DBS and OCBC near all-time highs as UOB lags. Are bank dividends still attractive?

Stocks

By Gerald Wong, CFA • 14 May 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

DBS and OCBC have climbed near all-time highs as UOB lags behind. We compare Singapore banks dividend yields to see if they still look attractive.

What happened?

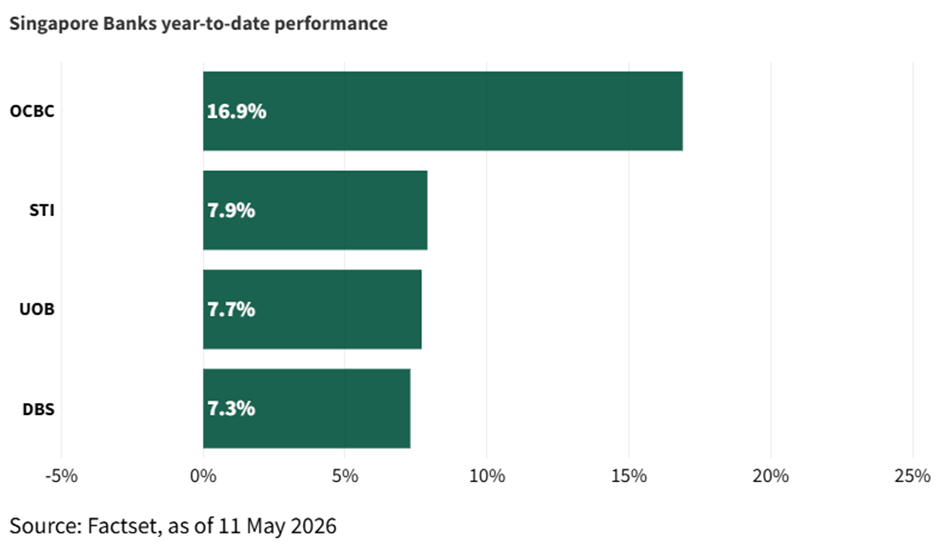

The share price performance of DBS, OCBC and UOB is back in focus.

Both DBS and OCBC have risen to close to their all-time highs, with OCBC's market value exceeding S$100 billion in April.

On the other hand, UOB has lagged behind the two banks.

This represents a fairly sharp reversal after the share prices of DBS, OCBC and UOB pulled back in March with the global geopolitical tensions.

With all three banks having reported their 1Q26 results, I have seen questions in the Beansprout community on whether Singapore bank dividends remain attractive after the recent share price gains.

In this article, we compare the latest earnings, dividend yields and valuations of DBS, UOB and OCBC to see how the three Singapore banks are positioned.

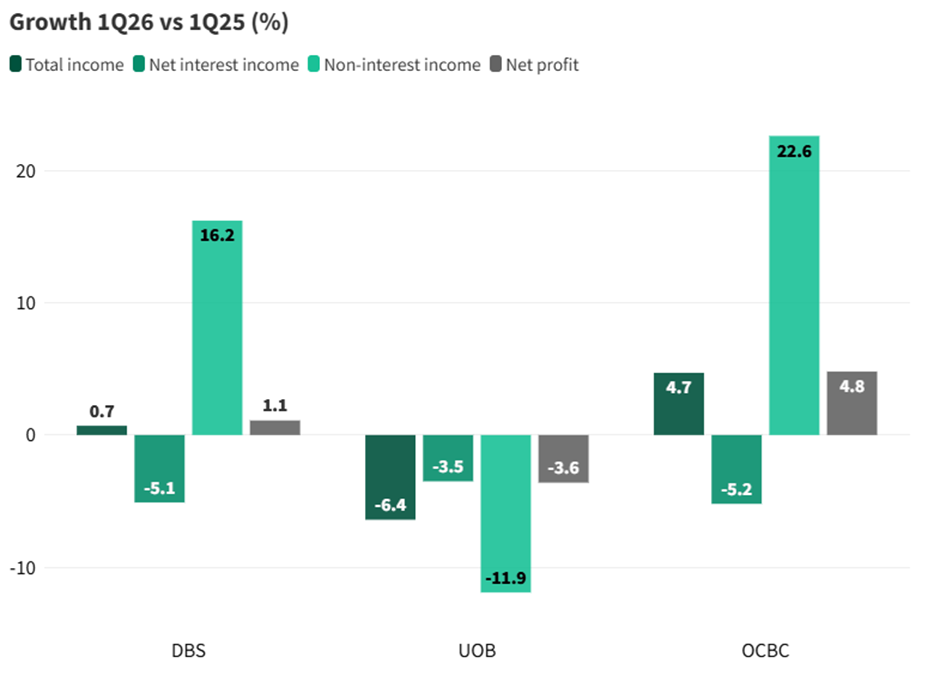

DBS and OCBC reported year-on-year net profit growth in 1Q26, while UOB saw a decline

OCBC stood out in 1Q26. Net profit rose 5% year-on-year to S$1.97 billion, supported by record non-interest income of S$1.61 billion, which grew 23% year-on-year. This was driven by broad-based growth across fees, trading and insurance income. Total income also rose 5% to a new high of S$3.83 billion.

DBS also reported a resilient quarter. Net profit rose 1% year-on-year and 24% quarter-on-quarter to S$2.93 billion, marking a record start to the year. Total income reached a new high of S$5.95 billion, supported by record wealth management performance, record transaction services fees and stronger markets trading income. Return on equity stood at 17.0%.

UOB was the laggard among the three banks. Its 1Q26 net profit fell 4% year-on-year to S$1.44 billion, although this was 2% higher quarter-on-quarter. The year-on-year decline reflected a high base in 1Q25, normalisation in non-interest income from record levels, and continued pressure on net interest margin.

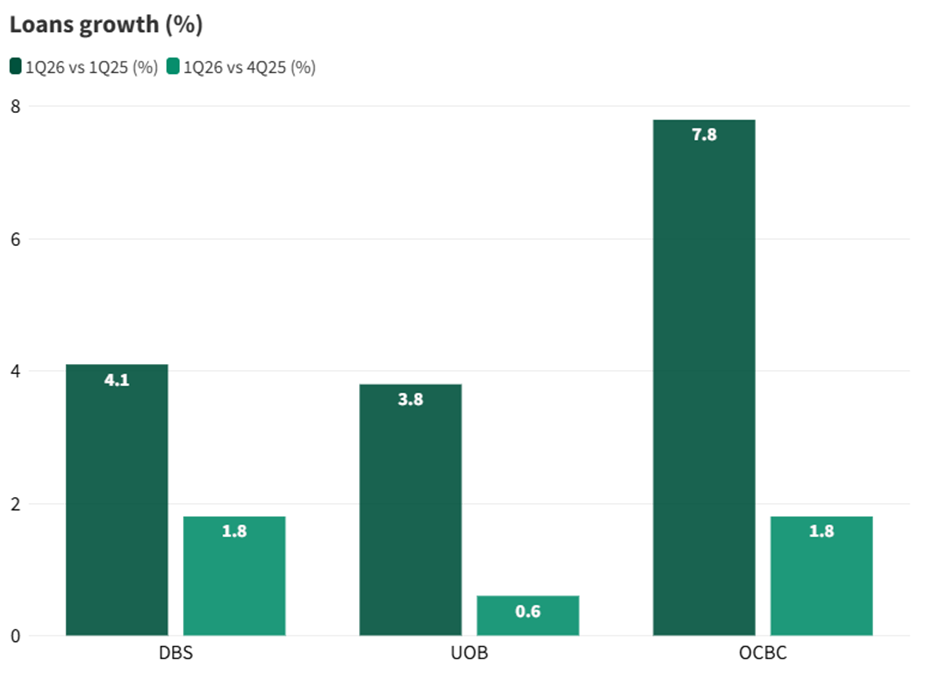

OCBC led loan growth in 1Q26, with all three banks expanding their loan books

OCBC reported the strongest loan growth among the three banks in 1Q26. Its loan book grew to S$347 billion, 8% on a reported basis or up 9% year-on-year on a constant-currency basis. This was supported by broad-based growth across industries and markets including Singapore, Malaysia and its international markets.

DBS saw gross loans rise 4% on a reported basis or 6% year-on-year in constant-currency terms to S$453 billion, led by corporate loans across the region. On a quarter-on-quarter basis, loans grew 2%, or S$8 billion, with broad-based growth in non-trade corporate loans.

UOB reported loan growth of 4% year-on-year, broadly in line with management’s full-year guidance for low single-digit loan growth.

Overall, all three banks continued to grow their loan books, suggesting that credit demand in Singapore and the region remains resilient despite a more uncertain global backdrop.

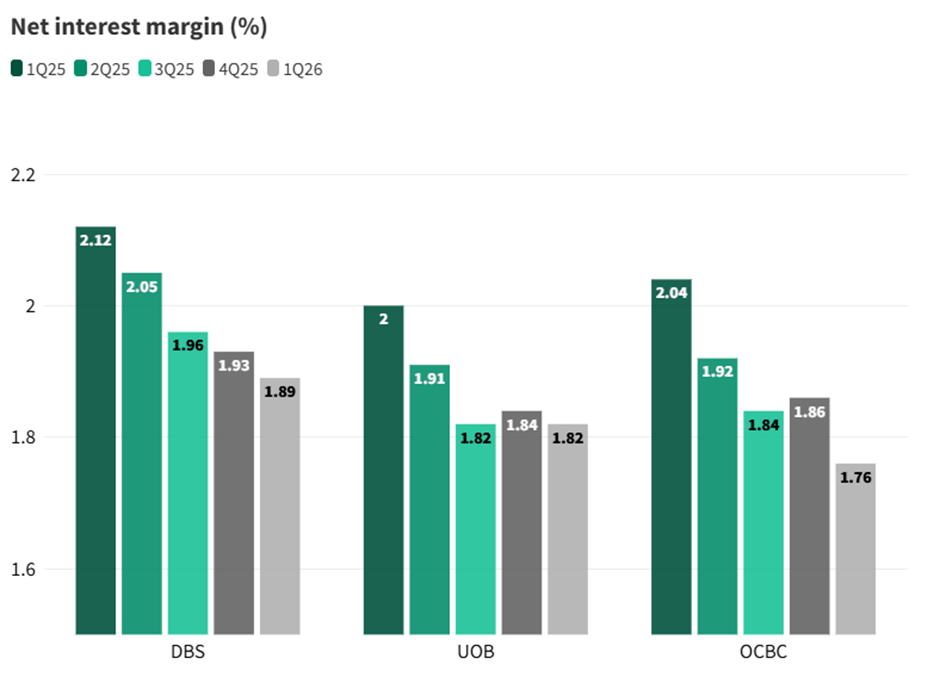

Net interest margin compression resumed in 1Q26, with all three banks seeing declines

Net interest margins ticked up modestly in 4Q25, but pressure resumed in 1Q26 as benchmark interest rates continued to soften.

DBS still reported the highest net interest margin at 1.89%, although this was 4 basis points (0.04%) lower quarter-on-quarter and 23 basis points (0.23%) lower year-on-year. Management said the impact from lower SORA and HIBOR, as well as a stronger Singapore dollar, was partly offset by hedging and balance sheet growth.

OCBC saw the steepest sequential compression. Its net interest margin fell 10 basis points (0.10%) quarter-on-quarter to 1.76%, and was 28 basis points lower year-on-year, reflecting lower SGD, HKD and USD benchmark rates, loan yield compression and a shift into high-quality assets.

UOB’s net interest margin held up better, narrowing just 2 basis points (0.02%) quarter-on-quarter to 1.82%. Asset repricing pressure was partly offset by active funding cost management.

Overall, net interest margin pressure remains a key headwind for the banks in 2026. If interest rates continue to fall, net interest income could remain under pressure, even as loan growth stays resilient.

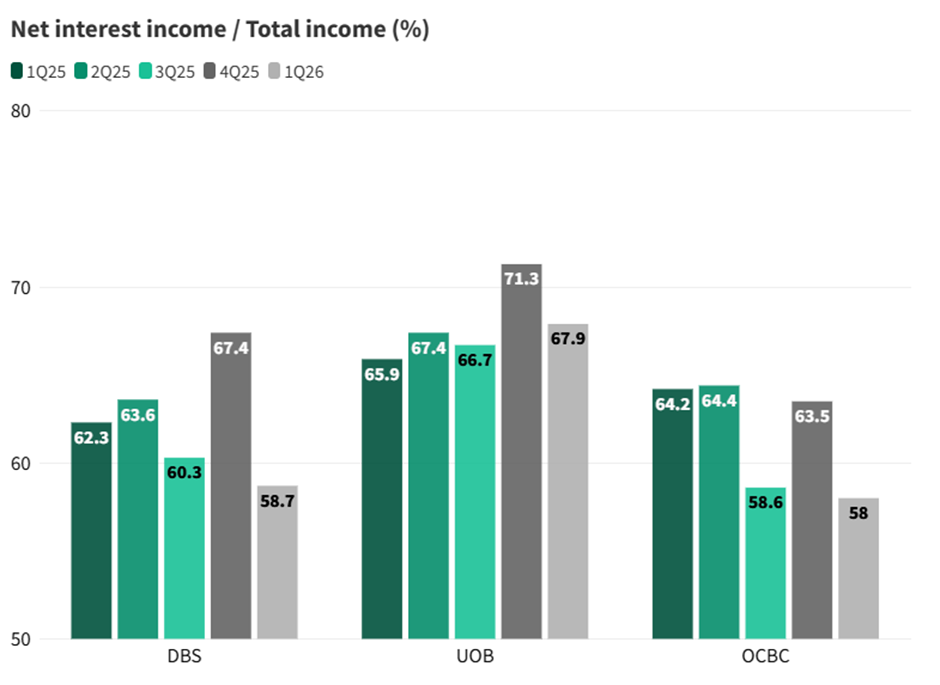

Net interest income as a share of total income diverged further in 1Q26

DBS and OCBC saw their earnings mix shift further towards non-interest income in 1Q26.

For DBS, net interest income made up 58.7% of total income. This reflects stronger contributions from fee income and market trading income, making DBS less dependent on interest rates than before.

OCBC’s net interest income share fell to 58.0%, from 63.5% in 4Q25, as record non-interest income more than offset the decline in net interest income. Non-interest income contributed more than 40% of total income, highlighting the strength of OCBC’s diversified franchise.

UOB remained the most reliant on net interest income, with net interest income making up 67.9% of total income in 1Q26. While this was lower than 71.3% in 4Q25 due to stronger trading income, UOB’s earnings are still more sensitive to falling interest rates compared with DBS and OCBC.

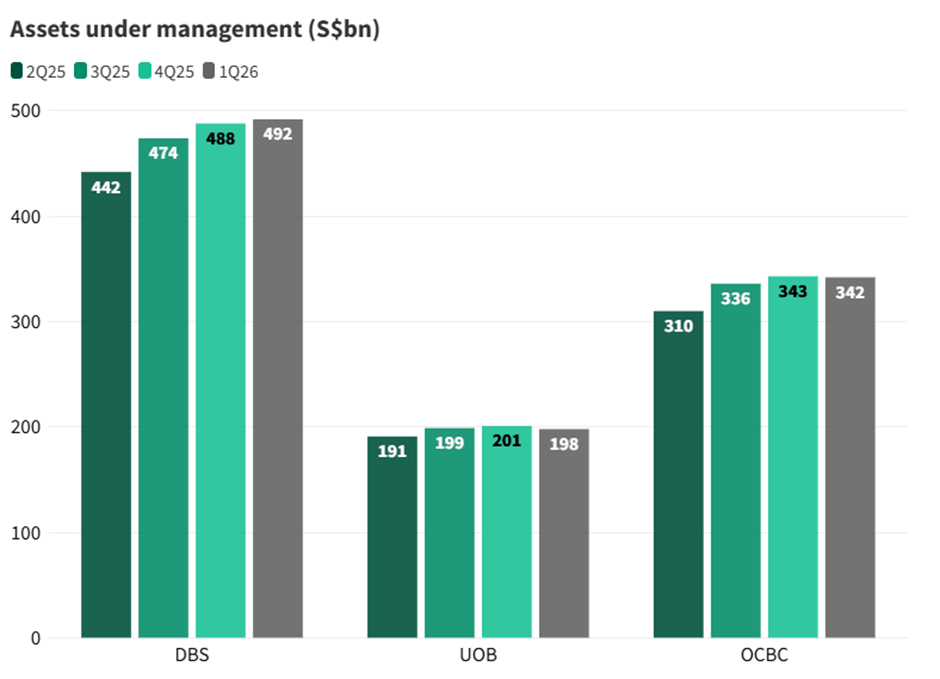

DBS and OCBC delivered record fee income in 1Q26, while wealth AUM hit new highs

The key story in 1Q26 was the continued shift towards fee-driven income, especially from wealth management.

DBS reported record commercial book net fee income of S$1.48 billion, up 16% year-on-year and 35% quarter-on-quarter. Wealth management fees reached a record S$907 million, while transaction services fees also hit a new high of S$257 million.

OCBC also delivered a strong fee performance. Net fee income rose 24% year-on-year to S$675 million, led by a 34% increase in wealth management fees to S$422 million. Trading and insurance income also grew strongly, supported by higher customer flow income and stronger insurance new business value.

UOB’s fee income was more muted, with net fee income of S$637 million, down 8% year-on-year due to a high base in 1Q25, though it rose 2% quarter-on-quarter. Other non-interest income rebounded sharply from the previous quarter, helped by stronger treasury and trading activities.

Wealth assets under management (AUM) continued to grow at DBS and OCBC. DBS’ AUM rose to S$492 billion, while OCBC’s banking wealth management AUM grew 12% year-on-year to S$342 billion. UOB’s AUM eased slightly to S$198 billion.

OCBC also announced the acquisition of HSBC’s wealth business in Indonesia, which supports its strategy to grow wealth management in the region.

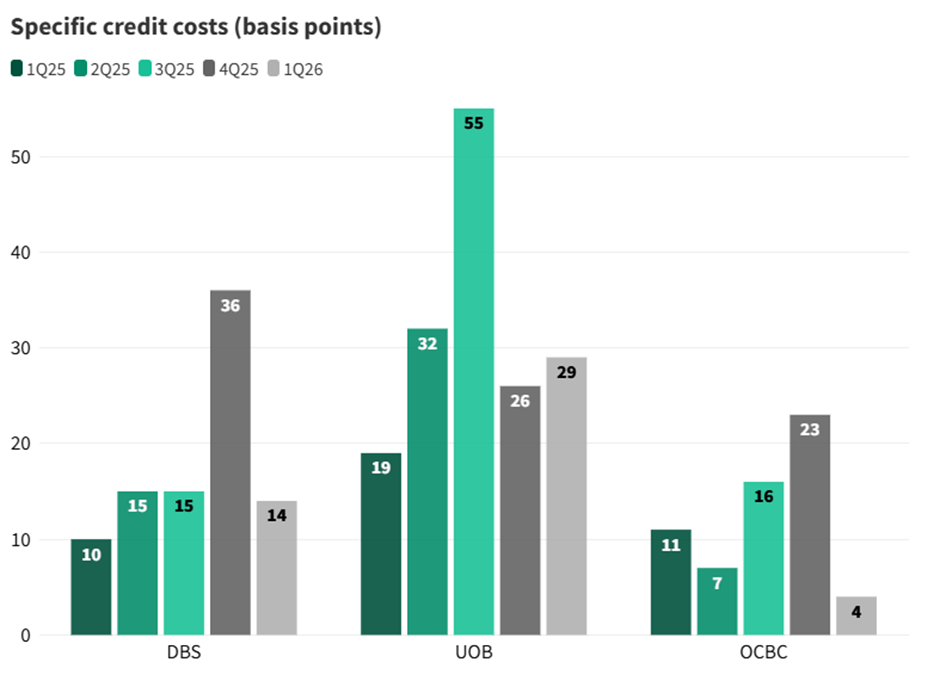

Asset quality held steady; specific allowances normalised at DBS

Asset quality remained broadly stable across the three banks in 1Q26.

The main credit story was DBS, where specific allowances normalised after a higher 4Q25 figure linked to a single real estate non-performing loan. Specific allowances fell to S$157 million, or 14 basis points of loans, while total allowances stood at S$190 million.

OCBC also saw specific credit costs fall sharply to 4 basis points, from 23 basis points in 4Q25. However, total allowances rose to S$216 million, mainly due to higher general provisions and additional management overlays for macro uncertainty.

UOB reported total allowances of S$203 million, with total credit costs of 26 basis points, within its full-year 2026 guidance of 25 to 30 basis points.

Non-performing loans (NPL) ratios were stable across all three banks. OCBC had the lowest NPL ratio at 0.9%, unchanged for the eighth consecutive quarter, while DBS stayed at 1.0% and UOB at 1.5%.

Overall, there were no signs of broad-based deterioration in credit quality. Investors should continue to watch real estate-related exposures and any second-order impact from the Middle East conflict.

All 3 banks kept FY2026 outlook unchanged

All three Singapore banks kept their FY2026 outlook broadly unchanged following the 1Q26 results.

DBS Group Holdings maintained its guidance, with management expecting rate headwinds to be largely offset by hedging and deposit growth even under a “higher-for-longer” rate environment. Total income is still expected to be broadly similar to FY2025 levels, while net profit may come in slightly lower. Specific credit costs are guided at around 17 to 20 basis points. CEO Tan Su Shan also flagged uncertainty from the Iran war and potential second-order effects, although stress tests suggest DBS’ credit portfolio remains sound.

UOB also kept its FY2026 guidance unchanged. The bank continues to expect low single-digit loan growth, net interest margin of 1.75% to 1.80%, high single-digit fee income growth and low single-digit operating cost growth. Total credit costs are guided at 25 to 30 basis points. UOB added that its Middle East exposure is limited and has been stress-tested, with capital and provision buffers remaining resilient.

OCBC reiterated its FY2026 outlook as well, expecting stable-to-growing total income supported by double-digit growth in non-interest income and mid-single-digit loan growth. Credit costs are guided at 20 to 25 basis points, while the cost-to-income ratio is expected to remain in the low-to-mid 40% range.

Under CEO Tan Teck Long, OCBC continues to execute its “Next Frontier” strategy, focused on strengthening its Singapore and Hong Kong hubs, refreshing its ASEAN strategy, completing its S$2.5 billion capital return plan by FY2026, and expanding wealth management through the acquisition of HSBC’s wealth business in Indonesia.

How does OCBC's current valuation compare to DBS and UOB?

OCBC has a lower forward dividend yield compared to DBS and UOB.

DBS stands out for income visibility. Its planned capital return dividend of S$0.15 per quarter through FY2026 to FY2027, on top of its ordinary dividend, provides a clearer payout path. At an annualised dividend run rate of about S$3.24 per share and a share price of around S$58.83, this implies a forward yield of about 5.5%.

OCBC has also maintained guidance for a 50% ordinary dividend payout ratio in 2026, compared to its 60% total dividend payout ratio in 2025. OCBC offers a forward dividend of 4.3%. Both OCBC and UOB typically pay dividends twice a year. UOB 's forward dividend yield is 4.6 per cent.

OCBC price to book at 1.68x, lower than DBS’ 2.41x

Across all three banks, valuations are above historical averages, with DBS trading at 2.41x price-to-book versus its historical average of 1.49x. OCBC trades at 1.68x price-to-book, lower than DBS but higher than its historical average of 1.14x. UOB is currently trading at 1.25x price-to-book, the cheapest among the three banks, but higher than its long-term average of 1.14x.

What would Beansprout do?

The 1Q26 results reinforce a clear divergence between DBS, OCBC and UOB

DBS and OCBC both delivered record total income, supported by strong fee and wealth management performance, while UOB's earnings were softer year-on-year due to a high base, although credit costs and net interest margin held up relatively better than expected.

OCBC has delivered the strongest earnings surprise in 1Q26 and the best share price performance year-to-date, with wealth management momentum and the HSBC Indonesia acquisition strengthening its longer-term growth profile

Investors may want to watch whether net interest margin compression stabilises and how quickly capital is returned to shareholders.

UOB appears more reliant on stable credit costs and a recovery in fee income to support earnings, leaving its earnings trajectory more sensitive to credit conditions.

Hence for income investors, DBS still offers a higher forward dividend yield, stronger franchise quality and market leadership.

If I am looking to diversify my portfolio beyond DBS by adding another Singapore bank, then I may consider OCBC through its exposure to banking, wealth management and insurance in one name, albeit with a lower yield.

More broadly, this fits with our view that Singapore should remain a core part of a portfolio, supported by the market's relative resilience, dividend support, and safe haven appeal.

It also reflects our focus on looking beyond Singapore REITs for income, by building a more diversified portfolio with quality dividend names such as the local banks. Explore how to build a more diversified Income Pot here.

All three banks are also among the largest Singapore blue chip stocks, making them a natural starting point for investors looking to build exposure to Singapore's economy.

If you prefer broad exposure to all 3 banks and blue chips, you can learn more about the Straits Times Index (STI).

If you could only invest in one Singapore bank today, would you pick DBS, OCBC or UOB? Share your thoughts with us in the comments below or in our Telegram group!

Planning to invest in OCBC, UOB or DBS? Compare the best Singapore brokers to find the right trading platform, and see the latest promotions and sign-up rewards available.

Enjoyed this insight? Follow Beansprout on Telegram, Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments