How we pick growth stocks and size them in our portfolios

Stocks

By Gerald Wong, CFA • 17 Jul 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

Learn how to pick growth stocks using a 4-stage investment process, from finding stock ideas to screening, research, entry price and exit rules.

What happened?

Finding stock ideas is easy.

The harder part is knowing which ideas deserve our capital.

This is especially important for the Opportunity Pot within Beansprout's four pots of wealth, where we look for companies that may grow meaningfully over the next one to three years.

The Opportunity Pot is not meant to capture every market move, nor is it where we take random punts based on headlines.

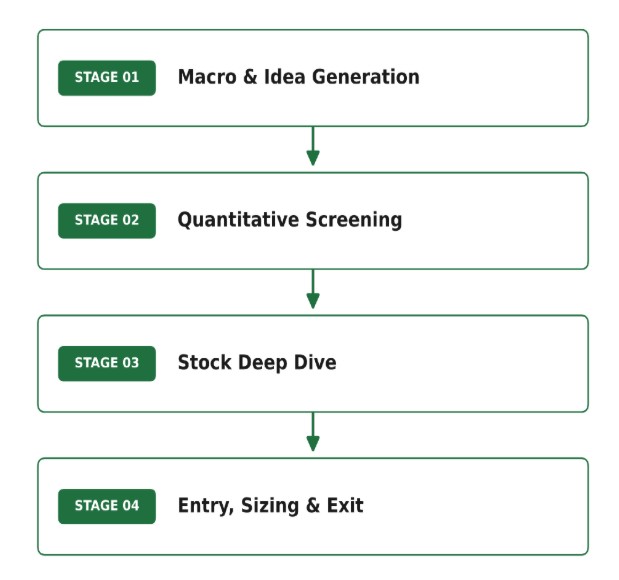

At Beansprout, we use a structured 4-stage process to move from investment idea to live position.

In this article, we explain how this process works, from finding stock ideas to screening, deep research, entry price, position sizing and exit rules.

What is the Opportunity Pot in Beansprout’s investment framework

The Opportunity Pot is where we place higher-conviction ideas that could deliver meaningful growth over the next one to three years.

These ideas may come from structural trends, earnings recovery, undervalued companies, corporate actions, or emerging market themes.

Unlike my Growth Pot, which focuses on broad market exposure through diversified ETFs, the Opportunity Pot allows me to express higher conviction in individual companies that I believe can outperform.

However, the Opportunity Pot should still be managed with discipline.

That is why the Opportunity Pot forms only one part of Beansprout's Four Pots of Wealth framework alongside the Liquidity Pot, Income Pot and Growth Pot.

It is deliberately kept smaller than the rest of the portfolio, so that it can express conviction without derailing our broader financial plan.

Every stock in the Opportunity Pot should have a clear investment thesis, an appropriate position size and predefined exit criteria before any capital is invested.

Having a disciplined investment process helps ensure that decisions are based on research and conviction rather than emotions or market noise.

How we pick and size growth stocks

Every investment considered for the Opportunity Pot follows the same structured process before capital is committed.

While our investment framework consists of six individual steps, these can be grouped into four practical stages that take a stock from an initial investment idea to a live portfolio position.

This allows me to gradually narrow hundreds of potential opportunities into a small number of companies that deserve a place in the Opportunity Pot.

The Opportunity Pot journey

| Stage | What we do |

|---|---|

| Stage 1 | Start with macro trends, industry developments and company-specific catalysts before identifying potential investment ideas. |

| Stage 2 | Screen companies based on revenue and earnings momentum, balance sheet strength and return on equity to narrow the list. |

| Stage 3 | Assess business quality, management, catalysts and valuation before developing a written investment thesis. |

| Stage 4 | Decide the appropriate position size, set an entry price and define when to review or exit the investment. |

Each stage acts as another filter.

Rather than trying to predict which stocks will perform best, I focus on following a repeatable process that improves the quality of every investment decision.

The sections below explain each stage in greater detail.

Stage 1: Find stock ideas from macro themes and market insights

We start with the big picture.

Markets do not move in isolation. They are shaped by interest rates, currencies, commodity prices, economic cycles, government policy and investor sentiment.

Instead of starting with a random list of stocks, we first ask: what are the major themes that could create opportunities?

For example, falling interest rates may support asset prices and companies with high funding costs.

Currency moves can affect exporters, importers and companies with overseas earnings.

Commodity prices can influence sectors such as energy, materials, construction and transport.

Regional growth trends also matter. If capital is flowing into ASEAN, China, India or another market, companies with exposure to these regions may benefit.

Policy changes can create opportunities too. Government spending, subsidies, regulation and national priorities often create winners and losers.

Alongside this top-down view, we use Beansprout’s own market insights.

This includes weekly market updates, sector commentary, community discussions, broker upgrades, analyst reports, corporate announcements, earnings results, dividend updates and M&A activity.

The strongest investment ideas often emerge when several independent sources point towards the same opportunity.

For example, a structural growth theme may also be supported by improving earnings, positive management guidance and favourable industry developments. When different pieces of evidence reinforce the same investment thesis, it gives me greater confidence to investigate the company further.

At this stage, the objective is not to decide what to buy.

The goal is to narrow the universe into a focused shortlist of around 20 stock ideas that fit a clear macro or thematic opportunity.

These companies then move to the next stage of the investment process, where they are screened using objective financial criteria before any deeper research begins.

Stage 2: Screen growth stocks using Beansprout’s three-factor stock screening framework

Not every interesting story becomes a good investment.

A company may benefit from an attractive industry trend, but still struggle with slowing earnings, excessive debt or weak profitability.

That is why the next step is to apply a quantitative screening framework before conducting deeper research.

At Beansprout, we look at three key factors: revenue and earnings momentum, balance sheet strength, and return on equity.

| Screening factor | What we look for | Why it matters |

| Revenue and earnings momentum | Positive or improving revenue and earnings growth | Shows whether the company is growing rather than shrinking |

| Gearing | Net debt/equity below 1.0x preferred, with caution if above 1.5x | Too much debt can make a company fragile |

| Return on equity (ROE) | ROE above 8% | Measures how well management uses shareholders’ capital |

These metrics do not tell me everything about a company.

However, they help eliminate businesses where the numbers do not support the investment story before I spend time conducting deeper research.

Revenue and earnings momentum

The first factor is revenue and earnings momentum.

We prefer companies where revenue and earnings are growing, or at least improving. Ideally, earnings should grow faster than revenue. This may suggest better efficiency, stronger margins, or operating leverage.

Balance sheet strength

The second factor is balance sheet strength.

Growth often requires companies to invest.

A company may need to build new capacity, expand into overseas markets, develop new products, hire more employees or acquire another business.

Debt is not always bad, but too much debt can become a problem when interest rates rise, cash flows weaken, or refinancing conditions tighten.

As a guide, we prefer companies with net debt to equity below 1.0x. If gearing rises above 1.5x, we would need stronger evidence that the company has stable cash flows to support it.

Return on equity (ROE)

The third factor is return on equity, or ROE.

ROE measures how effectively a company generates profit from shareholders’ capital. A higher ROE can indicate that the company has a stronger business model, better pricing power, or more disciplined management.

To move forward, a stock should ideally pass all three checks.

There is some room for judgement. For example, a company may be strong in growth and returns, but temporarily stretched on gearing because of an acquisition.

In that case, we may keep it on a watchlist rather than discard it immediately.

The key is to apply the screen consistently rather than lowering the criteria because a stock is popular or its share price has already risen.

By the end of this stage, the broad list of investment ideas should have been narrowed into a focused shortlist for deeper qualitative research.

For a deeper look at the exact filters we use, read our full guide to the Opportunity Pot stock screening framework, where we explain how we assess liquidity, revenue growth, earnings momentum, gearing and ROE before a stock moves into deeper research.

You can also check out the stocks that screen well using this framework using Beansprout's Opportunity Pot stock screener.

Stage 3: Research growth stocks through business quality, catalysts and valuation

Screening helps us find companies that look promising on the surface.

However, strong financial metrics alone are not enough to justify buying a stock.

Numbers tell me what has happened. But, it does not tell us whether the business can keep growing, whether management can execute, or whether the stock has enough upside to justify the risk.

This is where I conduct a deeper assessment of the company's competitive position, management team, growth catalysts and valuation.

The first area we look at is business quality.

The first question I ask is whether the company has a high-quality business that can continue creating value over the long term.

We want to understand what the company does, how it makes money, who its customers are, and why customers choose it over competitors.

More importantly, we want to know whether its competitive advantage is sustainable.

For example, does the company benefit from scale, brand strength, cost leadership, intellectual property, network effects, regulatory barriers, or long-standing customer relationships?

The stronger and more durable these competitive advantages are, the more confidence I have that the company can continue growing over time.

The second area is management quality.

Even great businesses require capable management teams.

Where possible, we look at results briefings, investor days, company visits or management commentary.

We want to understand how management thinks, not just what management reports.

Some questions matter more than others.

- Has management delivered on past guidance?

- Has capital been allocated sensibly between dividends, buybacks, acquisitions and reinvestment?

- Does management understand the risks in the business?

- Are they honest when conditions become more difficult?

Strong management teams are often willing to make difficult decisions early rather than delaying problems.

The third area is growth catalyst identification.

A stock can remain cheap for a long time if nothing changes.

Catalysts are the events or developments that may cause the market to revalue the company.

These can include stronger earnings, margin recovery, new product launches, market expansion, cost optimisation, restructuring, asset sales, share buybacks, special dividends, M&A activity, or policy support.

Understanding the catalyst also helps me estimate when the investment thesis is likely to play out.

The fourth area is valuation.

Finally, I assess whether the share price already reflects the company's future prospects.

We do not want to buy a stock just because it has a good story. Even an outstanding business can become a poor investment if I pay too high a price.

We want to see enough upside to justify the risk.

Depending on the company, this may involve looking at price-to-earnings, EV/EBITDA, dividend yield, price-to-book, discounted cash flow, or valuation against historical averages and peers.

We also consider different scenarios.

- In the base case, what do we think the company is worth if the thesis plays out reasonably well?

- In the bear case, what happens if earnings disappoint, margins weaken, or the catalyst does not appear?

- In the bull case, what could the stock be worth if the outcome is better than expected?

Thinking through different scenarios helps me compare the potential upside against the downside before investing.

Develop an investment thesis

After completing my research, I summarise everything into a written investment thesis.

Writing the thesis forces me to explain why I want to own the company before investing.

If I cannot explain the investment clearly, I probably do not understand the business well enough yet.

My investment thesis usually answers five questions.

| Element | Key question |

|---|---|

| Investment rationale | Why am I interested in this company now? |

| Growth catalysts | What could drive the share price higher? |

| Key risks | What could cause the investment thesis to fail? |

| Valuation | What do I believe the company is worth? |

| Exit strategy | What would cause me to sell? |

This written investment thesis also serves as a reference point after I invest.

Rather than reacting to every headline or share price movement, I can compare new information against my original investment thesis to determine whether anything has fundamentally changed.

By the end of Stage 3, we should have a concise investment thesis.

It should explain the theme, the catalyst, the valuation, the risks, and what would make us change our mind.

Only companies with a clear investment thesis move on to the final stage of the investment process, where I decide how much to invest and how the position fits within the Opportunity Pot.

Stage 4: Set stock entry price, position size and exit rules

Knowing what to buy is only half the job.

A good stock idea can still become a poor investment if we overpay, size it too aggressively, or fail to exit when the thesis breaks.

That is why I decide on my entry price, position size and exit rules before buying.

Finding a good company does not automatically make it a good investment at any price.

Before buying, I first estimate what the company is worth and set an entry price that offers sufficient potential upside.

I do not want to chase a stock simply because the growth story sounds attractive.

If the share price has already moved sharply, I may wait for a better entry point or gradually build the position over time.

For a new investment, I may start with a smaller allocation and add when:

- the company delivers stronger results

- the growth catalyst becomes clearer

- my conviction increases

- the share price falls to a more attractive level

Size the position based on conviction

Once I have identified an acceptable entry price, I decide how much of the Opportunity Pot to allocate to the stock.

At Beansprout, we use a star rating to reflect our overall conviction in each Opportunity Pot idea.

The rating is based on everything we have learned from the earlier stages, including the company's financial performance, business quality, management, growth catalysts and valuation.

Higher conviction allows me to allocate a larger portion of the Opportunity Pot, while lower conviction results in a smaller position or no investment at all.

| Star rating | Conviction | Typical allocation within the Opportunity Pot |

|---|---|---|

| ★★★★★ | Highest conviction | 15% to 25% |

| ★★★★☆ | Strong conviction | 8% to 20% |

| ★★★☆☆ | Moderate conviction | 3% to 10% |

| ★★☆☆☆ | Low conviction | Reduce or exit the position |

| ★☆☆☆☆ | Avoid | 0% allocation |

These ranges are guidelines rather than fixed allocations.

Even if two companies receive the same rating, I may invest different amounts depending on factors such as liquidity, diversification and the overall balance of the Opportunity Pot.

Regardless of conviction, I keep a hard cap of 25% for any single position within the Opportunity Pot.

This ensures that one investment cannot dominate the portfolio or significantly derail long-term performance if the investment thesis proves incorrect.

Set a clear return target before investing

For every stock, I document the expected return and investment horizon before buying.

Having a clear return target helps me stay disciplined throughout the investment journey. It reduces the temptation to hold a stock indefinitely simply because I already own it, or to chase short-term price movements.

Instead, I compare every investment opportunity against a consistent set of expectations before committing capital.

| Metric | What I aim for |

|---|---|

| Minimum upside before investing | 15% to 20% |

| Target annualised return | 8% to 12% |

| Investment horizon | 1 to 3 years |

| Valuation basis | Bottom-up fundamental analysis |

These metrics work together.

I generally look for at least 15% to 20% upside to my estimate of fair value before initiating a position. This provides a margin of safety if business conditions become more challenging than expected.

Over a one-to-three-year investment horizon, I aim for an annualised return of around 8% to 12%, although actual returns will depend on market conditions and how quickly the investment thesis plays out.

My valuation is based on the company’s underlying earnings, balance sheet, cash flows and growth prospects rather than short-term share price movements.

By estimating the company’s fair value first, I can decide whether the current price offers an adequate margin of safety.

Monitor the investment and know when to exit

Buying a stock is not the end of the investment process.

Companies continue to report earnings, industries evolve and new information becomes available.

Rather than monitoring the share price alone, I regularly review whether the original investment thesis remains intact.

One of the most difficult parts of investing is knowing when to sell. That is why I define my exit criteria before buying the stock.

Some of the situations that may lead me to reduce or exit a position include:

- The investment thesis is broken. The original reasons for owning the company no longer apply because of changes in management, industry structure or competitive position.

- The stock reaches my estimate of fair value. If most of the expected upside has already been realised, I may trim or exit the position.

- A better investment opportunity becomes available. Capital is limited. If I identify another company offering a better combination of upside and risk, I may redeploy part of my portfolio.

- The company's fundamentals deteriorate. Rising debt, weakening earnings, declining cash flow or repeated execution issues may indicate that the original thesis is no longer valid.

- The position becomes too large. A strong share price performance may cause a stock to exceed its intended portfolio allocation. In such cases, I may rebalance the position back to an appropriate size.

Importantly, I do not automatically sell simply because a share price falls.

If the decline is caused by a broad market correction and the company's long-term fundamentals remain intact, I may continue holding the investment.

Instead of reacting emotionally to short-term price movements, I focus on whether the facts supporting the investment have changed.

By documenting my investment thesis before buying, I have a clear framework for deciding whether to continue holding, increase my position or exit altogether.

How to use this stock investment process before buying growth stocks

The Opportunity Pot is not a place for guesses.

Every stock we own has passed through each stage of the investment process, with no shortcuts.

The table below summarises how an initial idea may eventually become a position in the Opportunity Pot.

Stage | Step | Process | Output |

|---|---|---|---|

| 01 | Idea generation | Company and industry news, research, conferences and investment themes | Broad list of investment candidates |

| 02 | Quantitative screening | Revenue and earnings momentum, balance sheet strength and return on equity | Focused shortlist |

| 03 | Qualitative screening and investment thesis | Business analysis, management assessment, industry discussions and the five-factor scorecard. Document the rationale, catalysts, risks, valuation and exit conditions | Deeper understanding of the company. Only the strongest ideas advance |

| 04 | Portfolio construction and risk management | Set the entry price, expected return and position size based on conviction. Monitor the thesis, review the valuation and apply sell discipline | Final Opportunity Pot position. Protect capital and compound returns |

Before buying, I should be able to answer a few important questions clearly.

- Which macro or thematic trend does this stock fit?

- Did it pass the quantitative three-factor screen?

- What is the catalyst, and when do we expect it?

- What are the entry price, target price and stop loss?

- Why is this a better use of capital than other stocks on the shortlist?

I should also know how much I am prepared to invest, what would cause me to sell and when I will review the position.

If I cannot answer these questions, it does not necessarily mean the company is a poor investment.

It may simply mean I need more evidence, a more attractive entry price or a clearer catalyst before putting capital behind the idea.

The Opportunity Pot rewards patience and preparation, rather than activity for its own sake.

What would Beansprout do?

I would use the Opportunity Pot within Beansprout's four pots of wealth only for stock ideas where the upside is clear, the risks are understood, and the process has been followed.

This means starting with the theme, applying objective screens, doing proper research, and writing down the entry price, target price and exit levels before buying.

You can screen for stocks that meet Beansprout’s 3-factor opportunity framework here, and learn more about our key market growth themes here.

I would also keep the Opportunity Pot deliberately sized, so that higher-growth ideas can add to returns without taking over the entire portfolio.

For me, the main takeaway is not to find more stock ideas. It is to become more disciplined about which growth stock ideas deserve capital.

The stock market will always offer new stories. The challenge is knowing which ones are worth acting on.

If you are looking for greater clarity on the markets and the investment decisions that matter, explore Beansprout Pro for our latest views, portfolio thinking and the reasoning behind each opportunity.

See how we would invest S$100,000 in Singapore stocks today with Beansprout Pro's model portfolio.

Which Singapore stocks are you watching as long-term growth themes gain momentum? Share your thoughts in the comments below or join the discussion in our Beansprout Telegram community.

Planning to invest in stocks? Check out Beansprout's guide to the best stock trading platforms in Singapore with the latest promotions and see the latest promotions and sign-up rewards available.

Enjoyed this insight? Follow Beansprout on Telegram, Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments