SK Hynix's US$28 billion Nasdaq listing: What it means for the AI theme

Stocks

By Ng Hui Min • 09 Jul 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

We do a deep dive at SK Hynix’s planned Nasdaq ADR listing, why it matters for the AI memory trade, and what investors should watch next.

What happened?

SK Hynix is preparing for one of the largest capital raises in stock market history.

The South Korean memory chipmaker plans to list American Depositary Receipts, or ADRs, on the Nasdaq, with the aim of raising up to US$28 billion, or about 43 trillion won.

If priced at the top of the range, it would become the largest ADR offering on record, surpassing Alibaba’s US$21.8 billion New York listing in 2014.

We've previously mapped out how value is created across the AI supply chain, where we highlighted SK Hynix as one of the leading suppliers of high bandwidth memory (HBM), a critical component that enables AI accelerators to process large models efficiently by providing the high-speed memory bandwidth needed for AI training and inference.

We've also discussed what's driving the broader AI investing theme, and asked the harder question of whether the AI rally has run ahead of fundamentals.

This listing also comes shortly after South Korea announced a major industrial investment push, with SK Hynix and Samsung Electronics at the centre of its semiconductor strategy.

Together, these developments show how strongly companies, governments and investors are betting on continued demand for AI infrastructure.

In this article, we look at SK Hynix’s listing plans, and what this could mean for AI and memory-focused investors.

#1 - Why is SK Hynix listing on Nasdaq?

SK Hynix already trades on the Korea Exchange in Seoul, so this is not a first-time listing.

Instead, it is planning an American Depositary Receipt, or ADR, listing on Nasdaq.

An ADR allows overseas shares to trade in the US in US dollars, making it easier for global investors to buy and sell the stock.

The main reason is access.

Large US funds may find it more costly and operationally harder to buy Korean-listed shares directly. An ADR reduces that friction and could help SK Hynix reach a wider investor base.

There is also a valuation angle.

SK Hynix has said it wants its valuation to better reflect its corporate value. This points to the “Korea discount”, where Korean-listed companies have often traded at lower valuations than comparable US-listed peers.

A Nasdaq listing could also put SK Hynix more directly beside other global semiconductor names such as Micron, which is already listed in the US.

Another possible benefit is future index inclusion.

By listing directly on Nasdaq, SK Hynix could become eligible for inclusion in the Nasdaq-100. If that happens, passive funds tracking the index, including large exchange-traded funds (ETFs) such as the Invesco QQQ Trust, may need to buy the stock.

This could create additional demand from large ETFs, including those that track the Nasdaq-100.

SK Hynix plans to issue up to 17.79 million new common shares, representing about 2.5% of its existing share base.

Each common share will be represented by 10 ADRs, meaning up to 177.9 million ADRs could be issued.

The fundraising target is up to US$28 billion, far larger than the US$9.6 billion to US$14.4 billion range reportedly floated earlier.

That sharp increase suggests investor appetite for AI memory exposure has grown quickly.

Trading on Nasdaq is targeted for 10 July 2026, with subscription and payment expected on 14 July. The new underlying Korean shares are expected to list on KOSPI on 29 July.

As with any large fundraising exercise, the final size and timetable may still change depending on investor demand.

#2 - Where SK Hynix may use the US$28 billion proceeds

Unlike a typical IPO, SK Hynix is not raising money to repay debt or build a general cash pile.

The ADR proceeds are earmarked for capacity expansion.

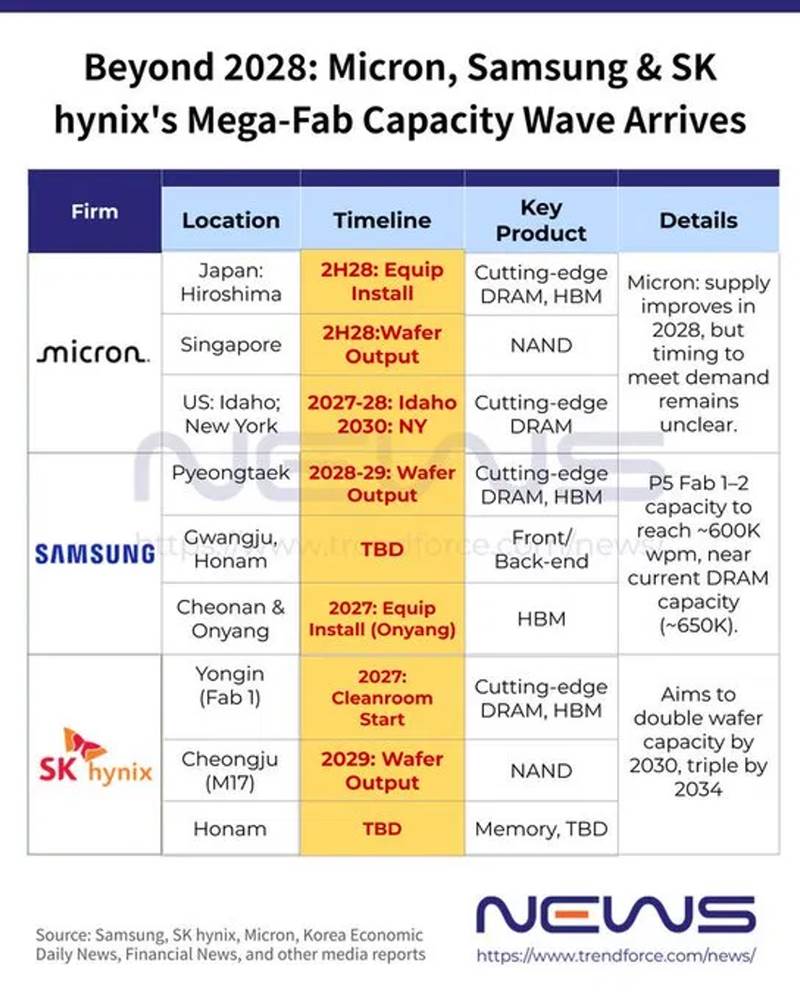

This includes building the first fab at the Yongin semiconductor cluster, constructing and equipping the Cheongju P&T7 advanced-packaging fab for AI memory such as HBM, and buying chipmaking equipment such as extreme ultraviolet (EUV) scanners.

This matters because advanced packaging and HBM capacity are critical bottlenecks in the AI supply chain.

But the ADR raise is only one part of a much bigger story.

Just days before SK Hynix’s filing, South Korea announced a major national investment plan centred on semiconductors, physical AI and AI data centres.

Samsung Electronics and SK Hynix are expected to play central roles, with both companies committing large sums toward new chip fabrication capacity in South Korea.

For SK Hynix, this includes plans to accelerate its Yongin cluster, build a new NAND flash factory in Cheongju, and invest in additional packaging capacity.

Put together, the ADR listing looks less like a standalone fundraising event and more like the financing leg of a government-backed semiconductor expansion plan.

South Korea is doubling down on its role in the global AI supply chain, with SK Hynix positioned as one of the key beneficiaries.

But there are risks too.

Large-scale capacity expansion has historically been a warning sign in the memory industry, especially if supply grows faster than demand.

There is also political risk, as some critics in South Korea have questioned whether new fab locations are being driven by commercial logic or regional political considerations.

The key things to watch are capital expenditure discipline, HBM demand, memory pricing and whether these new projects are executed without creating future oversupply.

#3 - Early demand for SK Hynix’s Nasdaq ADR appears strong

Early signs suggest that some large investors are interested in the listing.

In an SEC filing, three prominent investors, Baillie Gifford, Coatue Management and Situational Awareness LP, indicated that they could buy up to US$7 billion of the new ADRs as cornerstone investors. That would account for roughly a quarter of the entire offering.

A cornerstone investor is a large investor that signals interest before a listing is completed. This can give the market more confidence that there is demand for the offering.

Situational Awareness LP is especially notable because it is an AI-focused hedge fund founded by former OpenAI researcher Leopold Aschenbrenner.

The fund focuses on public equities that could benefit from the buildout toward more advanced AI, and its assets have reportedly grown sharply in under two years.

SK Hynix already makes up about 6.5% of its disclosed portfolio, even before this potential ADR purchase.

The presence of these cornerstone buyers sends an important signal.

It suggests that some specialist AI investors still see SK Hynix as a high-conviction way to gain exposure to the AI infrastructure buildout.

However, it also shows how much investor attention has become concentrated around the AI memory theme.

Strong cornerstone demand could support the offering, but it also shows how concentrated investor enthusiasm for AI memory has become.

#4 - What SK Hynix’s listing means for the AI memory trade

The SK Hynix ADR listing is more than just a large capital raise. It matters because SK Hynix sits at the centre of the AI memory trade, as one of the key suppliers of high bandwidth memory, or HBM, used in AI servers.

While graphics processing units (GPU) get most of the attention, HBM is needed to move data quickly enough for those GPUs to work efficiently. This gives SK Hynix an important role in the AI supply chain.

The listing could also draw closer comparisons with Micron, another major memory chipmaker exposed to AI demand. If SK Hynix trades at a discount despite its stronger HBM position, a Nasdaq listing could help narrow the valuation gap by improving access for global investors.

There is also a market structure angle, as a US dollar-denominated ADR would make SK Hynix easier for global funds to buy, while potential Nasdaq-100 eligibility could add passive demand.

For AI investors, the key question is whether this marks the start of a broader re-rating for memory stocks, or a sign that expectations around AI memory demand are becoming stretched.

A. Why SK Hynix is a key bottleneck in the AI supply chain

High bandwidth memory, or HBM, is one of the tightest supply constraints in the AI supply chain because it allows GPUs to move data fast enough for AI training and inference.

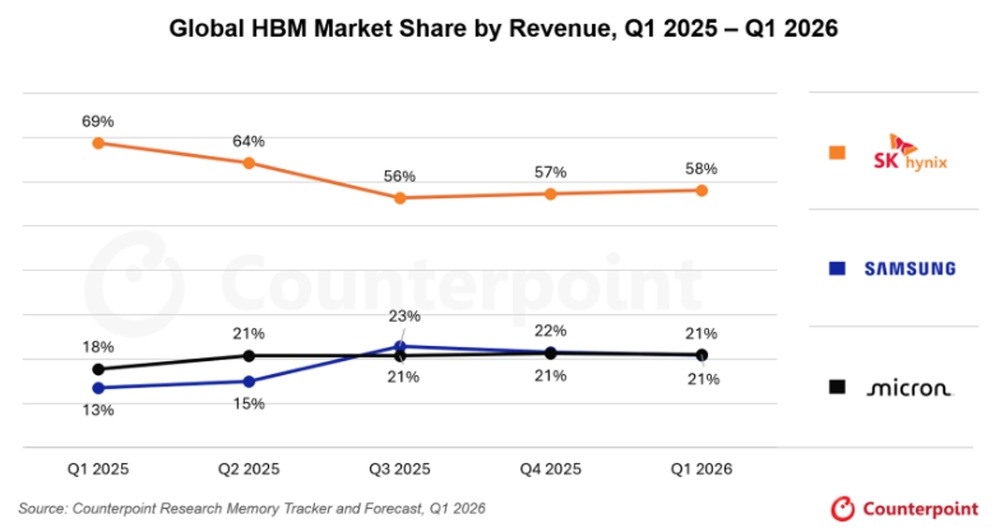

SK Hynix is estimated to hold around 50% to 60% of the global HBM market, ahead of Samsung and Micron, and is widely seen as Nvidia’s key HBM supplier.

This gives SK Hynix strong pricing power.

HBM is not an easy product for customers to switch away from, as it is highly specialised, difficult to manufacture and closely tied to GPU performance.

SK Hynix’s early lead in HBM3E has allowed it to benefit from a market where demand has exceeded supply for several years.

This is already showing up in its earnings, with SK Hynix now generating stronger semiconductor profits than Samsung’s chip division.

The ADR listing is therefore more than just a fundraising exercise.

It highlights where value is being captured in the AI buildout today: not just by GPU designers, but also by the memory suppliers that make AI infrastructure work.

It also explains why South Korea’s government has placed SK Hynix and Samsung at the centre of its national AI and semiconductor investment strategy.

B. Why the Micron comparison matters for SK Hynix ADR listing

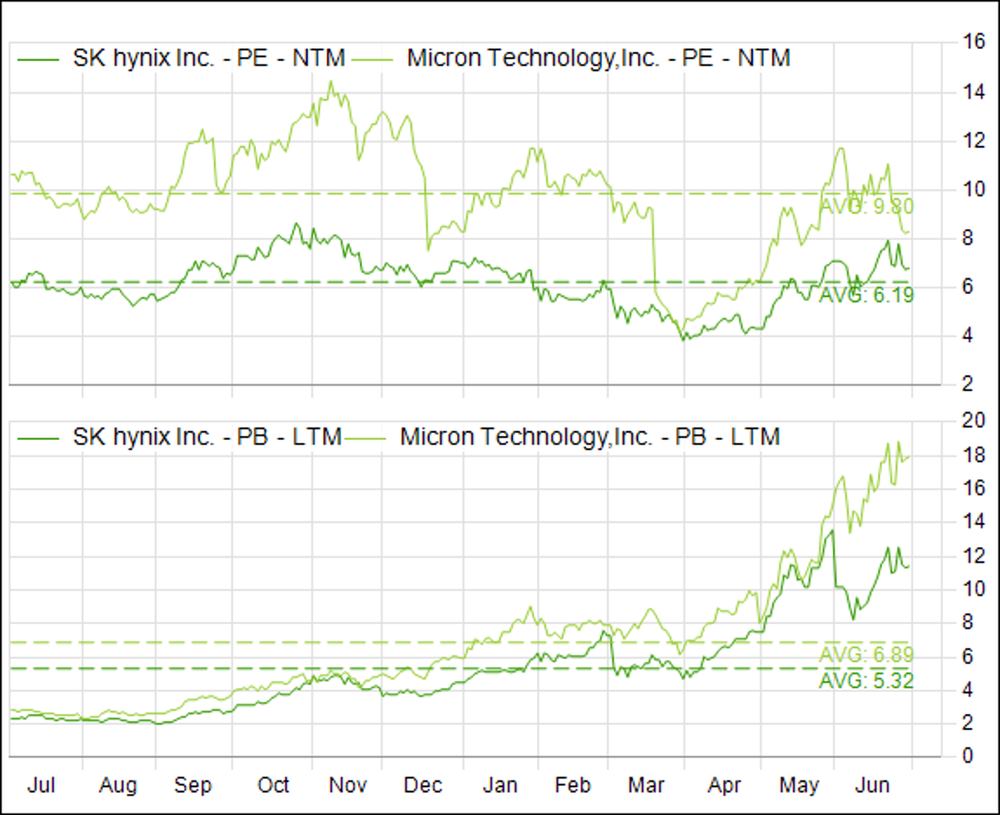

On paper, SK Hynix and Micron are both major memory chipmakers riding the same AI-driven HBM cycle.

Yet SK Hynix still trades at a lower forward earnings multiple than Micron, even though its HBM position appears stronger with its leading market share position.

That gap reflects the “Korea discount”, where Korean-listed companies have historically traded at lower valuations than comparable US-listed peers.

A Nasdaq ADR could help narrow this gap by making SK Hynix easier for global investors to access in US dollars.

It may also encourage investors to compare SK Hynix more directly with Micron, rather than viewing it mainly as a Korean market stock.

This does not mean the valuation gap will disappear overnight.

Memory remains a cyclical industry, and investors will still need to assess whether today’s HBM demand can support earnings growth beyond the current AI infrastructure boom.

But if global investors increasingly view SK Hynix as the leading HBM supplier to the AI ecosystem, the ADR listing could help SK Hynix attract a higher valuation.

C. What TSMC’s ADR tells us about SK Hynix’s US listing

SK Hynix is not the first Asian technology company to use a US listing to improve global investor access.

TSMC is the best example and offers a useful comparison.

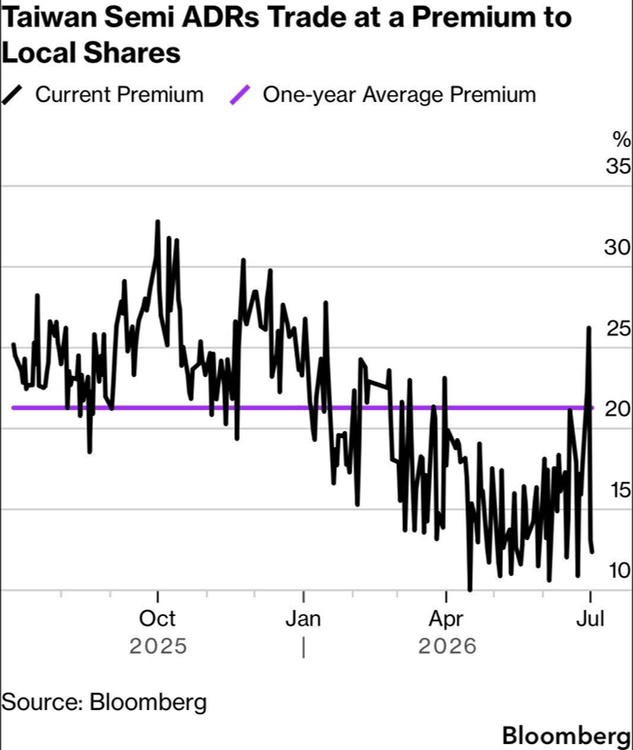

TSMC is listed in Taiwan, but it also has an ADR that trades in the US.

Its ADR has often traded at a premium to its Taiwan-listed shares because it gives US investors easier access to one of the world’s most important semiconductor companies, in US dollars and during US trading hours.

A premium means investors are paying more for the US-listed version of the shares than the underlying shares in the home market.

That premium has not been constant.

It has widened when US investor appetite for semiconductors and AI exposure was strong, and narrowed or even turned into a discount when sentiment toward the chip cycle weakened.

The lesson for SK Hynix is that a US listing can help reduce friction and attract more global capital, but it does not remove business cycle risk.

If AI memory demand remains strong, SK Hynix’s ADR could trade at a premium to its Korean shares, especially if US investors view it as one of the most direct ways to own the HBM theme.

But if memory prices weaken or investors worry about oversupply, the ADR premium could disappear quickly.

In other words, the Nasdaq listing may help close the access and valuation gap, but the longer-term share price will still depend on HBM demand, pricing power and capex discipline.

D. Could SK Hynix’s ADR trade at a premium?

If SK Hynix attracts strong demand from US AI-focused investors, its ADR could trade at a premium to its South Korea-listed shares, similar to what has happened with TSMC at different points in time.

That would mean investors are willing to pay extra for the convenience of accessing SK Hynix through Nasdaq.

Hedge funds may then try to profit from the price gap between the ADR and the underlying Korean shares. This is known as arbitrage.

However, the opposite could happen too.

If global risk appetite weakens, or if investors are unsure about how freely the ADRs can be converted into Korean shares, the ADR could trade at a discount instead.

This is why the structure of the ADR matters, not just the size of the offering.

Some investors may prefer to wait until trading begins and the pricing relationship between the ADR and South Korea-listed shares becomes clearer.

SK Hynix may also not be the last Asian memory company to explore this route.

Japan’s Kioxia is reportedly looking at its own ADR issuance in 2027, while interest in a possible Samsung Electronics ADR has also increased after SK Hynix’s announcement.

The bigger point is that US listings could become a way for Asian semiconductor companies to close the gap between where they are listed and where global AI capital is concentrated.

#5 - Is SK Hynix’s Nasdaq listing a peak signal or positive for the AI trade?

This is the key question for investors, and the answer is probably both.

A US$28 billion capital raise is a very large ask, especially if it comes close to other major AI-linked listings.

Some of the demand may come from investors trimming existing AI positions, including Micron or semiconductor ETFs, to make room for SK Hynix.

That could create short-term pressure on other AI memory or semiconductor names.

At the same time, the listing could also expand the pool of capital or new money flowing into the AI trade.

SK Hynix has been difficult for many US and global investors to access directly, so the Nasdaq ADR removes an accessibility barrier.

Potential Nasdaq-100 inclusion could also create passive buying demand, which would be additive rather than simply a rotation from other AI stocks.

The cornerstone investors also suggest that some AI-focused funds still see SK Hynix as a high-conviction way to gain exposure to AI infrastructure.

However, this cuts both ways.

Strong demand from specialist AI funds supports the bull case, but it also highlights how concentrated investor enthusiasm around AI memory has become.

The “peak signal” argument should not be dismissed either.

SK Hynix’s share price has already risen sharply, and large equity raises have sometimes appeared near the later stages of market enthusiasm.

There is also a risk that aggressive capacity expansion by SK Hynix, Samsung and others eventually leads to oversupply, as has happened in past memory cycles.

However, this does not look like a simple insider cash-out.

SK Hynix is raising capital to build fabs, advanced packaging capacity and equipment for a market where HBM demand remains tight.

Our view is that the ADR listing is best seen as a live stress test for the AI memory trade.

Strong bookbuilding, stable post-listing trading and eventual index inclusion would support the view that the AI trade is still expanding.

Weak demand or poor aftermarket performance would suggest investors are becoming more cautious about AI memory valuations.

Either way, the market reaction after SKHY starts trading will likely tell us more than trying to call the top in advance.

#6 - Key risks for SK Hynix and AI memory investors

The AI memory story looks structurally attractive, but it is not a one-way trade.

The biggest risk is that the capex cycle runs ahead of demand.

SK Hynix is raising capital to fund new fabs, advanced packaging capacity and chipmaking equipment, while South Korea’s broader semiconductor investment plan also points to a major capacity build-out from both SK Hynix and Samsung.

This is the kind of aggressive expansion that has historically preceded memory downcycles, especially when demand slows and chip prices fall.

Investors should also watch for early signs of scepticism around the AI infrastructure cycle.

Recent weakness in chip stocks shows how quickly sentiment can turn if the market starts to worry about excess AI capacity, slower hyperscaler spending or oversupply in memory chips.

There is also political risk.

South Korea’s national investment plan is partly tied to regional development goals, which could make execution more complex if fab locations or timelines are influenced by political considerations rather than purely commercial logic.

Finally, the ADR structure itself carries uncertainty.

If SK Hynix’s ADRs are not freely convertible into the underlying Korean shares, the ADR could trade at a persistent premium or discount, depending on investor demand, liquidity and arbitrage activity.

The key things to watch are HBM pricing, capacity additions, AI server demand, capex discipline, and how the ADR trades relative to the South Korea-listed shares once trading begins.

#7 - What to watch after SK Hynix ADR starts trading on Nasdaq

Once SK Hynix starts trading on Nasdaq, the early share price reaction will be important.

A stable debut would suggest that global investors still have strong appetite for AI memory exposure, especially through companies linked to HBM.

A sharp pullback, on the other hand, could suggest that investors are becoming more cautious about valuations across the AI supply chain.

I would also watch how the ADR trades relative to SK Hynix’s South Korea-listed shares.

If the ADR trades at a premium, it would suggest that investors are willing to pay more for the convenience of buying SK Hynix in the US.

If it trades at a discount, it could point to weaker demand, concerns about the ADR structure, or broader caution toward chip stocks.

Beyond the first few days of trading, the bigger question is whether HBM demand remains strong.

HBM pricing has been firm because supply has been tight, but investors will need to watch whether prices hold up as SK Hynix, Samsung and other memory companies add more capacity.

This is where capital discipline becomes important.

SK Hynix is investing heavily in new fabs, packaging facilities and equipment. If the company expands carefully, the new capacity could support future growth.

But if the industry adds too much capacity too quickly, it could eventually lead to oversupply and weaker memory prices.

Investors should also keep an eye on whether SK Hynix moves closer to Nasdaq-100 inclusion.

This could become another source of demand from passive funds, although it should be seen as a possible future catalyst rather than something guaranteed.

Overall, the post-listing performance will offer useful clues on whether the AI memory trade is still attracting fresh capital, or whether investors are starting to turn more selective.

What would Beansprout do?

For most Singapore investors, SK Hynix is still not an easy stock to access today, since it is not listed on SGX and is mainly available through South Korea-listed shares or over-the-counter routes.

That should change once the Nasdaq ADR starts trading, as investors will be able to buy it through most US market brokerage accounts.

Even for investors who do not plan to buy SK Hynix directly, the listing is worth watching because it is a useful barometer for the AI memory trade.

Strong demand for the ADR and a smooth path toward Nasdaq-100 inclusion would support the view that HBM remains one of the tightest bottlenecks in the AI supply chain.

A weak reception or sharp post-listing pullback would be a warning sign, especially given how much corporate and government capex is now tied to continued AI memory demand.

For investors considering direct exposure, we would treat SK Hynix as an Opportunity Pot stock rather than a core holding.

Its size, liquidity and earnings momentum should look strong after the ADR listing, but balance sheet strength and capital discipline need close monitoring given the scale of planned capex.

The AI memory story looks real, but memory remains cyclical, so position sizing matters and investors should avoid treating any AI-linked stock as a buy at any price.

For those who want more context, we have explained how AI is driving renewed interest in global markets and tech stocks and looked at whether the AI rally has more room to run.

You can also read our guide to the AI value chain and the companies powering each stage of growth.

If you are considering opening a brokerage account to invest in the US markets, new Moomoo users who sign up through Beansprout can receive a S$60 FairPrice voucher, S$20 worth of SK Hynix ADR fractional shares, and unlock up to S$1,200 in welcome rewards when they meet the funding requirements. Find out more about the Moomoo promotion here.

Are you watching the SK Hynix listing, or do you already have exposure to the AI memory trade through other names? Share your thoughts with us in the comments below or in our Telegram group!

Follow Beansprout on YouTube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments