3 worst-performing Singapore Next 50 stocks in June 2026. Which look attractive after the pullback

Stocks

By Ng Hui Min • 26 Jun 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

We look at the three worst-performing Singapore Next 50 stocks in June 2026, what weighed on them and whether the pullback offers opportunities.

What happened?

Singapore stocks have continued their strong run this year.

The iEdge Singapore Next 50 Liquidity Weighted Index delivered a total return of 12.2% from end-2025 to end-May 2026, outperforming the Straits Times Index’s 9.7% return over the same period. However, the gains have not been evenly spread.

Earlier, we examined the five best-performing Singapore Next 50 stocks in 1Q 2026, where names such as CSE Global and Hong Leong Asia stood out.

At the same time, investor interest in Singapore’s mid-cap space has broadened, especially as selected tech stocks have benefited from the AI and data centre infrastructure cycle.

We have also looked at Singapore’s construction upcycle, where government spending and infrastructure projects may support companies exposed to building materials and related services.

Since then, we have seen questions from the Beansprout community on whether the recent pullback in some Next 50 names could be a buying opportunity, or whether the weakness points to deeper issues.

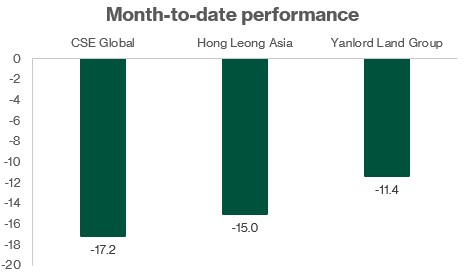

In this article, we look at three of the worst-performing iEdge Singapore Next 50 stocks month-to-date in June 2026 and assess if they look attractive as an investment opportunity.

#1 – CSE Global Limited (SGX: 544)

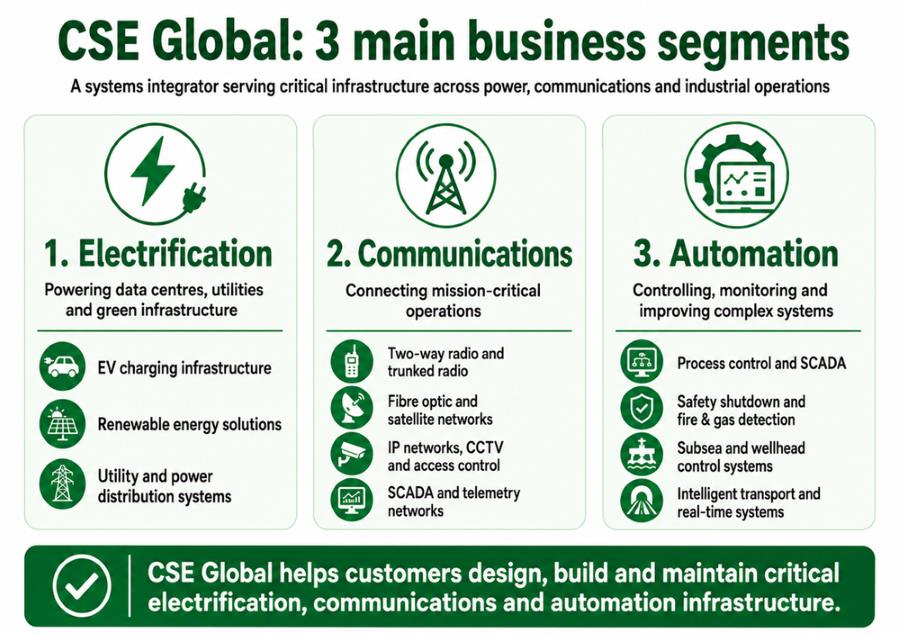

CSE Global is a global systems integrator that provides electrification, communications and automation solutions to customers across data centres, industrial, oil and gas, and utilities markets.

CSE Global had been one of the strongest performers among Singapore mid-cap companies, supported by growing investor interest in its exposure to data centres, electrification and critical infrastructure.

However, CSE Global’s share price pulled back around 17.2% in June after a boardroom dispute raised concerns over governance and board stability.

The issue began after CSE announced that Independent Non-Executive Director Tan Chian Khong would resign on 2 June 2026. Tan had also been the company’s Lead Independent Director, as well as Chairman of both the Audit and Risk Committee and the Nominating Committee.

The disagreement appeared to stem from a proposed board refresh, as well as differing views over the conduct and pace of CSE’s ongoing strategic review.

This strategic review had been announced in March 2026 following a request from Heliconia Capital Management, a Temasek subsidiary and CSE’s controlling shareholder. It came after CSE received a preliminary, non-binding expression of interest from a third party to discuss a potential strategic transaction.

In other words, the recent weakness in CSE’s share price appears to have been driven more by governance uncertainty than by a deterioration in its underlying business.

Despite the boardroom uncertainty, CSE Global’s latest operating performance remained strong.

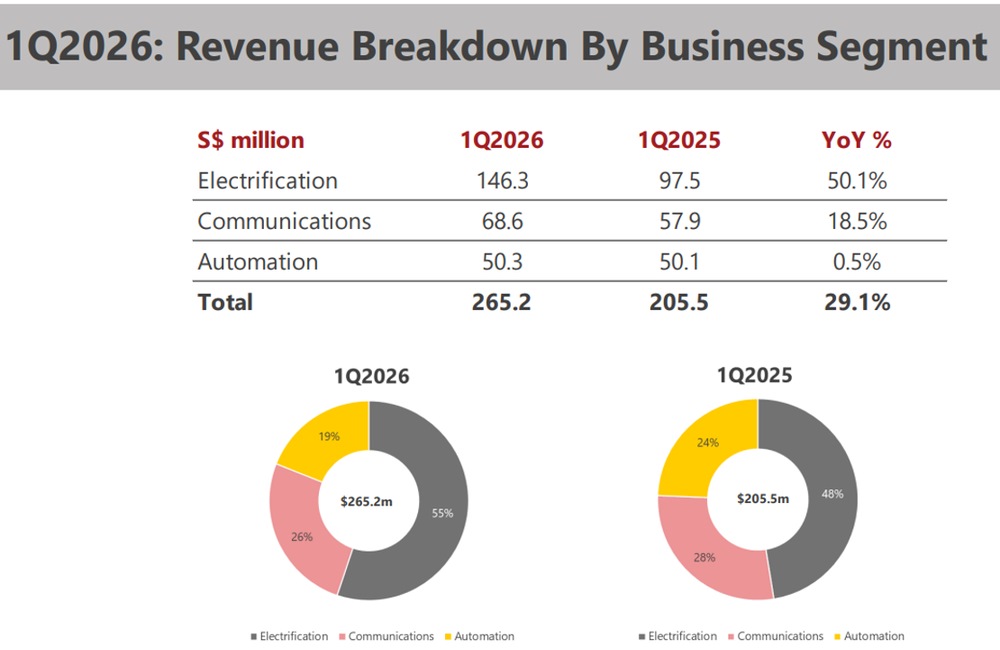

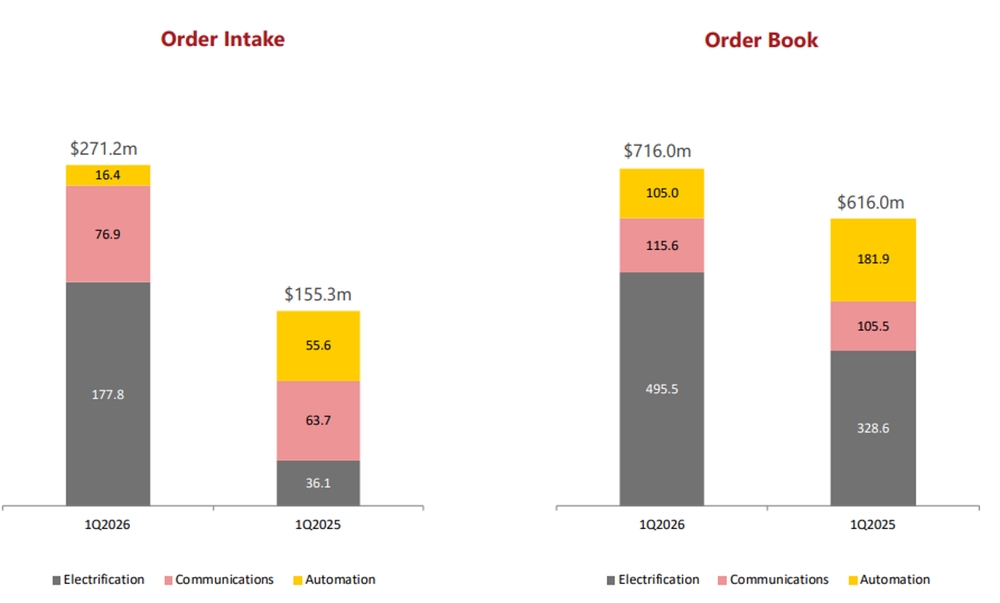

In its 1Q2026 business update, revenue rose 29.1% year-on-year to S$265.2 million, driven mainly by the Electrification segment.

Order intake jumped 74.6% to a record S$271.2 million, while the order book stood at S$716.0 million as at 31 March 2026, up 16.2% from a year earlier.

Management said roughly half of the order book is expected to be recognised as revenue in 2026, with the rest flowing through in 2027. This gives CSE better revenue visibility despite the near-term uncertainty.

The key growth driver remains data centre electrification in the US.

Management confirmed that CSE secured a significant order from Amazon Web Services (AWS) in 1Q2026 and is working to win more hyperscaler orders in the coming quarters.

The company is also widening its customer base beyond the largest hyperscalers to include second-tier players.

The Electrification segment now accounts for about 55% of group revenue, and management expects its contribution to continue rising as existing project orders are executed.

The Communications segment also grew, with revenue rising 18.5% year-on-year to S$68.6 million. Growth was supported by operations in Australia and New Zealand, as well as contributions from a recently acquired US subsidiary.

Management also noted that the Communications business is expanding its data centre exposure beyond the US into Europe and Australia.

However, investors should watch a few near-term headwinds.

First, margins are likely to come under pressure in 1H2026.

CSE is ramping up a new facility that is three times the size of its existing one to support the AWS contract. This means the company is currently carrying double rent, higher labour costs and underutilisation costs before full production begins.

Management expects the second half of 2026 to be stronger as the new AWS facility reaches full production.

Second, hardware and software costs have risen sharply, with some categories doubling over the past six months. This could weigh on gross margins, even if absolute profit dollars remain supported by higher revenue.

Third, oil price volatility has led some oil and gas customers to delay maintenance shutdowns, affecting the Automation segment in the near term. Management expects some of this demand to catch up in the second half, as maintenance work cannot be deferred indefinitely.

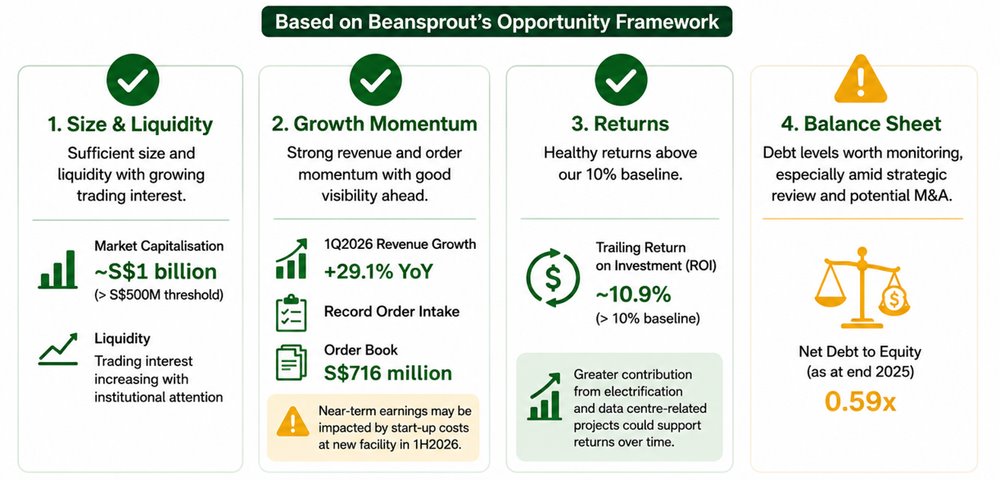

Based on Beansprout’s Opportunity framework, CSE Global still meets several key investment criteria.

First, the company has sufficient size and liquidity, with a market capitalisation of around S$1 billion. This is above our S$500 million threshold, and trading interest in the stock has also increased as institutional attention has grown.

Second, its revenue and order momentum remain strong. The 29.1% year-on-year revenue growth in 1Q2026, record order intake and S$716 million order book provide good visibility over future revenue. However, investors should note that near-term earnings may be affected by start-up costs at a new facility in 1H2026.

Third, CSE’s returns remain healthy. Its trailing return on investment is around 10.9%, clearing our 10% baseline. Over time, a larger contribution from electrification and data centre-related projects could help support returns.

The main area to watch is its balance sheet.

CSE Global’s net debt-to-equity stood at 0.59x as at end-2025, and debt levels are worth monitoring, especially if the strategic review leads to acquisitions or other capital allocation decisions.

Overall, the recent pullback appears to reflect concerns over governance and the strategic review, rather than weaker operating performance.

That said, investors may want to watch how the boardroom situation evolves, whether the strategic review leads to any concrete outcome, and whether CSE can convert its strong order book into sustainable earnings growth.

Related links:

#2 – Hong Leong Asia Ltd (SGX: H22)

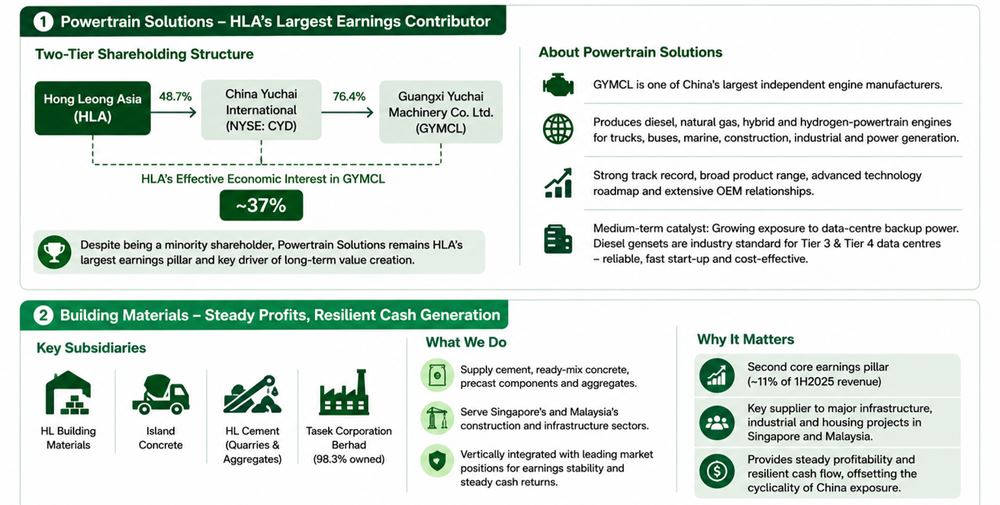

Hong Leong Asia is the industrial manufacturing and distribution arm of Hong Leong Group Singapore.

Its two main businesses are Powertrain Solutions and Building Materials.

Powertrain Solutions covers engines for trucks, buses, industrial equipment and data centre power generation, mainly through its partnership with Yuchai International in China.

Building Materials includes cement, precast concrete, ready-mix concrete and quarry products in Singapore and Malaysia.

The stock has had a strong run, rising more than 100% over the past year.

However, after approaching its high of S$3.88, Hong Leong Asia’s share price pulled back 15.0% month-to-date in June as investors digested a recent equity placement and acquisition.

First, Hong Leong Asia raised S$145 million through a follow-on equity offering, issuing 50 million shares at S$2.90 each. While the placement strengthens its balance sheet and supports future growth, it also increases the share base, which can create near-term selling pressure.

Second, the group completed the acquisition of Yong Tai Loong, or YTL, for S$90.7 million in April 2026.

YTL is a Singapore company with more than 60 years of history, specialising in architectural building products such as bomb shelters, door frames, PVC doors, letterboxes, bicycle racks and clothes racks for HDB flats.

The acquisition expands Hong Leong Asia’s exposure to Singapore’s public housing pipeline.

Management noted that YTL has about 20% market share, an order book stretching three to four years, and a well-automated, asset-light manufacturing base. The business is also cash generative and benefits from high customer stickiness, given that it is one of a small number of approved suppliers for certain building products.

The deal was funded through debt, which has raised some investor concerns over leverage. However, management described the transaction as earnings-accretive, by 4.6% on a reported basis and 18.6% on an adjusted basis excluding one-off costs.

The founders and key management team are also staying on to support a smooth transition.

Over time, there may also be room for YTL to expand beyond residential projects into civil projects and government buildings.

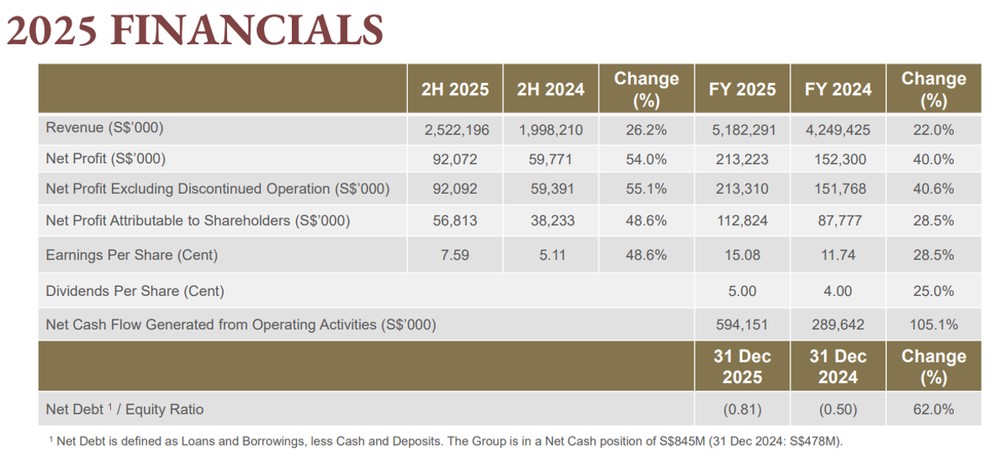

Hong Leong Asia’s latest full-year FY 2025 results remained strong.

Revenue grew 22% year-on-year to S$5.18 billion in FY2025, while net profit rose 29% to S$112.8 million. Earnings per share increased from S$0.12 to S$0.15.

The group paid total dividends of S$0.05 per share for FY2025, representing a payout ratio of about 33%. This appears well supported by cash generation.

Hong Leong Asia also maintained a net cash position of about S$845 million, while net asset value per share reached a five-year high of close to S$1.60.

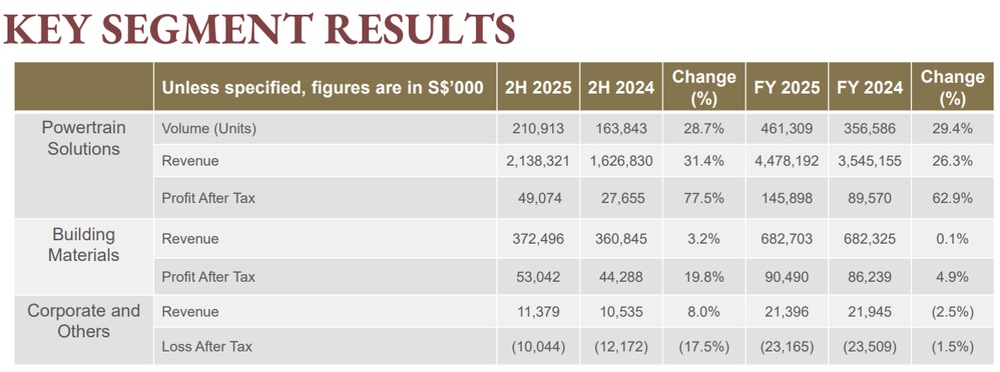

The main driver was the Powertrain Solutions segment.

Yuchai, Hong Leong Asia’s key partner and China’s largest independent engine maker, delivered volume growth of about 29% in FY2025, with around 461,000 units sold. Its profitability rose 63% for the year.

Growth was supported by two drivers.

First, exports of Chinese OEM-branded trucks and industrial machinery continued to grow strongly and now account for nearly a quarter of overall volumes.

Second, China’s domestic commercial vehicle market also recovered, with Yuchai gaining market share. Its on-road segment, which includes trucks and buses, grew 41.5%, well ahead of the broader market.

A smaller but fast-growing opportunity is high-horsepower natural gas engines for data centres. Volumes in this segment nearly tripled year-on-year in FY2025.

These engines also command much higher selling prices, which helped lift Yuchai’s gross margin from 14.7% in FY2024 to 16.5% in FY2025.

Management expects data centres and distributed power stations to remain key drivers of China’s power generator engine market, which is projected to grow strongly through 2030.

There could also be a longer-term catalyst from Yuchai’s preliminary listing application on the Hong Kong Stock Exchange.

If successful, this could provide a public market vehicle for its power generation subsidiary and support future R&D and expansion. However, management has cautioned that the process is still at an early stage.

The Building Materials segment delivered steadier growth. Revenue was broadly flat in FY2025, while profit rose 4.9%.

In Singapore, the precast business benefited from HDB-related demand.

Ready-mix concrete faced some near-term disruption from temporary land lease expirations at batching plant sites, but Hong Leong Asia has started addressing this through new site sign-ups.

One new batching plant began operations during the year, with another expected in 1H2027.

The group has also introduced larger 14 cubic metre trucks, which can carry about 45% more material per trip. This should help improve productivity and energy efficiency.

In Malaysia, the ready-mix business faced cost pressures from tax changes and stricter transport enforcement rules, but margins held up as pricing adjustments were passed through to customers.

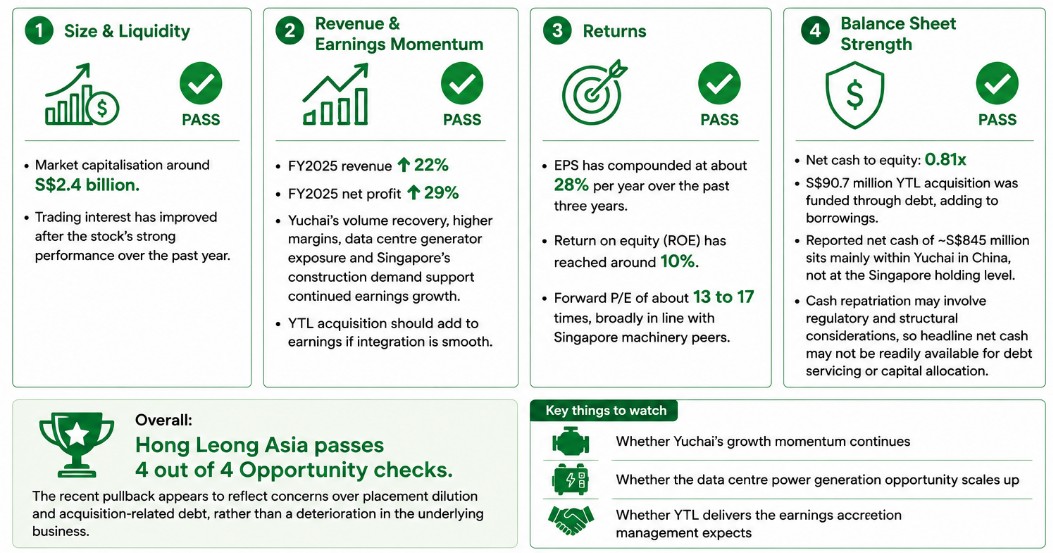

Hong Leong Asia continues to screen positively on Beansprout’s Opportunity framework.

Source: Beansprout

The company has sufficient size and liquidity, with a market capitalisation of around S2.4 billion. Trading interest has also improved after the stock’s strong performance over the past year.

Revenue and earnings momentum are healthy. FY2025 revenue rose 22%, while net profit increased 29%.

Yuchai’s volume recovery, higher margins, data centre generator exposure and Singapore’s construction demand point to continued earnings support.

The YTL acquisition should also add to earnings if integration is smooth.

Returns have improved as well. Earnings per share have compounded at about 28% per year over the past three years, while return on equity has reached around 10%.

Hong Leong Asia is in a net cash position.

Despite sitting on a net cash to equity of 0.81x as of end-December 2025, the S$90.7 million YTL acquisition was funded through debt, adding to borrowings at the group level.

While Hong Leong Asia reported a net cash position of about S$845 million as at FY2025, investors should note that much of this cash sits within Yuchai in China, rather than at the Singapore holding company level.

This matters because repatriating cash from China may involve regulatory and structural considerations. As a result, the group’s headline net cash position may not be as readily available for debt servicing or capital allocation as it appears.

Overall, Hong Leong Asia passes four of our four Opportunity checks.

The recent pullback appears to reflect concerns over placement dilution and acquisition-related debt, rather than a deterioration in the underlying business.

For investors, the key things to watch are whether Yuchai’s growth momentum continues, whether the data centre power generation opportunity scales up, and whether YTL delivers the earnings accretion management expects.

Related links:

- Hong Leong Asia latest valuation, share price and analysis

- Hong Leong Asia dividend history and forecast

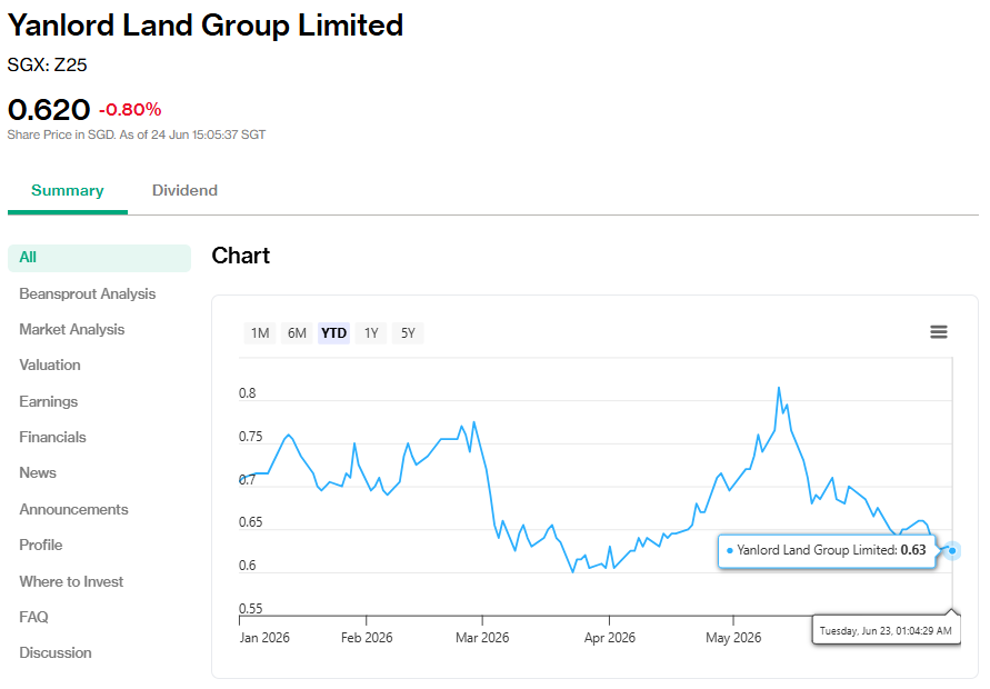

#3 – Yanlord Land Group Limited (SGX: Z25)

Yanlord Land Group is a Singapore-listed property developer focused on high-end residential, commercial and integrated developments in China.

The group also owns a portfolio of investment properties and hotels in Singapore through its acquisition of United Engineers.

These include UE BizHub CITY, UE BizHub TOWER, Rochester Mall and Park Avenue hotels.

Yanlord’s share price has traded between S$0.38 and S$0.825 over the past year.

While the stock has recovered from its lows, it fell 10.7% month-to-date in June, giving back part of its earlier gains.

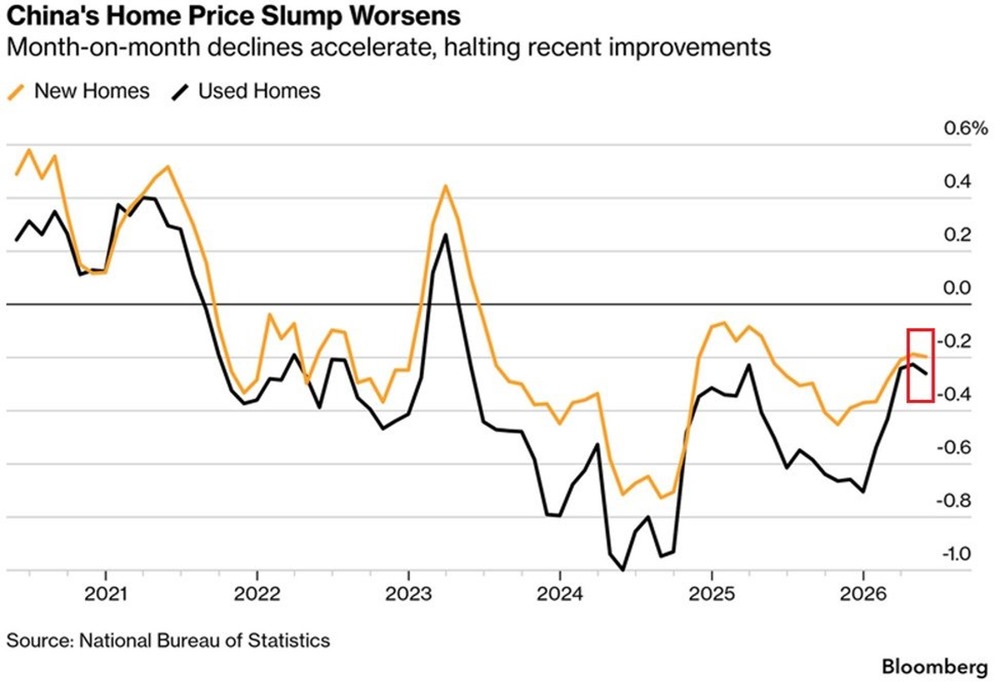

The main headwind remains China’s property market.

New home prices across 70 Chinese cities fell 0.2% month-on-month in May, while resale home prices declined 0.26%, the sharpest monthly fall in three months.

The recovery has also been uneven.

Some of the strongest signs of improvement have been seen in larger and wealthier cities, such as Hangzhou, which has benefited from stronger technology and AI-related investment activity. In contrast, many Tier 2 cities continue to face softer demand.

This matters for Yanlord because its exposure is spread across cities such as Nanjing, Suzhou, Zhuhai, Chengdu and Tianjin, where the recovery may be less consistent.

Yanlord acknowledged this in its response to shareholder questions ahead of its 2026 AGM.

Management said the China property sector is undergoing a structural adjustment after years of rapid expansion, and that recovery remains uneven across cities and segments. It also noted that the previous high-growth, high-leverage development model has become less common, with the industry moving towards more balanced and resilient business models.

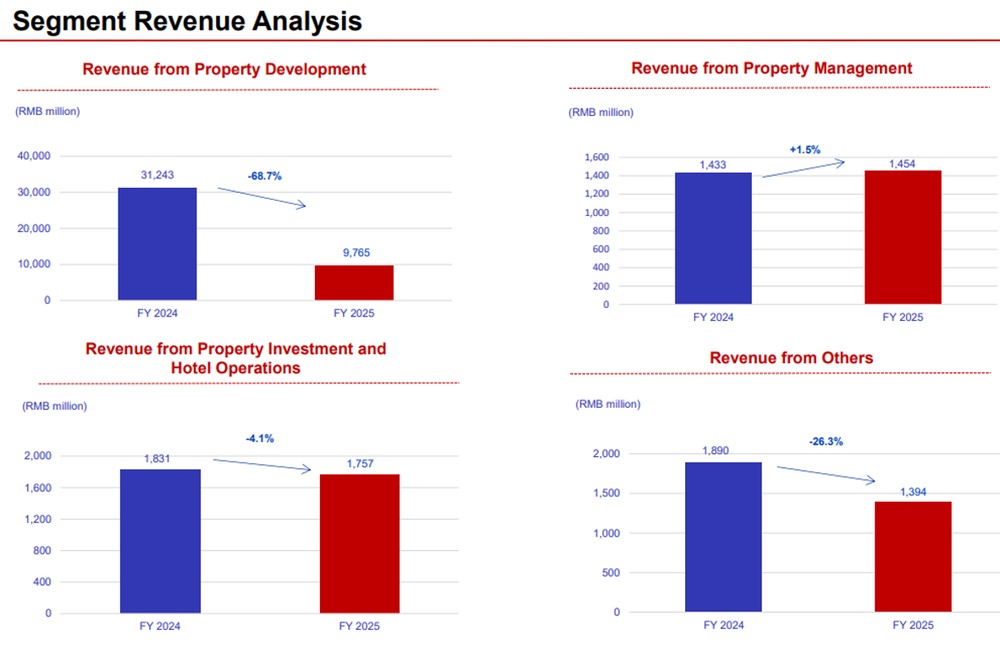

Yanlord returned to profit in FY2025, but its underlying business momentum remains weak.

Revenue fell 60.5% year-on-year to RMB14.4 billion, mainly due to a 68.7% decline in property development revenue as the group delivered fewer completed units.

Despite the sharp revenue decline, Yanlord returned to profitability.

The group reported profit for the year of RMB435 million, reversing a loss of RMB3.8 billion in FY2024. This was helped by a stronger gross margin, which improved from 9.4% to 27.9%, as well as a steep fall in impairment losses.

However, the recovery was not broad-based. In 2H2025,

Yanlord reported a loss of RMB110 million, as revenue recognition slowed and gross margin narrowed to 19.7%. This suggests that the full-year profit was supported more by favourable project mix and lower impairments than by a sustained demand recovery.

Contracted sales also remained weak.

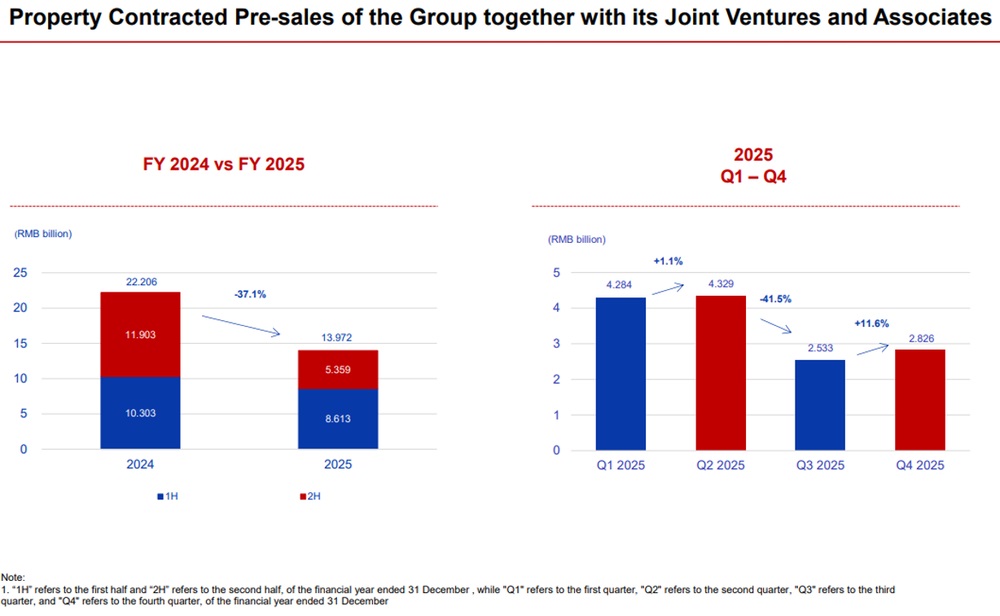

Yanlord and its joint ventures recorded contracted pre-sales of RMB14.0 billion in FY2025, down 37.1% from the previous year. Contracted gross floor area fell 33.0%.

The quarterly trend was mixed.

Pre-sales were broadly stable in the first half of the year, fell sharply in the third quarter, and recovered slightly in the fourth quarter. This suggests demand remains uneven rather than firmly improving.

One positive is that Yanlord had RMB17.5 billion of contracted pre-sales pending revenue recognition as at 31 December 2025. This provides some near-term revenue visibility for 1H2026 and beyond.

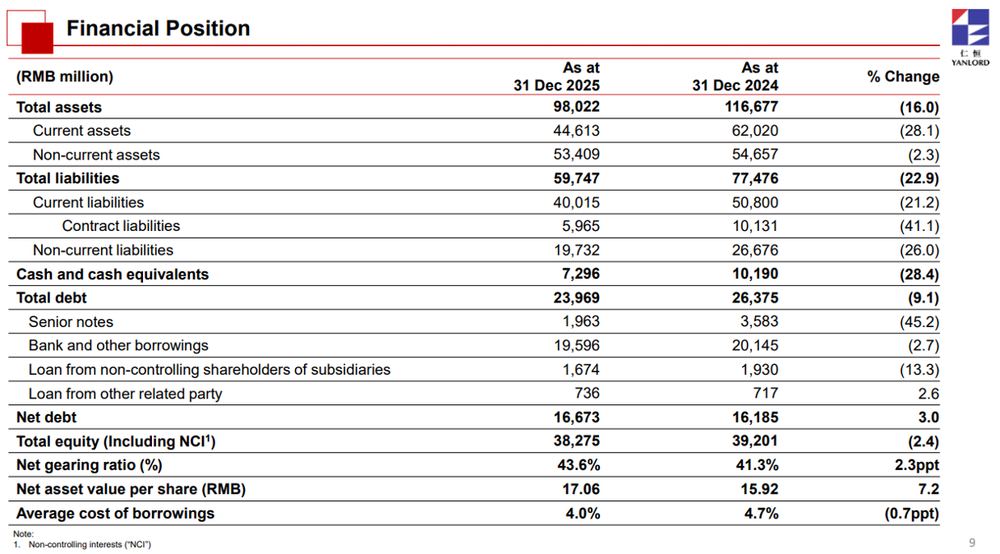

On the balance sheet, total debt fell 9.1% to RMB24.0 billion, while the average borrowing cost improved from 4.7% to 4.0%.

However, cash and cash equivalents declined 28.4% to RMB7.3 billion, while net gearing edged up to 43.6%. Bank and other borrowings due within one year stood at RMB5.9 billion.

Management has described its liquidity position as adequate, supported by internal cash, property sales proceeds and refinancing from existing banking relationships. Still, the decline in cash and upcoming debt maturities are worth watching.

Yanlord also trades at a steep discount to its net asset value per share of S$3.13.

Management attributed the valuation gap to weaker confidence in China’s property sector and impairment losses recognised in FY2025. However, it did not rule out further impairments, noting that changes in market conditions, assumptions or development plans may affect the carrying value of properties.

A potential near-term catalyst is the reported possible sale of a 50% stake in 79 Anson Road, part of Yanlord’s Singapore portfolio. The company has declined to comment on market speculation, but such a transaction could strengthen cash flow and support debt reduction if it materialises.

For 1H2026, Yanlord plans new project launches across the Yangtze River Delta, Hainan and the Bohai Rim, including Nantong, Suzhou, Wuxi, Taicang, Haikou and Jinan. The group did not acquire new landbank in FY2025 and said it will only consider doing so when there are clearer signs of a sustained market recovery.

Yanlord does not screen strongly on Beansprout’s Opportunity framework at this stage.

Its market capitalisation is around the S$500 million level, which is close to our minimum threshold. However, trading liquidity can be thin.

Revenue and earnings momentum remain weak.

Revenue fell 60.5% in FY2025, contracted pre-sales declined 37.1%, and the group returned to a loss in 2H2025. Consensus also expects near-term EPS losses, suggesting that earnings visibility remains limited.

The balance sheet is another key risk.

While total debt declined, Yanlord still had RMB24.0 billion of debt, net gearing of 43.6%, cash down 28.4% year-on-year, and RMB5.9 billion of borrowings due within one year. Management has described liquidity as adequate, but the margin for error remains limited.

Returns are also not a strong positive factor for now.

The FY2025 profit was helped by lower impairments and favourable project mix, rather than a clear operational rebound. With the second half turning loss-making and consensus expecting near-term losses, ROE is not yet a meaningful support.

Overall, Yanlord passes fewer than two of our four Opportunity checks.

The stock remains a macro call on when China’s property market stabilises, especially in Yanlord’s key cities across the Yangtze River Delta and Greater Bay Area.

A potential 79 Anson Road divestment could provide a near-term catalyst, but investors may want to see clearer signs of stronger contracted sales, improved cash flow and lower balance sheet risk before turning more constructive.

Related links:

What would Beansprout do?

All three stocks have underperformed the iEdge Singapore Next 50 Index month-to-date in June 2026, but for very different reasons.

CSE Global’s pullback appears to be driven more by governance uncertainty than weaker operations.

With 1Q2026 revenue up 29%, record order intake and a S$716 million order book, the underlying business remains strong, but I would watch for clarity on the new Lead Independent Director appointment and strategic review. Learn more about CSE Global Limited here.

Hong Leong Asia looks the most interesting among the three.

The recent pullback reflects concerns over placement dilution and acquisition-related debt, but its underlying earnings momentum remains supported by Yuchai’s data centre power generation tailwind and the accretive YTL acquisition. Learn more about Hong Leong Asia here.

Yanlord is the name I would be most cautious on for now.

While its return to profit in FY2025 is encouraging, falling pre-sales, net gearing of 43.6% and continued weakness in China’s property market make it more of a speculative recovery play. Learn more about Yanlord here.

Overall, CSE Global still looks operationally strong but needs governance clarity, Yanlord requires more evidence of property market recovery, while Hong Leong Asia appears to offer the most balanced opportunity after its recent pullback.

We have also taken a deeper look at Singapore’s construction upcycle, and how government spending and infrastructure demand may support companies across the construction value chain.

For a broader look at the long-term themes that may support Singapore stocks, you can also learn more about our key market growth themes here.

For investors looking for higher-conviction ideas beyond the STI, our Opportunity Pot framework looks at factors such as size and liquidity, revenue and earnings momentum, returns, and balance sheet strength.

You can use Beansprout’s 4-factor screener to find stocks that meet these criteria.

Which Singapore stocks are you watching as government spending and infrastructure demand continue to support the construction sector? Share your thoughts in the comments below or join the discussion in our Beansprout Telegram community.

Planning to invest in stocks? Check out Beansprout's guide to the best stock trading platforms in Singapore with the latest promotions and see the latest promotions and sign-up rewards available.

Enjoyed this insight? Follow Beansprout on Telegram, Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments