CapitaLand Ascendas REIT Preferential Offering - What should unitholders do?

REITs

By Gerald Wong, CFA • 08 Apr 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

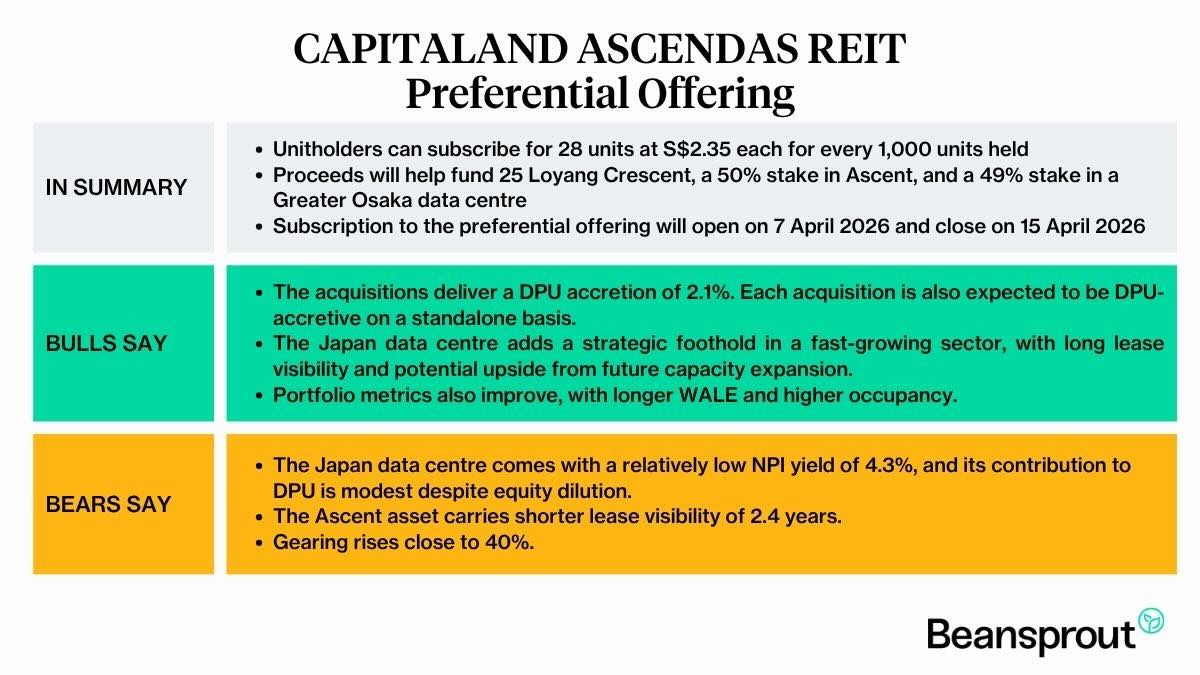

The CapitaLand Ascendas REIT preferential offering will offer entitled unitholders the right to buy 28 new units at S$2.35 each for every 1,000 units held.

What happened?

CapitaLand Ascendas REIT (CLAR) has been on an acquisition spree recently.

On 24 March 2026, CapitaLand Ascendas REIT announced three acquisitions valued at around S$1.41 billion.

To fund its latest acquisitions, as well as partially finance earlier acquisitions in Singapore, the United States and Spain, two potential acquisitions in Singapore, and related transaction expenses, , CapitaLand Ascendas REIT launched an equity fund raising of at least S$900 million through a private placement and preferential offering.

Earlier, CapitaLand Ascendas REIT entered Spain with S$185.4 million logistics portfolio acquisition, added a US logistics property for S$94.5 million in January and acquired 2 Singapore assets for around S$700 million in June last year.

This follows a trend of Singapore REITs being active in acquisitions in fundraising, after we saw the preferential offering by Lendlease REIT last month.

If you are a CapitaLand Ascendas REIT unitholder and wondering what you should do about the preferential offering, read on to find out.

5 things to know about the CapitaLand Ascendas REIT preferential offering

#1 – Existing unitholders can buy new units at S$2.35 each

As part of its equity fund raising, CapitaLand Ascendas REIT (CLAR) is offering new units to existing unitholders at S$2.35 per unit.

This price was fixed after the private placement was completed, and represents a 6.5% discount to CapitaLand Ascendas REIT’s volume-weight average price (VWAP) of S$2.5126 on 23 March 2026, or a 5.1% discount to the adjusted VWAP of S$2.4751, and a 6.4% discount to the closing price of S$2.51 as of 6 April 2026.

#2 – Eligible unitholders are entitled to 28 units for every 1,000 units you own

Eligible unitholders will receive provisional allotments on the basis of 28 preferential offering units for every 1,000 existing units held as at 5.00 p.m. on 1 April 2026, which is the record date.

In total, CapitaLand Ascendas REIT will issue about 129.1 million preferential offering units and raise about S$303.5 million from this part of the fund raising.

#3 – The preferential offering is non-renounceable

CapitaLand Ascendas REIT’s preferential offering is non-renounceable, which means you cannot sell or transfer your entitlement to someone else.

You can either accept your allotted units, decline them, or apply for excess units. If you do nothing, your entitlement simply lapses.

#4 – You can apply for excess units if other investors do not take up their allotment

If some unitholders do not subscribe for their entitlement, those leftover units may be reallocated to investors who apply for excess preferential offering units.

CapitaLand Ascendas REIT said excess units may come from unitholders who decline their allotments, ineligible unitholders, or fractional entitlements.

In allocating excess units, preference will be given to the rounding of odd lots, while directors and substantial unitholders will rank last for excess allocations.

#5 - The preferential offering is underwritten

CapitaLand Ascendas REIT's preferential offering is underwritten by a group of banks including DBS, J.P. Morgan, OCBC, UOB and Mizuho.

Under the underwriting agreement, each bank has agreed to procure subscribers for its share of the preferential offering units, or failing that, to subscribe for those units itself, subject to certain conditions.

This means that if existing unitholders do not fully subscribe for the preferential offering, the underwriters are expected to step in for their respective portions, assuming the conditions in the underwriting agreement are met. This reduces the risk that CapitaLand Ascendas REIT raises less capital than planned.

What you need to know about CapitaLand Ascendas REIT’s latest acquisitions

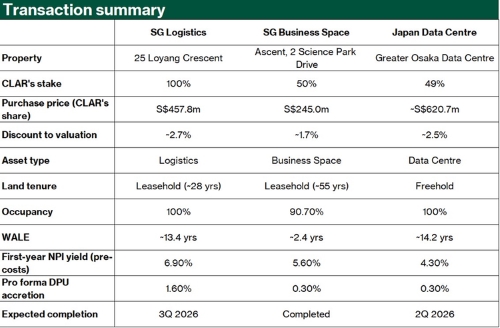

CapitaLand Ascendas REIT is acquiring three assets that strengthen different parts of its portfolio: a logistics asset at 25 Loyang Crescent, a 50% stake in Ascent at Singapore Science Park, and a 49% stake in a Tier III hyperscale data centre in Greater Osaka, Japan.

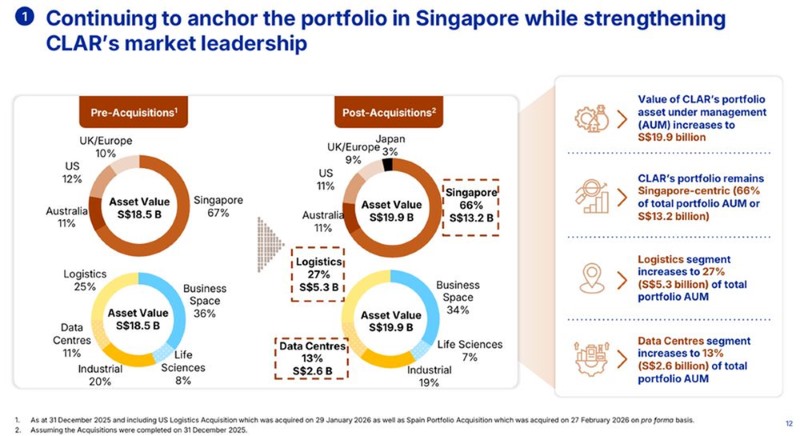

Together, these acquisitions support CapitaLand Ascendas REIT's push into higher-quality logistics, business space and data centre assets, while keeping Singapore as the core of its portfolio.

#1 - Loyang asset is a large logistics and industrial complex

The Loyang asset stands out for its long leaseback and specialised features.

It is a large logistics and industrial complex in eastern Singapore with waterfront facilities, yard space and a ramp-up warehouse.

The property will be leased back to Toll Offshore Petroleum Services on a 12-year absolute triple-net lease, with a weighted average lease expiry of about 13.4 years and annual rent escalation of 2.5%.

It also has an untapped plot ratio, giving CLAR potential redevelopment upside over time.

#2 - Ascent at 2 Science Park Drive within walking distance of Kent Ridge MRT station

Ascent adds a quality business space asset in Singapore Science Park, one of Singapore’s key research and innovation clusters.

The property is 90.7% occupied, with tenants including Johnson & Johnson, Dyson and Merck.

It is also a modern seven-storey building completed in 2016, with a long remaining land tenure of about 55.5 years and annual rental escalations in most leases.

#3 - CapitaLand Ascendas REIT's first investment in Japan

The Japan data centre is arguably the most strategic of the three.

This is CapitaLand Ascendas REIT's first investment in Japan, giving it exposure to a new developed market and a sector supported by long-term digital infrastructure demand.

The asset is freehold, completed in 2023, fully occupied by a global investment-grade hyperscaler, and comes with a long weighted average lease expiry of about 14.2 years.

There is also potential to expand power capacity by 13.3% in the medium to long term.

Overall, the acquisitions suggest CapitaLand Ascendas REIT is not just growing bigger, but becoming more focused on assets with long leases, resilient tenants and exposure to structural growth themes.

#4 - Acquisitions expected to be yield accretive

On a pro-forma basis, CapitaLand Ascendas REIT’s portfolio occupancy would rise from 90.9 percent to 91.5 percent, while weighted average lease expiry would extend from 3.7 years to 4.3 years.

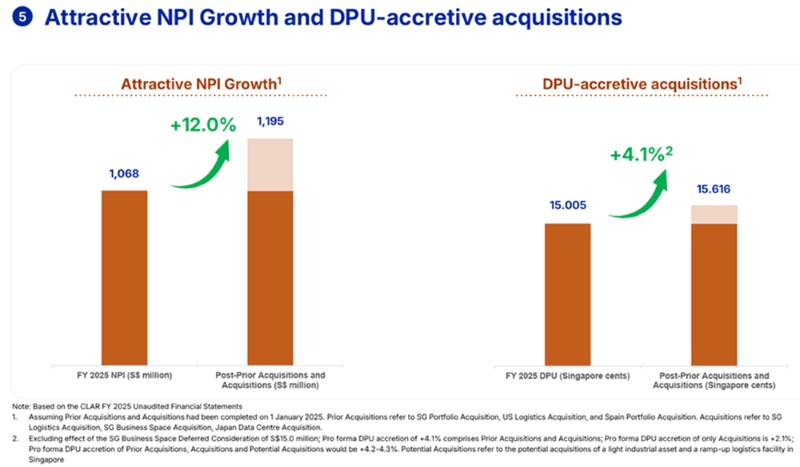

Based on CLAR’s pro forma figures, the three acquisitions together are expected to raise FY2025 DPU by about 0.318 Singapore cents, or 2.1 percent, from 15.005 Singapore cents to 15.323 Singapore cents, assuming all three had been completed on 1 January 2025.

Each acquisition is also expected to be DPU-accretive on a standalone basis.

Including the acquisitions announced since October 2025, total pro forma DPU accretion rises to about 4.1 percent.

CLAR is also evaluating two more Singapore assets, a light industrial property and a ramp-up logistics facility. If these proceed, pro forma DPU accretion could rise further to around 4.2 to 4.3 percent.

Private placement and preferential offering to fund acquisition

To help fund the acquisitions, CapitaLand Ascendas REIT launched an equity fund raising on 24 March 2026 through a private placement and a preferential offering, with total gross proceeds of S$903.5 million.

The private placement raised about S$600.0 million at an issue price of S$2.406 per unit, while the preferential offering is expected to raise about S$303.5 million at S$2.35 per unit.

Though the private placement was oversubscribed, it was completed at the bottom end of the indicated price range, suggesting that while there was sufficient institutional demand for the fund raising, investors remained selective.

The equity fund raising is not meant to fully pay for the acquisitions on its own.

Based on CapitaLand Ascendas REIT's acquisition announcement, the total acquisition outlay is about S$1.41 billion, of which around S$496.6 million will be funded by net proceeds from the equity fund raising and about S$911.4 million will come from debt financing.

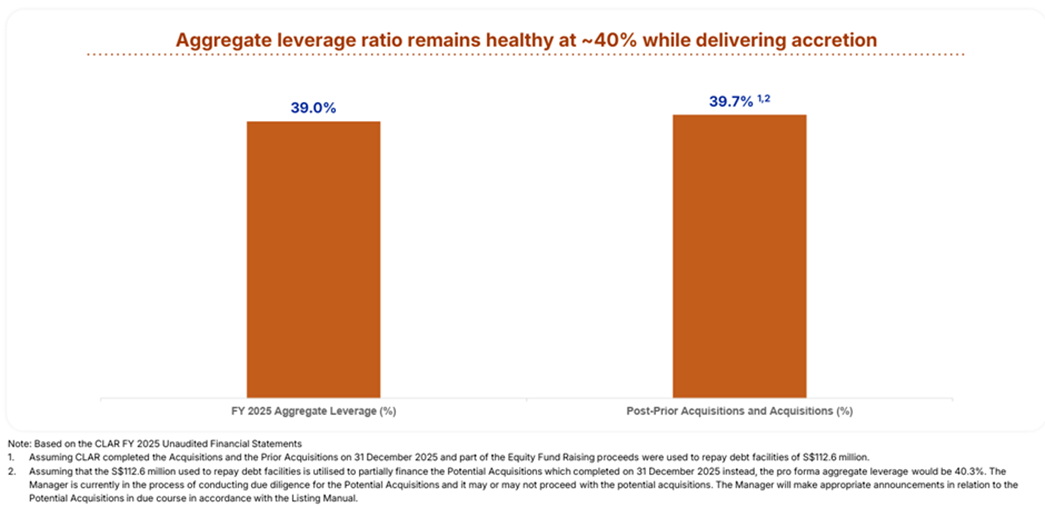

This mix of equity and debt is important because it helps CLAR manage its balance sheet. CapitaLand Ascendas REIT's aggregate leverage stood at 39.0% as at 31 December 2025. The manager said the equity fund raising would help keep leverage within its desired range.

On a pro forma basis, aggregate leverage would be 39.7% after taking into account the prior acquisitions and the latest acquisitions. If the equity had not been raised and temporarily used to repay debt before deployment, CapitaLand Ascendas REIT would have had less financial flexibility.

Part of the proceeds will go towards the three latest acquisitions, including about S$218.3 million for 25 Loyang Crescent, S$93.5 million for the 50% stake in Ascent, and S$188.3 million for the 49% stake in the Japan data centre.

What would Beansprout do?

Overall, the acquisitions appear to be distribution per unit accretive and are in line with CapitaLand Ascendas REIT’s strategy of strengthening its exposure to logistics, business space and data centre assets.

This is worth noting because the uplift from the acquisitions may help offset the slight decline in distribution per unit reported in CLAR’s second-half 2025 results.

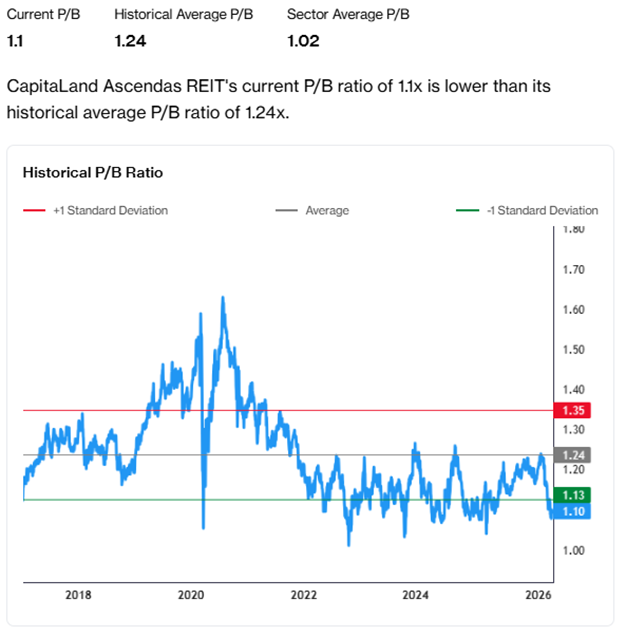

From a valuation perspective, CapitaLand Ascendas REIT is trading at about 1.1 times book value based on its pre-acquisition book value, or around 1.06 times based on its pro forma net asset value of S$2.36.

Both are below its long-term average of 1.2 times book, suggesting that valuations still look reasonable relative to its own history.

Based on the pro forma distribution per unit of 15.323 Singapore cents and a closing price of S$2.51 as of 6 April 2026, CapitaLand Ascendas REIT would offer a dividend yield of about 6.1%.

This is broadly in line with the CSOP iEdge S-REIT Leaders Index ETF forward distribution yield of 6.1%.

Importantly, this is also above CapitaLand Ascendas REIT's long-term average dividend yield of 5.5%, and above the yield on the 10-year Singapore government bond.

This suggests that the recent pullback in CapitaLand Ascendas REIT's unit price may have made its yield more attractive for income-focused investors.

Hence, while the dividend yield of CapitaLand Ascendas REIT is attractive compared to its historical average, I will also be thinking about how I can build a diversified income portfolio beyond Singapore REITs to grow my income pot.

How to subscribe to the CapitaLand Ascendas REIT preferential offering?

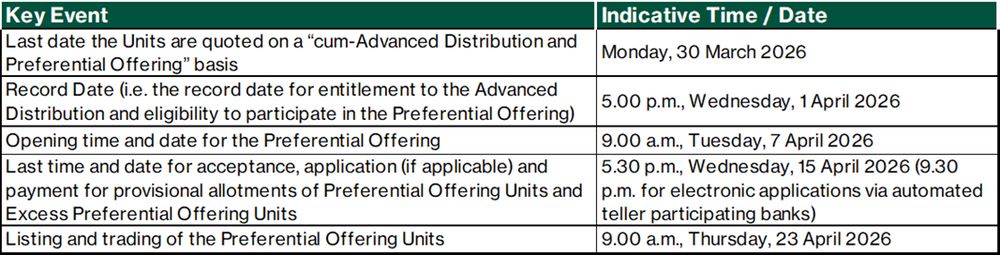

The Preferential Offering opened on 7 April, and will close on 15 April 2026 (Wednesday).

- 7 April 2026: Opening date for the Preferential Offering

- 15 April 2026: Closing Date

- 23 April 2026: Expected date for crediting of the Preferential Offering Units and commencement of trading of the Preferential Offering Units

If you are interested to subscribe to the preferential offering, you may do so via:

- ATM (DBS, POSB, OCBC and UOB)

- Online at investors.sgx.com and remittance via PayNow

- Application Form

- Provisional Allotment Letter (PAL) issued to eligible scripholders

To screen for Singapore REITs with lowest price-to-book valuation or highest dividend yield, check out our best Singapore REIT screener.

If you are new to investing in Singapore REITs, you can start to learn more about Singapore REITs here.

If you prefer diversification without picking individual REITs, you can also gain exposure through Singapore REIT ETFs.

Related links:

- CapitaLand Ascendas REIT share price and share price target

- CapitaLand Ascendas REIT dividend history and forecast

Check out Beansprout's guide to the best stock trading platforms in Singapore with the latest promotions to invest in CapitaLand Ascendas REIT.

Enjoyed this insight? Follow Beansprout on Telegram, Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments