Yangzijiang, Keppel and Seatrium in focus: Weekly Review with SIAS

Stocks

Powered by

By Gerald Wong, CFA • 16 Mar 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

We share about Yangzijiang Shipbuilding, Keppel and Seatrium in the latest Weekly Market Review.

What happened?

In this week's Weekly Market Review in partnership with Securities Investors Association Singapore (SIAS), we discuss key developments in the global equity market alongside Yangzijiang Shipbuilding, Keppel and Seatrium.

Watch the video to learn more about what we are looking out for this week.

Weekly Market Review

1:33 - Macro Update

- As we enter the third week of the Iran conflict with no clear endgame in sight, geopolitical volatility continues to drive global sell-offs. The S&P 500 slid 1.6% over the past week, while the Straits Times Index held relatively flat at 4,842 points.

- Oil prices remain the primary indicator of investor sentiment. Brent crude initially surged past $110 per barrel before easing briefly to $80, but has now climbed back above the $100 mark.

- Consequently, inflation fears have reignited. The US 10-year Treasury yield has spiked above 4.2%, dashing early-year hopes for multiple rate cuts. Meanwhile, gold prices have eased to around $5,000 per ounce due to a strengthening US dollar.

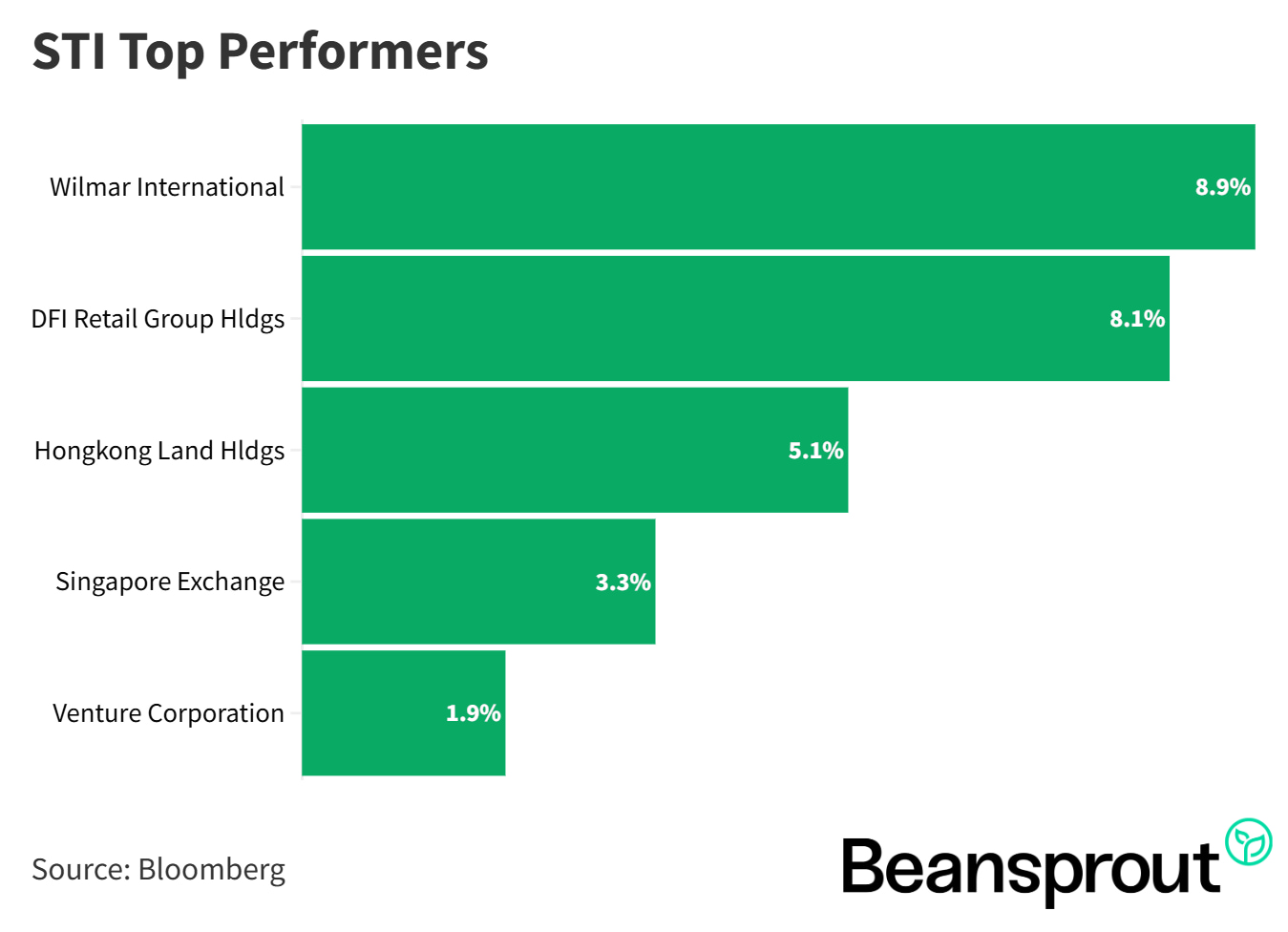

- The Singapore market continues to act as a safe haven, holding up well due to offshore and marine sectors catching wind from the oil price volatility. Top performers included Wilmar which gained 9%, DFI Retail Group up 8%, and SGX which rose 3.3% on the back of high trading volumes.

- Conversely, interest-rate-sensitive and transport names suffered. Yangzijiang Shipbuilding fell 5% last week, alongside UOL, Fraser Logistics and Commercial Trust, and Mapletree Pan Asia Commercial Trust, which all saw notable sell-downs.

STI Top Performers:

STI Worst Performers:

- Mapletree Pan Asia Comm Trust

- Genting Singapore

- Frasers Logistics and Comm Trust

- UOL Group

- Yangzijiang Shipbuildings

Yangzijiang Shipbuilding (SGX: BS6)

- Yangzijiang shares experienced a massive run in February, driven by stellar full-year 2025 results.

- Revenue nearly doubled to RMB 28.5 billion in 2025 from RMB 15 billion in 2021, while profit after tax surged to RMB 8.6 billion in 2025 from RMB 2.6 billion RMB in 2022.

- The company demonstrated strong forward visibility by securing sizable orders and setting a robust 2026 new order win target of RMB 4.5 billion. They also aim to deliver more vessels this year compared to last year.

- Investors were rewarded with a FY2025 dividend of $0.20 per share, representing a 50% payout ratio.

Keppel (SGX: BN4)

- Keppel delivered impressive full-year results, with core profit improving significantly to 1.1 billion in 2025, up from 793 million in 2024.

- A key growth driver was its asset management business. Funds under management have grown massively from 37 billion in 2020 to 95 billion in 2025, representing a 21% compounded annual growth rate.

- The company declared a highly attractive total FY25 dividend of $0.47 per share. This payout includes an interim dividend of $0.15, a proposed final cash dividend of $0.19, a special cash dividend of $0.02, and a special dividend in specie of one Keppel REIT unit for every nine Keppel shares held, which is equivalent to about $0.11 per share.

Seatrium (SGX: S51)

- Seatrium saw a sharp uptick in its share price late in February after reporting a return to strong profitability.

- Revenue improved 24% year-on-year to 11.5 billion, while net profit after tax more than doubled to 324 million from 157 million in 2024.

- The company is successfully executing its value-unlocking and cost-optimization plan. They have booked over $230 million in gains from divestments and secured $50 million in annualized cost savings. Moving forward, management has earmarked an additional $200 million of assets for divestment and targets a further $100 million in cost savings.

- Management declared a dividend of $0.03 per share and announced the continuation of its $100 million share buyback program, of which $58 million has already been repurchased.

Read more: 3 best-performing Singapore blue chip stocks in February. Can the rally continue?

Related Links:

- Yangzijiang Share Price and Share Price Target

- Yangzijiang dividend forecast and dividend history

- Keppel Share Price and Share Price Target

- Keppel dividend forecast and dividend history

- Seatrium Share Price and Share Price Target

- Seatrium dividend forecast and dividend history

Technical Analysis

Straits Times Index

- The index is stabilizing around 4,842 points after pulling back from its late-February high of 5,014.

- Holding the critical 4,790 support level established in January is essential to maintain momentum for recapturing the 5,041 all-time high.

- Momentum is slightly weak but not deteriorating, with the RSI reading at 45 and staying out of oversold territory.

- The MACD remains negative but is converging toward the signal line, suggesting that downward pressure from the geopolitical conflict is subsiding.

Dow Jones Industrial Average

- The index has retraced 8 percent from its high, with expectations of another 1,000-point drop as the conflict continues.

- The next critical double-bottom support zone rests between 45,500 and 45,700 based on the October and November lows.

- Momentum is extremely weak as the RSI has dipped below the 30-point oversold mark.

- The MACD line is diverging sharply downward from its signal line, confirming accelerating bearish pressure toward the 46,000 level this week.

S&P 500

- The broad market index is down 5.4 percent from its 7,002 high, trading near 6,632 after briefly touching a new low of 6,623.

- Expect a further slide toward the next major technical support level of 6,521 established last November.

- A technical rebound remains unlikely until the downward-trending RSI hits the 30-point oversold mark.

- Expanding negative divergence on the MACD signals that dominant downside momentum will persist toward the 6,500 level.

Learn more about the S&P 500 index here.

Nasdaq Composite Index

- The tech index fell up to 8 percent from its January high after failing to break the massive 24,019 double-top resistance level.

- Near-term support sits at 21,800, but an escalation in the conflict could drag the index down another 300 points toward the 21,000 level.

- Indicators are highly bearish with the RSI sitting weakly at 37 and yet to reach the 30-point technical rebound level.

- The MACD is once again diverging downward from its signal line, indicating more downward pressure in the near term.

What to look out for this week

Monday, 16 March 2026: Sasseur REIT ex-dividend

Tuesday, 17 March 2026: FOMC Meetings begin

Wednesday. 18 March 2026: Fed Interest Rate Decision, Micron earnings

Thursday, 19 March 2026: Alibaba earnings, US Producer Price Index (PPI) data

Get the full list of stocks with upcoming dividends here.

Follow us on Telegram, Youtube, Facebook and Instagram to get the latest financial insights.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments