Beyond blue chips: 3 Singapore tech stocks riding the AI boom. What should investors watch?

Stocks

By Gerald Wong, CFA • 22 May 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

Singapore tech stocks have surged on the AI boom. I look at AEM, UMS and Frencken, and what investors should watch after the rally.

What happened?

Singapore tech stocks have had a strong run this year.

The global AI rally has become harder to ignore, even as investors continue to debate whether expectations have run too far.

Earlier, we highlighted why Singapore stocks may still be worth watching beyond their dividend appeal, with AI and data centres emerging as one of the market’s structural growth themes.

Investors are looking for Singapore-listed companies that can offer exposure to the global AI and semiconductor upcycle.

For Singapore investors, the AI opportunity may extend across the technology value chain, including semiconductors, testing, precision engineering and advanced manufacturing.

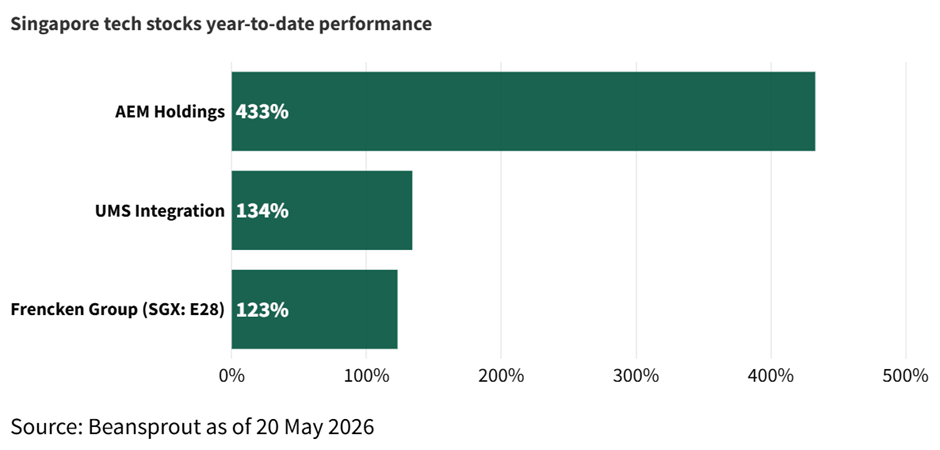

Three names have stood out: AEM Holdings, UMS Integration and Frencken Group.

Against this backdrop, there has been active discussion within the Beansprout community on whether Singapore technology stocks still have room to run after their sharp gains or has much of the good news been priced in.

In this article, I look at three Singapore tech stocks trading near recent highs, what has driven their rally, and what investors should watch before chasing the gains and how they stack up against the key metrics we focus on in our investment framework: earnings growth, return on equity, and balance-sheet strength.

Why Singapore tech stocks are gaining from the AI boom

The first phase of the AI rally was about obvious winners.

Nvidia sold the chips. The hyperscalers bought them. TSMC manufactured them. Investors followed the money.

But AI is not just a chip story.

AI chips need to be designed, fabricated, packaged, tested, assembled and integrated into increasingly complex systems. As chips become more powerful, the supporting ecosystem becomes more important.

That is where some Singapore-listed companies come in.

They may not own the AI platforms. They may not build the most advanced GPUs. But they sit in parts of the value chain that become more relevant when semiconductor complexity rises.

Testing becomes harder. Precision engineering becomes more important. Equipment supply chains become tighter. Manufacturing partners with the right capabilities become more valuable.

This is the investment case behind the rally in AEM, UMS and Frencken.

But as always, the market has moved first.

Now investors need to decide whether earnings can catch up.

#1 – AEM Holdings (SGX: AWX)

AEM is the most direct AI-related name among the three.

The company provides semiconductor and electronics test solutions, with exposure to advanced semiconductor testing, high-performance computing and AI-related chip applications.

This matters because AI chips are not ordinary chips.

They are more power-dense, more thermally complex and more difficult to test. As AI workloads scale, testing is no longer a boring back-end process. It becomes a bottleneck, a quality-control function and potentially a source of competitive advantage.

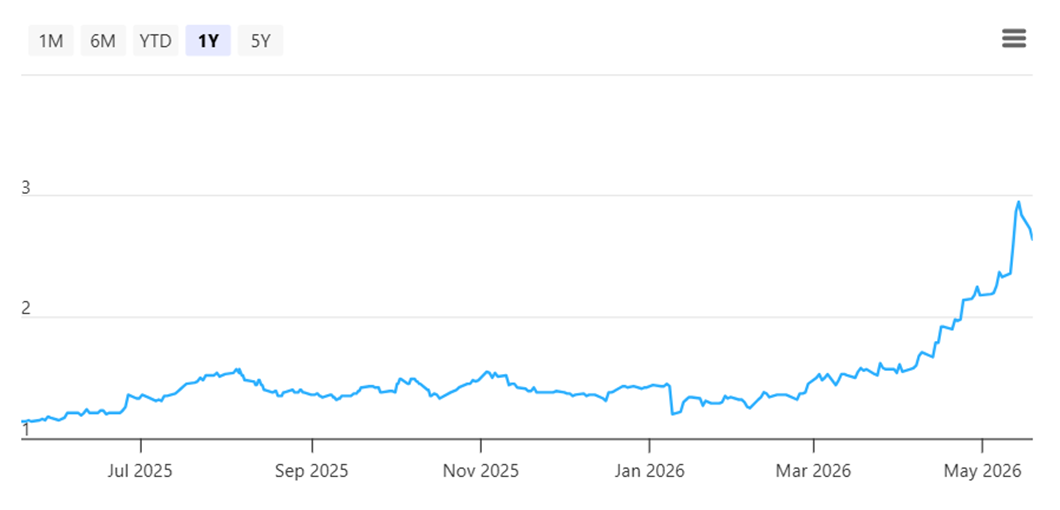

This could help explain its strong share price performance. AEM’s share price stood at S$9.16 as of 20 May 2026, after touching S$10.68 on 15 May 2026. The stock has surged by about 433% year-to-date, making it one of the strongest-performing Singapore tech stocks in 2026.

The latest results gave investors reason to believe the rally was not purely speculative.

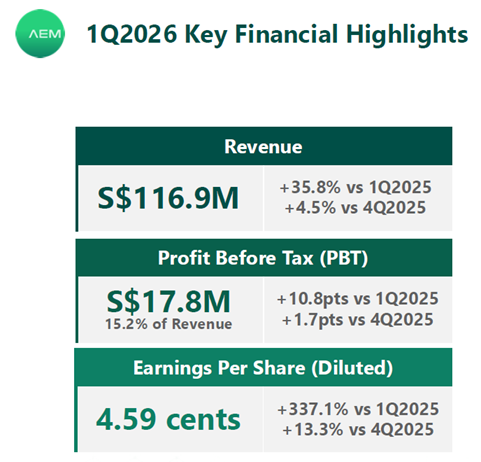

For 1Q2026, revenue rose 35.8% year-on-year to S$116.9 million, while net profit jumped 329.4% to S$14.3 million.

Diluted earnings per share rose 337% to 4.59 cents, meaning earnings growth significantly outpaced revenue growth.

The key driver was continued production ramp-up from its fabless AI and high-performance computing (HPC) customer, alongside improving demand from its PC and foundry customer.

The standout was Test Cell Solutions. Revenue from the segment rose 72.0% year-on-year to S$88.1 million, accounting for more than three-quarters of group revenue.

However, profitability is still recovering from a low base. AEM’s current return-on-equity (ROE) stands at 3.46%, which remains far below the levels it achieved during its previous earnings upcycle.

The balance sheet is a strength. AEM has a net debt-to-equity ratio of -0.12, which means it is in a net cash position.

However, the sharp rally also means expectations have risen significantly.

In short, AEM has strong earnings acceleration and a healthy balance sheet, but ROE still needs to improve meaningfully to justify the higher valuation.

AEM is no longer being valued simply as a cyclical recovery stock. The market is now asking whether it can become a structural beneficiary of AI and high-performance computing demand.

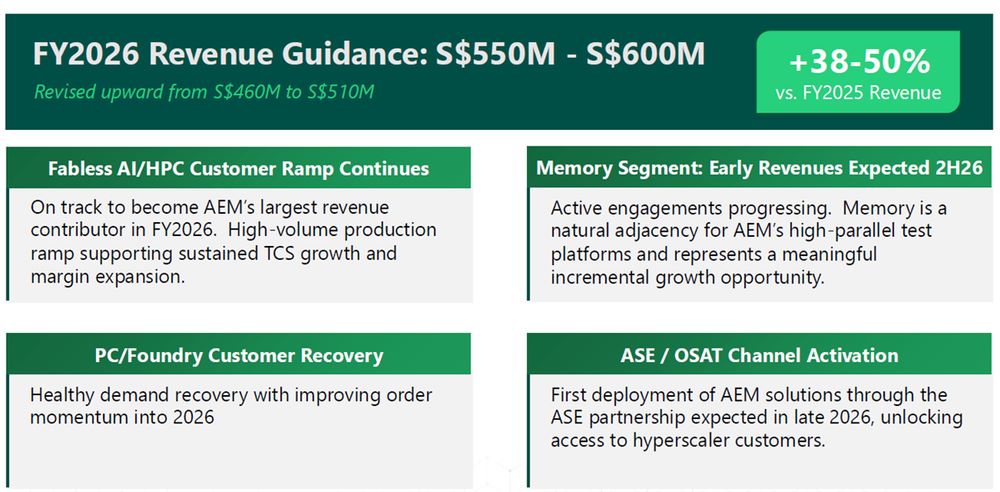

Management also raised FY2026 revenue guidance to S$550 million to S$600 million, around 20% above its earlier range.

Another potential catalyst is AEM’s strategic partnership with ASE Technology, one of the world’s leading providers of semiconductor assembly and testing services. Under the partnership, an ASE subsidiary agreed to subscribe for S$12 million of new AEM shares, while the collaboration aims to accelerate AI and HPC test innovation.

AEM said the partnership could open up new opportunities, including hyperscaler clients, with first deployment of its solutions expected in late 2026.

If AI and high-performance computing demand continues to grow, testing could become an even more important part of the semiconductor value chain. AEM may benefit if more customers require high-volume testing solutions for increasingly complex chips.

However, the sharp rally also means expectations have risen significantly.

At current levels, investors are no longer buying AEM as a cheap cyclical recovery stock. They are paying for stronger execution, sustained AI/HPC revenue contribution, and margin improvement.

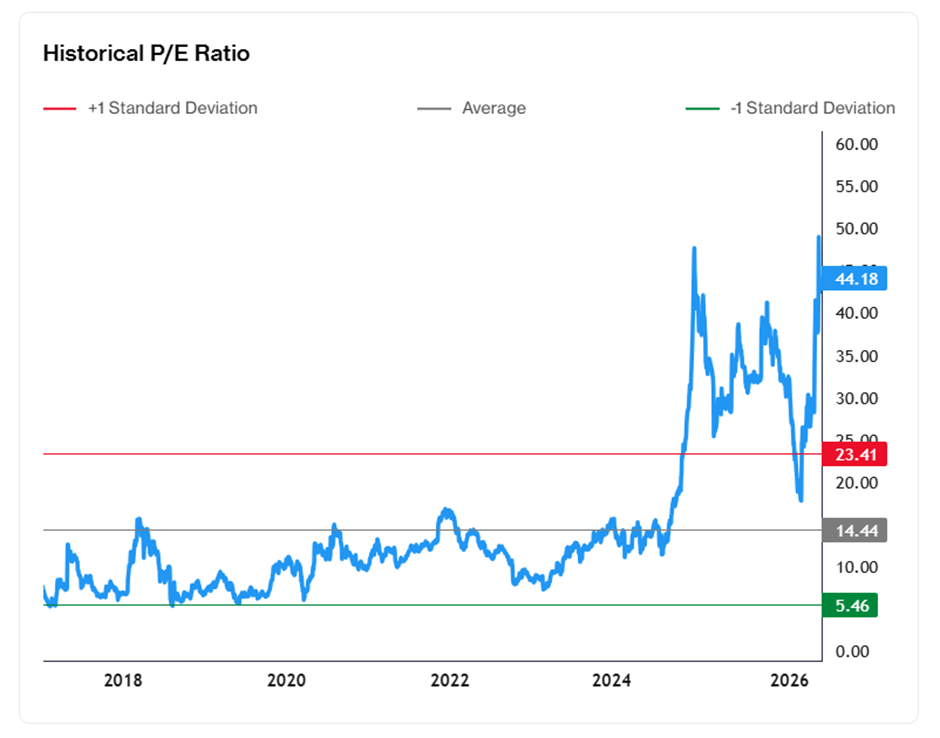

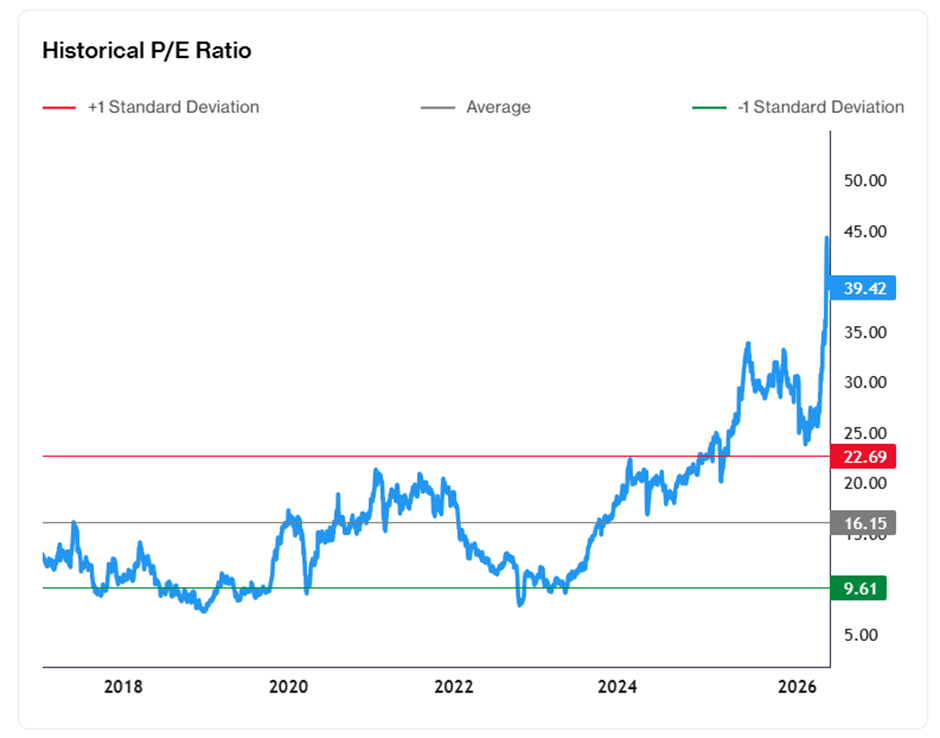

Valuation has also become more demanding. AEM’s current P/E ratio was 42.4x, above its historical average P/E ratio of 14.42x.

From here, the market will want evidence that the AI/HPC ramp is durable, rather than just a one-quarter boost.

The key question for AEM is simple: can it turn a strong AI-related recovery into a multi-year earnings cycle?

Related links:

- AEM Holdings latest valuation, share price and analysis

- AEM Holdings dividend history and dividend forecast

#2 – UMS Integration (SGX: 558)

UMS is a different kind of AI trade.

It is less direct than AEM, but still plugged into the semiconductor supply chain. The company manufactures high-precision components and provides electromechanical assembly and final testing services for customers in semiconductor equipment, aerospace and precision engineering.

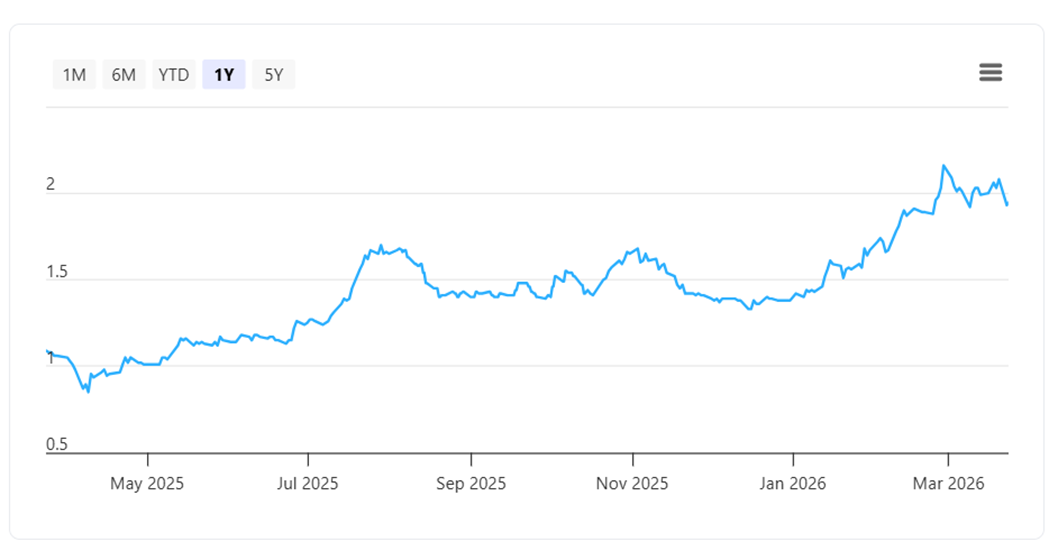

UMS’ share price has risen by about 134% year-to-date, supported by stronger interest in semiconductor equipment-related names. Its share price reached a high of S$3.15 before retreating to around S$2.65 as of 20 May 2026.

UMS benefits when the semiconductor equipment cycle improves. If chipmakers continue investing in capacity, advanced packaging and AI-related production, suppliers like UMS may see stronger demand.

That is already showing up in its results.

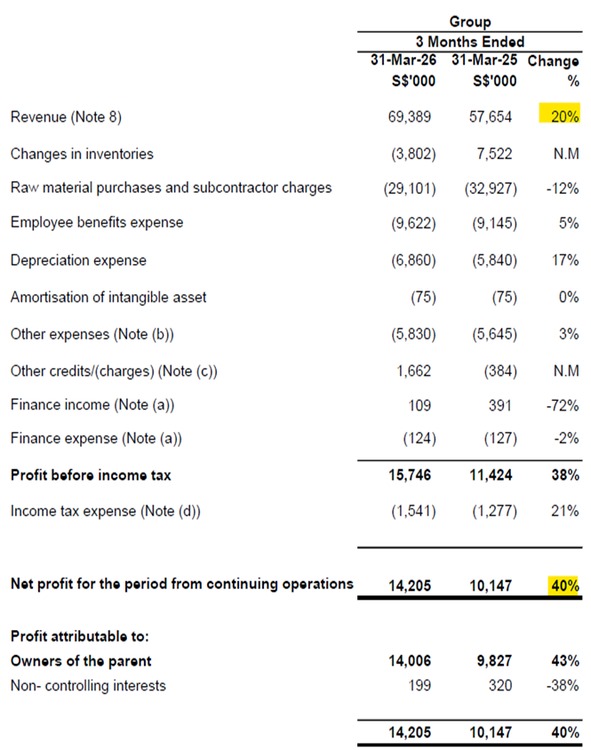

For 1QFY2026, revenue rose 20% year-on-year to S$69.4 million, while net attributable profit increased 43% to S$14.0 million.

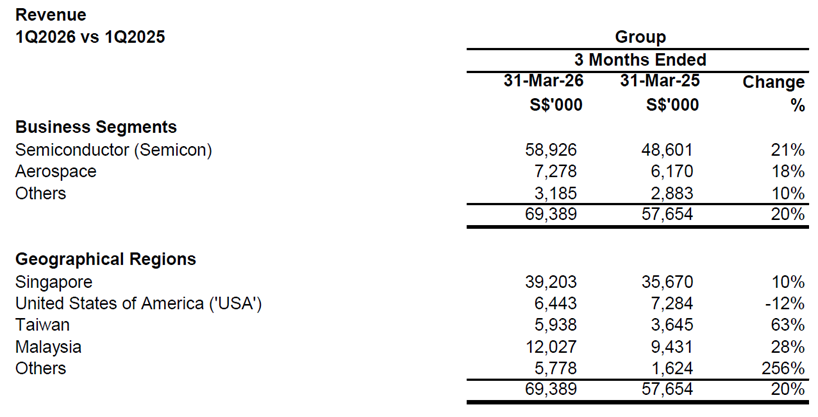

Growth was broad-based, with semiconductor revenue up 21%, aerospace revenue up 18%, and the “Others” segment up 10%.

Within the semiconductor business, component sales rose 26% to S$36.5 million, driven by stronger demand from a new customer, while semiconductor integrated system sales grew 14% to S$22.4 million.

The stronger performance was broad-based, with all core business segments reporting double-digit sales growth.

UMS’ semiconductor business grew 21% year on year, while aerospace revenue rose 18%. Revenue from its “Others” segment also increased 10%.

Within the semiconductor business, component sales rose 26% year on year to S$36.5 million, driven by higher demand from a new customer. Semiconductor Integrated System sales grew 14% year on year to S$22.4 million.

Its ROE is also stronger than AEM’s. UMS’ current ROE stands at 10.41%, suggesting better capital efficiency at this stage of the cycle.

The balance sheet also appears comfortable. UMS has a net debt-to-equity ratio of -0.04, which means it remains in a net cash position.

The more interesting part of the story is UMS’ pipeline of new product introductions, or NPIs.

UMS’ new key customer is contributing significant NPI activity, with many products still undergoing qualification. This matters because NPI work can be an early sign of future production demand. If these products are successfully qualified and move into volume production, they could expand UMS’ revenue base over time.

This gives UMS a longer growth runway. A new major customer can diversify revenue, improve utilisation and position the company for future programmes in advanced packaging and AI-related tools.

However, investors should not ignore the risks.

Semiconductor equipment remains a cyclical business. Demand can look strong when customers are expanding capacity, but it can slow quickly if orders are delayed, inventories build, or capex plans are pushed back.

NPI activity also takes time to convert into meaningful revenue. Products need to be qualified, customers need to ramp production, and order volumes still depend on the broader semiconductor capex cycle.

Valuation has also become more demanding. UMS’ current P/E ratio stands at around 38.1 times, compared with its historical average of 16.1 times.

The market is already assuming that the upcycle has legs.

For UMS, the key question is not whether the latest quarter was strong. It was. The real question is whether the new customer ramp-up and NPI pipeline can turn today’s cyclical recovery into a more durable earnings cycle.

Related links:

- UMS Integration latest valuation, share price and analysis

- UMS Integration dividend history and dividend forecast

#3 – Frencken Group (SGX: E28)

Frencken is the most diversified of the three.

That makes it more stable in some ways, but also less of a pure AI story.

The company provides high-technology manufacturing solutions across semiconductors, medical, analytical life sciences, industrial automation and automotive.

Its business includes product design, development, prototyping, engineering, final testing and series manufacturing.

This gives Frencken a broader earnings base than AEM or UMS.

But the trade-off is that investors may not get the same direct exposure to AI/HPC testing or semiconductor equipment demand.

The stock has still rallied strongly.

Frencken’s share price stood at S$3.05 as of 20 May 2026, after touching S$3.52 on 15 May 2026. The stock has risen by about 123% year-to-date, reflecting renewed optimism around its semiconductor and high-technology manufacturing exposure.

However, the latest results were more mixed than the share price performance suggests.

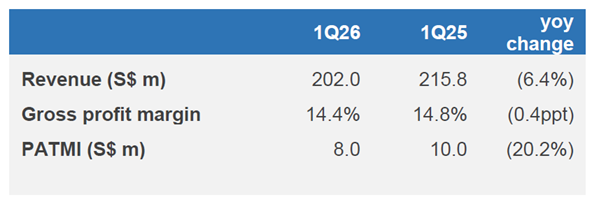

For 1Q2026, revenue fell 6.4% year-on-year to S$202.0 million. Net profit attributable to shareholders declined 20.2% to S$8.0 million, partly due to a foreign exchange loss of S$1.1 million.

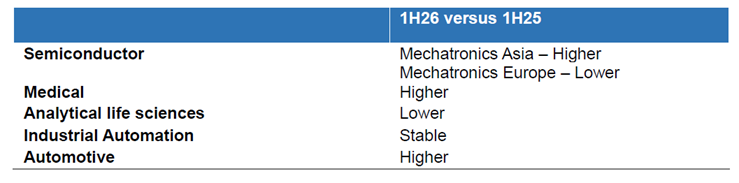

Unlike AEM and UMS, earnings did not outpace revenue growth. Instead, earnings fell faster than revenue, partly due to lower contributions from the semiconductor and analytical life sciences segments in Mechatronics Europe, as well as a foreign exchange loss.

The semiconductor segment remained important, accounting for 48.9% of group revenue.

But semiconductor revenue fell 7.0% year-on-year to S$98.8 million. Strength in Mechatronics Asia was offset by weaker sales from Mechatronics Europe.

The company is exposed to the semiconductor upcycle, but the recovery is not yet evenly reflected across the business.

Its ROE stands at 8.58%, below UMS but above AEM. This suggests reasonable, but not exceptional, capital efficiency.

The balance sheet remains a clear strength. Frencken has a net debt-to-equity ratio of -0.15, meaning it is also in a net cash position.

Management remains positive in FY2026. It expects stronger business momentum in the second half, supported by customer projections, stronger capabilities and continued execution. That gives investors something to look forward to.

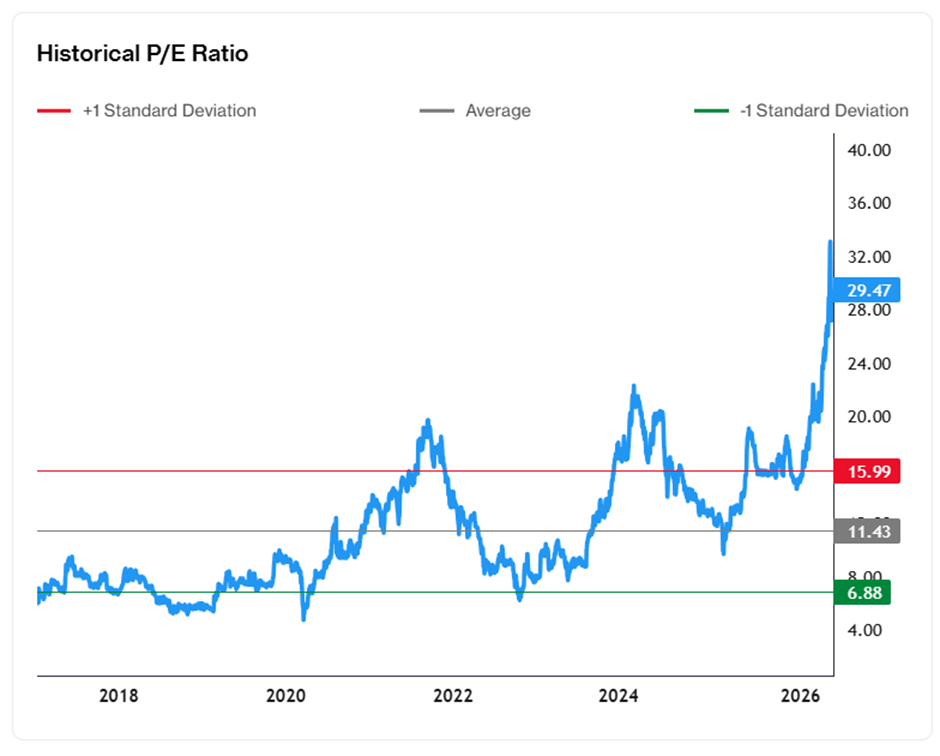

But again, the valuation has moved ahead. Frencken’s current P/E ratio was around 29.3 times, compared with its historical average of 11.42 times.

For Frencken, the market is pricing in on a second-half recovery.

Now the company needs to deliver it.

The key thing to watch is whether Mechatronics Asia can sustain growth, Mechatronics Europe can recover, and earnings can catch up with the share price.

Related links:

- Frencken Group latest valuation, share price and analysis

- Frencken Group dividend history and dividend forecast

What would Beansprout do?

The rally in AEM, UMS and Frencken shows that investors are increasingly willing to pay for Singapore-listed exposure to AI, semiconductors and advanced manufacturing, one of the growth themes we have highlighted.

But after such sharp share price gains, investors should not rely on the AI narrative alone.

This is where I would fall back on our Beansprout’s 4-factor Opportunity framework: investability, profitability, earnings growth quality and balance sheet strength.

AEM has the strongest earnings growth momentum, with net profit growing much faster than revenue in the latest quarter, but its ROE remains low and still needs to recover meaningfully. Learn more about AEM here.

UMS offers the most balanced profile, with earnings growth outpacing revenue growth, a healthier ROE, and support from new product introductions that could extend its growth runway. Learn more about UMS here.

Frencken has the broadest business base and a reasonable ROE, but its latest quarter showed earnings declining faster than revenue, which means the recovery still needs to be proven. Learn more about Frencken here.

On balance sheet strength, all three companies are in net cash positions, giving them flexibility to invest through the cycle.

However, investors should watch whether future expansion, capex or working capital needs start to absorb more cash.

I would watch if their earnings recovery can be strong enough, and durable enough, to justify the sharp re-rating that has already happened.

For investors who want to understand the broader AI opportunity, you can read our guide on how to invest in AI, where we look at the different parts of the AI value chain beyond just the big US technology stocks.

You can also read our take on whether the AI rally has gone too far, where we discuss the reasons the rally may be real, as well as the warning signs investors should watch.

At the same time, I would not limit my search for long-term growth opportunities to technology stocks alone.

There may also be other avenues to capture structural growth in the Singapore market, including companies linked to infrastructure, data centres, energy security and regional expansion. If you are looking for more Singapore stock ideas linked to long-term growth themes, you can explore our high-conviction curated stock opportunities here.

You can also screen for stocks that meet Beansprout’s 4-factor Opportunity framework here.

Which Singapore stocks are you watching as AI and other long-term growth themes gain momentum? Share your thoughts in the comments below or join the discussion in our Beansprout Telegram community.

Planning to invest in tech stocks and ETFs? Check out Beansprout's guide to the best stock trading platforms in Singapore with the latest promotions and see the latest promotions and sign-up rewards available.

Enjoyed this insight? Follow Beansprout on Telegram, Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments