanding after the rally ● Future upside depends on whether fee income and wealth management growth can continue offsetting NIM pressure |

There may also be other avenues to capture structural growth in the Singapore market, including companies linked to infrastructure, data centres, energy security and regional expansion.

If you are looking for more Singapore stock ideas linked to long-term growth themes, you can explore our high-conviction curated stock opportunities here.

You can also screen for stocks that meet Beansprout’s 4-factor Opportunity framework here.

If you prefer broad exposure to blue chips without picking individual names, you can also learn more about the Straits Times Index (STI).

Is there a Singapore blue chip stock you are looking out for? Share with us in the comments below or in our Telegram group!

Planning to invest in Singapore blue chip stocks? Check out Beansprout's guide to the best stock trading platforms in Singapore with the latest promotions to invest in the Singapore market and see the latest promotions and sign-up rewards available.

Enjoyed this insight? Follow Beansprout on Telegram, Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments