Why I’m looking beyond Singapore REITs to blue chip stocks for income

REITs

By Gerald Wong, CFA • 24 May 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

We compare Singapore REITs and blue chip stocks, and explain why a broader mix may help investors build more resilient income.

What happened?

Singapore real estate investment trusts (S-REITs) have long been popular with investors looking for passive income.

After the recent pullback in Singapore REITs, many readers in the Beansprout Telegram community started asking whether the sector had become attractive again.

That is a fair question. Lower share prices have pushed up dividend yields to 6% for some Singapore blue chip REITs which are trading near their 5-year lows.

This was why I previously examined whether Singapore REITs could be a buying opportunity, as rising interest rates and bond yields weighed on the sector.

At the same time, we saw DBS and OCBC near all-time highs after their recent earnings and also offering attractive dividend yields.

This naturally raises a broader question: should investors continue to rely on REITs as the main source of portfolio income?

In this article, I examine if REITs should still be the main source of portfolio income, and why high-quality dividend stocks such as Singapore blue chips may offer a more sustainable alternative over the long term.

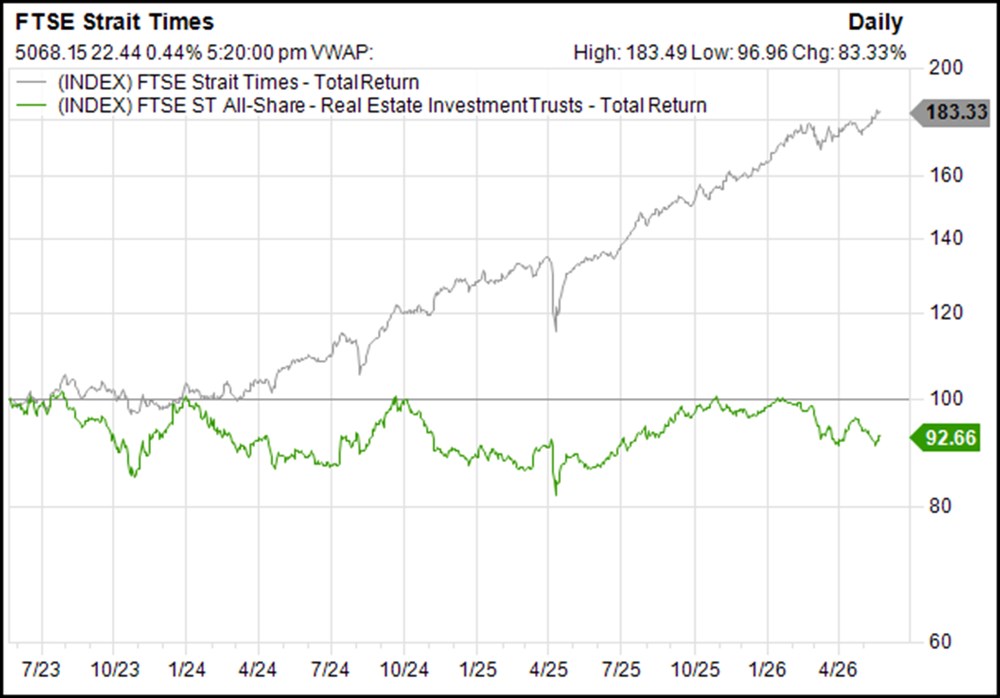

Singapore REITs have lagged blue chips stocks

We think it is important to look beyond headline yield alone.

While REITs can still play a role in an income portfolio, relying too heavily on them may leave investors more exposed to higher interest rates, debt risk, unit dilution, and weaker distribution growth.

Recent market performance highlights this clearly. Singapore blue chip stocks such as DBS, OCBC and Singtel have been key drivers of STI returns in recent years, helped by stronger share price performance and rising dividends.

By contrast, while Singapore REIT have continued to provide income, they have generally underperformed the broader market over recent multi-year periods.

This was especially evident in 2025, when the STI delivered a total return of 26.7% including dividends, compared with 14.4% for S-REITs.

To us, this reinforces a simple point that building sustainable income is not just about chasing the highest yield today.

It is also about owning businesses that can protect their payouts, grow earnings over time, and stay resilient across different interest rates and economic cycles.

That is why we have been diversifying more and leaning towards high-quality dividend stocks as the foundation of a long-term income portfolio.

Past performance is not indicative of future performance.

Why I am looking beyond Singapore REITs to blue chip stocks for sustainable income

#1 - Singapore REITs tend to have higher debt levels

While REITs are often valued for their attractive distribution yields, investors should also be mindful of their reliance on debt.

REITs borrow to acquire and own property assets, and many already operate with relatively high gearing levels. This can become a greater risk when market conditions weaken.

When interest rates rise, REITs may face higher borrowing costs when refinancing maturing debt.

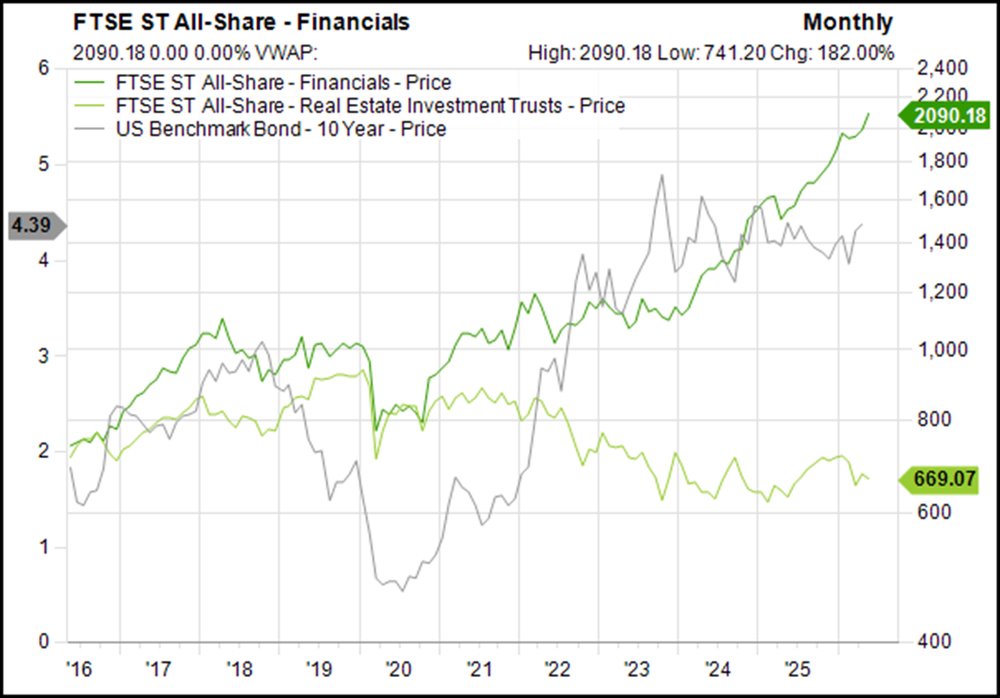

We have seen this in the past month, as higher bond yields made REIT yields look less attractive by comparison and weighed on the sector performance.

On the other hand, some Singapore blue chip stocks may be less vulnerable to interest rate swings than REITs.

This is especially so for Singapore blue chip stocks in a net cash position, such as Venture. Several other blue chip stocks also have relatively low debt levels, such as Singtel, as they have been focused on more active capital management.

That makes them less directly exposed to rising funding costs than REITs.

Also, falling property valuations can push gearing ratios higher. To strengthen their balance sheets, some REITs may need to raise equity through new unit issuances or sell assets at less favourable prices.

These measures can put pressure on distributions and dilute existing unitholders.

#2 - REITs have less flexibility to retain cash and reinvest

REITs are required to pay out most of their taxable income to unitholders. This helps support yield in the short term, but it also leaves them with less cash to reinvest.

That can make it harder for REITs to fund new growth, strengthen the balance sheet or reduce debt when conditions become more difficult.

Dividend-paying companies like banks have more flexibility. They can keep part of their profits and use that money to grow the business, improve operations or strengthen their finances.

At the same time, they can continue to provide shareholders with reliable and consistent dividends.

This ability to balance growth, financial resilience, and shareholder rewards makes dividend stocks a more durable and adaptable source of income compared with REITs.

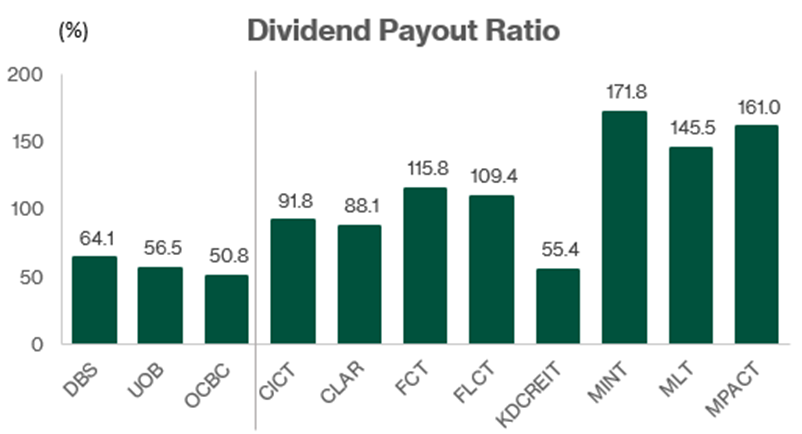

Fiscal year-ends differ across S-REITs: FCT and FLCT have a 30 September 2025 year-end; MINT, MLT and MPACT have a 31 March 2026 year-end; all others have a 31 December 2025 year-end.

#3 - REITs may be concentrated in one property segment

Many REITs are concentrated in a specific property segment, such as retail, office, or logistics, and some are also focused on a single market.

This means their income can be more sensitive to weakness in one sector or city. For example, softer retail sales or lower office occupancy in a key market can have a direct impact on distributions.

A case in point is Frasers Centrepoint Trust (FCT). Its portfolio comprises nine suburban retail malls in Singapore.

While its focus on necessity-based malls has supported relatively stable performance over the years, the REIT remains closely tied to the health of Singapore’s retail property market and consumer spending trends.

If retail conditions deteriorate meaningfully, rental income growth and distributions could come under pressure.

By contrast, Singapore blue chip stocks may have more diversified revenue streams across different products, services, and markets.

For example, Singapore banks such as DBS, OCBC and UOB generate income from lending, wealth management, payment processing, and other financial services.

Singtel has exposure to telecom services, digital solutions, and regional operations.

This broader base can help to reduce the impact of a downturn in any single segment, making their earnings and dividends potentially more resilient over time.

As a result, their dividends may prove more resilient over time, particularly during periods of economic uncertainty.

#4 - Dividend growth potential is higher for stocks.

A REIT’s distribution per unit can remain flat for long periods. A high yield may sometimes reflect a weaker unit price rather than stronger income growth.

This means the headline yield can look attractive, even when the underlying growth in distributions is limited.

By contrast, companies with growing earnings have more scope to raise dividends over time.

For example, Singapore banks may be able to support this through business expansion, new sources of fee income, productivity improvements, and regional growth.

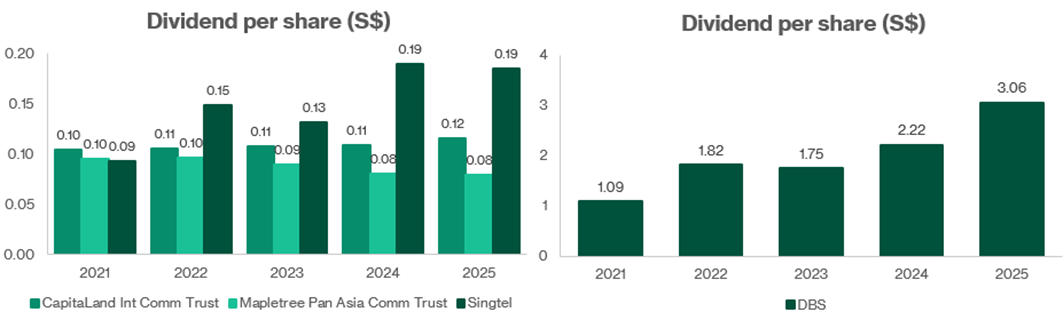

DBS has announced a Capital Return Dividend in addition to its ordinary dividend, providing a higher total dividend payout.

Likewise, many other Singapore blue chip stocks have also committed to dividend growth.

Singtel has announced a Value Realisation Dividend (VRD) which aims to return excess capital from the company’s asset recycling program to shareholders.

Singtel's dividend policy combines a core payout ratio of 70% to 90% of underlying net profit with an annual VRD of 3 to 6 cents per share.

For the full-year 2026, Singtel declared a total ordinary dividend of 18.5 cents per share (a 9% increase year-on-year), which includes a core dividend of 13.4 cents and a VRD of 5.1 cents per share.

ST Engineering has adopted a progressive policy that pays out roughly one-third of its year-on-year increase in net profit (excluding divestment/impairment effects) as incremental dividends.

Over the long term, this gives investors the potential for both rising dividends and capital appreciation.

For Singtel and Mapletree Pan Asia Commercial Trust, 2025 denotes financial year ending 31-Mar-26, with prior years presented on the same financial-year basis.

#5 - REIT acquisitions may not always be accretive to unitholders

When a REIT or business trust funds an acquisition by issuing new units, the portfolio may become larger but each investor ends up owning a smaller share of it.

The acquisition may lift total income, but that income is now spread across more units.

As a result, the benefit to each existing unitholder may be smaller than it first appears.

Over time, if acquisitions are not done at attractive prices or funded carefully, this can dilute the value of each unit even as the REIT grows.

Dividend-paying companies have more ways to grow shareholder value. They can expand earnings through their operations, raise dividends as profits increase, and in some cases return capital through share buybacks.

This gives them more flexibility to grow earnings per share over time, rather than relying on new unit issuance to drive growth.

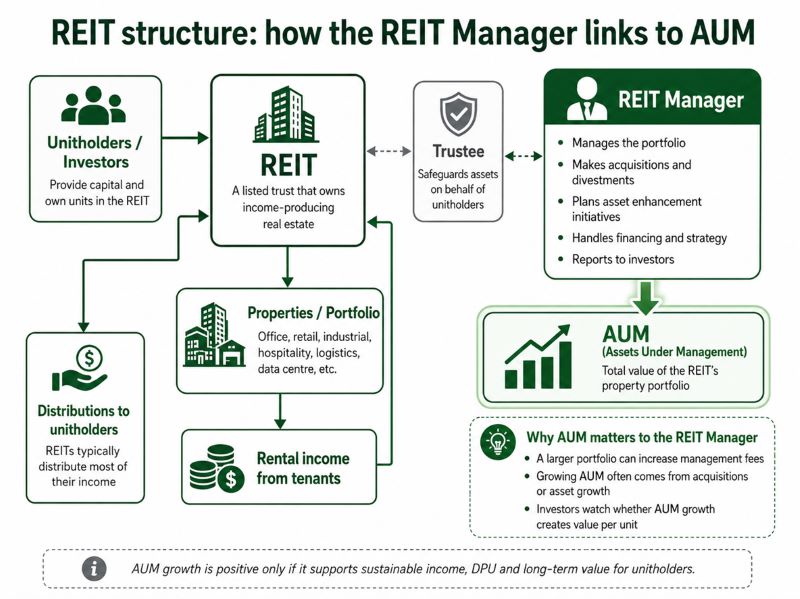

In addition, many Singapore REITs are externally managed, and the manager’s fees are often linked to the size of the portfolio.

This can create an incentive to pursue growth in assets under management, even when it may not fully benefit minority unitholders.

As a result, investors need to pay closer attention to whether acquisitions, capital raising, and fee structures are aligned with long term value creation.

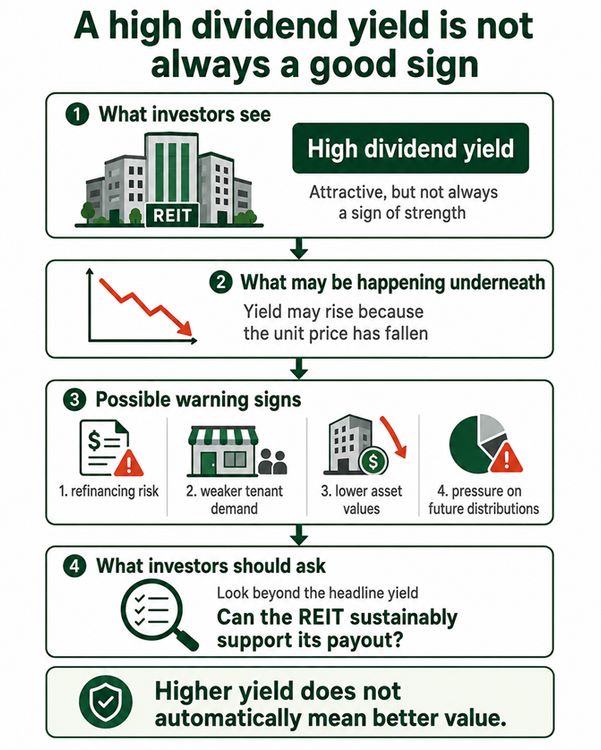

#6 - A REIT with high dividend yield can sometimes be a warning sign.

A high yield can be attractive, but it is not always a sign of strength.

Sometimes, a REIT’s dividend yield rises simply because its unit price has fallen.

That may reflect concerns about refinancing risk, weaker tenant demand, lower asset values, or pressure on future distributions.

In other words, a higher yield does not automatically mean better value.

That is why we think investors should look beyond the headline number and ask whether the underlying business is truly in a position to sustain its payout.

What would Beansprout do?

I have been looking for ways to grow my Income Pot and earn more passive income.

A natural place to start is the Singapore market, which continues to offer attractive dividend yields.

But rather than relying too heavily on Singapore REITs alone, I would look at building a broader mix of income sources.

Singapore REITs can still play a useful role, especially for investors who want steady income, property exposure, or potential upside if interest rates fall.

However, REITs also come with risks, including refinancing costs, asset values, and possible dilution when they raise capital.

You can screen for the best Singapore REITS here.

That is why I would also consider high-quality Singapore blue chip stocks in the Straits Times Index (STI) that offer attractive dividends, sustainable earnings growth, strong balance sheets, and resilient business models.

For my Income Pot, the key is not just to chase the highest yield. It is to build an income portfolio that can hold up across different market conditions.

By combining quality dividend stocks with selected REITs, investors may be better placed to grow dividends over time, while improving the resilience of their portfolio.

You can find out some of our investment ideas to capture opportunities in the market here.

If you’d like to screen for other Singapore stocks with attractive dividend yields and potential upside, you can explore our Singapore dividend stocks screener.

Do you prefer Singapore blue chip stocks or REITs? Share with us in the comments below or in our Telegram group!

Planning to invest in Singapore REITs or blue chip stocks? Compare the best Singapore brokers to find the right trading platform, and see the latest promotions and sign-up rewards available.

Follow Beansprout on Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments