3 worst-performing Singapore blue chip stocks in 2026. Can they bounce back?

Stocks

By Gerald Wong, CFA • 20 Mar 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

We look at the three worst-performing Singapore blue chip stocks year-to-date in March 2026 and examine what is weighing on their share prices, and whether they could offer turnaround opportunities in 2026.

What happened?

Singapore’s stock market dipped in March 2026.

Earlier, we looked at the 3 best-performing Singapore blue chip stocks in February 2026 and examined whether their rally could continue.

But the March pullback showed that even the banks were not spared, with DBS’ dividend yield moving close to 6% as its share price weakened.

Against this backdrop, we also looked at 3 Singapore REITs with dividend yields above 6% and examined 3 SGX-listed ETFs offering dividend yields above 6% as well.

With income opportunities re-emerging across the market, attention has also turned to the laggards.

In this article, we look at the 3 Singapore blue chip stocks that have been hit the hardest year-to-date, and examine what is weighing on their share prices, their latest earnings and developments, and what could drive a recovery.

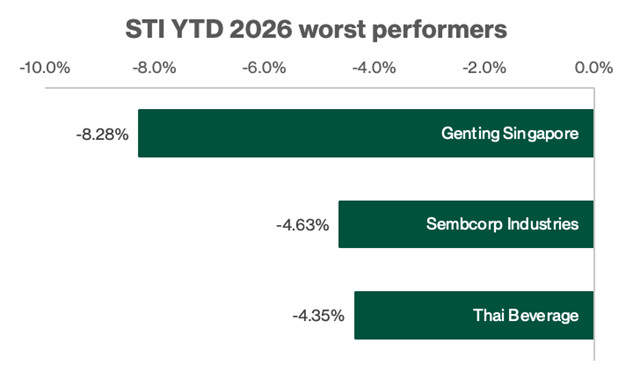

3 worst-performing Singapore blue chip stocks year-to-date in 2026

#1 – Genting Singapore Limited (SGX: G13)

Genting Singapore is Singapore’s integrated resort operator behind Resorts World Sentosa (RWS), with gaming and non-gaming revenue streams across hotels, attractions, retail and dining.

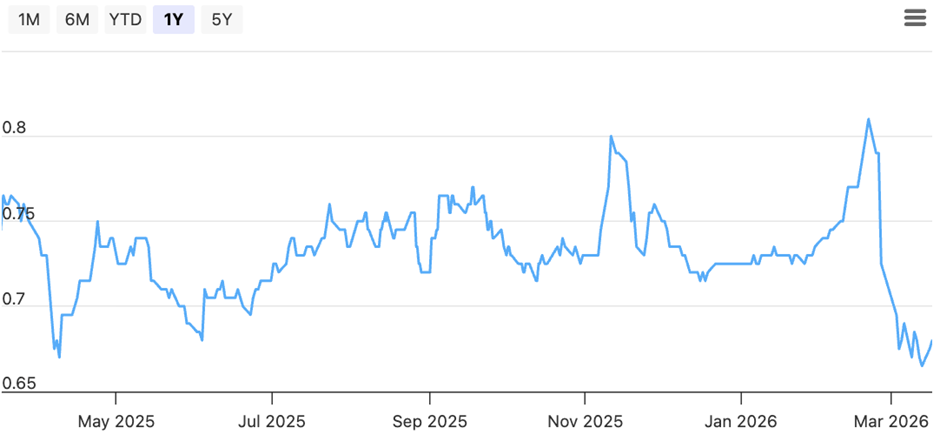

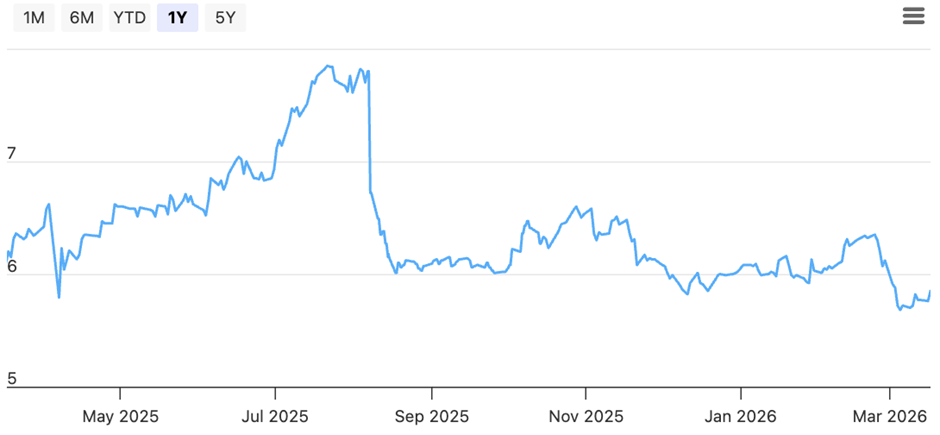

As of 13 March 2026, Genting Singapore share price was S$0.665, representing a year-to-date decline of 8.3%, making it one of the weakest blue chip performers.

The weaker share price performance comes as Genting Singapore works through a transition year for RWS.

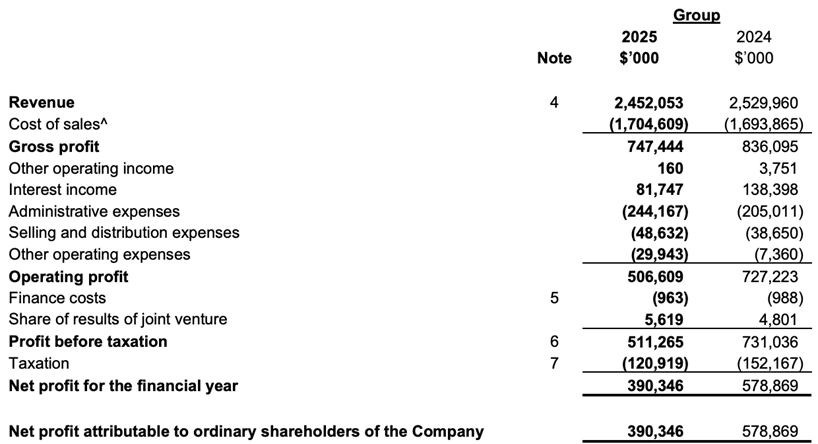

In its latest FY2025 results, Genting Singapore reported revenue of S$2.45 billion, while net profit fell 33% year-on-year to S$390.3 million.

The decline reflected softer-than-expected gaming recovery and pressure on operating leverage as renovation works continued across the resort.

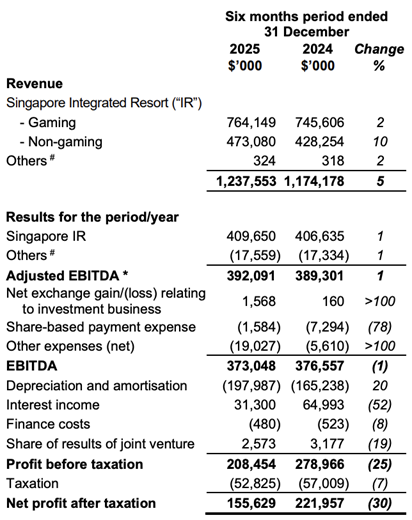

The weaker performance was especially visible in the second half as 2H 2025 profit fell 30% to S$155.6 million.

The shortfall was driven mainly by weaker-than-expected gaming performance.

While Singapore’s broader gaming market continued to recover in 2025, Genting Singapore underperformed amid renovation disruption at RWS and stronger competition from Marina Bay Sands.

The non-gaming business was also affected by the ongoing transformation.

Hotel occupancy eased to 77% in 4Q2025, partly because The Laurus was not fully available for bookings despite its official opening in October 2025.

Management said it had intentionally held back the full room inventory because some facilities, including the bar and spa, were not yet ready.

This meant the contribution from the new hotel came through more slowly than some investors had expected.

One key issue investors are watching is execution on the RWS 2.0 pipeline.

Temporary closures and renovation works are weighing on near-term visitor traffic, gaming volumes and non-gaming revenue.

But management’s goal is to strengthen the resort’s longer-term competitiveness ahead of future licence reviews and the next growth phase.

There are, however, some early signs of progress.

Management said key attractions are starting to ramp up, with The Laurus now operational ahead of schedule, and its spa and bar recently opened.

At The Weave, tenants are progressively moving in, with The People’s People microbrewery concept expected to anchor nightlife activity from 2Q2026.

Management expects tenants to be largely in place by 4Q2026, which could help improve visitor spending and non-gaming contribution over time.

The broader redevelopment remains on track.

Genting Singapore reaffirmed that its S$5 billion capex commitment under RWS 2.0 remains intact.

It has spent about S$1.8 billion so far out of the broader S$6.8 billion project commitment, with capex expected to peak in 2027 and 2028 at around S$1.1 billion per year.

Management said the project remains within budget.

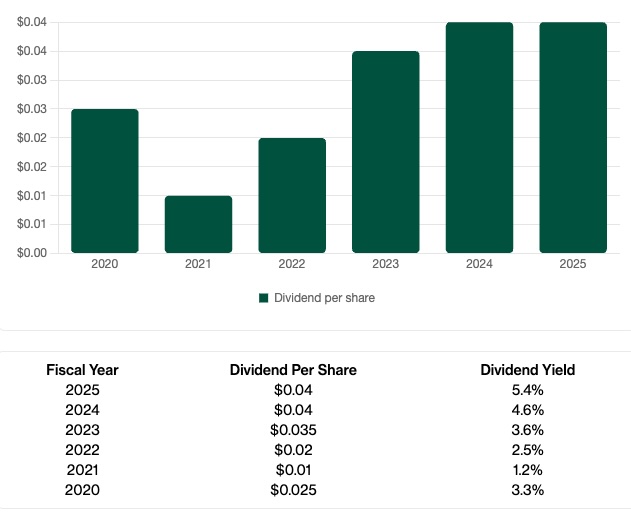

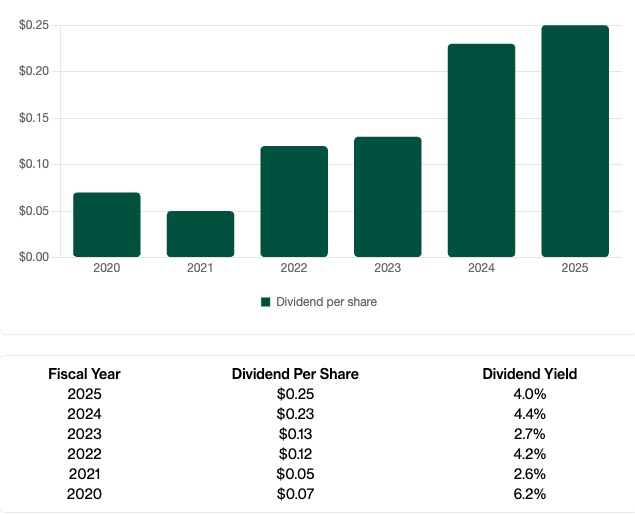

On dividends, Genting Singapore declared an interim dividend of S$0.02 per share and proposed a final dividend of S$0.02 per share, bringing total dividends for FY2025 to S$0.04 per share, unchanged from FY2024.

Despite the sharp drop in earnings, the group kept the total dividend unchanged from a year earlier, implying a payout ratio of about 124%.

Management said it remains committed to a progressive dividend approach, but also noted that future dividend decisions will depend more on earnings growth than on maintaining a fixed payout ratio.

Based on a share price of about S$0.665 on 13 March 2026, this implies a trailing twelve month (TTM) dividend yield of around 6.0%.

Consensus is forecasting a dividend of S$0.042 per share for FY26, implying a forward dividend yield of 6.3%.

As a gauge of market expectations, consensus estimate puts Genting Singapore’s share price target at S$0.853 as of mid-March 2026, implying potential upside of 28.3% if the RWS 2.0 refresh translates into stronger operating momentum.

Find out how much dividends you would have received as a shareholder of Genting Singapore in the past 12 months with the calculator below.

Related Links:

- Genting Singapore Limited share price history and share price target

- Genting Singapore Limited dividend forecast and dividend yield

#2 – Sembcorp Industries Ltd (SGX: U96)

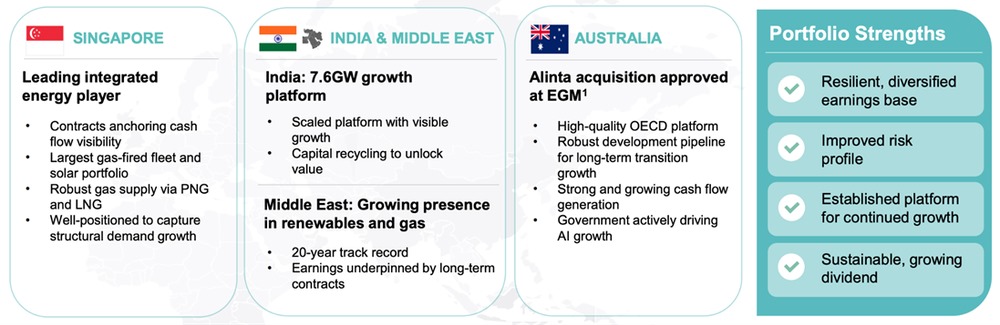

Sembcorp Industries is an energy and urban development group. It has built a growing renewables platform across Asia, alongside its Gas and Related Services business.

Sembcorp has been one of the weaker blue chip performers year-to-date.

As of 13 March 2026, Sembcorp share price was S$5.77, down 4.63% year-to-date, making it one of the weakest blue chip performers.

The share price weakness comes after a softer set of FY2025 results.

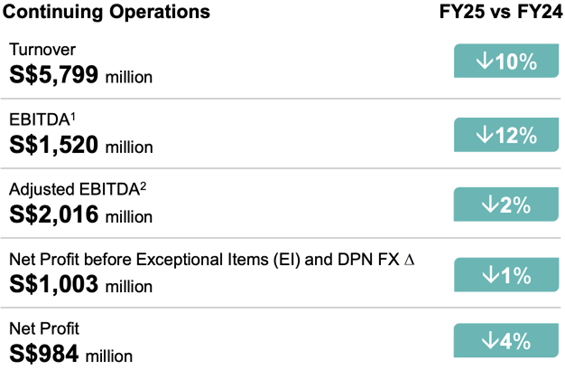

For the year ended 31 December 2025, Sembcorp reported revenue of S$5.8 billion, down 10% year on year, while net profit fell 4% to S$984 million.

The main drag came from the Gas and Related Services segment, where lower contribution from the UK business and weaker generation spreads in Singapore weighed on earnings, although this was partly offset by higher contribution from Senoko Energy.

That said, the gas business remains relatively well contracted.

As of February 2026, around 80% of Sembcorp’s contracted Singapore portfolio was locked in for five years or more, which provides some earnings visibility even as margins on newly contracted volumes come under pressure.

One key area investors are likely to watch in 2026 is re-contracting.

Management said that 47% of Singapore’s gas-fired power capacity will need to be re-contracted during the year, which means pricing and margin outcomes could become an important driver of earnings.

A longer-term theme that management continues to highlight is rising electricity demand from data centres and high-tech manufacturing.

Sembcorp secured 120MW of new long-term contracts in 2025, followed by another 150MW of load from Micron in January 2026.

This suggests the group is actively capturing demand from power-intensive customers, which could become a more important growth driver as Singapore gradually expands data centre capacity and AI-related infrastructure increases electricity usage.

The group is also investing to support this future demand.

Its 600MW hydrogen-ready plant in Singapore is expected to be completed in 4Q2026, which should strengthen its ability to serve new contracted load while gradually positioning the portfolio for a lower-carbon power mix.

Outside gas, the Renewables segment continued to provide support. Underlying net profit from renewables rose 5% to S$192 million, helped by stronger performance from its India portfolio.

Operational renewables capacity reached 15.0GW by end-2025, up from 13.1GW a year earlier. Including projects under development and construction, gross renewables capacity has reached 20.4GW.

This suggests Sembcorp’s renewables platform is still scaling up meaningfully, although near-term profitability can still be affected by issues such as curtailment and tariff pressure in markets like China.

The Integrated Urban Solutions segment also remained relatively resilient.

Underlying net profit before exceptional items rose 3% year-on-year to S$178 million, supported by the build-out of low-carbon industrial parks and ready-built industrial space, although reported performance was affected by portfolio reshaping and the absence of contributions from divested waste-management assets.

Even so, management has guided that the Gas and Related Services segment may face pressure in 2026 from lower margins on newly contracted volumes in Singapore.

This suggests near-term headwinds may remain, even as the group continues investing for longer-term growth.

Despite the softer earnings, Sembcorp raised its dividend.

The group paid an interim dividend of 9.0 cents and proposed a final dividend of 16.0 cents, bringing total FY2025 dividends to 25.0 cents per share, up from 23.0 cents in FY2024.

Management said the higher dividend reflects confidence in the resilience of the underlying business and its ability to generate sustainable returns, even as near-term gas margins soften.

Based on Sembcorp’s share price of S$5.77 as of 13 March 2026, the FY2025 dividend of 25.0 cents implies a trailing twelve month (TTM) dividend yield of about 4.3%.

Consensus is forecasting a FY26 dividend of S$0.267, implying a dividend yield of 4.6%.

Consensus estimates put the share price target at S$6.78, implying an upside of about 17.5% from S$5.77.

The key will be whether earnings can stabilise after a softer FY2025, and whether Sembcorp can continue scaling its renewables platform while navigating tighter margins in parts of its gas business.

Find out how much dividends you would have received as a shareholder of Sembcorp Industries in the past 12 months with the calculator below.

Related links:

- Sembcorp Industries share price history and share price target

- Sembcorp Industries dividend history and dividend forecast

#3 – Thai Beverage (SGX: Y92)

Thai Beverage, or ThaiBev, is one of Southeast Asia’s largest beverage companies, with a portfolio spanning spirits, beer, non-alcoholic beverages and food.

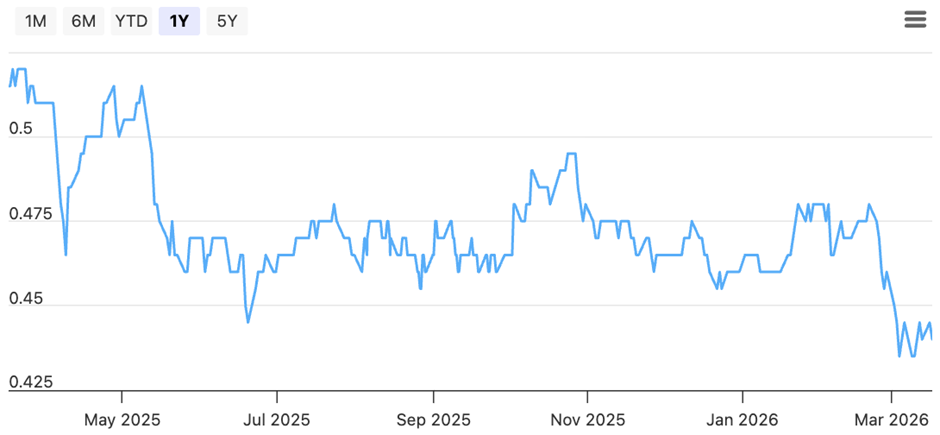

ThaiBev has been one of the weakest blue chip performers year-to-date. Its share price is down 4.35% year-to-date. As of 13 March 2026, ThaiBev’s share price stood at S$0.44.

The weaker share price performance comes as ThaiBev continues to face a cautious consumer backdrop in its key markets.

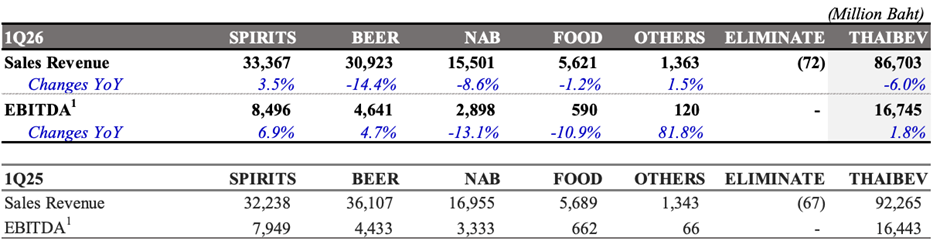

In its latest business update for 1Q FY2026 (quarter ended 31 December 2025), ThaiBev reported sales revenue of THB 86.7 billion, down 6% year-on-year, as weaker consumer sentiment weighed on demand.

However, EBITDA rose 1.8% to THB 16.7 billion, supported by better cost management and margin improvement in parts of the business.

Performance across segments was mixed.

ThaiBev’s spirits business recorded 3.5% year-on-year revenue growth to THB 33.4 billion, supported by higher sales volume and improved margins.

In contrast, the beer business saw revenue fall 14.4% year-on-year to THB 30.9 billion, reflecting softer demand.

Some of this weakness appears to have been caused by temporary factors rather than structural issues.

In Vietnam, wet weather affected alcohol consumption, while in Thailand, the Thai-Cambodia military border conflict weighed on spirits demand.

If these disruptions ease, the operating backdrop could improve.

Looking ahead, there are also reasons to expect some support for margins.

Key raw material costs have fallen across major segments, including molasses for spirits, malt for beer, and resin for non-alcoholic beverages.

If these lower input costs continue to flow through, they could support broader gross margin expansion in FY2026.

At the same time, investors are still watching the regulatory backdrop closely in Thailand and Vietnam.

In Vietnam, the planned increase in special consumption tax on alcoholic beverages remains an overhang for affordability and demand over time.

In Thailand, alcohol regulation has also remained in focus, which may continue to affect sentiment around alcohol-related consumption.

Another medium-term factor to watch is the potential for value-unlocking corporate actions.

ThaiBev owns a portfolio of quality beer and food and beverage assets that could potentially command higher valuations under a different corporate structure or listing strategy.

However, while this remains a possible re-rating catalyst, the timing is still uncertain and would likely depend on market conditions and business performance.

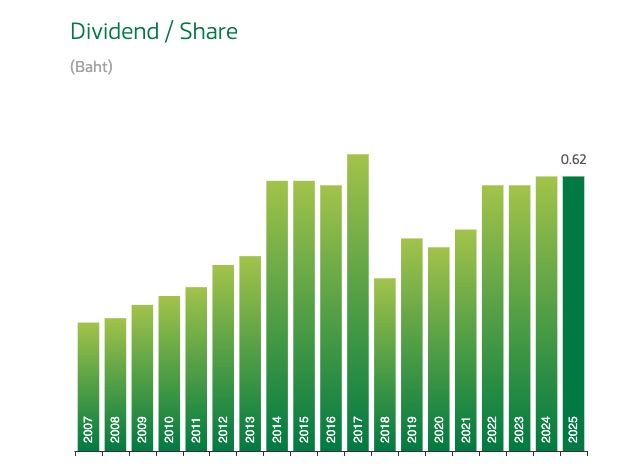

For FY2025 (year ended 30 September 2025), ThaiBev declared a total dividend of THB 0.62 per share (THB 0.15 interim and THB 0.47 final), representing a payout ratio of about 61.4%. This works out to roughly S$0.025 per share for FY2025.

Based on ThaiBev’s share price of S$0.44 as of 13 March 2026, this implies a trailing twelve month (TTM) dividend yield of about 5.7%.

Consensus is expecting a FY26 dividend of S$0.024, implying a forward dividend yield of 5.5%.

For Thai Beverage, consensus estimates put the share price target at S$0.503, implying an upside of about 14.3% from S$0.44.

A rebound would likely depend on a recovery in consumer sentiment in Thailand and Vietnam, and how the regulatory environment for alcohol evolves, which can affect volumes and pricing power.

Find out how much dividends you would have received as a shareholder of Thai Beverage in the past 12 months with the calculator below.

Related links:

- Thai Beverage Public Company Limited share price history and share price target

- Thai Beverage Public Company Limited dividend history and dividend forecast

What would Beansprout do?

With the pullback in share prices, I have been looking at opportunities in the market once again.

But I would not assume that every stock that has fallen is automatically a bargain, because some are facing temporary execution issues while others may be dealing with more persistent headwinds.

How we look at these names depends on what we are trying to achieve — whether the focus is on upside potential or on reliable income.

If the goal is upside, the key question is whether the company can turn its business performance around.

If the goal is income, the more important question is whether the dividend is sustainable and supported by earnings, rather than just looking at the headline yield.

Genting Singapore currently offers a dividend yield of about 6.0%, the highest among the three. However, the payout ratio is elevated after weaker earnings in FY2025, which means the yield partly reflects the share price decline. Any upside would likely depend on whether operating performance improves as the RWS 2.0 upgrades are completed.

ThaiBev offers a yield of around 5.7%, but the income outlook depends on a recovery in consumer demand in Thailand and Vietnam. While the spirits segment has been more resilient, weaker beer sales and regulatory uncertainty mean both earnings and dividends may take time to stabilise. This makes the turnaround story more important than the headline yield.

Sembcorp Industries has a lower yield of about 4.3%, but it stands out because it was the only one of the three to raise its dividend despite softer earnings. This suggests stronger confidence in the underlying business, supported by longer-term drivers as its renewables capacity continues to grow.

| Stock | The good | Key risks |

| Genting Singapore | ● Trailing twelve month dividend yield of about 6.0% ● RWS 2.0 could strengthen the resort’s long-term competitiveness once upgrading works are completed ● Consensus target price of S$0.853 implies potential upside of about 28.3% | ● Dividend not covered by earnings — payout ratio hit ~124% in FY2025 ● FY2025 net profit fell 33% YoY to S$390.3 million ● Ongoing renovation disruptions continue to weigh on gaming volumes and hotel occupancy ● Recovery depends on successful execution of the RWS 2.0 transformation |

| Thai Beverage | ● Trailing twelve month dividend yield of about 5.7% ● Spirits business remained resilient and EBITDA improved despite weaker revenue ● Consensus target price of S$0.503 implies potential upside of about 14.3% | ● 1Q FY2026 revenue fell 6% YoY amid weaker consumer sentiment ● Consumer sentiment remains weak across key markets ● Regulatory headwinds in both Thailand and Vietnam adding pressure on volumes and pricing |

| Sembcorp Industries | ● Only stock of the three to raise its dividend despite softer earnings ● Long-term growth story intact via renewables ● Trailing twelve month dividend yield of about 4.3% ● Consensus target price of S$6.76 implies potential upside of about 17.2% | ● FY2025 net profit fell 4% YoY to S$984 million ● Gas margins under pressure, with 47% of Singapore capacity needing re-contracting in 2026 ● Lowest trailing dividend yield of the three at 4.3% |

As I shared in our update on how to react with the recent geopolitical tensions and uncertainty around the interest rate outlook, I have been reviewing my own financial plan to make sure it still provides enough security and peace of mind. Rather than trying to predict every market move, the focus is on making sure each part of the portfolio is positioned for different scenarios.

The key is not to move entirely to cash or try to time every shift in interest rates, but to stay diversified across liquidity, income, and growth, so the portfolio can remain resilient through different market conditions.

If you prefer broad exposure to blue chips without picking individual names, you can also learn more about the Straits Times Index (STI).

Learn more about how shifting economic drivers are broadening opportunities beyond Singapore blue chips here.

If you’d like to screen for other Singapore stocks with attractive dividend yields and potential upside, you can explore our Singapore dividend stocks screener.

[Beansprout Exclusive Longbridge Promotion] Get bonus S$50 FairPrice voucher within 5 working days, plus 5% p.a. interest boost coupon (worth ~S$100) when you sign up for a Longbridge account via Beansprout. Plus, stand a chance to win 1g of gold bar. Promo ends on 31 March 2026. T&Cs apply. Learn more about the Longbridge promotion here.

Check out the best stock trading platforms in Singapore with the latest promotions to invest in Singapore blue chip stocks.

Enjoyed this insight? Follow Beansprout on Telegram, Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments