3 Singapore blue-chip REITs near 5-year lows with dividend yields around 6%. Are they worth considering for income?

REITs

By Gerald Wong, CFA • 13 May 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

We take a closer look at three Singapore blue-chip REITs that are trading near 5-year lows and offering dividend yield of around 6%.

What happened?

Several Singapore blue-chip REITs are trading near their 5-year lows.

This caught my attention after we recently looked at whether Singapore REIT dividend yields are still attractive with the recent bounce, and how some REITs are trying to grow their distributions through acquisitions.

Despite these developments, not all REITs have recovered with some blue-chip REITs remaining near the low end of their 5-year price range.

Many in the Beansprout community have been asking whether these lower prices present an opportunity to build exposure, or if they reflect concerns over DPU growth and interest costs.

In this article, I look at three Singapore blue-chip REITs trading near 5-year lows, and whether their dividend yields are worth considering.

3 Singapore blue-chip REITs trading near 5-year lows with dividend yield of around 6%

#1 – CapitaLand Ascendas REIT (SGX: A17U)

CapitaLand Ascendas REIT, or CLAR, is Singapore’s first and largest listed business space and industrial REIT. Its portfolio is anchored in Singapore, but also includes assets in the US, Australia, the UK and Europe.

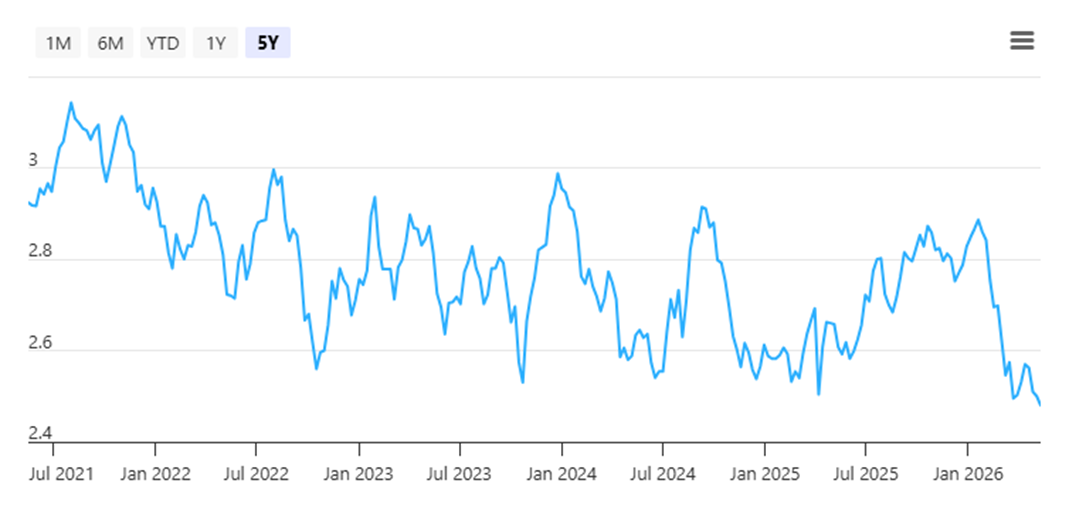

CLAR’s share price is around S$2.47 as of 12 May 2026 and trading near the low end of its 5-year range, while its dividend yield has become more attractive after the decline in share price.

What stands out from CLAR’s latest 1Q 2026 business update is that the REIT is still actively expanding its portfolio despite the weaker market sentiment.

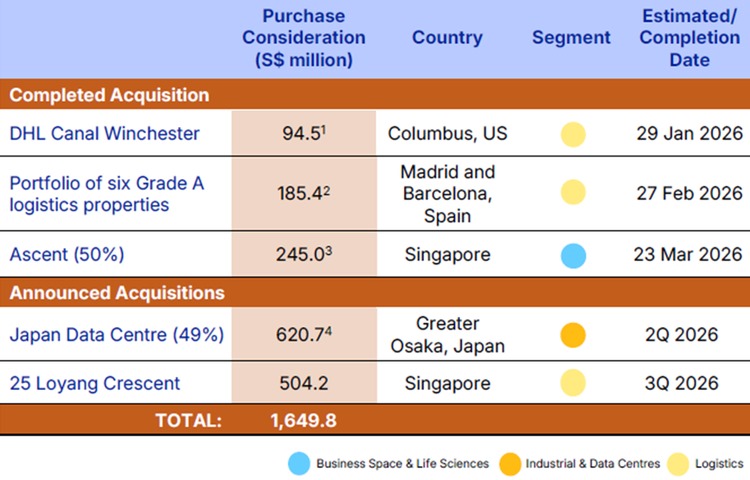

In 1Q 2026, CLAR completed or announced about S$1.6 billion of acquisitions, including DHL Canal Winchester in the US, a portfolio of six Grade A logistics properties in Spain, a 50% stake in Ascent at Singapore Science Park, a 49% stake in a Japan data centre, and 25 Loyang Crescent in Singapore.

These acquisitions are expected to be potentially DPU-accretive, with initial NPI yields ranging from 4.3% to 7.4% before transaction costs.

This gives CLAR several potential growth drivers.

The Japan data centre acquisition marks its first investment in Japan and expands its global data centre footprint, while 25 Loyang Crescent adds a fully occupied logistics and industrial asset in Singapore with a long WALE.

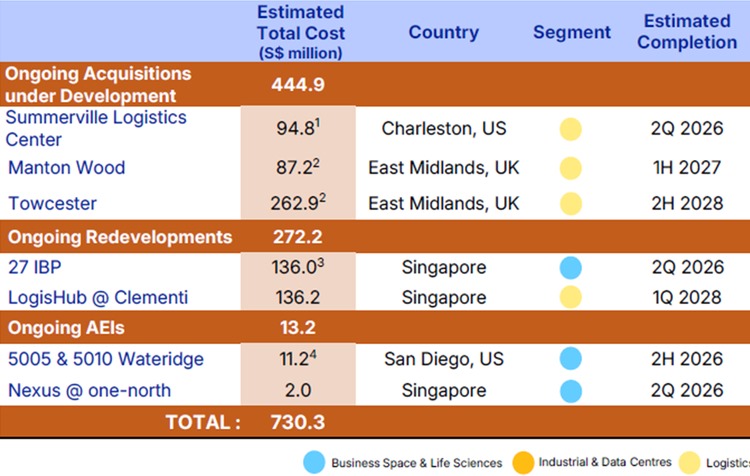

CLAR also has seven ongoing development and asset enhancement projects, with an estimated total cost of S$730.3 million, which could support future portfolio rejuvenation.

However, the latest 1Q 2026 operating metrics were mixed.

Portfolio occupancy fell slightly to 90.5% as at 31 March 2026, from 90.9% at end-2025. Singapore occupancy declined to 90.6%, while US occupancy remained lower at 85.7%.

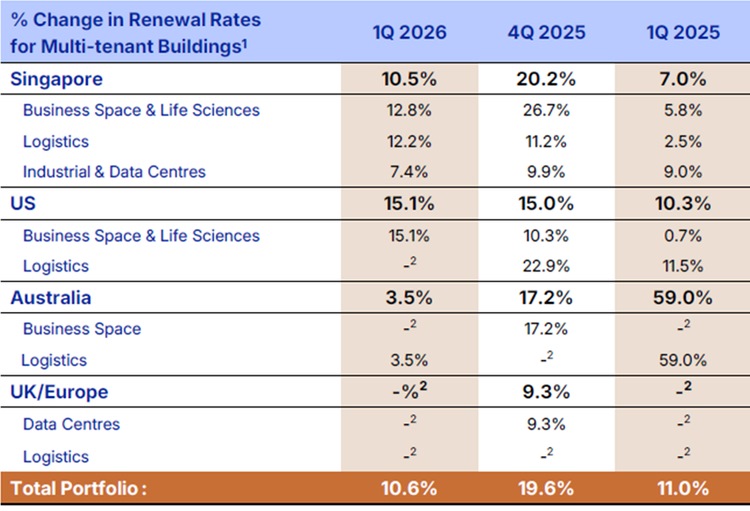

The positive point is that rental reversions remained healthy at 10.6% in 1Q 2026, although CLAR expects rental reversions for FY2026 to moderate to the mid-single-digit range.

Gearing is also an area to watch.

CLAR’s aggregate leverage rose to 42.0% as at 31 March 2026 after recent acquisitions, although this is expected to improve to about 37.3% after its S$903.5 million equity fundraising, assuming the proceeds are used to repay debt facilities.

Its weighted average all-in cost of debt remained at 3.5%.

For FY2025, CLAR reported DPU of 15.005 Singapore cents, slightly lower than 15.205 cents in FY2024. Based on its unit price of S$2.46 as of 12 May 2026, CLAR offers a forward dividend yield of 6.3% and a Trailing Twelve Months (TTM) dividend yield of 7.6%.

CLAR’s lower share price and higher yield make it more interesting, but I would watch whether its new acquisitions and redevelopment projects can offset dilution from the recent equity fundraising and support sustainable DPU growth.

Find out how much dividends you would have received as a unitholder of CapitaLand Ascendas REIT in the past 12 months with the calculator below.

Related links:

- CapitaLand Ascendas REIT latest valuation, share price and analysis

- CapitaLand Ascendas REIT dividend history and forecast

- Capitaland Ascendas REIT invests S$1.4 billion in Singapore and Japan assets

- CapitaLand Ascendas REIT Preferential Offering - What should unitholders do?

#2 – Mapletree Industrial Trust (SGX: ME8U)

Mapletree Industrial Trust, or MIT, owns a diversified portfolio of industrial properties and data centres across Singapore, North America and Japan.

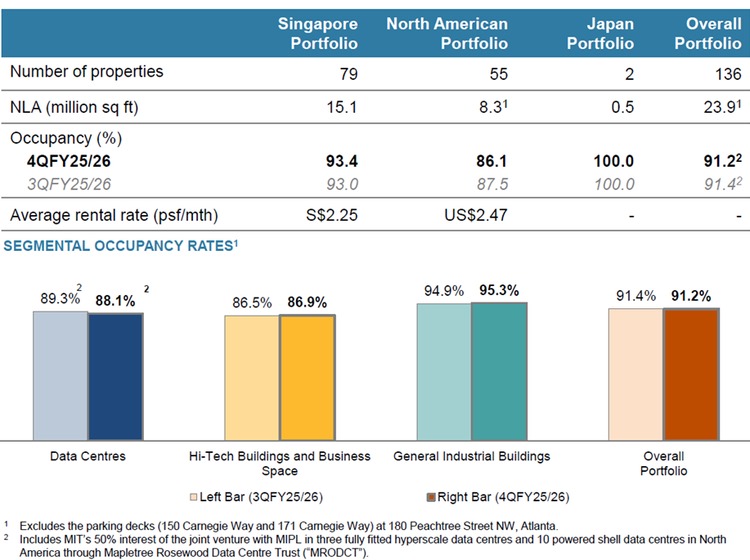

As at 31 March 2026, MIT had 136 properties, with assets under management of about S$8.3 billion. Data centres made up 57.3% of its AUM, while Singapore and North America each accounted for about 46% of data centre AUM.

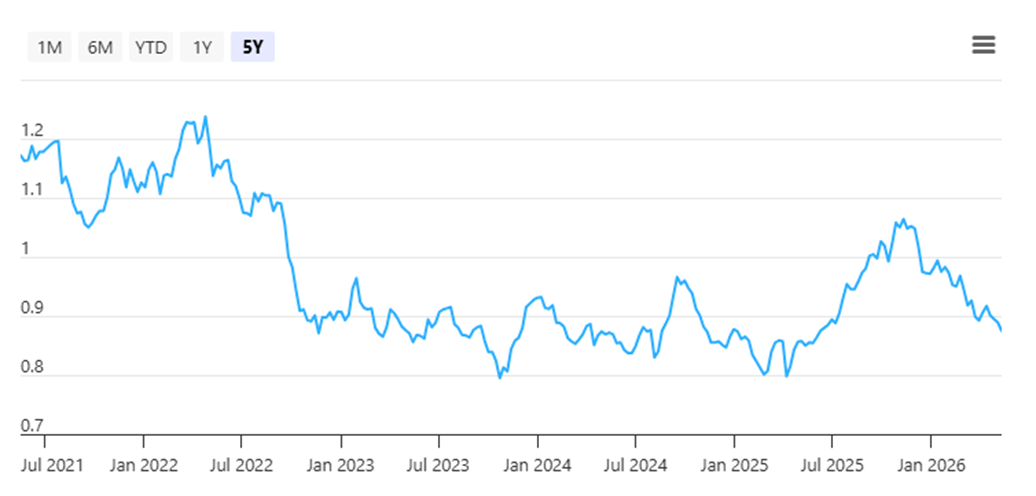

MIT’s share price is around S$1.94 as of 12 May 2026 and trading near the low end of its 5-year range.

MIT’s latest results help to explain why the share price has been under pressure.

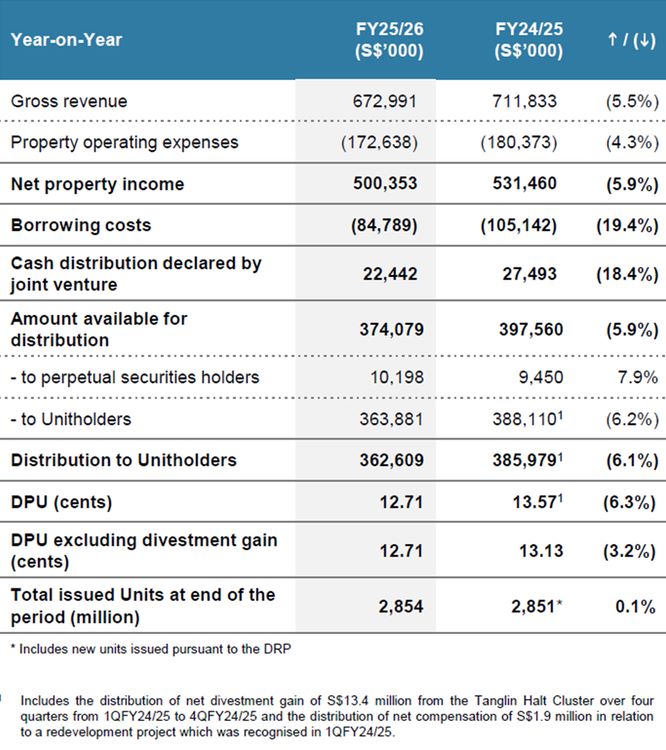

For FY25/26, DPU fell 6.3% year on year to 12.71 cents, while distribution to unitholders fell 6.1% to S$362.6 million. Gross revenue declined 5.5% to S$673.0 million, while net property income fell 5.9% to S$500.4 million.

The weaker performance was mainly due to the absence of income from divested Singapore properties, non-renewal of leases in the North American portfolio, and the depreciation of the US dollar against the Singapore dollar.

These headwinds were partly offset by higher contributions from the Japan portfolio, including the Osaka Data Centre, and new leases and renewals in Singapore.

There were still some encouraging operating signals.

Overall portfolio occupancy was 91.2% in 4Q FY25/26, slightly lower than 91.4% in the previous quarter. Singapore occupancy improved to 93.4% in 4QFY25/26, while Japan occupancy stayed at 100%. However, North American occupancy fell to 86.1%, and this remains the main drag on the portfolio.

MIT has been trying to manage this through active leasing and portfolio rebalancing.

It executed about 400,000 sq ft of leases in North America in FY25/26, including a 13-year lease to backfill vacant space at 2055 East Technology Circle in Tempe. It also renewed or leased 65% of North American lease expiries from FY23/24 to FY25/26.

Its balance sheet remains relatively strong.

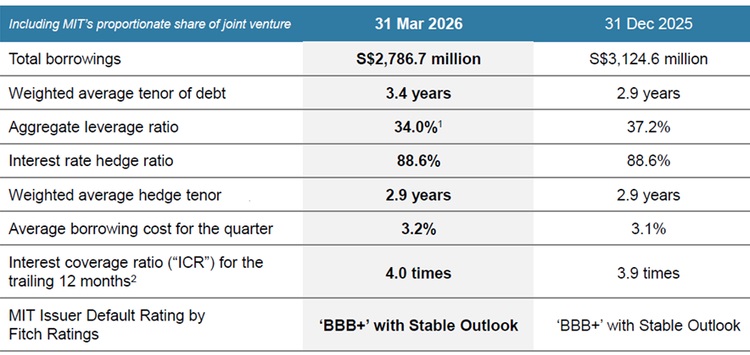

Aggregate leverage stood at 34.0% as at 31 March 2026, though it is expected to rise to about 37.5% after the drawdown of debt and redeployment of perpetual securities.

MIT also issued S$300 million of 3.25% perpetual securities ahead of the redemption of existing perpetual securities in May 2026.

For FY25/26, Mapletree Industrial Trust reported DPU of 12.71 Singapore cents, down from 13.57 cents in FY24/25. Excluding divestment gains, DPU would have declined by a smaller 3.2%.

Based on its unit price of S$1.94 as of 12 May 2026, MIT offers a forward dividend yield of 6.7% and a Trailing Twelve Months (TTM) dividend yield of 6.6%.

MIT still offers useful exposure to industrial assets and data centres, but I would watch whether North American lease non-renewals and higher replacement hedging costs continue to weigh on DPU.

Meanwhile, MIT aims to continue to pursue divestment programme in North America. MIT has identified S$500 million to S$600 million of assets to divest in the next one to two years. Besides enhancing financial flexibility, MIT aims to redeploy capital into new markets and high quality assets. Specifically, MIT is exploring entry into data centres in Japan and Europe.

Find out how much dividends you would have received as a unitholder of Mapletree Industrial Trust in the past 12 months with the calculator below.

Related links:

- Mapletree Industrial Trust latest valuation, share price and analysis

- Mapletree Industrial Trust dividend history and dividend forecasts

#3 – Keppel REIT (SGX: K71U)

Keppel REIT owns premium commercial assets across Singapore, Australia, South Korea and Japan. Its portfolio includes Ocean Financial Centre, Marina Bay Financial Centre, One Raffles Quay and Keppel Bay Tower in Singapore, as well as office and retail assets overseas.

Keppel REIT’s share price was around S$0.87 as of 12 May 2026, and share price is trading near the low end of its 5-year range.

Compared with the other two REITs, Keppel REIT’s latest operating update looks stronger.

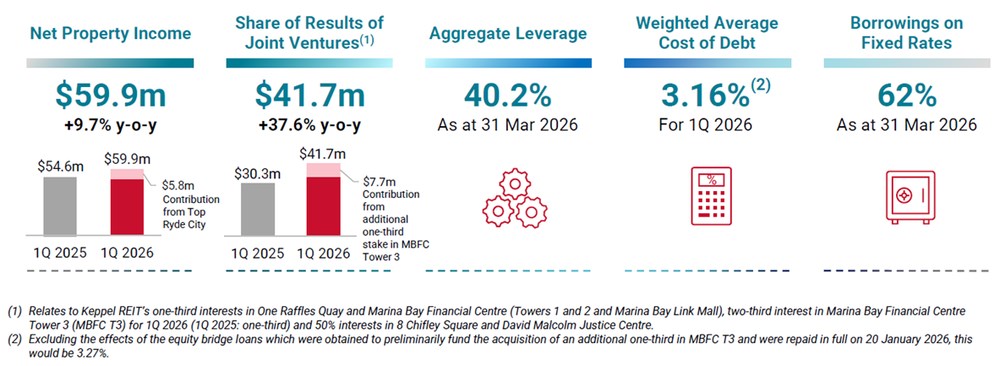

In 1Q 2026, property income rose 14.4% year on year to S$78.6 million, while NPI increased 9.7% to S$59.9 million. Distributable income including anniversary distribution rose 17.8% to S$62.9 million.

The improvement was mainly driven by contributions from Top Ryde City Shopping Centre, higher occupancy at Ocean Financial Centre, and the additional one-third interest in Marina Bay Financial Centre Tower 3.

Share of results of joint ventures rose 37.6% year on year, helped by the additional MBFC Tower 3 stake, higher rentals and lower borrowing costs.

The operational numbers were also healthy.

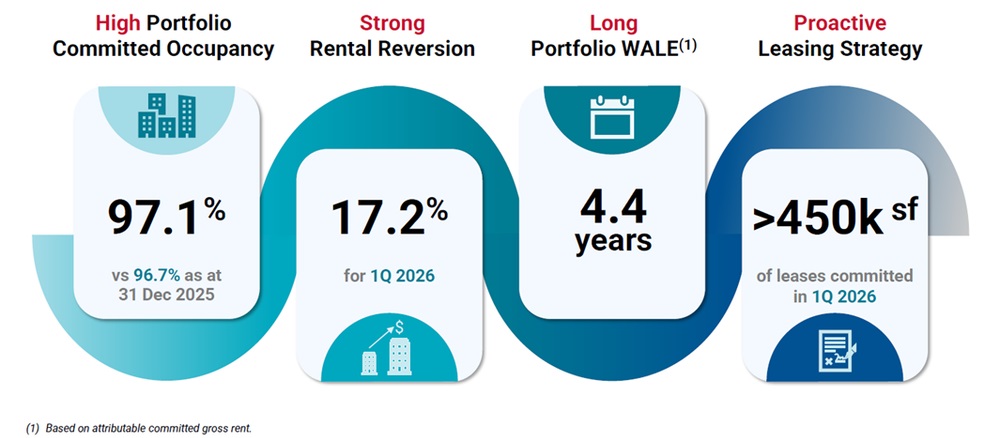

Portfolio committed occupancy improved to 97.1% as at 31 March 2026, from 96.7% at end-2025.

Keppel REIT also achieved a strong rental reversion of 17.2% in 1Q 2026, with more than 450,000 sq ft of leases committed during the quarter. New leasing demand and expansions were mainly driven by the banking, insurance and financial services sector.

Its Singapore office portfolio remains a key contributor.

Keppel REIT noted that Core CBD Grade A office rents rose to S$12.40 psf per month in 1Q 2026, while occupancy in the CBD Core Grade A market increased to 96.7%. This provides some support for its Singapore office assets, especially as average signing rents for Singapore office leases concluded in 1Q 2026 were above the average rent of leases expiring in 2026 and 2027.

That said, leverage and interest coverage still need to be monitored.

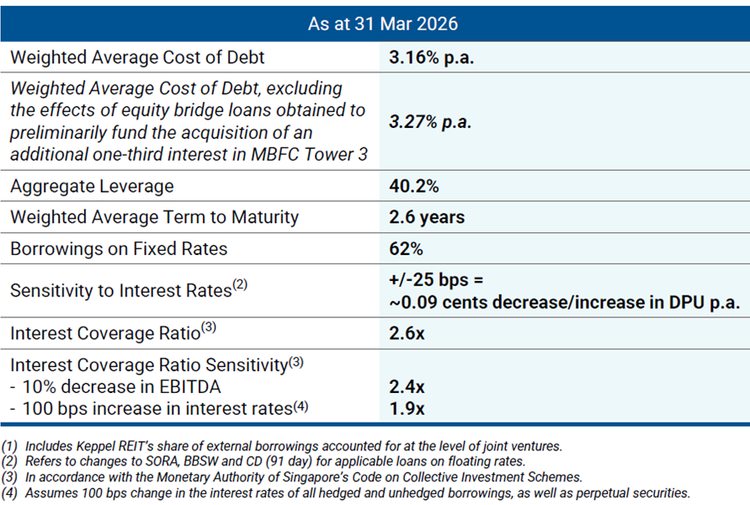

Keppel REIT’s aggregate leverage stood at 40.2% as at 31 March 2026, with a weighted average cost of debt of 3.16% and interest coverage ratio of 2.6 times. About 62% of its borrowings were on fixed rates.

For FY2025, Keppel REIT reported DPU of 5.23 Singapore cents, down from 5.60 cents in FY2024.

Based on its unit price of S$0.87 as of 12 May 2026, Keppel REIT offers a forward dividend yield of 5.7% and a Trailing Twelve Months (TTM) dividend yield of 6.0%.

Keppel REIT’s latest operating performance has been resilient despite its lower share price, but I would watch whether office demand, leverage and interest coverage remain supportive of stable distributions.

Find out how much dividends you would have received as a unitholder of Keppel REIT in the past 12 months with the calculator below.

Related links:

What would Beansprout do?

I think these blue-chip REITs are worth considering for investors building a long-term income portfolio, but I would build positions selectively and gradually rather than buy them simply because they are trading near 5-year lows.

All three REITs offer more attractive yields after the decline in share prices, but I would not look at the lower prices or higher yields in isolation.

If I were looking for a more diversified blue-chip REIT, I would start with CapitaLand Ascendas REIT. Its portfolio spans business space, logistics, industrial properties and data centres, while its recent acquisitions could support future DPU growth. However, I would still watch whether occupancy stabilises and whether the enlarged unit base from its equity fundraising affects DPU growth. Learn more about CapitaLand Ascendas REIT here.

Mapletree Industrial Trust would stand out to me if I wanted exposure to industrial assets and data centres, while still having a relatively healthy balance sheet. However, its latest DPU declined, and the North American portfolio remains a key drag, so I would want to see clearer signs of leasing stability before building a larger position. Learn more about Mapletree Industrial Trust here.

Keppel REIT had the strongest latest operating update among the three, with high occupancy and strong rental reversion. But as an office-focused REIT with gearing above 40%, I would be more selective and watch whether leasing demand and refinancing costs remain manageable. Learn more about Keppel REIT here.

Overall, I may consider building exposure gradually rather than all at once, while comparing each REIT’s dividend yield against its DPU trend, occupancy, gearing and interest coverage.

One final point I would keep in mind is that REIT yields may change quickly when borrowing costs rise or when capital raisings dilute distributions.

Because of that, I will still consider how I can build a diversified income portfolio beyond Singapore REITs to grow my income. Learn how to build a more dependable stream of passive income that can hold up across cycles here.

| REIT | The good | Key risks |

| CapitaLand Ascendas REIT | ● About S$1.6 billion of DPU-accretive acquisitions announced or completed in 1Q 2026 ● Positive portfolio rental reversion of 10.6% ● Gearing expected to improve to about 37.3% after equity fundraising | ● Portfolio occupancy dipped to 90.5% ● Aggregate leverage rose to 42.0% before the equity fundraising ● Execution risk from acquisitions and enlarged unit base |

| Mapletree Industrial Trust | ● Singapore portfolio occupancy improved to 93.4% ● Positive Singapore rental reversion of about 6.2% ● Aggregate leverage stood at 34.0%, giving it balance sheet flexibility | ● FY25/26 DPU fell 6.3% year on year ● North American lease non-renewals remain a drag ● Higher borrowing cost from repricing of maturing interest rate swaps may weigh on distributions |

| Keppel REIT | ● 1Q 2026 NPI rose 9.7% year on year ● Portfolio committed occupancy improved to 97.1% ● Strong rental reversion of 17.2% in 1Q 2026 | ● Aggregate leverage stood at 40.2% ● Interest coverage ratio of 2.6x leaves less room if rates rise ● Office-focused exposure means DPU depends on leasing demand and refinancing costs |

To screen for Singapore REITs with lowest price-to-book valuation or highest dividend yield, check out our best Singapore REIT screener.

If you prefer diversification without picking individual REITs, you can also gain exposure through Singapore REIT ETFs.

If you are new to investing in Singapore REITs, you can start to learn more about Singapore REITs here.

Is there a Singapore REIT you are looking out for? Share with us in the comments below or in our Telegram group!

Planning to invest in Singapore REITs? Compare the best Singapore brokerages to find the right trading platform, and see the latest promotions and sign-up rewards available.

Follow Beansprout on Telegram, Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments