Lendlease REIT Preferential Offering - What should unitholders do?

REITs

By Gerald Wong, CFA • 09 Mar 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

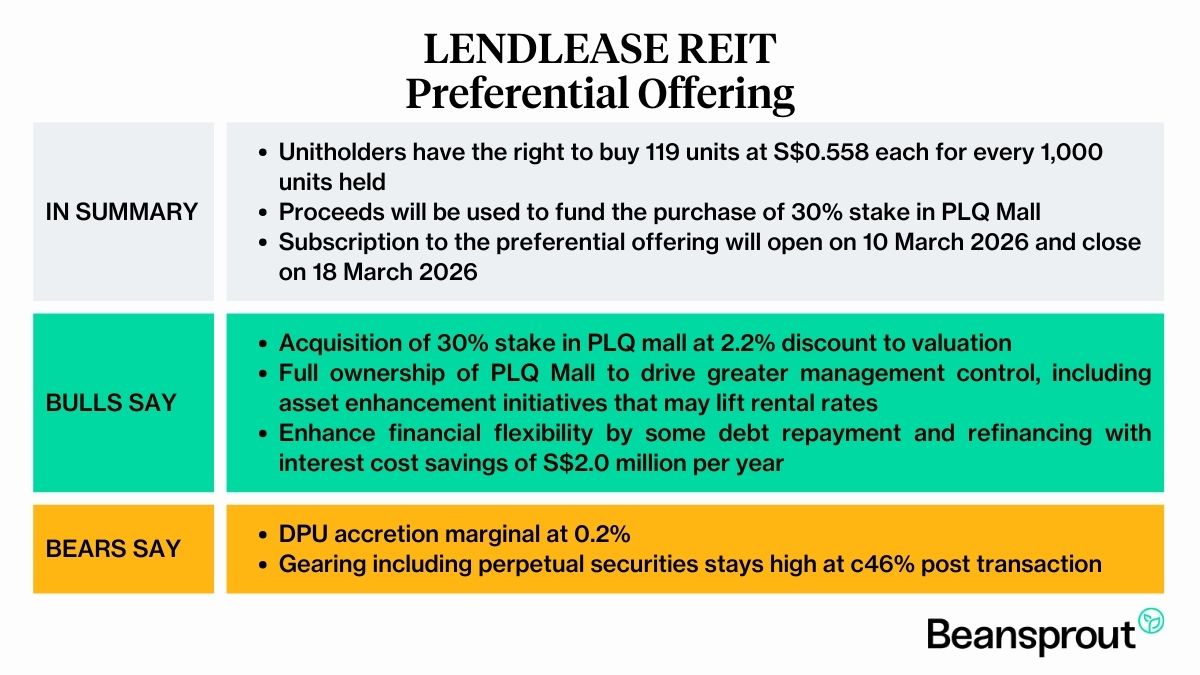

The Lendlease REIT preferential offering will offer entitled unitholders the right to buy 119 new units at S$0.558 each for every 1,000 units held.

What happened?

As interest rates continue to trend lower, Singapore REITs have been buying up assets.

Recently, Keppel REIT raised its stake in MBFC Tower 3, Keppel DC REIT acquired a Japan data centre, CapitaLand Ascendas REIT expanded its Singapore portfolio, and CapitaLand Integrated Commercial Trust (CICT) acquired CapitaSpring.

It appears that Singapore REITs are pursuing growth opportunities through acquisitions once again.

Following the acquisition of 70% interest in PLQ Mall in November 2025, Lendlease REIT announced that it will purchase the remaining 30% stake in PLQ Mall.

Lendlease REIT has also announced a preferential offering to fund the acquisition.

If you are a Lendlease REIT unitholder and wondering what you should do about the preferential offering, read on to find out.

We will dive deeper into the acquisition of PLQ Mall and find out how the preferential offering will impact Lendlease REIT’s dividend yield.

What you need to know about the Lendlease REIT Preferential Offering

- Lendlease Global Commercial REIT (Lendlease REIT) is offering shareholders the right to buy 119 new units for every 1,000 existing units, at S$0.558 each. This Preferential Offering (PO) will raise S$196.6m.

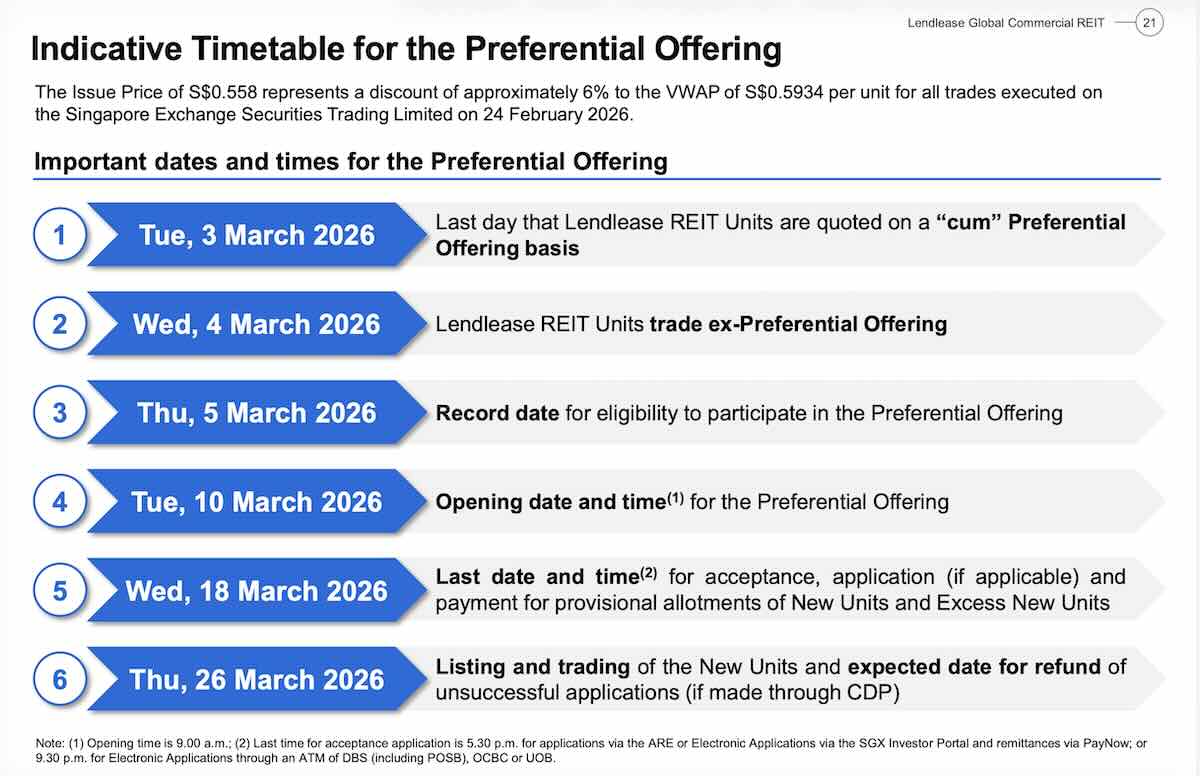

- Unitholders who held Lendlease REIT units on or before 5 March 2026 are eligible to subscribe to the Preferential Offering.

- Subscription to the rights and payment will open on 10 March 2026 and close on 18 March 2026. The new Preferential Offering units are expected to start trading on 26 March 2026.

- The proceeds will be used to acquire from sponsor Lendlease Corporation Limited the remaining 30% stake in PLQ Mall.

- This transaction does not require unitholder approval as it is conducted under the general mandate approved at the October 2025 AGM.

Lendlease REIT buys the remaining 30% stake in PLQ Mall

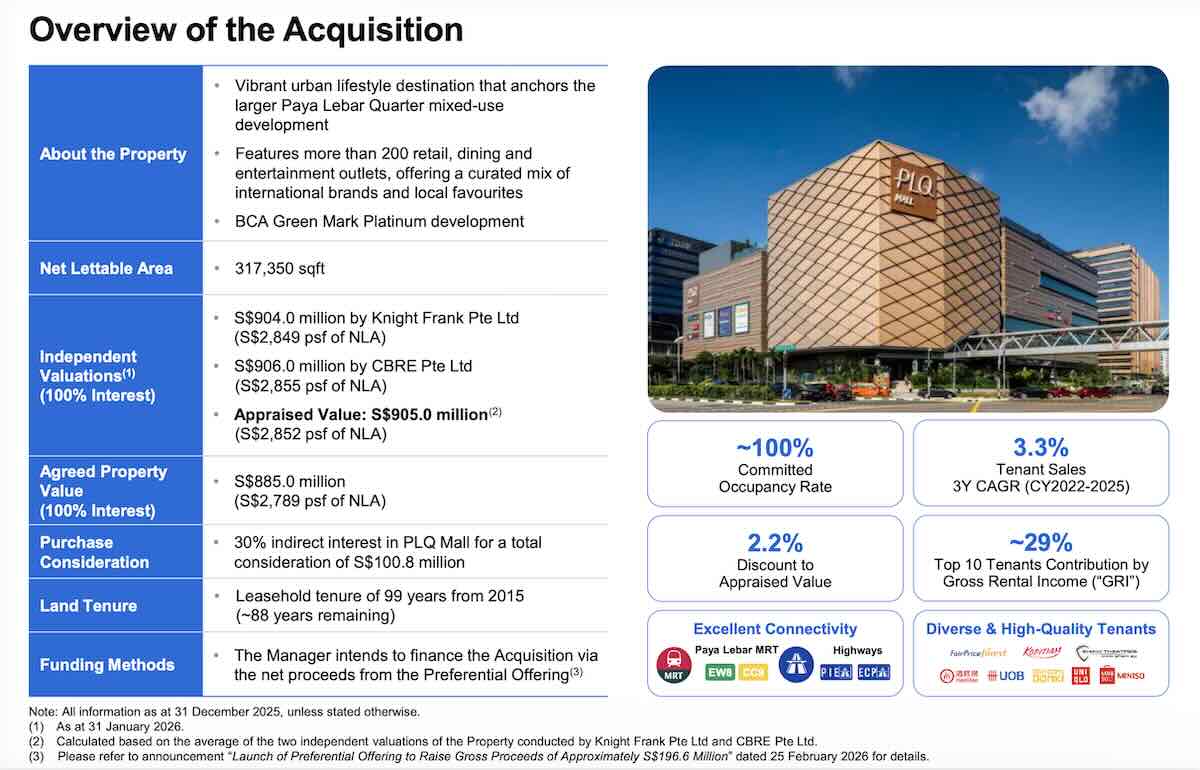

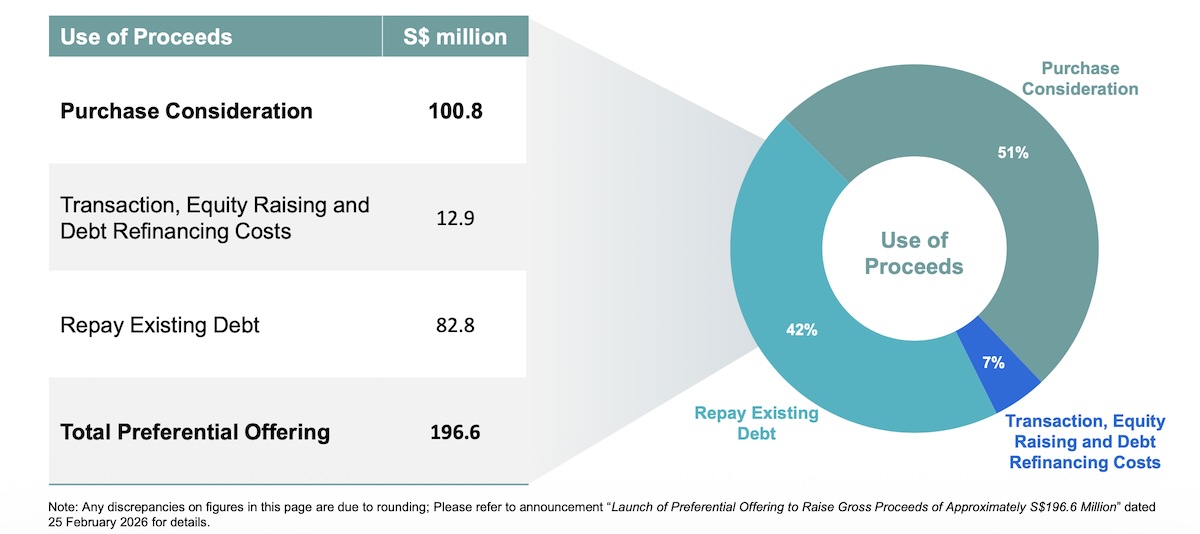

Lendlease REIT will acquire the remaining 30% stake in PLQ Mall for S$100.8 million, bringing its total ownership to 100%.

In November 2025, Lendlease REIT acquired an initial 70% stake in PLQ Mall for S$234.3 million, at a valuation of S$2,789 per square foot.

With the latest acquisition of the remaining 30% stake for S$100.8 million at the same valuation, the REIT will own 100% of the asset upon completion.

The acquisition will be funded through a preferential offering announced alongside the transaction, with the proceeds used to finance the purchase.

What you need to know about Lendlease REIT's acquisition of remaining 30% stake in PLQ Mall

#1 - PLQ Mall has high occupancy rate

PLQ Mall is a 7-storey retail mall and 3 basement car park levels that forms part of the Paya Lebar Quarter mixed-use development.

The property is a leasehold tenure of 99 years commencing from 29 June 2015, with 88 years remaining as at the date of this announcement.

PLQ Mall is currently fully occupied, with a committed occupancy of 100%. The tenant base is well diversified and includes established names such as UOB, FairPrice Finest, Uniqlo and Haidilao, with the top 10 tenants contributing about 29% of gross rental income.

As at 31 December 2025, the mall had a weighted average lease expiry (WALE) of 2.2 years by gross rental income, which provides some visibility on rental income in the near term, although lease renewals will need to be managed over the next few years.

#2 – Asset enhancement works to lift rental rates and refinancing to lower interest costs

By gaining full management and operational control over PLQ Mall, Lendlease REIT gained greater control to optimise the retail space.

Lendlease REIT has started asset enhancement work on approximately 16,000 sq ft of net leasable area on two floors of retail space. Management expects this reconfiguration to drive a substantial uplift in rental rates.

In addition, full ownership allows the refinancing of current borrowings at a lower interest cost. The refinancing is expected to extend approximately S$2 million in interest cost savings.

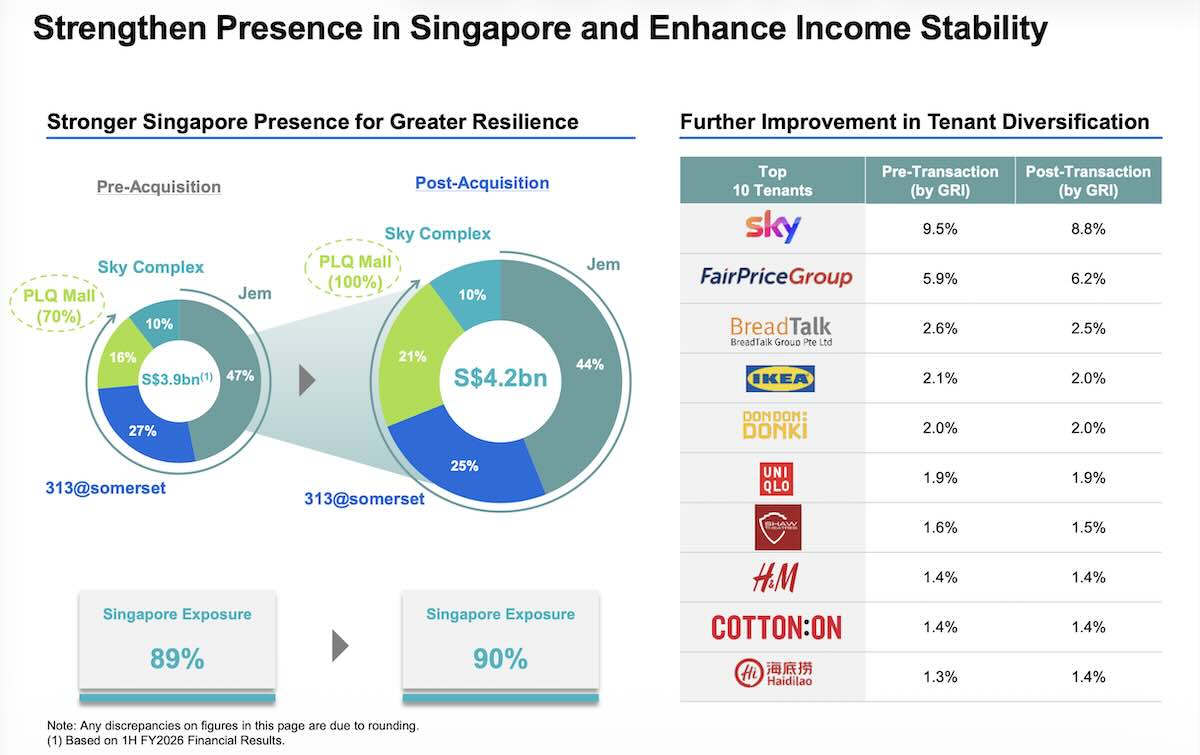

#3 - Transaction will increase Lendlease REIT's exposure to Singapore assets

This acquisition is expected to strengthen the resilience of Lendlease REIT’s portfolio by increasing its exposure to suburban retail and essential services, which tend to offer more stable rental income. Following the transaction, suburban retail will make up about 65.2% of the portfolio, up from 63% previously.

After completion, Lendlease REIT’s exposure to Singapore assets will also rise from 89% to 90%, further reinforcing its positioning as a Singapore-focused REIT with an emphasis on income stability and defensive retail assets.

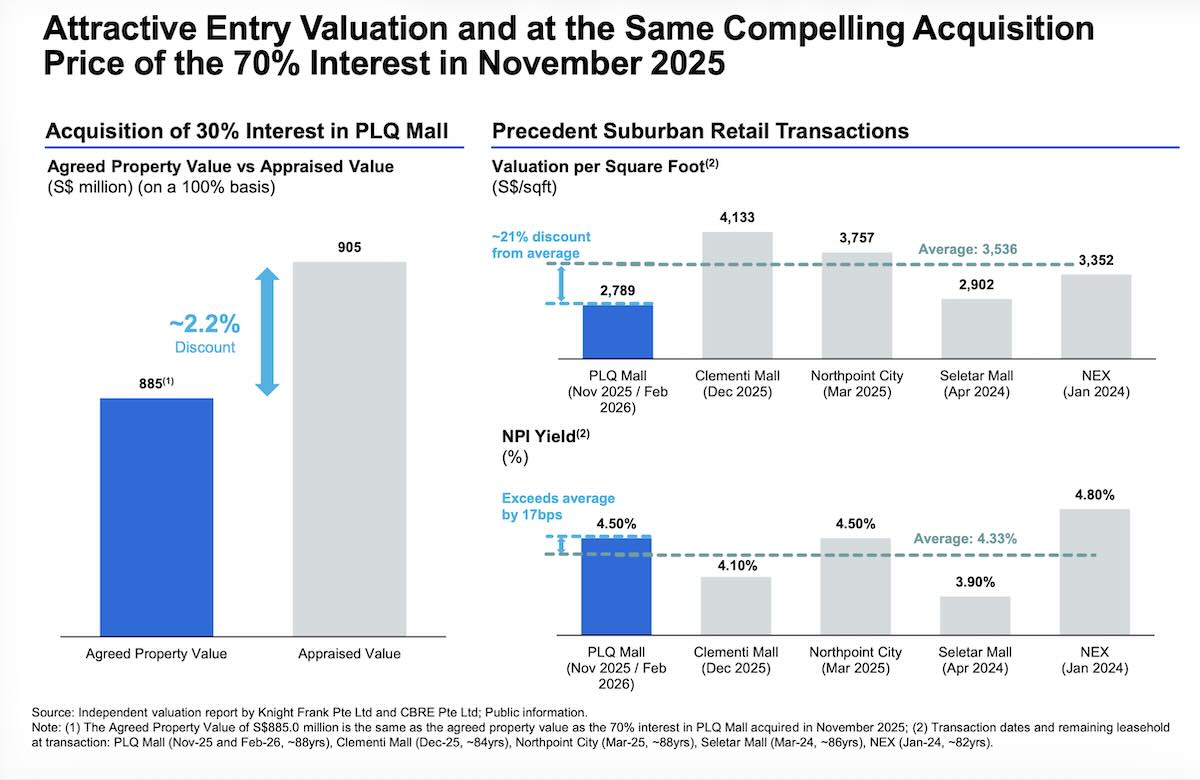

#4 - Acquisition price at discount to valuation

The proposed acquisition is being carried out at a similarly attractive valuation to the earlier purchase of the 70% stake in November 2025.

The agreed property value of S$885.0 million on a 100% basis represents a 2.2% discount to the independent valuation, and implies an NPI yield of about 4.5% per annum.

This yield is slightly higher than the average for recent suburban mall transactions, exceeding comparable deals by about 17 basis points, suggesting that the acquisition was completed at a reasonable entry price.

Preferential offering to fund acquisition

Lendlease REIT announced that the acquisition will be fully funded through an underwritten, non-renounceable preferential offering.

Under the offering, about 352.36 million new units will be issued at S$0.558 per unit, raising gross proceeds of approximately S$196.6 million.

Entitled unitholders can subscribe for 119 preferential units at S$0.558 each for every 1,000 units held.

The issue price of S$0.558 represents a 6.0% discount to Lendlease Global Commercial REIT’s volume-weighted average price of S$0.5934 per unit based on trades done on 24 February 2026.

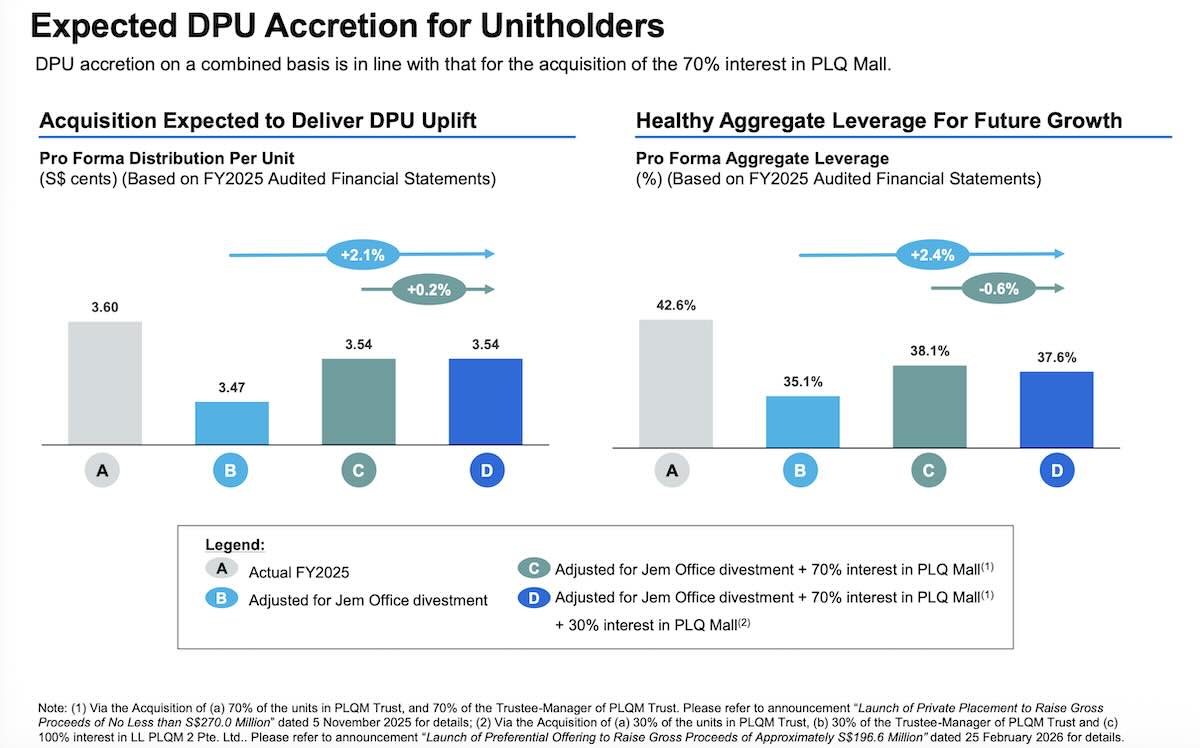

#1 - Acquisition expected to be marginally accretive

The acquisition of the remaining 30% stake in PLQ Mall is expected to be marginally accretive, with distribution per unit (DPU) projected to increase by about 0.2%. On a combined basis, including the earlier acquisition of the 70% stake in November 2025, the full transaction is estimated to be 2.1% DPU accretive on a pro forma basis.

Based on the pro forma figures, DPU would have increased to about 3.54 cents for the financial year ended 30 June 2025.

#2 - Gearing remains little changed post transaction

Part of the proceeds from the preferential offering will also be used to repay existing debt. Around S$82.8 million will go towards debt reduction, which is expected to lower the REIT’s aggregate leverage slightly to 37.6%, from 38.1% currently.

However, if perpetual securities of S$320 million are included, the effective gearing level remains elevated at around 46%.

Following the refinancing, Lendlease REIT is also expected to record interest cost savings of about S$2.0 million per year, which should provide some support to future distributions.

What would Beansprout do?

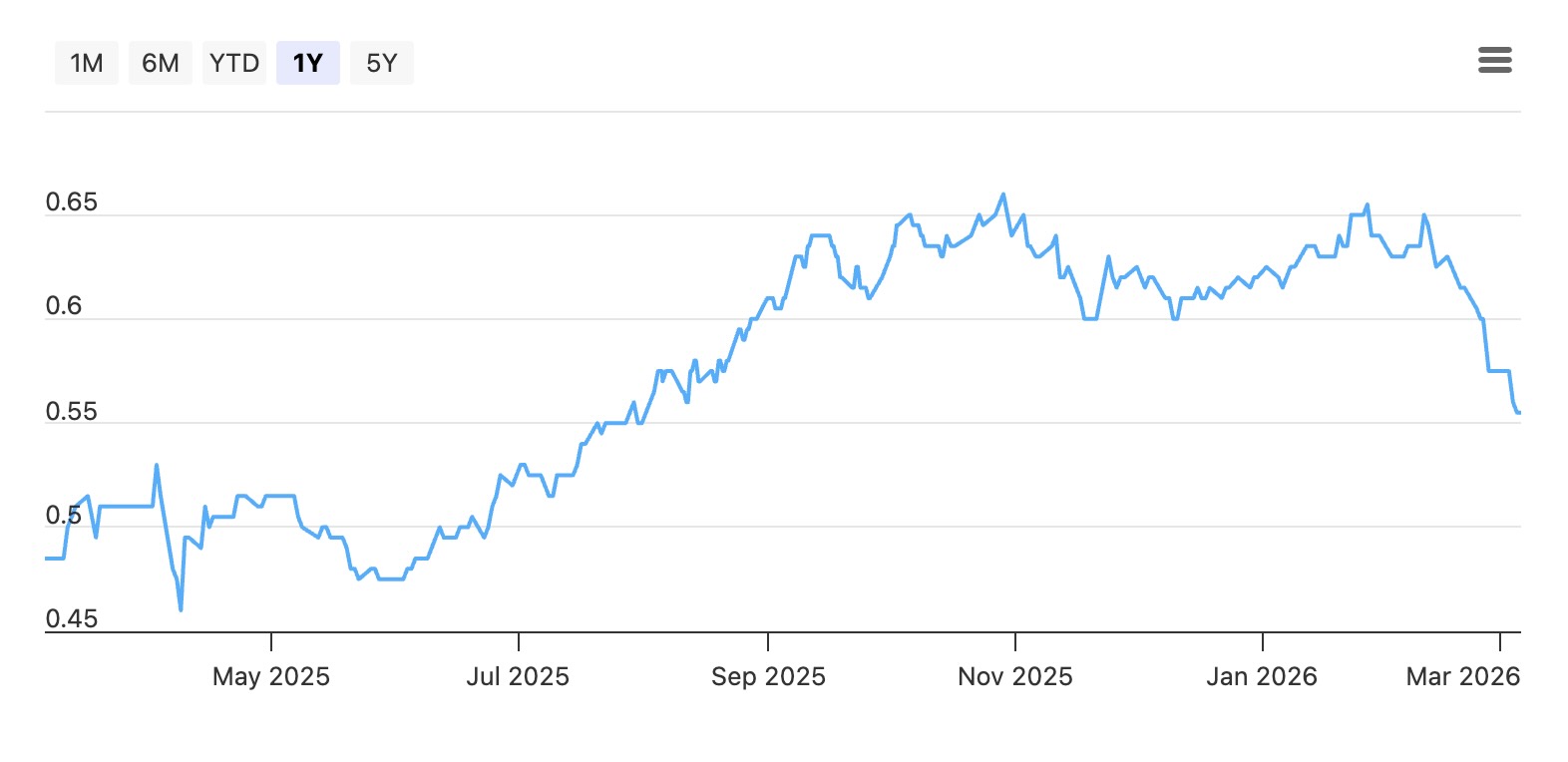

Lendlease REIT has underperformed the broader Singapore market year-to-date, with its unit price down about 11.2% since the start of the year.

With the preferential offering announced to fund the acquisition of a 30% stake in PLQ Mall, entitled unitholders can subscribe for 119 preferential units at S$0.558 each for every 1,000 units held.

The move to acquire full ownership of PLQ Mall is in line with Lendlease REIT's Singapore-focused growth strategy, and is intended to strengthen income stability by increasing exposure to suburban retail assets.

Full ownership of PLQ mall can also help to drive greater management control, including asset enhancement initiatives that may life rental rates.

However, the transaction is expected to be only marginally accretive, with the acquisition of the remaining 30% stake expected to lift DPU by about 0.2%.

In addition, Lendlease REIT's gearing level (including perpetual securities) remains high post the transaction, which may limit its ability to further grow its distributions without raising capital.

At the issue price of S$0.558, Lendlease REIT offers a historical distribution yield of about 6.3%, which is higher than several Singapore retail REIT peers.

In comparison, CapitaLand Integrated Commercial Trust (CICT) yields about 4.9%, Frasers Centrepoint Trust about 5.4%, and Suntec REIT around 5.1%.

Lendlease REIT's share price of S$0.555 as of 9 March 2026 is close to preferential offering. issue price of S$0.558.

If Lendlease REIT’s share price falls further below this level, Lendlease REIT's unitholders who are interested to buy additional units may be able to acquire more units from the market than to subscribe to the preferential offering at S$0.558 per unit, while taking into consideration brokerage and other transaction costs.

The underwriting banks would then have to take up units that are not taken up by eligible unitholders. In this scenario, there might be a potential subsequent overhang to the price of Lendlease REIT.

Overall, given that the transaction results in only a modest uplift in distribution per unit while overall gearing remains elevated, we are less enthusiastic about the preferential offering.

The preferential offering opens on 10 March 2026 at 9:00 a.m. and closes on 18 March 2026 at 5:30 p.m.

Recently, we shared that Singapore REITs are likely to benefit from falling interest rates.

To screen for Singapore REITs with lowest price-to-book valuation or highest dividend yield, check out our best Singapore REIT screener.

If you are new to investing in Singapore REITs, you can start to learn more about Singapore REITs here.

If you prefer diversification without picking individual REITs, you can also gain exposure through Singapore REIT ETFs.

Related links:

Check out Beansprout's guide to the best stock trading platforms in Singapore with the latest promotions to invest in Lendlease REIT.

Enjoyed this insight? Follow Beansprout on Telegram, Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments