3 Singapore blue chip stocks that rose despite the oil price surge. Is there further upside?

Stocks

By Gerald Wong, CFA • 25 Mar 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

Amid heightened geopolitical tensions in the Middle East, some Singapore blue chips have held up well. We break down three stocks that rose and what could continue supporting them.

What happened?

Markets have turned more volatile in March 2026.

Tensions in the Middle East have escalated, raising concerns about a prolonged disruption to global energy supplies and driving oil prices higher.

Recently, I examined how the Fed’s latest signal could affect Singapore blue chip stocks, as shifting rate expectations remain another key driver for the market.

Following the recent pullback, I’ve shared 3 Singapore REITs with dividend yields above 6% and 3 SGX ETFs with dividend yields above 6% for investors looking for income.

I also looked at whether there may be opportunities among the 3 worst performing blue chip stocks year-to-date.

On the other hand, some companies have stayed resilient through the volatility.

In this article, I look at three Singapore blue chip stocks that rose despite the Middle East conflict, and what may continue supporting them from here.

3 Singapore blue chip stock that rose despite higher oil prices

#1 – DFI Retail Group Holdings Limited (SGX: D01)

DFI Retail Group is a leading pan-Asian retailer operating brands such as Mannings, Guardian, Wellcome, Cold Storage, 7-Eleven, and IKEA across Hong Kong, Southeast Asia, and China.

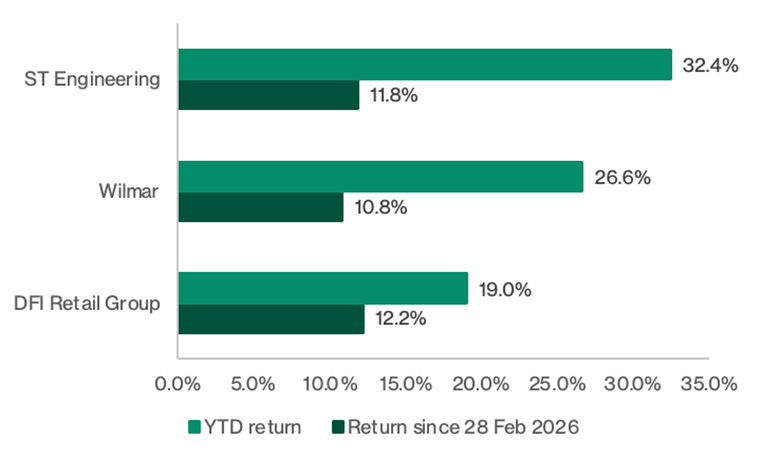

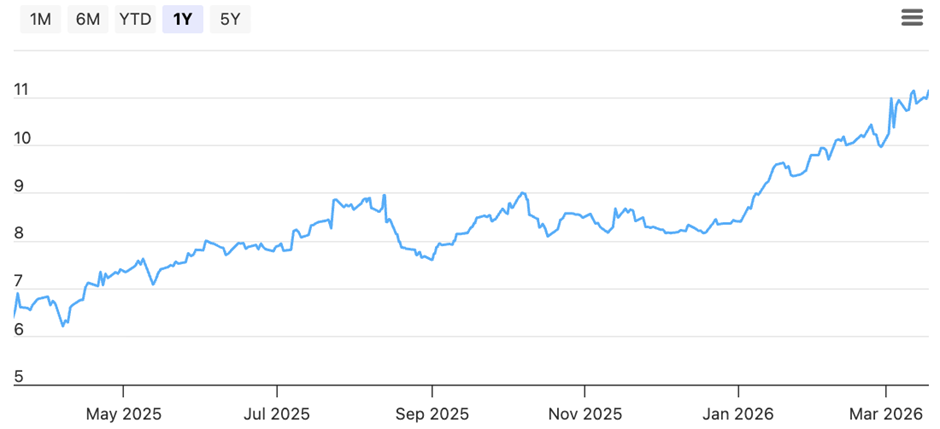

DFI has been one of the strongest blue chip performers since the US-Israel-Iran conflict began on 28 February 2026.

From 28 February 2026 to 18 March 2026, DFI’s share price rose 12.2% despite the heightened geopolitical uncertainty.

On a year-to-date basis (1 January 2026 to 18 March 2026), the stock is up 19.0%, suggesting DFI had already been supported by improving sentiment even before the latest market volatility.

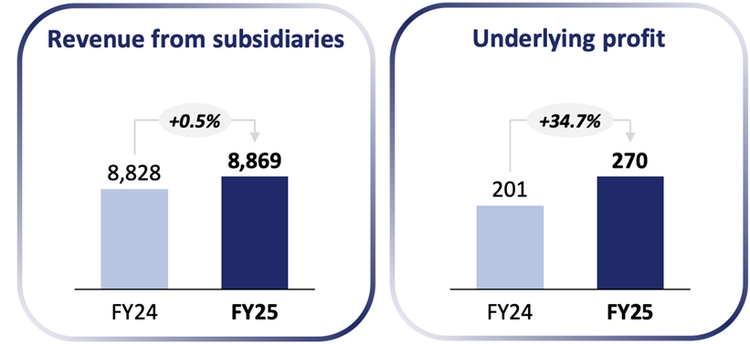

The resilience in the share price comes as DFI delivered a strong set of FY2025 results.

For the year ended 31 December 2025, DFI reported revenue of US$8.9 billion, while underlying profit attributable to shareholders rose 35% year-on-year to US$270 million, reaching the high end of its guidance range.

The improvement was driven by a recovery in like-for-like subsidiary sales, better margins and portfolio actions, including the divestment of its minority stake in Yonghui.

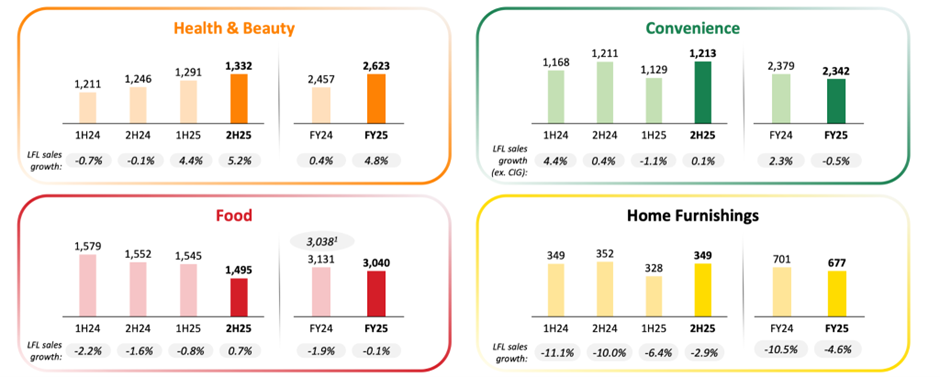

A key support for performance has been the Health & Beauty segment, while management continues to reposition the group from a portfolio investor into a more focused operating company.

DFI has simplified its structure through divestments, including the sale of its Singapore food business comprising Cold Storage and Giant to Macrovalue, allowing the group to focus capital and execution on businesses such as Guardian and 7-Eleven.

Within Health & Beauty, management said it has been working to create a more consistent store design and visual identity across markets. The aim is to improve customer navigation and increase basket size, with early results showing improvements in both sales and gross profit.

At the same time, DFI continues to tailor its approach market by market. For instance, management noted that Indonesia is more beauty-led because of its younger demographic, while there is also growing demand for wellness and dermatology-related products across the region.

The Convenience Store business is also looking beyond its traditional growth drivers.

Beyond ready-to-eat offerings, management said it is expanding into other categories such as merchandise sales to offset structural declines in cigarette sales. One recent example was a collaboration with K-pop group Seventeen to sell merchandise during their Hong Kong concert.

Management also sees room to grow store count in Tier 2 cities in South China, where convenience store penetration remains relatively low.

Importantly, DFI said it is currently the only profitable franchise licence operator of 7-Eleven in China among the 17 operators in the market, which suggests its operating model there remains differentiated.

While it has expressed interest in potentially expanding into other regions in China, management also stressed that it will remain disciplined and not overpay.

Capital allocation remains an important part of the story.

Management said about 50% of capex will go towards new store openings and refurbishments, especially within Health & Beauty, while 25% will be invested in digital and IT, and the remaining 25% in supply chain, store maintenance and sustainability.

Total capex is expected to remain within the guided range of US$200 million to US$220 million, with management highlighting a pipeline of high-return projects across store refurbishment, digitalisation and retail media.

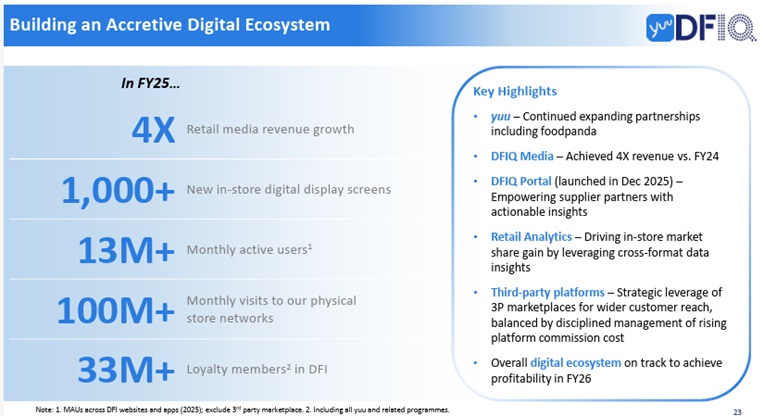

One longer-term theme investors are increasingly watching is digital media.

Management said it plans to expand in-store digital screens and improve utilisation before eventually exploring more premium pricing opportunities, such as charging higher advertising rates during peak traffic periods.

While still relatively small today, DFI sees retail media as a high-margin business that could support both earnings growth and valuation expansion over time. This is because advertising and membership-style income streams typically carry much higher margins than traditional retail operations.

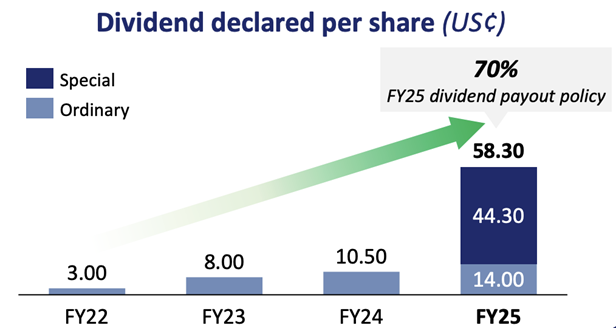

On shareholder returns, DFI has updated its dividend policy by raising its ordinary dividend payout ratio guidance to 70%, up from the previous level of around 60%. This reflects management’s confidence in the group’s cash generation and its commitment to returning more capital to shareholders.

In FY2025, DFI returned about US$740 million to shareholders, including the special dividend of 44.3 US cents per share and the ordinary dividends of 14 US cents paid during the year.

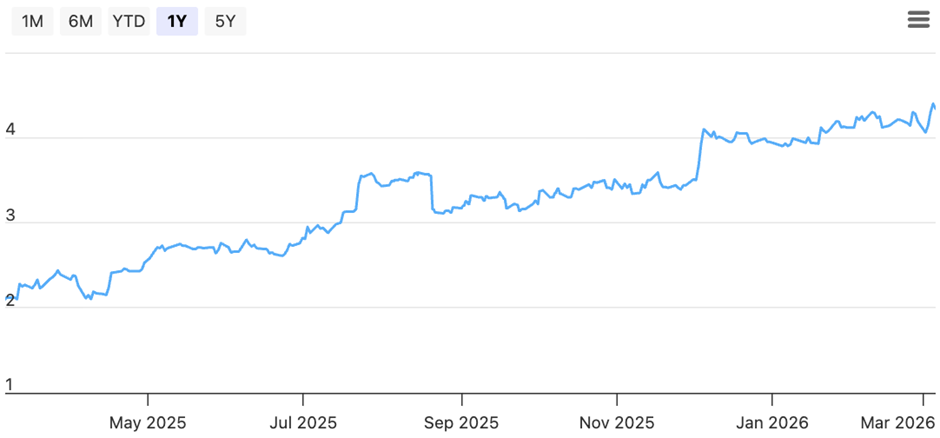

Based on its share price of US$4.70 as of 18 March 2026 and consensus estimates, DFI is expected to pay an FY2026 dividend of US$0.151 per share, which translates to a forward yield of about 3.2%.

The consensus target price of US$5.06 also implies potential upside of around 7.7% from current levels.

Find out how much dividends you would have received as a shareholder of DFI Retail Group Holdings Limited in the past 12 months with the calculator below.

Related Links:

- DFI Retail Group share price history and share price target

- DFI Retail Group dividend forecast and dividend yield

#2 – Singapore Technologies Engineering Ltd (SGX: S63)

ST Engineering is a global technology, defence, and engineering group with a diversified portfolio across Commercial Aerospace, Defence & Public Security, and Urban Solutions & Satcom.

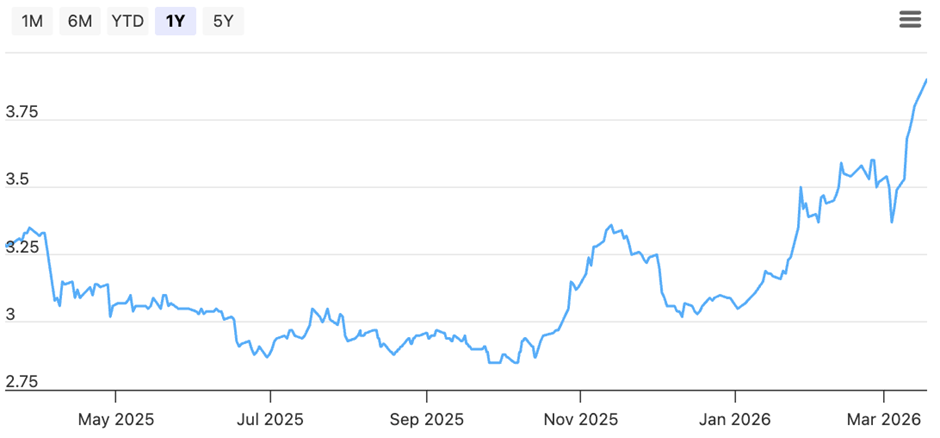

ST Engineering has been one of the strongest blue chip performers since the US-Israel-Iran conflict began on 28 February 2026.

From 28 February 2026 to 18 March 2026, ST Engineering’s share price rose 11.8% despite heightened geopolitical uncertainty.

On a year-to-date basis , the stock is up 32.4%, reflecting continued investor demand for defensive names and companies with exposure to rising global defence spending.

ST Engineering is looking to double its international sales with the Middle East as a major market.

The resilience in the share price comes as ST Engineering delivered solid operating momentum in FY2025.

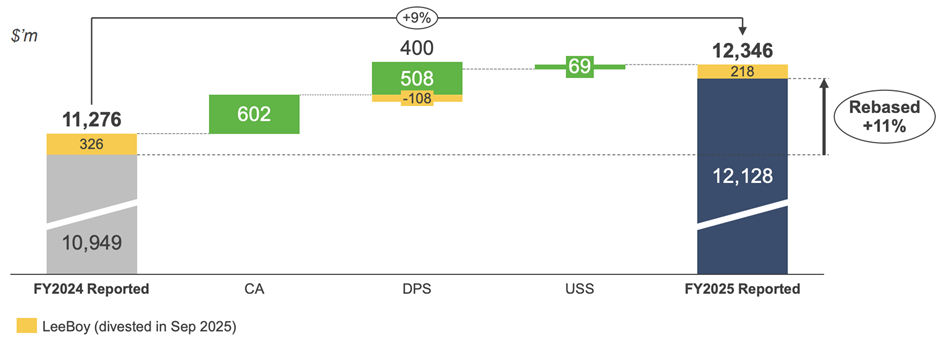

For the year ended 31 December 2025, the group reported revenue of S$12.35 billion, up 9% year-on-year, while base operating net profit rose 21% to S$851 million.

Reported net profit was lower due to one-off items, including impairments, but operating performance remained strong, supported by growth across its business segments.

A key driver of growth was Commercial Aerospace, which was the standout segment in FY2025.

The business benefited from rising engine MRO volumes, new shop capacity, a favourable product mix with greater contribution from higher-margin nacelles, and stronger operating leverage. This helped Commercial Aerospace deliver its strongest margin performance since the pandemic, supported by still-tight global MRO supply and resilient demand for maintenance services.

The Defence & Public Security segment also remained a major support, with broad-based growth across sub-segments and resilient margins. This matters because ST Engineering is increasingly positioning itself to capture a larger share of international defence spending.

Management highlighted that the group secured more than S$600 million of international defence contracts in FY2025, roughly double the level in FY2024.

It has also already secured a S$470 million five-year land platforms MRO contract with Qatar in 1Q2026, underscoring the Middle East as an increasingly important growth market.

More broadly, management said its international defence pipeline has expanded across land, naval, aerospace and munitions, with several sizeable contracts in advanced stages of negotiation.

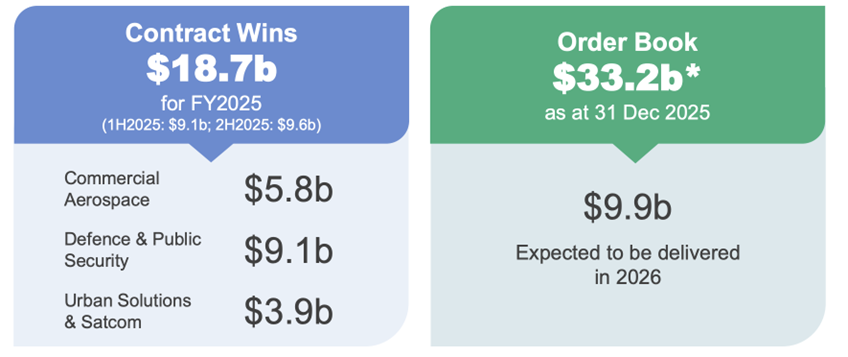

A key highlight has been contract momentum. ST Engineering secured a record S$18.7 billion of new contracts in FY2025, lifting its order backlog to S$33.2 billion, up from S$28.5 billion a year earlier.

This gives the group stronger earnings visibility, especially since S$9.9 billion of the backlog is scheduled for delivery in 2026, representing about 12% growth versus 2025 revenue.

In other words, a meaningful portion of next year’s revenue is already supported by work in hand.

The one weaker area was Urban Solutions & Satcom. While the core Urban Solutions business remained relatively steady and continued to benefit from a sizeable smart mobility order book, the satcom segment remained under pressure.

Wider losses in satcom weighed on segment margins in FY2025, making it the main drag on an otherwise strong result.

Even so, management said it has already implemented S$43 million of annualised cost savings, with another S$20 million expected by 2Q2026, which should help reduce the earnings drag.

It also confirmed that discussions with multiple parties on a potential sale or restructuring of the satcom business are still ongoing. If successful, this could improve group earnings quality and margins further.

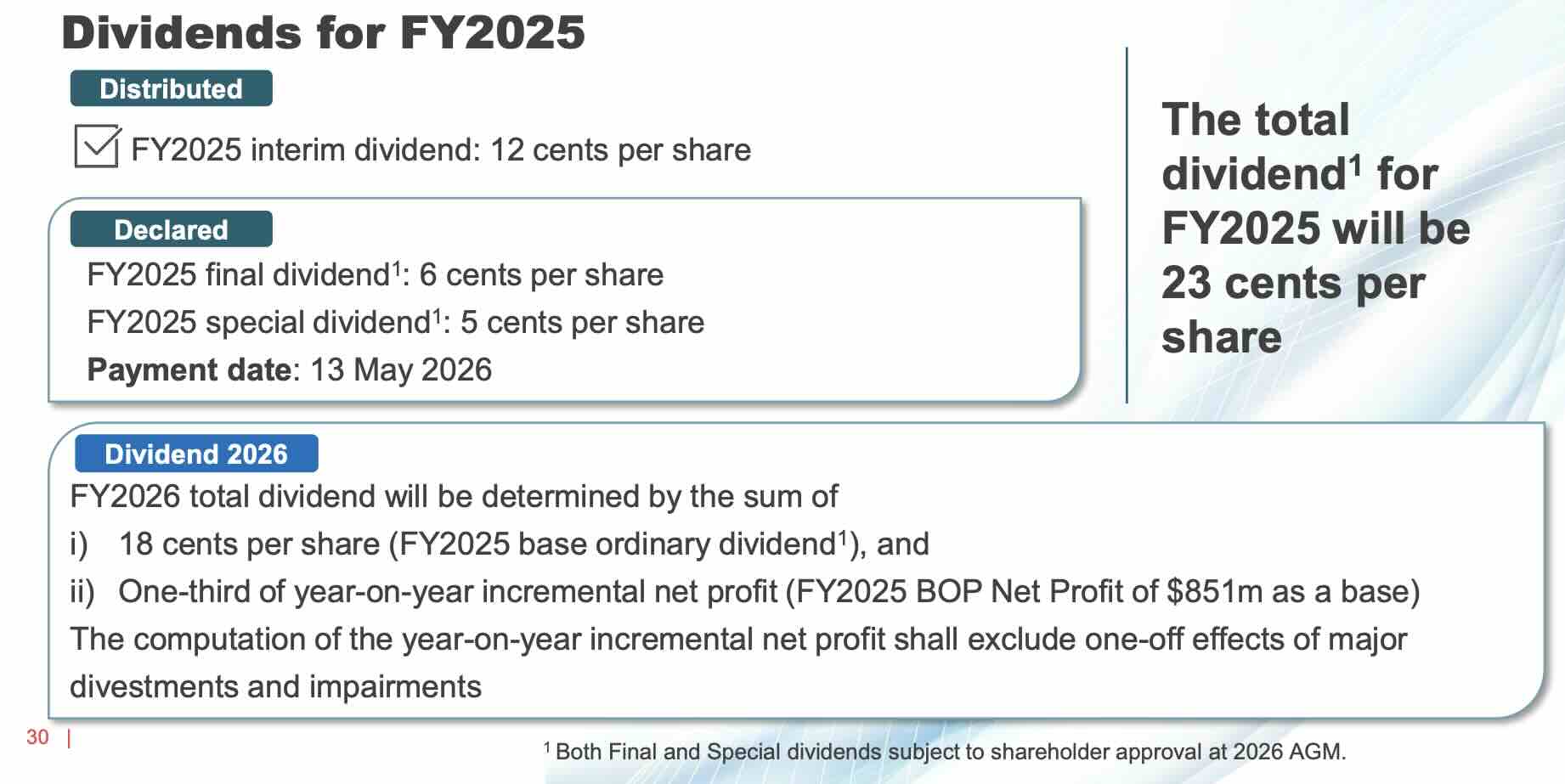

On dividends, ST Engineering has proposed a final dividend of 6.0 cents per share and a special dividend of 5.0 cents per share for FY2025, subject to shareholder approval.

Including interim dividends of 12.0 cents, the total dividend for FY2025 is 23.0 cents per share.

Looking ahead, ST Engineering has also set out a clearer dividend framework for FY2026, where total dividends will be determined by a base component plus one-third of year-on-year incremental net profit (excluding one-off effects of major divestments and impairments).

This policy provides a more transparent link between earnings growth and shareholder returns.

Based on its share price of S$11.15 as of 18 March 2026 and consensus estimates, ST Engineering is expected to pay an FY2026 dividend of S$0.206 per share, which translates to a forward yield of about 1.8%.

The consensus target price of $11.43 also implies a potential upside of around 2.5% from current levels.

Find out how much dividends you would have received as a shareholder of ST Engineering in the past 12 months with the calculator below.

Related Links:

- ST Engineering share price history and share price target

- ST Engineering dividend history and dividend forecast

#3 – Wilmar International Limited (SGX: F34)

Wilmar is Asia’s leading agribusiness group, with an integrated business across oil palm plantations, edible oils, oilseeds crushing, consumer packaged products, and feed and industrial products.

Wilmar has also been one of the strongest blue chip performers since the US-Israel-Iran conflict began on 28 February 2026.

From 28 February 2026 to 18 March 2026, Wilmar’s share price rose 10.8% despite the heightened geopolitical uncertainty.

On a year-to-date basis (1 January 2026 to 18 March 2026), the stock is up 26.6%, suggesting the rally has been supported by both improving fundamentals and a shift toward more resilient names.

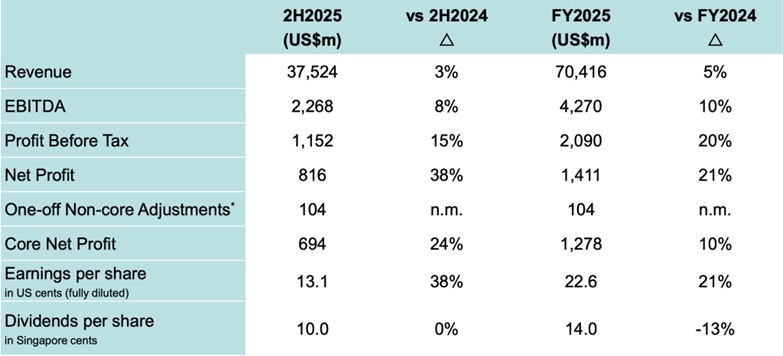

The resilience comes as Wilmar delivered a stronger set of FY2025 results.

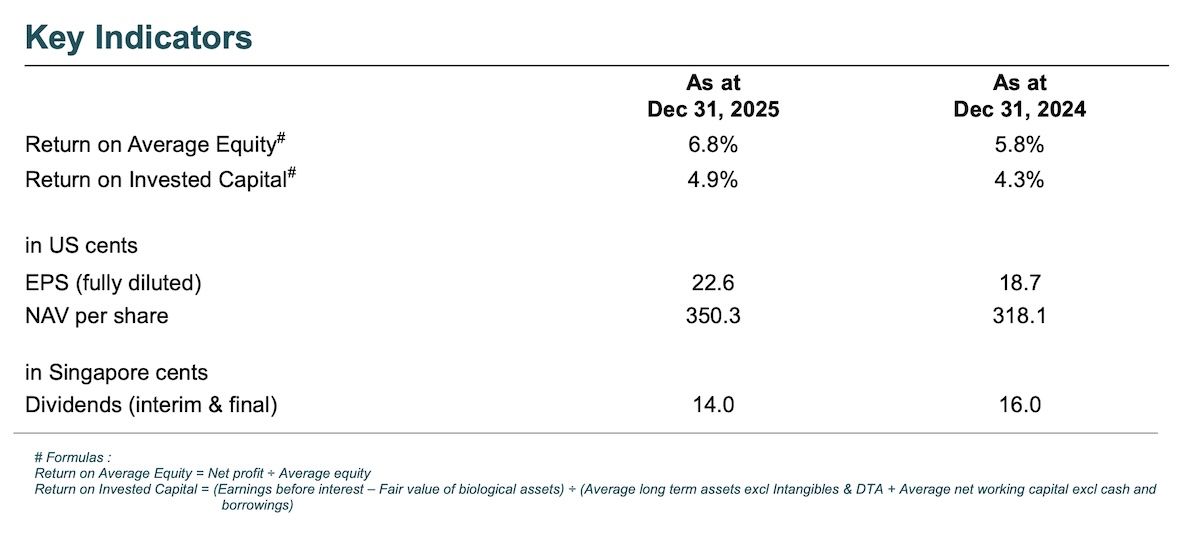

For the year ended 31 December 2025, Wilmar reported revenue of US$70.42 billion, up 4.5% year-on-year, while net profit rose 20.6% to US$1.41 billion.

Reported earnings were also helped by a net one-off gain, including a remeasurement gain related to Wilmar’s increased stake in the AWL Agri business.

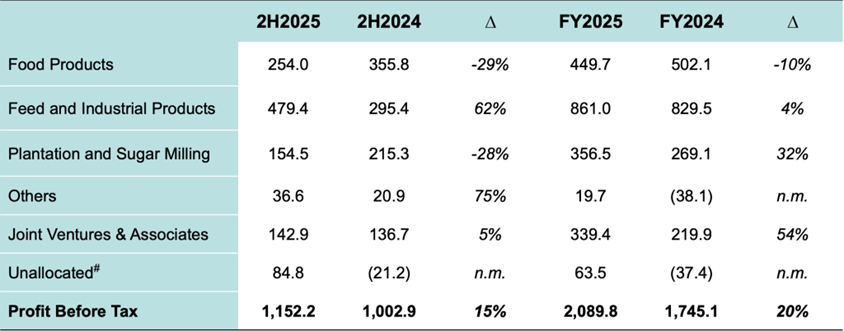

Operationally, two businesses were especially important to the FY2025 profit trend: upstream palm oil plantations and soy crushing.

In Feed & Industrial Products, profit before tax rose 4% to US$861 million for FY2025, with a particularly strong second half helped by improved sugar merchandising activities.

In Plantation and Sugar Milling, profit before tax rose 32% to US$356 million for the full year, although momentum softened in the second half as palm oil prices eased, fruit output declined due to unfavourable weather, and sugar conditions became less supportive.

The Food Products segment was steadier than the headline decline suggests. Profit before tax for the segment fell 10% to US$449.7 million, but this was mainly because FY2024 included one-off gains related to China associates and the Luhua share swap.

Excluding those items, food products profit was broadly flat year-on-year, with better flour and rice profitability partly offset by weaker sugar performance.

Sales volume for the segment still rose 5% to 34.7 million metric tonnes in FY2025.

Wilmar has also been in focus amid rising Middle East tensions due to its exposure to agricultural commodities and edible oils.

The impact of the Iran conflict on agribusiness players is not straightforward. At the same time, the effect is double-edged for an integrated group like Wilmar.

Higher crude palm oil prices can support upstream profitability, but they can also squeeze margins in downstream refining and consumer businesses if cost pass-through is limited.

This is why Wilmar’s integrated model matters: different parts of the business respond differently to the same commodity move. That diversification can help cushion volatility, but it also means not every segment benefits equally when palm oil prices rise.

This partly explains why Wilmar held up relatively well during the broader market pullback triggered by the oil spike in early March.

Investors appear to have viewed it as more defensive than many other consumer-facing names, with upstream exposure offering some support as palm oil prices strengthened through the biodiesel channel.

For FY2025, Wilmar declared a total dividend of S$0.14 per share, comprising an interim dividend of S$0.04 and a final dividend of S$0.10 per share.

Based on Wilmar’s share price of S$3.90 as of 18 March 2026 and consensus estimates, Wilmar is expected to pay an FY2026 dividend of S$0.145 per share, which translates to a forward yield of about 3.7%.

The consensus target price of $3.57 also implies a downside of around 5.3% from current levels.

Find out how much dividends you would have received as a shareholder of Wilmar International Limited in the past 12 months with the calculator below.

Related links:

What would Beansprout do?

When geopolitical tensions rise, I tend to look more closely at businesses that may hold up better in a volatile market.

That helps explain why names like DFI Retail Group, Wilmar and ST Engineering have performed relatively well since the conflict escalated.

But I would not assume that every defensive-looking blue chip automatically becomes a safe haven, especially when higher oil prices could keep inflation elevated and interest rates higher for longer.

What matters more is whether the business has real earnings support, strong execution, and a clear reason for its resilience.

It is also important to be clear about what we are buying the stock for, whether it is capital appreciation, dividend income, or a mix of both.

DFI Retail Group's share price has been supported by steadier earnings and defensive consumption, with improved margins and a net cash balance sheet. However, with a forward dividend yield of about 3.2%, the income may not be high enough for investors focused on yield.

Wilmar has an integrated agribusiness model, with exposure to both commodities and consumer staples demand. Wilmar currently has the highest dividend yield among the three at around 3.7%, but earnings can still be affected by swings between upstream and downstream segments.

ST Engineering stands out for its structural growth drivers, with strong order books and support from aerospace and defence spending. But after the recent run-up, ST Engineering offers a relatively low dividend yield of about 1.8%.

For me, the key is not to chase stocks simply because they have held up during a market shock.

What matters more is whether the business outlook remains solid, and whether the current price still offers a reasonable balance between risk and return.

Even for defensive names, valuation, earnings visibility and dividend yield still matter, especially if the macro environment becomes more uncertain.

| Stock | The good | Key risks |

| DFI Retail Group |

|

|

| Wilmar International |

|

|

| ST Engineering |

|

|

With higher oil prices, learn more about how Singapore blue chip stocks may be impacted here. As interest rate cut expectations moderate, learn how Singapore blue chip stocks may be impacted here.

As volatility continues, learn more about what we are doing with our portfolios amid the Middle East conflict here.

If you’d like to screen for other Singapore stocks with attractive dividend yields and potential upside, you can explore our Singapore dividend stocks screener.

If you prefer broad exposure to blue chips without picking individual names, you can also learn more about the Straits Times Index (STI).

Is there a Singapure blue chip stock you are looking out for amid the market volatility? Share with us in the comments below or in our Telegram group!

[Beansprout Exclusive Longbridge Promotion] Get bonus S$50 FairPrice voucher within 5 working days, plus 5% p.a. interest boost coupon (worth ~S$100) when you sign up for a Longbridge account via Beansprout. Plus, stand a chance to win 1g of gold bar. Promo ends on 31 March 2026. T&Cs apply. Learn more about the Longbridge promotion here.

Planning to invest in Singapore blue chip stocks? Compare the best Singapore brokers to find the right trading platform, and see the latest promotions and sign-up rewards available.

Follow Beansprout on Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments