Beyond Nvidia: The stocks powering the AI value chain

Stocks

By Ng Hui Min • 04 Jun 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

The AI boom is creating opportunities beyond Nvidia and chip stocks. We explain the AI value chain and the companies powering each stage of growth.

What happened?

Artificial intelligence (AI) stocks have been gaining momentum.

The Philadelphia Semiconductor Index is up 94.2% year to date.

Earlier, we looked at why artificial intelligence has become one of the biggest themes driving global markets.

We have previously highlighted AI and data centres as one of the key structural growth themes, supported by significant capital spending from hyperscalers and government initiatives to expand digital infrastructure.

As technology stocks continue to rally, we also discussed whether the AI gains are justified by stronger fundamentals or whether valuations have started to run ahead of earnings expectations.

The next question is where value is actually being created across the AI supply chain.

AI is far more than a handful of headline names. Behind every AI model, generated image and autonomous decision sits a complex network of chip designers, foundries, equipment makers, data centre operators, software providers and manufacturing partners.

Closer to home, Singapore-listed technology companies in semiconductor equipment, precision engineering and manufacturing services have also benefited as investors look for ways to gain exposure to the global AI buildout.

In this primer, we map out the AI value chain, explain how the different segments fit together, and share how we think about the opportunities and risks across each part of the ecosystem.

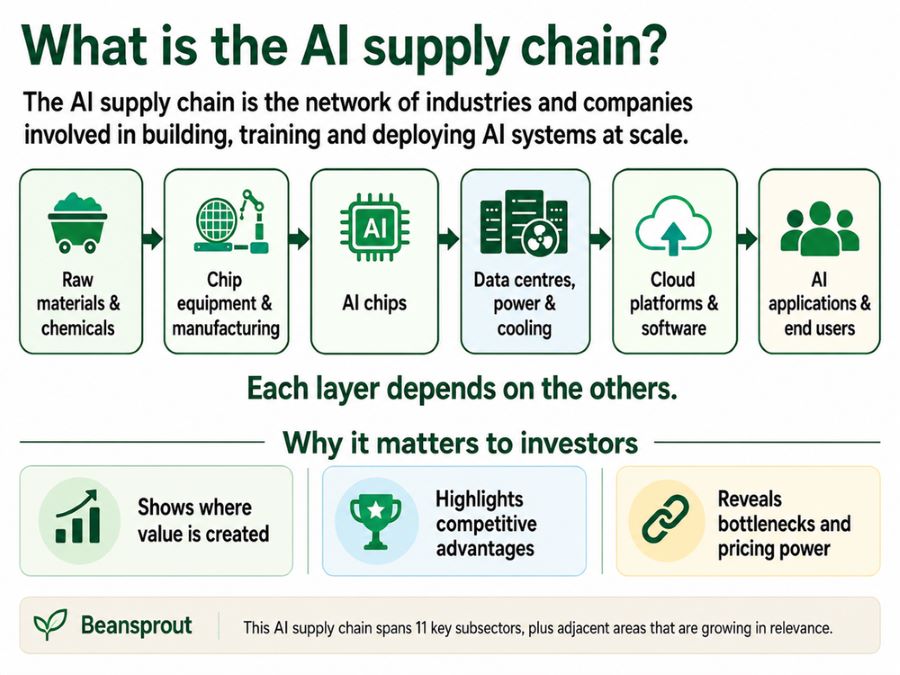

What is the AI supply chain?

The AI supply chain refers to the network of industries and companies involved in building, training and deploying AI systems at scale.

It starts with the raw materials, chemicals and equipment needed to make advanced chips.

It then moves into chip manufacturing, memory, servers, networking equipment, power systems, cooling infrastructure, data centres, cloud platforms and software applications that bring AI to end users.

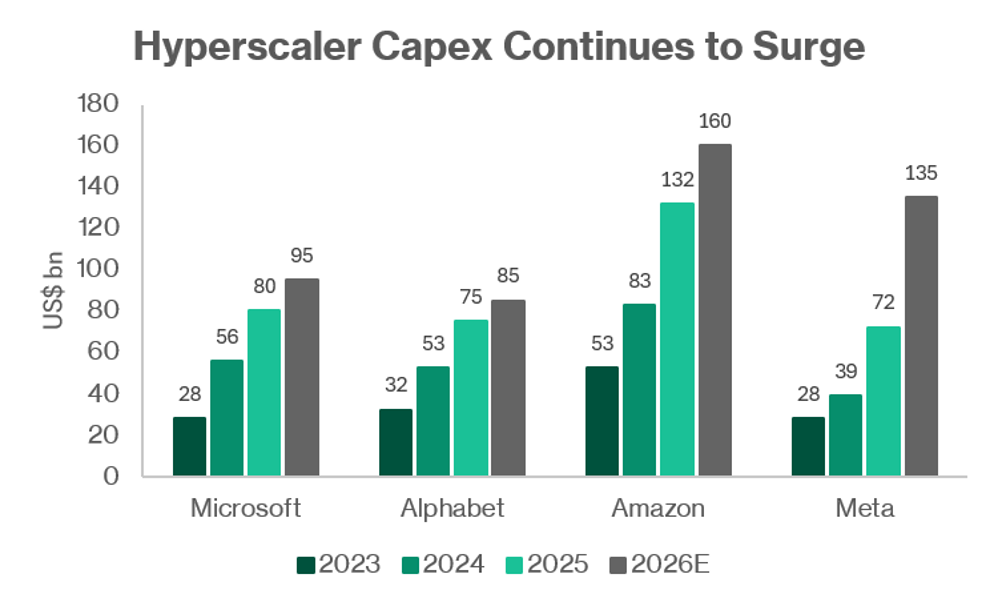

A large part of this demand is being driven by hyperscalers such as Microsoft, Amazon, Google and Meta, which are spending heavily to build the computing infrastructure needed for AI.

This capital spending flows through the AI value chain, supporting demand for advanced chips, AI servers, networking equipment, data centre power systems and cooling infrastructure.

Each layer depends on the others.

AI models cannot be trained without powerful chips. Chips cannot be manufactured without highly specialised equipment and materials.

Data centres cannot operate without reliable power, cooling and networking infrastructure. And AI applications cannot reach users without software platforms and digital services.

Understanding how these layers connect helps investors identify where value is being created, where competitive advantages are strongest, and where bottlenecks may give certain companies greater pricing power.

We have identified eleven key subsectors in the AI supply chain, along with a number of adjacent areas that are growing in relevance.

The AI supply chain: Subsector by subsector

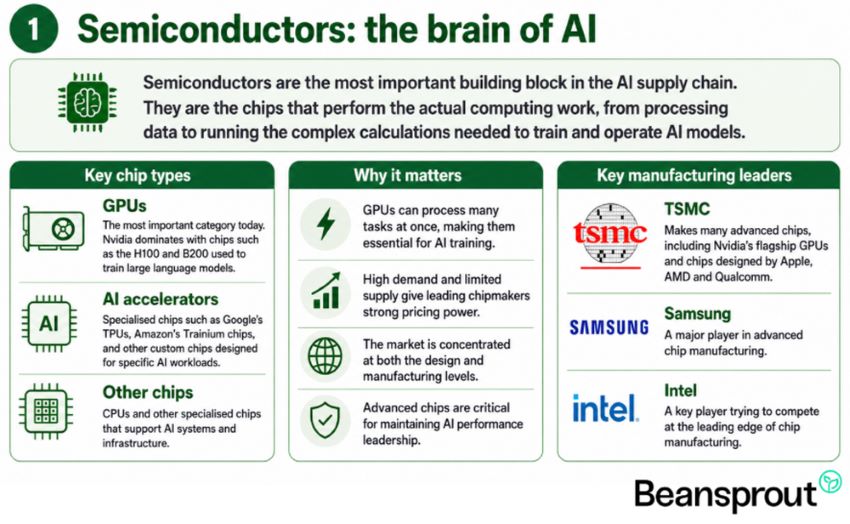

#1 - Semiconductors: the brain of AI

Semiconductors are the most important building block in the AI supply chain.

They are the chips that perform the actual computing work, from processing data to running the complex calculations needed to train and operate AI models.

The most important category today is the graphics processing unit, or GPU.

GPUs were originally designed for gaming, but their ability to process many tasks at once has made them essential for AI training.

Nvidia dominates this market with chips such as the H100 and B200, which are widely used to train large language models.

Beyond GPUs, there are also specialised AI accelerators, such as Google’s tensor processing units (TPUs), Amazon’s Trainium chips and other custom chips designed for specific AI workloads.

At the manufacturing level, production is highly concentrated.

Taiwan Semiconductor Manufacturing Company, or TSMC, makes many of the world’s most advanced chips, including chips designed by Nvidia, Apple, AMD and Qualcomm.

Samsung and Intel are the other major players trying to compete at the leading edge of chip manufacturing.

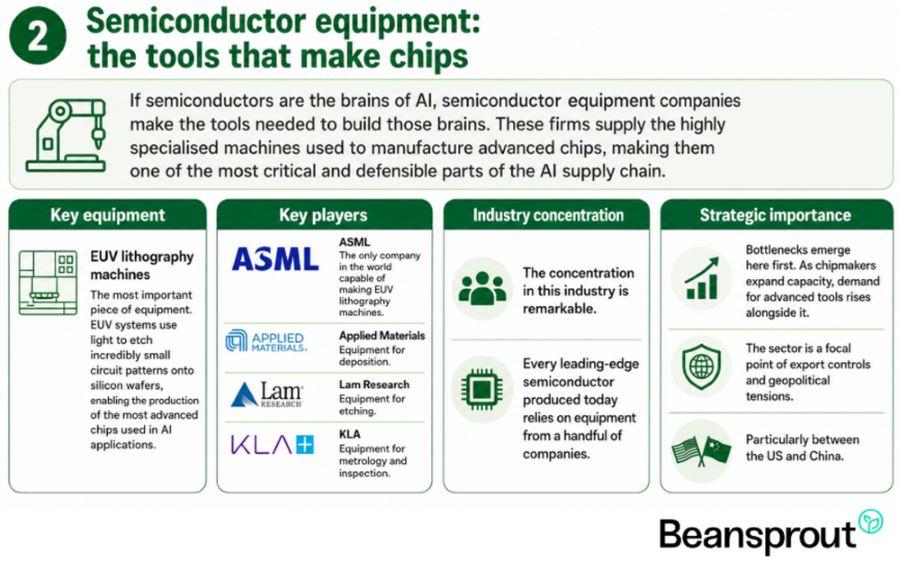

#2 - Semiconductor equipment: the tools that make chips

If semiconductors are the brains of AI, semiconductor equipment companies make the tools needed to build those brains.

These firms supply the highly specialised machines used to manufacture advanced chips, making them one of the most critical and defensible parts of the AI supply chain.

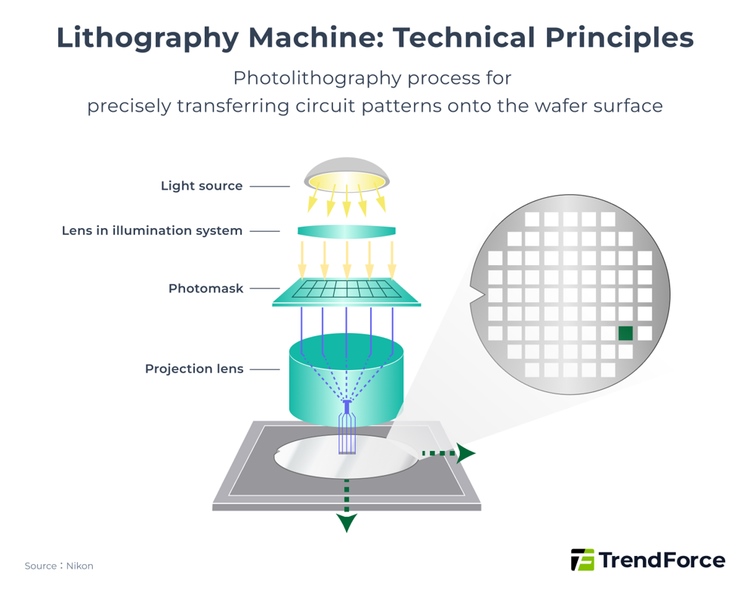

The most important piece of equipment is the extreme ultraviolet (EUV) lithography machine.

EUV systems use light to etch incredibly small circuit patterns onto silicon wafers, enabling the production of the most advanced chips used in AI applications.

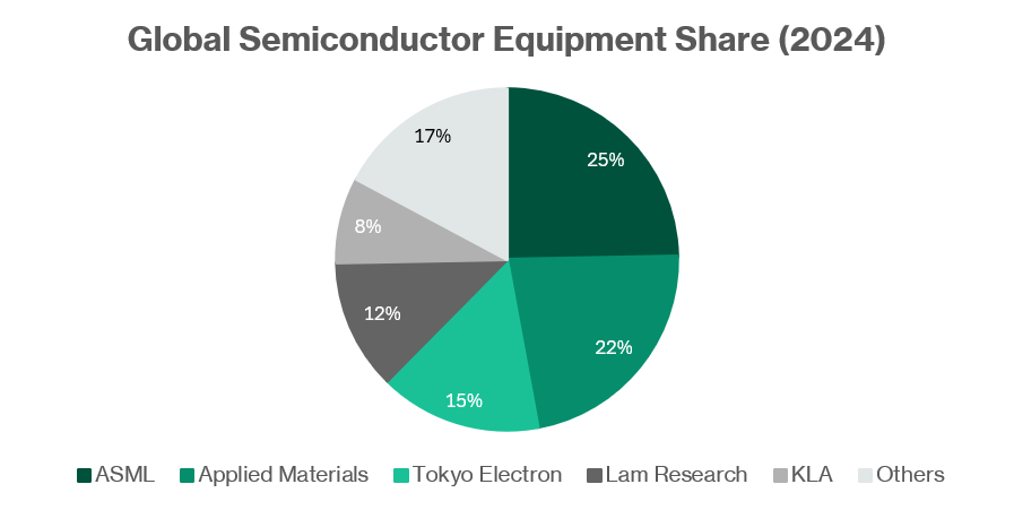

ASML is currently the only company in the world capable of manufacturing EUV lithography machines, giving it a unique position in the global semiconductor ecosystem.

Other key players include Applied Materials, Lam Research and KLA, which provide equipment for deposition, etching, metrology and inspection. These are essential steps in the chip fabrication process.

This part of the AI supply chain can be highly attractive because it is difficult to replicate.

Hence, the concentration in this industry is remarkable. Every leading-edge semiconductor produced today relies on equipment from a handful of companies.

Semiconductor equipment is often where AI-related bottlenecks emerge first. As chipmakers race to expand capacity, demand for advanced manufacturing tools rises alongside it. The strategic importance of these technologies has also made the sector a focal point of export controls and geopolitical tensions, particularly between the US and China.

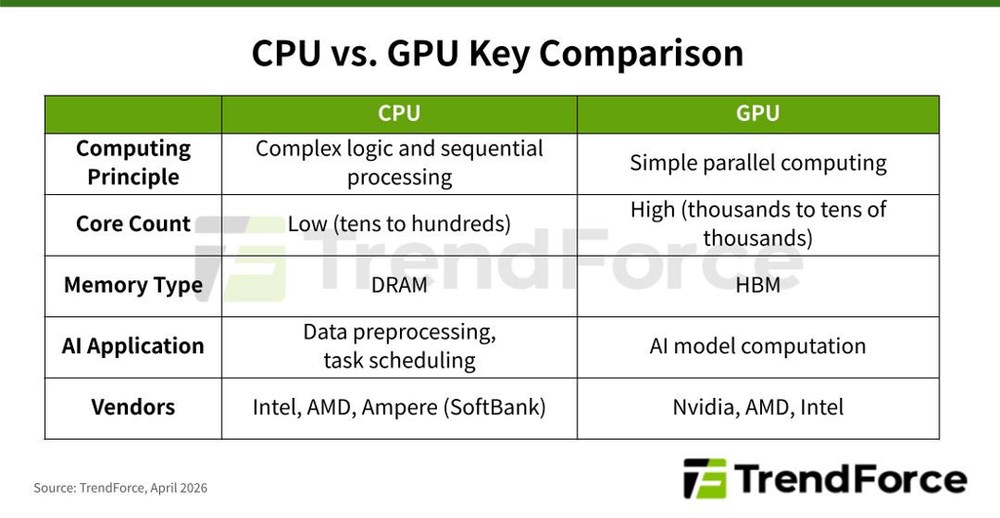

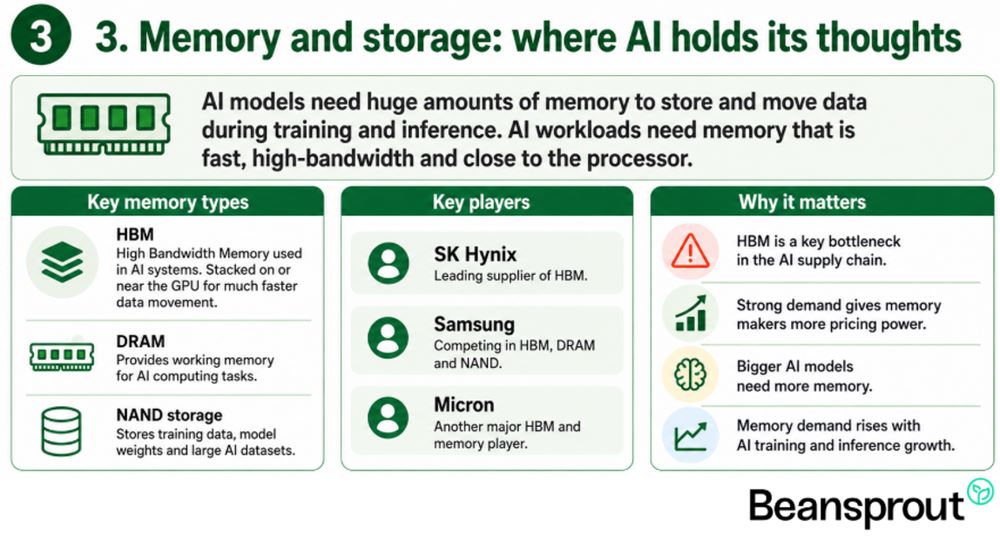

#3 - Memory and storage: where AI holds its thoughts

AI models need huge amounts of memory to store and move data during training and inference.

This is different from traditional computing. AI workloads require memory that is fast, high-bandwidth and located close to the processor.

High Bandwidth Memory, or HBM, is the key memory type used in AI systems. It is stacked vertically on or near the GPU, allowing data to move much faster than conventional memory.

SK Hynix is a leading supplier of HBM, with Samsung and Micron also competing in this market.

Traditional DRAM and NAND flash storage are also important because they store training datasets, model weights and large volumes of AI-related data.

HBM has become one of the key bottlenecks in the AI supply chain.

Strong demand has given memory makers greater pricing power, and as AI models become larger, memory requirements are likely to keep rising.

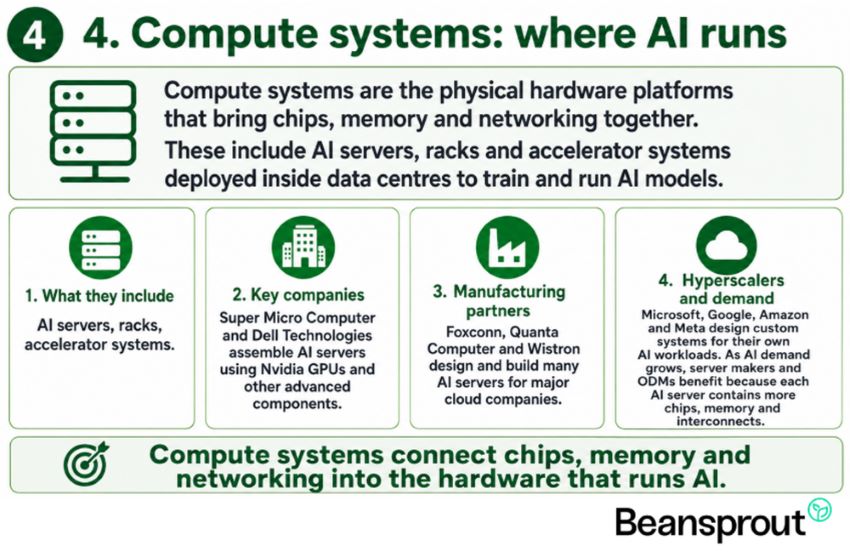

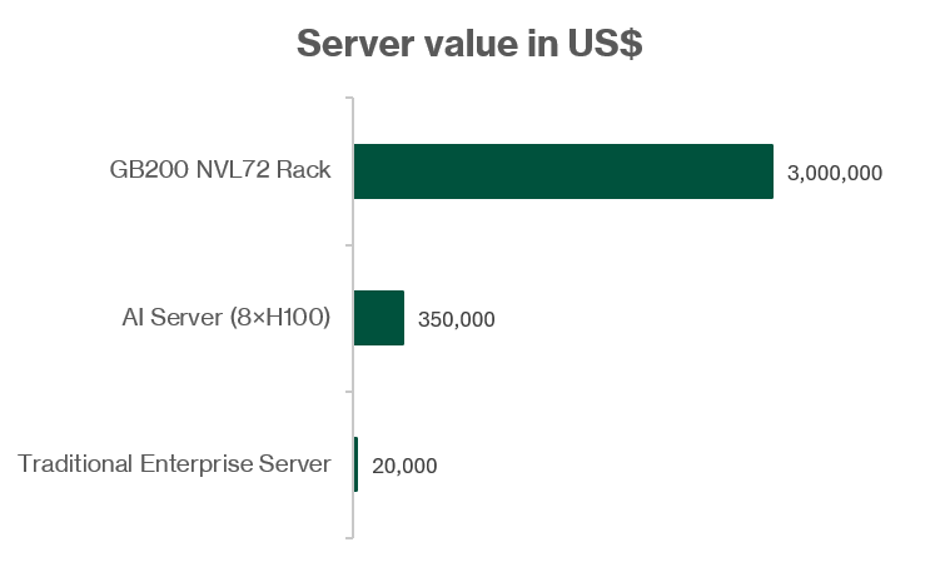

#4 - Compute systems: where AI runs

Compute systems are the physical hardware platforms that bring chips, memory and networking together.

These include AI servers, racks and accelerator systems that are deployed inside data centres to train and run AI models.

Companies such as Super Micro Computer and Dell Technologies assemble AI servers using Nvidia GPUs and other advanced components.

Taiwan-based manufacturers such as Foxconn, Quanta Computer and Wistron also play an important role, designing and building many of the world’s AI servers for major cloud companies.

The hyperscalers themselves, including Microsoft, Google, Amazon and Meta, also design custom systems for their own AI workloads.

As demand for AI computing grows, server manufacturers and original design manufacturers benefit from larger orders and higher-value systems, as each AI server now contains more chips, memory and interconnects than before.

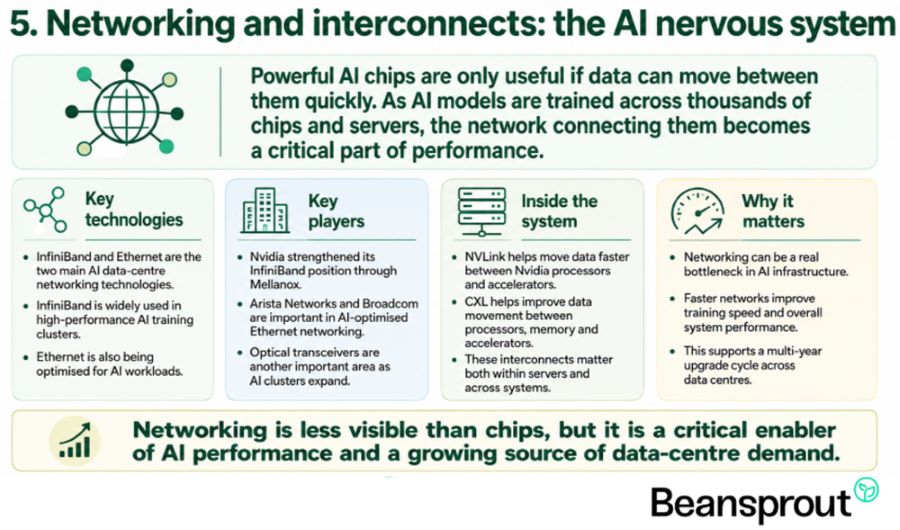

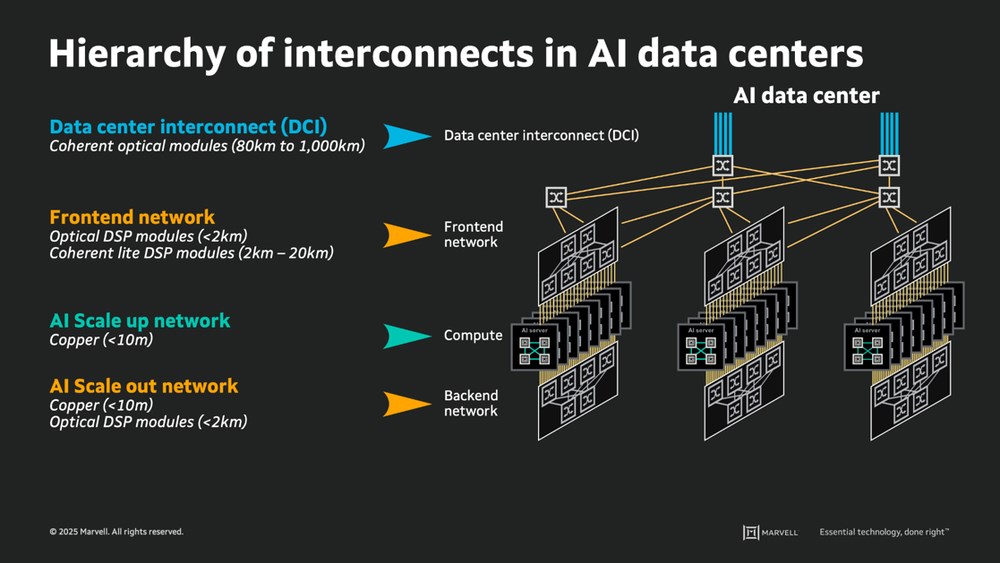

#5 - Networking and interconnects: the AI nervous system

Powerful AI chips are only useful if data can move between them quickly.

As AI models are trained across thousands of chips and servers, the network connecting them becomes a critical part of performance.

In AI data centres, InfiniBand and Ethernet are the two key networking technologies.

Nvidia’s acquisition of Mellanox gave it a strong position in InfiniBand, which is widely used in high-performance AI training clusters.

Arista Networks and Broadcom are important players in AI-optimised Ethernet networking.

Within servers and chips, technologies such as Nvidia’s NVLink and Compute Express Link, or CXL, help move data faster between processors, memory and accelerators.

Optical transceivers are another important area. These components convert electrical signals into light so data can travel quickly through fibre networks, and demand has risen sharply as AI clusters expand.

Networking is often less visible than chips, but it can be a real bottleneck. Faster AI networks help improve training speed and support a multi-year upgrade cycle across data centres.

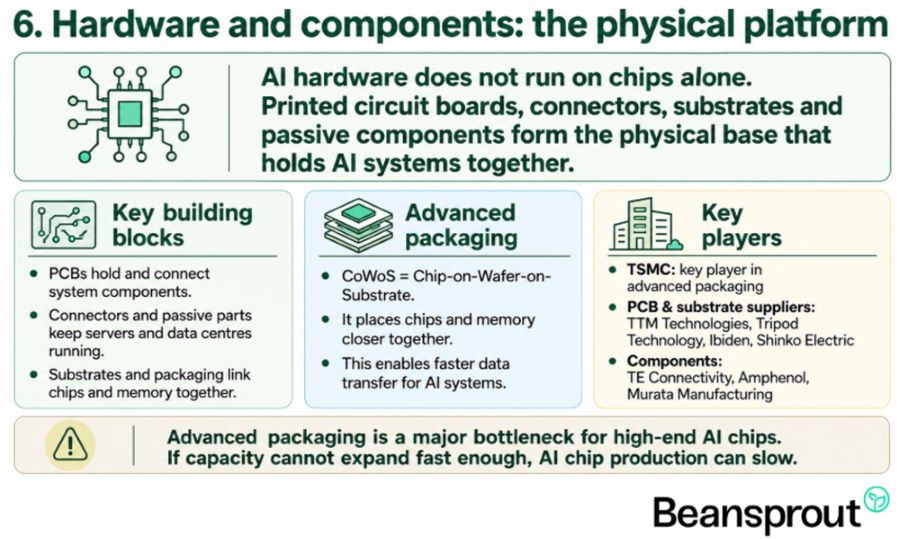

#6 - Hardware and components: the physical platform

AI hardware does not run on chips alone.

Printed circuit boards, connectors, substrates and passive components form the physical base that holds AI systems together.

As AI chips become more powerful, the hardware around them also needs to become more advanced.

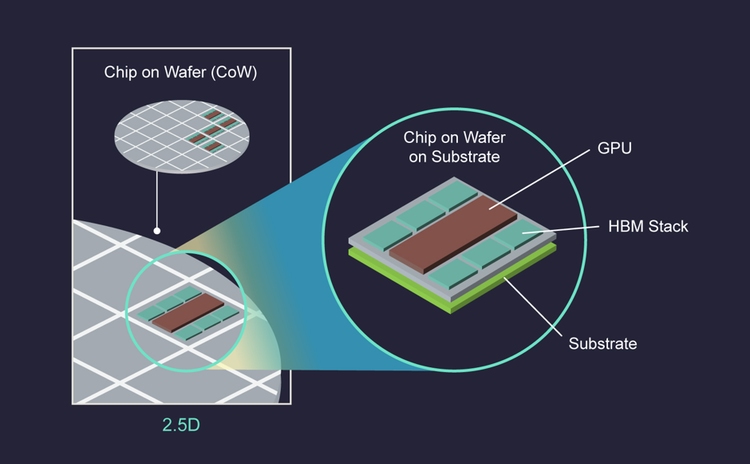

This includes advanced packaging technologies such as CoWoS (Chip-on-Wafer-on-Substrate), which allows multiple chips and memory components to be placed close together for faster data transfer.

TSMC is a key player in advanced packaging.

Printed circuit board (PCB) and substrate suppliers such as TTM Technologies, Tripod Technology, Ibiden and Shinko Electric also support the broader hardware ecosystem.

Connector and passive component makers such as TE Connectivity, Amphenol and Murata Manufacturing also supply essential parts used in AI servers and data centres.

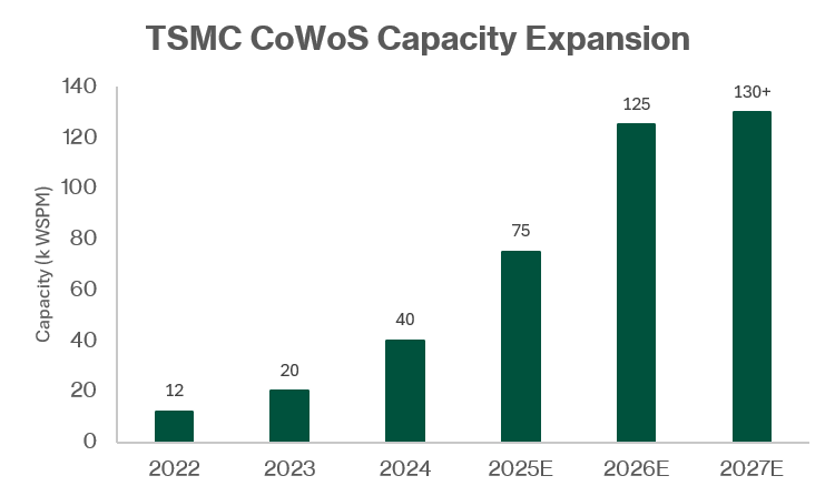

Advanced packaging has become a major bottleneck for high-end AI chips. If packaging capacity cannot expand fast enough, it can limit how quickly AI chipmakers scale production.

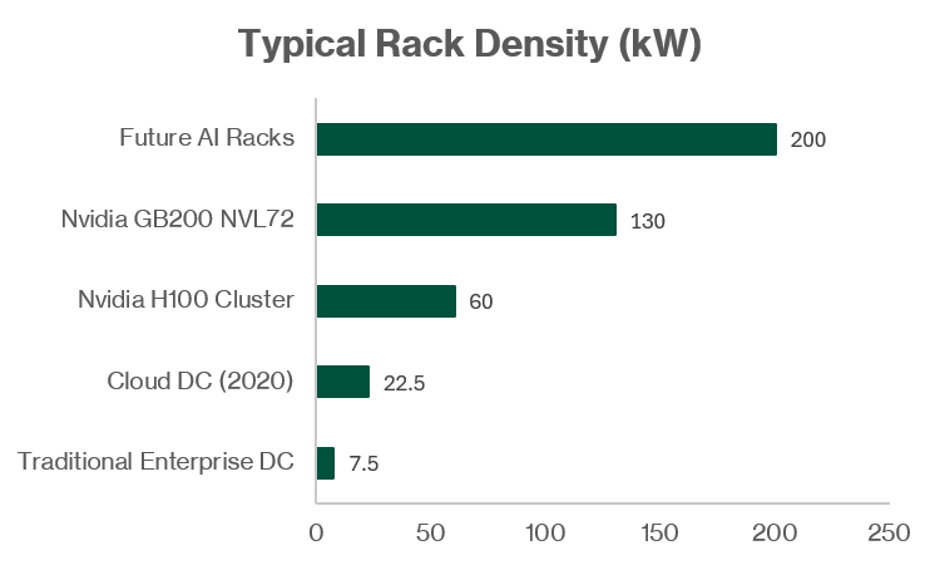

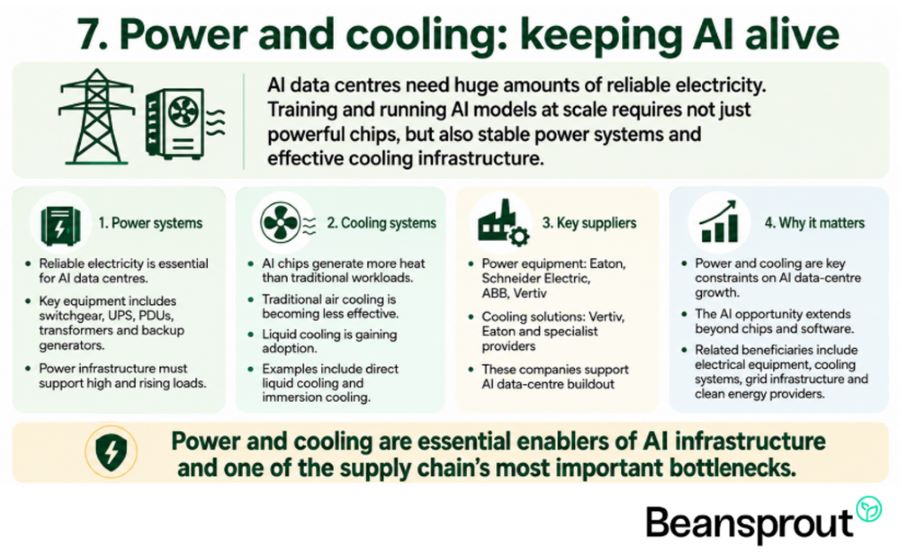

#7 - Power and cooling: keeping AI alive

AI data centres need huge amounts of reliable electricity.

They also need cooling systems that can handle the heat generated by powerful AI chips.

Training and running AI models at scale requires not just powerful chips, but also stable power systems and effective cooling infrastructure.

On the power side, data centres rely on equipment such as switchgear, uninterruptible power supplies, power distribution units, transformers and backup generators.

Major suppliers include Eaton, Schneider Electric, ABB and Vertiv.

On the cooling side, traditional air cooling is becoming less effective as AI chips generate more heat.

This is driving adoption of liquid cooling solutions, including direct liquid cooling and immersion cooling, supplied by companies such as Vertiv, Eaton and other specialist providers.

Power and cooling are becoming key constraints for AI data centre growth. This means the AI opportunity extends beyond chips and software to electrical equipment, cooling systems, grid infrastructure and clean energy providers.

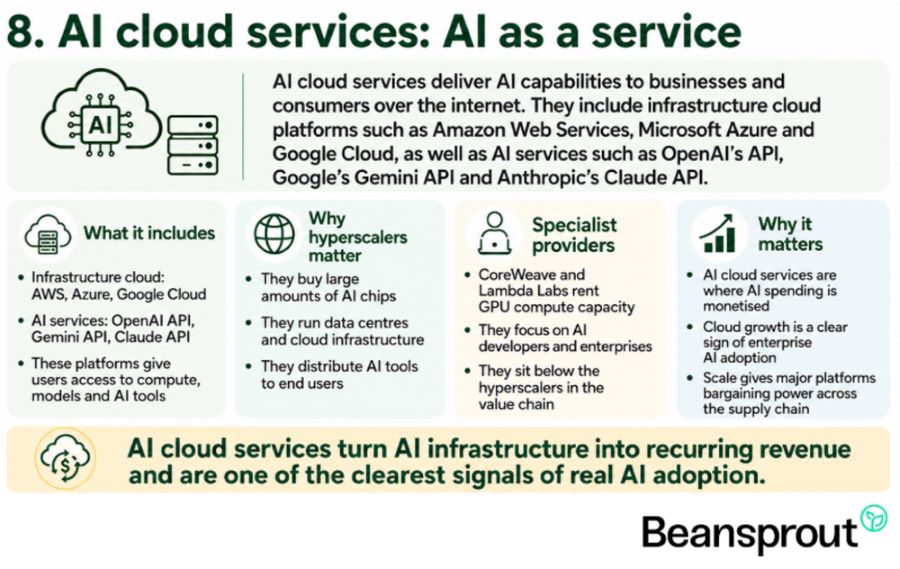

#8 - AI cloud services: AI as a service

AI cloud services are the platforms that deliver AI capabilities to consumers and businesses over the internet.

This includes infrastructure cloud platforms such as Amazon Web Services, Microsoft Azure and Google Cloud.

It also includes AI-specific services such as OpenAI’s API, Google’s Gemini API and Anthropic’s Claude API.

The hyperscalers are in a powerful position because they sit across multiple layers of the AI value chain.

They are among the largest buyers of AI chips, the operators of data centre infrastructure, and the distributors of AI tools to end users.

This gives them significant scale and bargaining power across the supply chain.

Below the hyperscalers, specialist AI cloud providers such as CoreWeave and Lambda Labs focus on renting GPU compute capacity to AI developers and enterprises.

AI cloud services are where AI spending is ultimately monetised.

Growth in AWS, Azure and Google Cloud is one of the clearest signs that enterprise AI adoption is turning into real revenue.

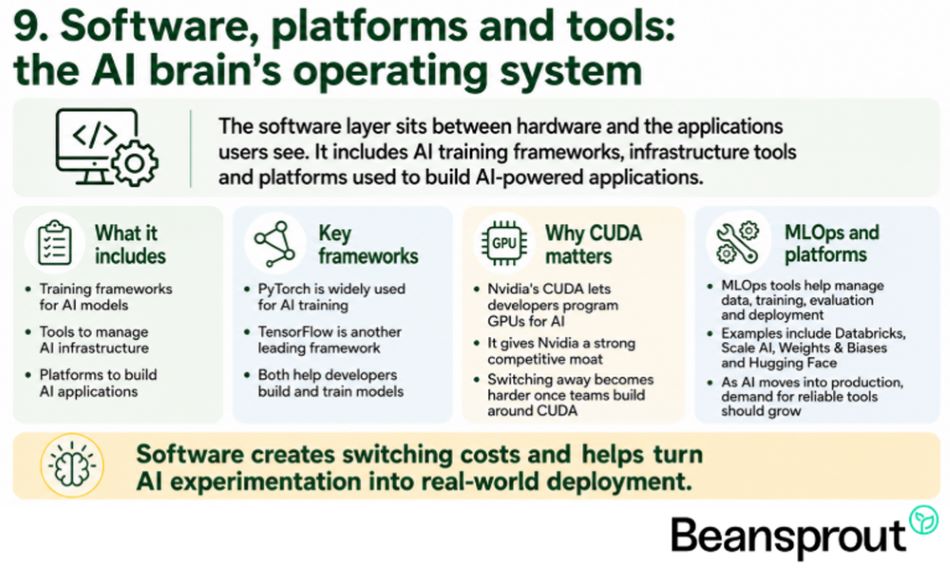

#9 - Software, platforms and tools: the AI brain’s operating system

The software layer sits between the hardware and the applications that users see.

It includes the frameworks used to train AI models, the tools used to manage AI infrastructure, and the platforms used to build AI-powered applications.

PyTorch, maintained by Meta, and TensorFlow, developed by Google, are two of the most widely used AI training frameworks.

Nvidia’s CUDA software stack is especially important because it allows developers to program Nvidia GPUs for AI workloads.

This gives Nvidia a strong competitive moat. Once developers build around CUDA, switching to another chip ecosystem becomes harder.

Above this layer are MLOps platforms, which help companies manage data pipelines, model training, evaluation and deployment.

Companies such as Databricks, Scale AI, Weights & Biases and Hugging Face operate in this area.

Software creates switching costs. As more AI models move from experimentation to production, demand for reliable deployment and management tools should continue to grow.

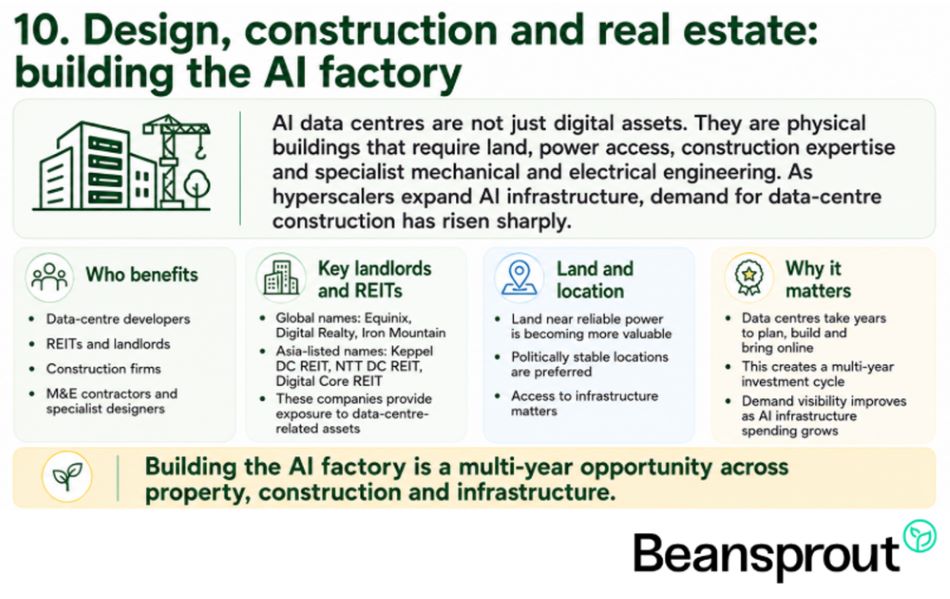

#10 - Design, construction and real estate (building the AI factory)

AI data centres are not just digital assets.

They are physical buildings that require land, power access, construction expertise and specialist mechanical and electrical engineering.

As hyperscalers expand AI infrastructure, demand for data centre construction has risen sharply.

This benefits data centre developers, REITs, construction firms, M&E contractors and specialist designers.

Global data centre landlords such as Equinix, Digital Realty and Iron Mountain lease space to hyperscalers and enterprises, while Asia-listed names such as Keppel DC REIT, NTT DC REIT and Digital Core REIT also provide exposure to industrial and data centre-related assets.

Land near reliable power sources and in politically stable locations is becoming increasingly valuable.

Data centres take years to plan, build and bring online. This creates a multi-year investment cycle and gives companies involved in design, construction and real estate better demand visibility as AI infrastructure spending continues.

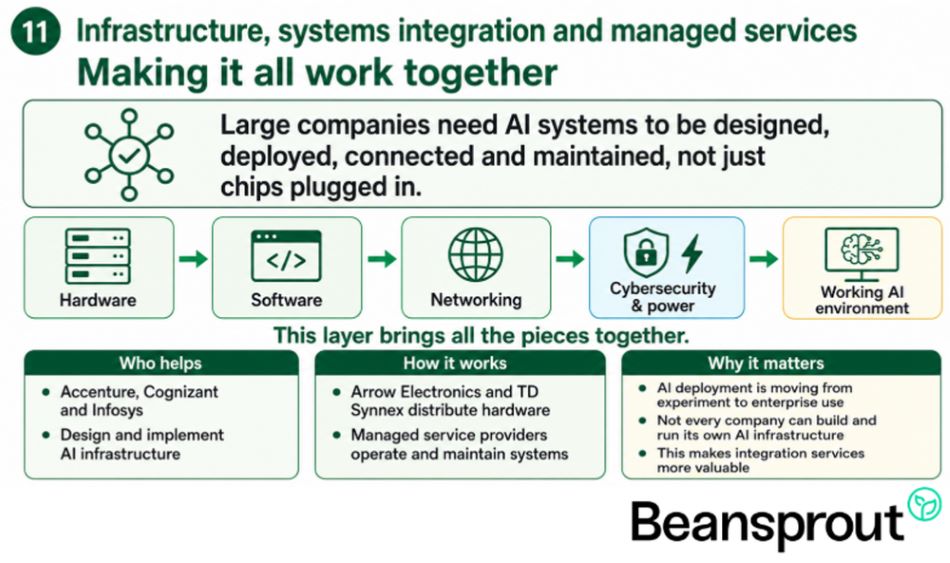

#11 - Infrastructure, systems integration and managed services: making it all work together

Large companies do not simply buy AI chips and plug them in.

They need entire systems to be designed, deployed, connected and maintained.

This creates demand for systems integrators, managed service providers and IT infrastructure specialists that can bring together hardware, software, networking, cybersecurity and power systems into a working AI environment.

Companies such as Accenture, Cognizant and Infosys help enterprises design and implement AI infrastructure and applications.

IT distributors such as Arrow Electronics and TD Synnex help move hardware through the channel to customers.

Managed service providers then help enterprises operate and maintain these systems over time.

As AI moves from experimentation to real enterprise deployment, this layer becomes more important. Many companies will want to use AI, but not every company has the expertise to build and run its own AI infrastructure.

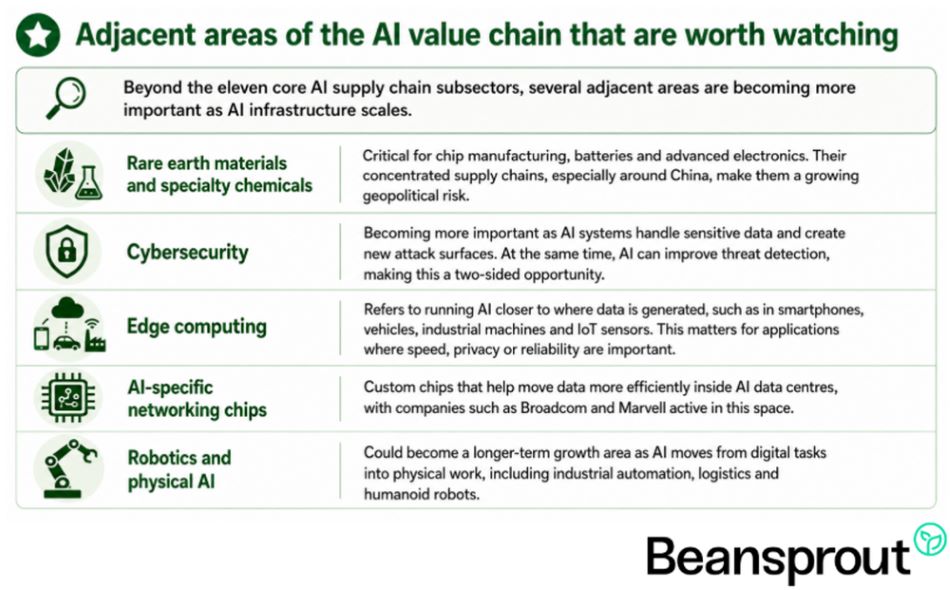

Adjacent areas of the AI value chain that are worth watching

Beyond the eleven core AI supply chain subsectors, several adjacent areas are becoming more important as AI infrastructure scales.

Rare earth materials and specialty chemicals are critical for chip manufacturing, batteries and advanced electronics. Their concentrated supply chains, especially around China, make them a growing geopolitical risk.

Cybersecurity is also becoming more important as AI systems handle sensitive data and create new attack surfaces. At the same time, AI can improve threat detection, making this a two-sided opportunity.

Edge computing refers to running AI closer to where data is generated, such as in smartphones, vehicles, industrial machines and IoT sensors. This matters for applications where speed, privacy or reliability are important.

AI-specific networking chips are another area to watch. These custom chips help move data more efficiently inside AI data centres, with companies such as Broadcom and Marvell active in this space.

Finally, robotics and physical AI could become a longer-term growth area as AI moves from digital tasks into physical work, including industrial automation, logistics and humanoid robots.

What would Beansprout do?

The AI supply chain is broad, and not every part of it offers the same risk-reward profile.

For me, I would focus first on segments with strong competitive advantages, high switching costs or structural supply constraints, such as advanced semiconductors, semiconductor equipment and leading-edge manufacturing.

At the same time, I would be careful not to treat every AI-related company the same way as different parts of the supply chain behave differently. Some companies are direct beneficiaries of AI infrastructure spending, while others may only have indirect exposure.

Semiconductor equipment and AI memory remain in strong growth phases driven by hyperscaler spending and HBM demand, while data centre infrastructure and REITs tend to offer more stable and predictable cash flows through long-term leases with hyperscalers.

Geopolitics also remains a key risk, given the concentration of critical technologies and supply chains across the US, China, Taiwan and Europe.

I would fall back on our Beansprout’s 4-factor Opportunity framework focusing on investability, profitability, earnings growth quality and balance sheet strength.

I would check if any of the Singapore-listed names in precision engineering, semiconductor services and infrastructures appear on our Opportunity stock screener, which could offer a local angle on the global AI buildout.

The AI opportunity is not a single trade. It is a long-term infrastructure investment cycle, and understanding where value accrues along the supply chain is just as important as identifying the technology itself.

To me, broad equity exposure can sit within the Growth Pot, while higher-conviction AI names can be sized within the Opportunity Pot so that I can participate without taking excessive concentration risk.

If you are looking for more Singapore stock ideas linked to AI growth theme, explore our high-conviction curated stock opportunities here.

Which part of the AI value chain are you watching most closely now? Share with us in the comments below or in our Telegram group!

Enjoyed this insight? Follow Beansprout on Telegram, Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments