CapitaLand Ascendas REIT preferential offering oversubscribed with strong excess demand

REITs

By Gerald Wong, CFA • 19 Apr 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

CapitaLand Ascendas REIT’s preferential offering was oversubscribed after strong excess demand. Here’s what the final allocation results mean for unitholders.

What happened?

The results of the CapitaLand Ascendas REIT preferential offering are out.

Earlier this month, CapitaLand Ascendas REIT launched a preferential offering at S$2.35 per unit, on the basis of 28 new units for every 1,000 existing units held.

The preferential offering was part of the REIT’s larger equity fund raising to help finance its S$1.4 billion acquisition in Singapore and Japan.

After the recent preferential offerings by other REITs such as Lendlease REIT which was not fully covered, many investors were interested to see if we might be stronger takeup of the CapitaLand Ascendas REIT preferential offering.

In this article, I will dive deeper into the CapitaLand Ascendas REIT preferential offering allotment results, and find out what it means for unitholders and the REIT sector.

What you need to know about the CapitaLand Ascendas REIT preferential offering allocation

| Item | Units | % of preferential offering |

|---|---|---|

| Valid acceptances | 96,136,788 | 74.45% |

| Excess applications | 219,259,057 | 169.79% |

| Total applications | 315,395,845 | 244.24% |

| Units available under preferential offering | 129,134,664 | 100.00% |

| Units left for excess allocation | 32,997,876 | 25.55% |

| Source: CapitaLand Ascendas REIT | ||

#1 - Overall demand was strong

The key takeaway from the final results is that demand for CapitaLand Ascendas REIT’s preferential offering was strong overall, with the offering more than fully covered.

In total, applications came up to 315.4 million units, or 244.24% of the 129.1 million units available under the preferential offering.

A large part of this demand came from excess applications.

While valid acceptances under unitholders’ original provisional allotment came up to 96.1 million units, investors also applied for an additional 219.3 million units through excess applications, meaning they were asking for more units than they were originally entitled to.

#2 - Excess applications were far above the units available

The final numbers also show that demand for excess units was much higher than the number of units left over after the initial take up.

After valid acceptances, only about 33.0 million units remained available for excess allocation.

However, excess applications came up to 219.3 million units, or about 6.6 times the number of units available for redistribution.

This means investors who applied for excess units are unlikely to receive all the units they asked for.

#3 - Take up by entitled unitholders was not full

However, it is worth noting that the initial take up by entitled unitholders was not full.

Valid acceptances, which refer to the units subscribed for under investors’ original provisional allotment, came up to 96.1 million units, or 74.45% of the 129.1 million units available under the preferential offering.

This means not all eligible unitholders chose to subscribe for the units they were allocated.

As a result, 33.0 million units were left to be redistributed through the excess application process, and in this case, the strong excess demand helped absorb the balance.

#4 - The sponsor accepted its allotment in full

CLI RE Fund Investments, the sponsor related entity, accepted its full provisional allotment of 21,838,011 units. CapitaLand Ascendas REIT Management Limited also accepted its full provisional allotment of 83,639 units.

After completion of the preferential offering, CLI RE Fund Investments will own 801,766,980 units, or about 16.07% of total units in issue.

The manager will own 2,979,661 units, or about 0.06% of total units in issue.

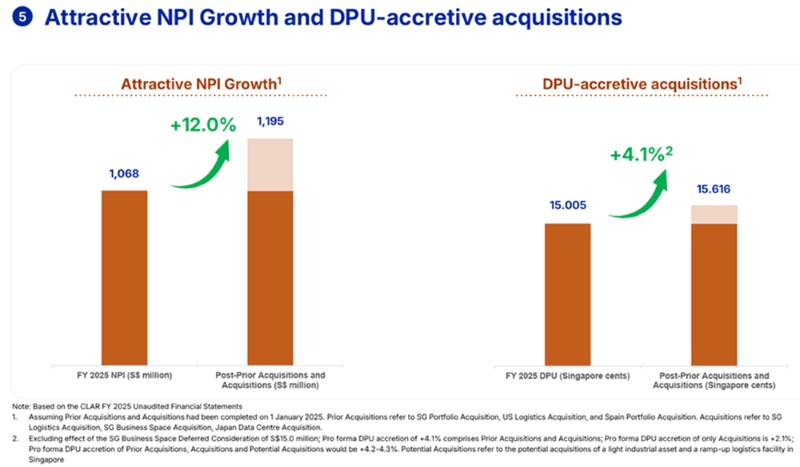

#5 - The acquisitions are expected to be accretive

Based on CapitaLand Ascendas REIT’s earlier pro forma figures, the three announced acquisitions are expected to increase FY2025 DPU by about 0.318 Singapore cents, or 2.1%, from 15.005 Singapore cents to 15.323 Singapore cents, assuming they had been completed on 1 January 2025.

This accretion was based on the earlier equity fund raising structure, which included the S$600 million private placement at S$2.406 per unit and the preferential offering at S$2.35 per unit.

Including acquisitions announced since October 2025, total pro forma DPU accretion rises to around 4.1%.

Aggregate leverage is expected to rise only slightly from 39.0% to 39.7%, while pro forma NAV per unit is expected to improve from S$2.29 to S$2.36.

What would Beansprout do?

To me, this latest update on CapitaLand Ascendas REIT preferential offering allotment looks broadly supportive.

The preferential offering was still more than fully covered overall, as strong demand for excess units helped to support demand even though the initial take up by entitled unitholders was not full.

That should reduce concerns about any overhang from unsold units. The listing date for the preferential offering units is 23 April 2026.

More importantly, the broader case for the acquisition still looks intact. The acquisitions are expected to be accretive, leverage remains manageable, and pro forma NAV improves.

CapitaLand Ascendas REIT's share price has recovered in recent weeks with the broader REIT sector, as the easing of concerns on the Middle East conflict has led to lower Singapore government bond yields.

Based on the pro forma DPU of 15.323 cents and a closing price of S$2.58 as of 25 March 2026, it would offer a dividend yield of about 5.9%. This would be above its historical average dividend yield of 5.5%.

This makes the valuation of CapitaLand Ascendas REIT still attractive compared to its historical average, and makes it worth considering if I am looking for REIT ideas to grow my income.

I will also be thinking about how I can build a diversified income portfolio beyond Singapore REITs to grow my income pot. Explore other income ideas here.

To screen for Singapore REITs with lowest price-to-book valuation or highest dividend yield, check out our best Singapore REIT screener.

If you are new to investing in Singapore REITs, you can start to learn more about Singapore REITs here.

If you prefer diversification without picking individual REITs, you can also gain exposure through Singapore REIT ETFs.

Related links:

Check out Beansprout's guide to the best stock trading platforms in Singapore with the latest promotions to invest in CapitaLand Ascendas REIT.

Enjoyed this insight? Follow Beansprout on Telegram, Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments