3 Singapore blue chip stocks with forward dividend yields of above 6%. Are their payouts sustainable?

Stocks

By Goh Lay Peng • 19 May 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

We look at three Singapore blue chip stocks with forward dividend yields above 6%, and assess whether their dividend payouts can be sustained after their latest results.

What happened?

I've been looking at Singapore blue chip stocks with dividend income.

Earlier, we looked at DBS, OCBC and UOB’s latest dividends, as the three Singapore banks continued to draw interest after their latest results.

We also looked at 3 Singapore blue-chip REITs near 5-year lows with dividend yields around 6% as REITs remain a popular option for investors looking for passive income.

Beyond the banks and REITs, some Singapore blue chip stocks are also offering forward dividend yields above 6% after the decline in their share prices.

This has led to questions from the Beansprout community on whether these higher dividend yields are attractive, or if they reflect concerns about weaker earnings and lower future payouts.

In this article, I compare three Singapore blue chip stocks with forward dividend yields above 6% in May 2026, and whether their payouts look sustainable after their latest results.

3 Singapore blue chip stocks with forward dividend yields of above 6%

#1 - SIA (SGX: C6L)

Singapore Airlines, or SIA, is Singapore’s national carrier.

The group operates both the full-service Singapore Airlines brand and low-cost carrier Scoot, giving it exposure to premium and budget travel demand.

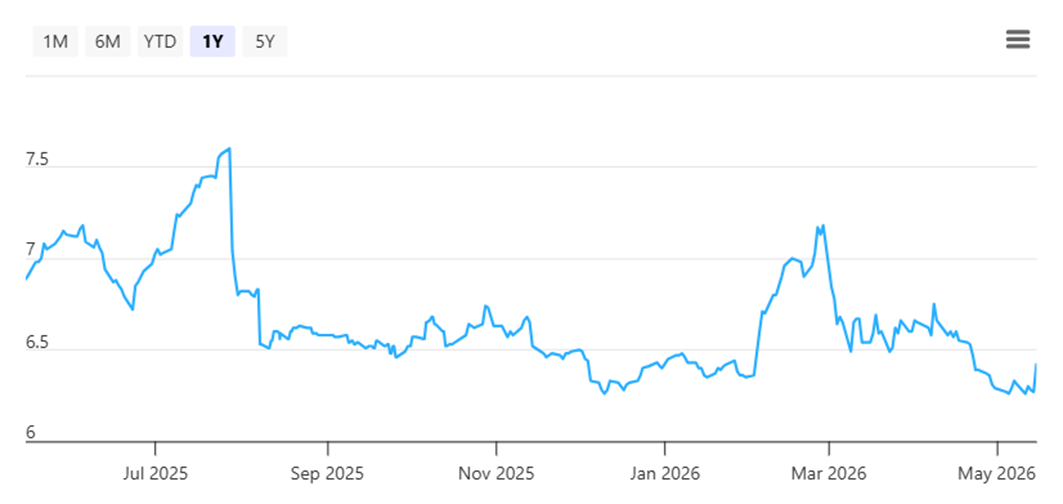

SIA’s share price stood at S$6.41 as of 18 May 2026, little changed from S$6.40 at the end of 2025 and remains near its 5-year low. SIA’s share price has come under pressure more recently as oil prices rose, raising concerns about future fuel costs.

SIA’s latest results were strong at the operating level.

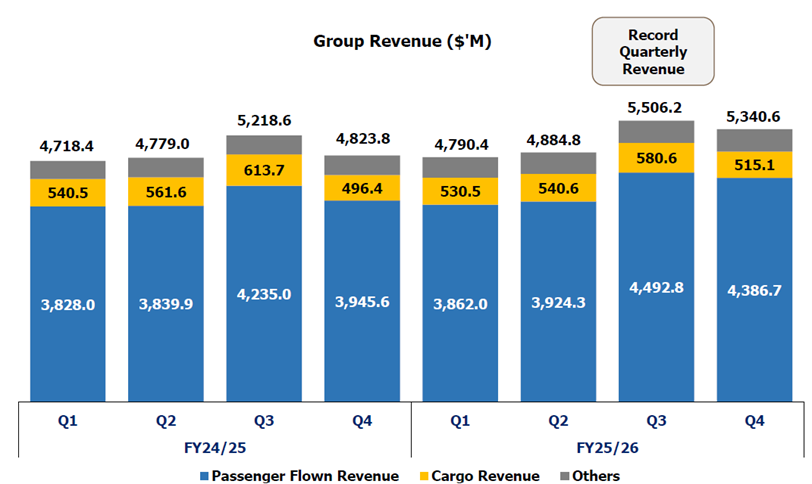

For FY2025/26, revenue rose 5.0% year on year to a record S$20.5 billion, driven by growth in passenger revenue. Revenue growth also strengthened in the second half of FY2025/26, rising 8% year on year.

Passenger demand remained resilient.

SIA and Scoot carried a record 42.4 million passengers during the year, up 7.7% year on year. Passenger load factor rose to 87.7%, while passenger yields increased 1.0%.

Cargo revenue, however, declined 2% year on year.

Operating profit increased 39.0% to S$2.4 billion, helped by healthy travel demand, higher passenger yields and increased capacity across both SIA and Scoot.

Total expenditure rose 1.8% year on year, as non-fuel costs increased 5.4%. This was partly offset by a 6.7% decline in net fuel cost, as fuel prices were still relatively lower over the past 12 months. However, this may not repeat in FY2026/27 if oil prices stay elevated.

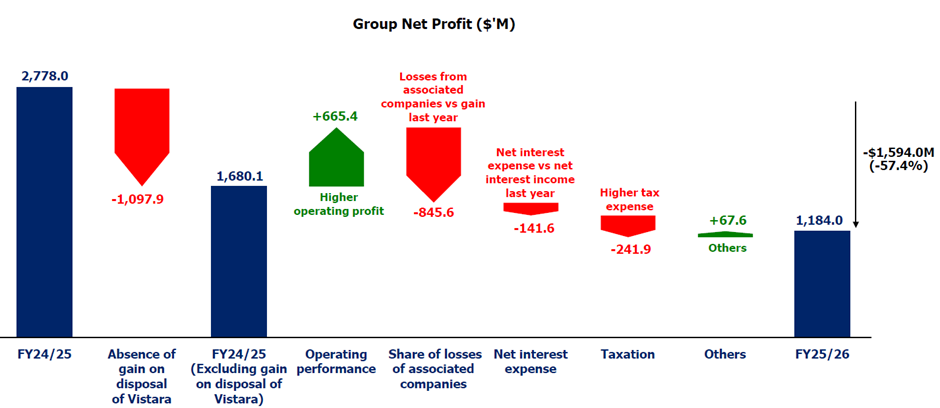

Net profit told a more mixed story.

Net profit fell 57.4% year on year to S$1.18 billion. This was mainly because the previous year included a one-off accounting gain from the Air India-Vistara merger, while SIA also recognised its share of Air India’s full-year losses.

The key risk is that airline earnings can change quickly.

The higher jet fuel price environment was only partially reflected in its March 2026 fuel cost, with the full impact expected to feed through in FY2026/27.

While SIA and Scoot have raised airfares, these adjustments do not fully offset the increase in jet fuel prices.

Air India is another factor to watch.

We previously highlighted that Air India’s losses and potential capital needs could affect how investors think about SIA’s future dividend capacity. The latest results show that Air India losses are already weighing on SIA’s reported earnings.

Against this backdrop, this makes the dividend sustainability picture more nuanced.

For FY2025/26, SIA proposed a final ordinary dividend of 22 cents per share and a final special dividend of 7 cents per share.

Together with the interim ordinary dividend of 5 cents and interim special dividend of 3 cents paid earlier, total dividends for FY2025/26 would amount to 37 cents per share.

Of this, total special dividends for the year would amount to 10 cents per share.

Based on its share price of S$6.41 as of 18 May 2026, SIA offers a Trailing Twelve Months (TTM) dividend yield of 5.9%

Overall, I would see SIA as a cyclical dividend stock rather than a defensive income stock.

Reflecting SIA’s strong balance sheet, the board has announced that they are planning a special dividend over the next three years.

Based on consensus estimates on FY26/27 dividend of S$0.44, SIA offers a potential forward dividend yield of 6.9%. The upside comes from the ability to pay higher special dividends.

While the forward dividend yield may look attractive, future dividends will still depend on travel demand, fuel prices, Air India losses and how much cash the group needs to support long-term growth.

Find out how much dividends you would have received as a shareholder of SIA in the past 12 months with the calculator below.

Related links:

- SIA latest valuation, share price and analysis

- SIA dividend forecast and dividend yield

- How SIA’s 5.8% dividend yield may be affected by Air India’s capital raising

#2 - Thai Beverage Public Company Limited (SGX: Y92)

Thai Beverage, or ThaiBev, is one of Southeast Asia’s largest beverage companies. Its business spans spirits, beer, non-alcoholic beverages and food.

ThaiBev’s share price stood at S$0.445 as of 18 May 2026, down by about 3.3% year-to-date.

We previously highlighted ThaiBev as one of the weaker-performing Singapore blue chip stocks in 2026, as the group faced a cautious consumer backdrop in its key markets.

Beer demand was weak, while investors were also watching alcohol regulations in Thailand and Vietnam.

Since then, its latest 1H26 results suggest that the business remains mixed, but not weak across the board.

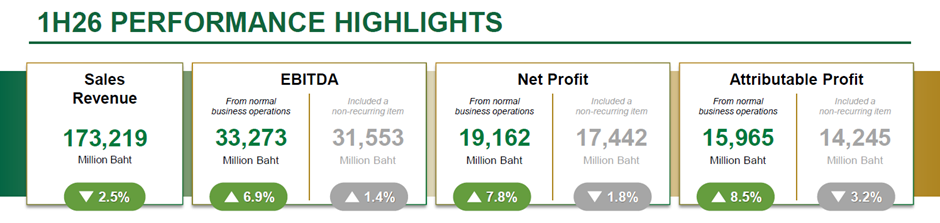

For 1H26, sales revenue fell 2.5% year on year to Baht 173.2 billion. This was mainly due to softer performance in the beer and non-alcoholic beverage businesses.

However, profit from normal operations improved.

EBITDA from normal business operations rose 6.9% year on year to Baht 33.3 billion, while net profit from normal business operations increased 7.8% to Baht 19.2 billion.

Attributable profit from normal business operations rose 8.5% to Baht 16.0 billion.

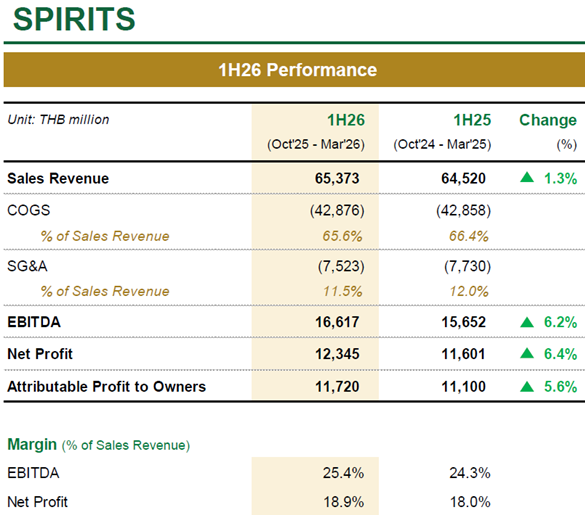

The spirits business remained the key support.

In 1H26, spirits sales revenue rose 1.3% year on year to Baht 65.4 billion. EBITDA increased 6.2% to Baht 16.6 billion, while net profit rose 6.4% to Baht 12.3 billion. Attributable profit to owners also grew 5.6% to Baht 11.7 billion.

This was supported by growth in 2Q26, continued growth in the international business, and lower key raw material costs. Spirits EBITDA margin improved to 25.4%, from 24.3% a year ago.

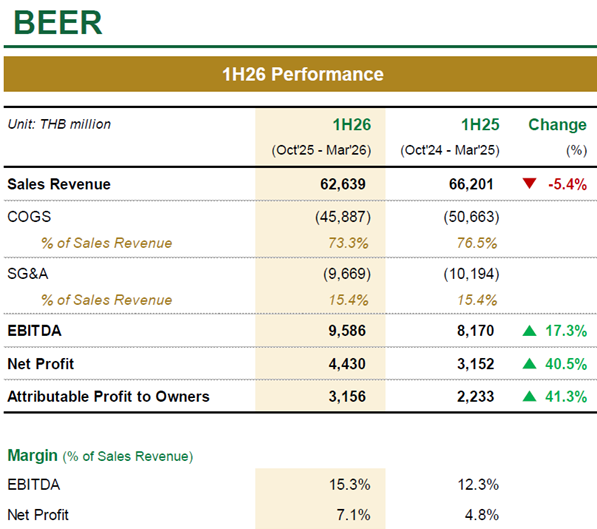

The beer business showed a different picture.

Sales revenue fell 5.4% year on year to Baht 62.6 billion, mainly due to weaker 1Q26 performance amid subdued market conditions in Thailand, severe weather in Vietnam and unfavourable exchange rate translation.

However, beer sales revenue rebounded in 2Q26 and profitability also improved.

Beer EBITDA rose 17.3% to Baht 9.6 billion, while net profit increased 40.5% to Baht 4.4 billion. Attributable profit to owners rose 41.3% to Baht 3.2 billion. Beer EBITDA margin expanded to 15.3%, from 12.3% a year ago.

This suggests that while beer demand remains soft, lower raw material costs and operational improvements helped to support margins.

However, the weaker spots were also on non-alcoholic beverages and food.

Both businesses remained under pressure amid softer operating performance and a challenging competitive environment. This means the recovery was not broad-based across all segments.

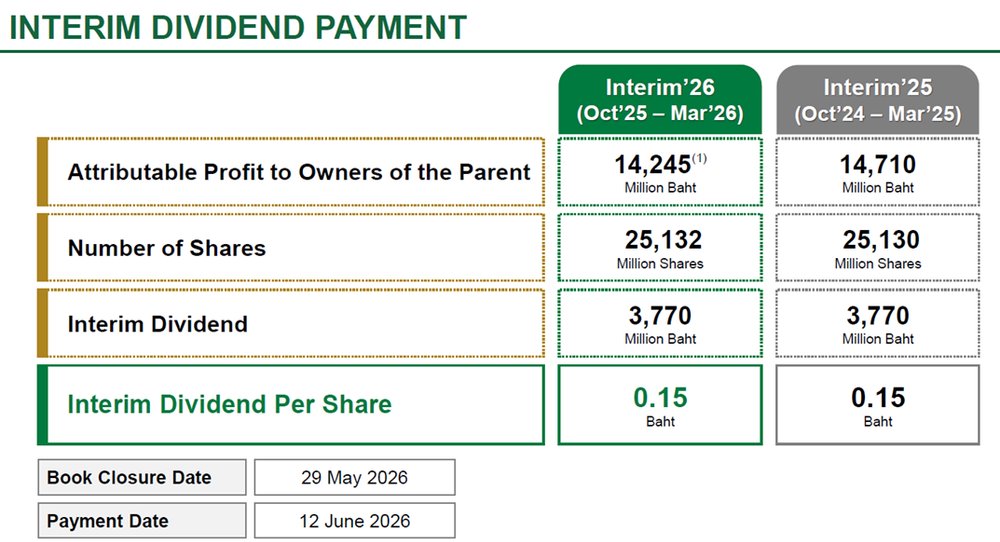

ThaiBev maintained its interim dividend at Baht 0.15 per share, unchanged from the previous year.

This makes ThaiBev’s dividend look more sustainable than its share price weakness may suggest.

The interim dividend was maintained even though reported attributable profit fell slightly after including a non-recurring impairment loss from discontinued operations of a joint venture.

For FY2025, ThaiBev declared total dividends of THB 0.62 per share, comprising an interim dividend of THB 0.15 and a final dividend of THB 0.47.

Based on its share price of S$0.445 as of 18 May 2026, ThaiBev offers a Trailing Twelve Months (TTM) dividend yield of 5.6%.

More importantly, normalised profit continued to grow.

That said, there are still risks to watch.

Beer demand remains soft, non-alcoholic beverages are still under pressure, and Singapore investors are exposed to Thai baht currency movements when dividends are translated into Singapore dollars.

Overall, ThaiBev appears to offer the most defensive dividend profile among the three stocks in this list.

Based on consensus FY26 dividend per share estimates of S$0.03, Thai Beverage is trading at a forward dividend yield of around 6.6%, which remains attractive relative to Singapore government bond yields and many regional consumer staples peers.

At a share price of about S$0.445, the stock continues to appeal to income-focused investors.

I would still watch whether the beer and non-alcoholic beverage segments can stabilise before expecting stronger dividend growth.

Find out how much dividends you would have received as a shareholder of Thai Beverage in the past 12 months with the calculator below.

Related links:

- Thai Beverage Public Company Limited latest valuation, share price and analysis

- Thai Beverage Public Company Limited dividend history and dividend forecast

#3 - Genting Singapore Limited (SGX: G13)

Genting Singapore owns and operates Resorts World Sentosa. Its business is tied to gaming, tourism, hotels, attractions, dining and lifestyle spending.

This gives Genting Singapore exposure to Singapore’s tourism recovery, but also makes its earnings sensitive to visitor spending, competition and cost pressures.

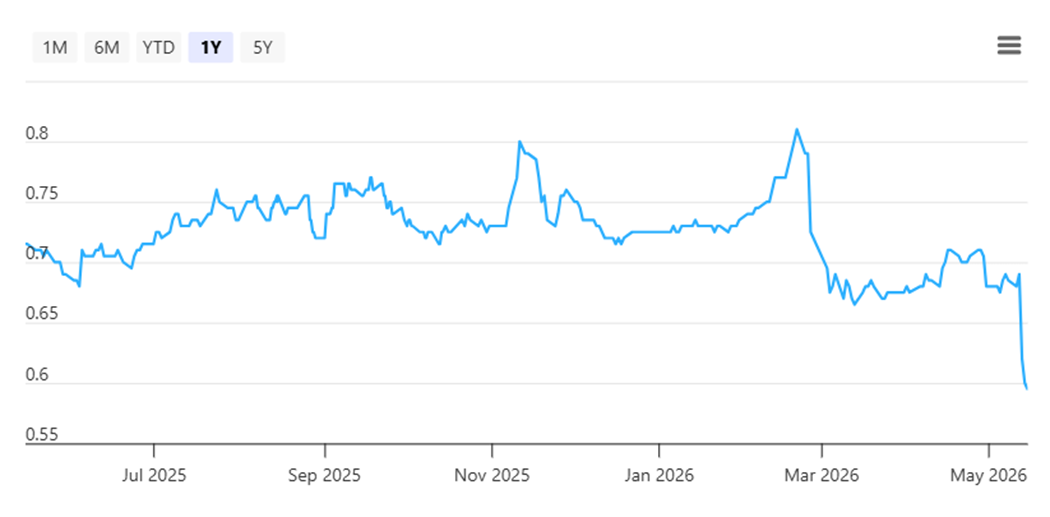

Genting Singapore’s share price stood at S$0.59 as of 18 May 2026, fallen by about 19% year-to-date and is also currently near its 5-year low.

We previously highlighted that Genting Singapore was also one of the weaker-performing Singapore blue chip stocks in 2026, as it worked through a transition year for Resorts World Sentosa. Its FY2025 net profit fell 33% year on year to S$390.3 million, while renovation works and weaker gaming performance weighed on the business.

The latest 1Q26 results suggest that the earnings pressure has not gone away.

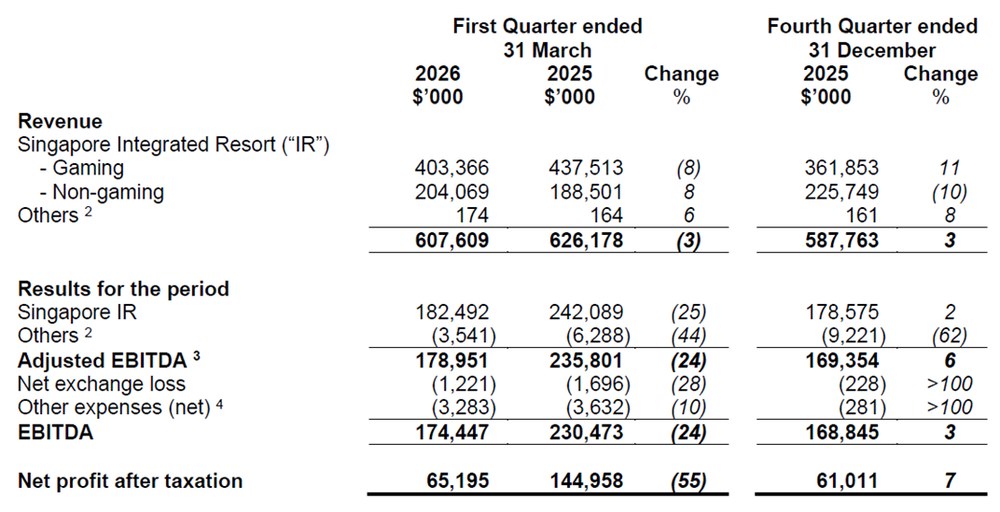

For 1Q26, Genting Singapore’s revenue fell 3% year on year to S$607.6 million. Gaming revenue declined 8%, while non-gaming revenue rose 8%.

The bigger pressure came at the profit level.

Adjusted EBITDA fell 24% year on year to S$179.0 million, while net profit after tax fell 55% to S$65.2 million.

This makes Genting Singapore the stock I would be most cautious about from a dividend sustainability perspective.

The non-gaming business showed some improvement, supported by higher visitation to key attractions such as Universal Studios Singapore and the Singapore Oceanarium.

However, this was not enough to offset weaker gaming revenue and higher costs.

Genting Singapore remarked that geopolitical developments have increased cost pressures across energy, freight and logistics, while elevated airfares are weighing on travel demand and consumer sentiment.

There is also a reinvestment angle to consider.

The group continues to invest in new concepts, hotel and asset enhancements, amenities and technology applications. These investments may help strengthen Resorts World Sentosa over the long term, but they could also weigh on margins and cash flow in the near term.

Another risk is the casino licence renewal.

RWS’ casino licence was renewed for only two years from 6 February 2025, instead of the usual three-year term, after its tourism performance was assessed to be unsatisfactory. The next evaluation was recommended to take place in 2026.

This does not mean the licence will not be renewed.

However, it does add another area for investors to watch, especially as RWS 2.0 remains important to Genting Singapore’s longer-term growth story.

On dividends, Genting Singapore maintained total FY2025 dividends at 4 cents per share, unchanged from FY2024. However, the payout ratio rose to 124%, which means the dividend exceeded earnings for the year.

Based on its share price of S$0.59 as of 18 May 2026, Genting Singapore offers a Trailing Twelve Months (TTM) dividend yield of 6.8%.

That does not necessarily mean the dividend will be cut immediately, especially since Genting Singapore has historically maintained a strong balance sheet.

However, it does suggest that the margin of safety has become thinner.

Based on consensus estimates on FY26 dividend per share remaining stable at S$0.04, Genting Singapore is offering a forward dividend yield of 6.8%. However, the higher dividend yield compensates investor concern about the payout rather than simply an attractive income opportunity.

Find out how much dividends you would have received as a shareholder of Genting Singapore in the past 12 months with the calculator below.

Related Links:

- Genting Singapore Limited latest valuation, share price and analysis

- Genting Singapore Limited dividend forecast and dividend yield

What would Beansprout do?

For me, the key is not to look at the forward dividend yield in isolation.

SIA, ThaiBev and Genting Singapore all offer forward dividend yields above 6%, but the quality of those yields is not the same.

ThaiBev looks like the most defensive income name with a sustainable dividend profile among the three. Its reported profit was affected by a non-recurring impairment loss, but normalised earnings continued to improve and the interim dividend was maintained. Learn more about ThaiBev here.

SIA still has strong operating momentum and a solid balance sheet, but I would treat it as a cyclical income stock. Airline earnings can be affected by fuel prices, travel demand, competition and Air India losses. The special dividend plan provides some visibility, but I would not assume that SIA’s high dividend yield is risk-free. Learn more about SIA here.

Genting Singapore offers an attractive forward dividend yield, but I would be the most cautious here since the payout ratio is above 100%. Its weaker 1Q26 earnings, payout ratio above 100%, RWS 2.0 capital needs and upcoming casino licence evaluation mean the dividend has less margin of safety compared to the other two. Learn more about Genting Singapore here.

That said, if I were building my Income Pot, I would not buy any of these stocks simply because the yield is above 6%.

I would first ask whether the dividend is backed by recurring earnings, whether the balance sheet can support the payout, and whether the business is facing temporary or structural pressure.

Among the three, ThaiBev may be worth a closer look for investors who want a more defensive dividend stock, while SIA may appeal to those comfortable with airline-cycle volatility.

For Genting Singapore, I would prefer to see clearer signs that earnings and margins are stabilising before relying on the current dividend yield.

Learn how to build a more dependable stream of passive income that can hold up across cycles here.

| Stock | The good | Key risks |

| SIA (SGX: C6L) | ● Forward dividend yield of 6.9% ● FY2025/26 operating profit rose 39% ● Record passenger traffic of 42.4 million passengers | ● Net profit fell due to absence of one-off gain ● Higher fuel costs may weigh on margins ● Air India losses and capital needs remain a drag |

| Thai Beverage (SGX: Y92) | ● Forward dividend yield of 6.6% ● Normalised attributable profit rose 8.5% ● Interim dividend maintained at 0.15 baht per share | ● Beer and non-alcoholic beverages remain soft ● Consumer sentiment in Thailand and Vietnam still mixed ● Regulatory and currency risks remain |

| Genting Singapore (SGX: G13) | ● Forward dividend yield of 6.8% ● FY2025 dividend maintained at 4 cents per share ● RWS 2.0 may support longer-term growth | ● 1Q26 net profit fell 55% year on year ● FY2025 payout ratio was above 100% ● Casino licence renewal remains a risk |

If you are new to Singapore blue chip stocks, read our Singapore blue chip stocks guide to understand how they work before investing.

If you prefer broad exposure to blue chips without picking individual names, you can also learn more about the Straits Times Index (STI).

Are you looking at any Singapore blue chip dividend stocks? Share your thoughts with us in the comments below or in our Telegram group!

Planning to invest in Singapore blue chip stocks? Check out Beansprout's guide to the best stock trading platforms in Singapore with the latest promotions to invest in the Singapore market and see the latest promotions and sign-up rewards available.

Enjoyed this insight? Follow Beansprout on Telegram, Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments