DBS and Mapletree Industrial Trust in focus: Weekly Review with SIAS

Stocks

Powered by

By Gerald Wong, CFA • 04 May 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

We look at DBS, Mapletree Industrial Trust and the key developments shaping the Singapore stock market in the latest Weekly Market Review.

What happened?

In this week's Weekly Market Review in partnership with Securities Investors Association Singapore (SIAS), we discuss the fresh all-time highs in US markets, the impact of stronger bank earnings in Singapore, and the latest updates on DBS and Mapletree Industrial Trust.

Watch the video to learn more about what we are looking out for this week.

Weekly Market Review

1:16 - Macro Update

- US markets continued to rally last week, with the S&P 500 rising 1.0% to a new high of 7,230, while the NASDAQ gained 1.1% and also reached a fresh all-time high, supported by strong earnings from major technology companies.

- The rally in US equities was driven mainly by upbeat results from names such as Alphabet, which helped offset concerns about geopolitical tensions and interest rates.

- Oil prices painted a less positive picture, rising to the highest level since 2020 as there was still no resolution to the Middle East conflict.

- The Federal Reserve kept interest rates unchanged, as expected, but comments from officials suggested that support for rate cuts is fading, which pushed the US 10-year bond yield back towards 4.4%.

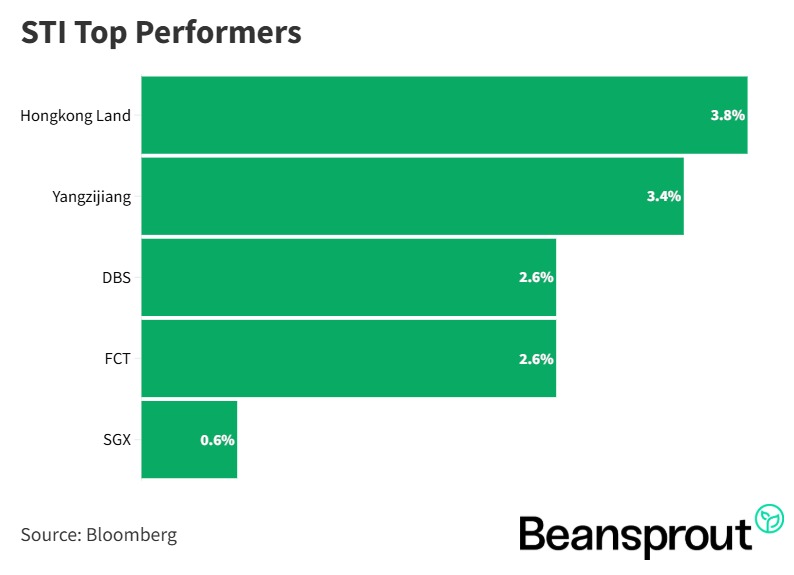

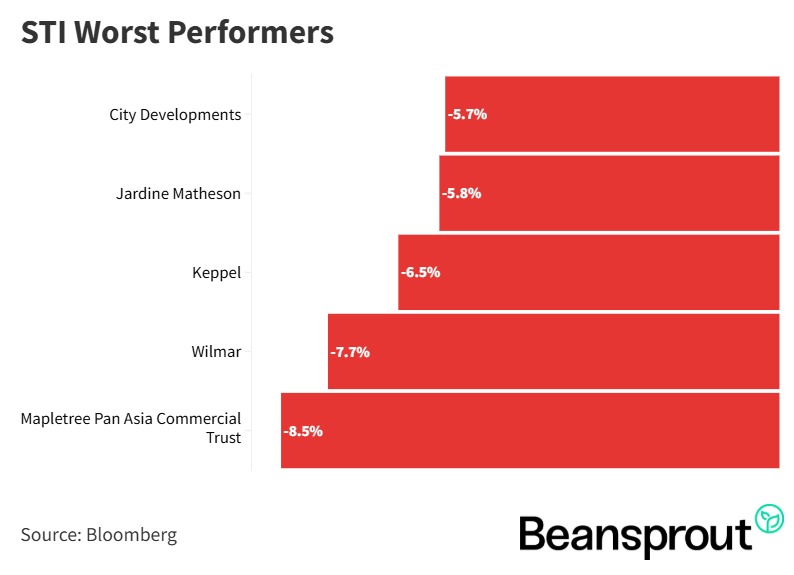

- In Singapore, DBS was one of the top STI performers, rising 2.6% after reporting record quarterly profit, while Wilmar and Keppel were among the weaker names after their recent results.

- Investors are watching a busy week ahead, with UOB and OCBC earnings due, alongside the latest US non-farm payroll data.

STI Top Performers:

STI Worst Performers:

Companies in Focus:

DBS (SGX: D05)

- DBS’ share price has recovered to around S$58.50, representing a strong rebound from the weakness seen during the Middle East conflict in March.

- The bank reported a strong set of first-quarter results, with total income rising 1% year on year to S$5.9 billion, while profit before tax increased 2% year on year to a record S$3.5 billion.

- While net interest margin slipped slightly to 1.89% from 1.93% in the previous quarter, this was largely expected given the decline in benchmark interest rates in Singapore.

- A key driver of earnings was stronger fee income, particularly from wealth management. First-quarter wealth management fee income rose to a record S$907 million, up nearly 20% from S$724 million a year earlier.

- With the strong results, DBS declared a first-quarter total dividend of 81 cents per share, made up of 66 cents ordinary dividend and 15 cents capital return dividend.

- Management also maintained its full-year 2026 guidance, suggesting that the bank believes it has started the year on a firm footing despite global uncertainties.

- At current levels, DBS is trading above its historical average on both price-to-book and price-to-earnings measures, although its annualised dividend still implies a yield of close to 5.5% based on the current share price.

Related Links:

- DBS (SGX: D05) latest valuation, share price and analysis

- DBS (SGX: D05) dividend history and dividend forecast

- DBS profit rises 1% and declares S$0.81 in total dividends in 1Q26: Our Quick Take

Mapletree Industrial Trust (SGX: ME8U)

- Mapletree Industrial Trust has seen its share price come under pressure, and its latest results help explain some of the weakness.

- For the fourth quarter of FY2025/26 ended March 2026, DPU fell 8% year on year to 3.09 cents, down from 3.36 cents in the previous year.

- Part of the decline was due to the absence of divestment gains that had boosted distributions a year earlier. Excluding those gains, DPU would have been 3.25 cents, representing a smaller 4.9% decline.

- The weaker result was also driven by lower contributions from the North America portfolio following lease non-renewals, as well as the weaker US dollar and Japanese yen against the Singapore dollar.

- These pressures were partly offset by higher contribution from the Singapore portfolio and the completion of final fitting-out works at the Osaka data centre.

- Portfolio occupancy in Singapore improved slightly to 93.4%, but North America occupancy fell further to 86.1%, pulling overall portfolio occupancy down to 91.2%.

- On a more positive note, Singapore rental reversions remained healthy, with portfolio weighted average rental reversion at 6.2%.

- MIT’s balance sheet remains fairly sound, with aggregate leverage declining to 34% after asset divestments, though average borrowing cost edged up slightly to 3.2% from 3.1% in the previous quarter.

- At current levels, MIT is trading at around 1.17 times price to book, below its historical average of about 1.3 times, while offering a dividend yield of above 6%, although investors remain cautious given the recent decline in DPU.

Related Links:

- Mapletree Industrial Trust (SGX: ME8U) latest valuation, share price and analysis

- Mapletree Industrial Trust (SGX: ME8U) dividend history and dividend forecast

Technical Analysis

Straits Times Index

- The STI is attempting to stabilise around the 4,900 pivot level, with the index up about 0.6% on Monday morning to 4,942.

- Immediate support is around 4,800, referencing the 20 January low of 4,790, while 5,000 remains the key near-term resistance level and 5,041 is still the year-to-date high to watch.

- Momentum indicators are fairly neutral. The relative strength index (RSI) is at around 50, suggesting there is not much strong momentum in either direction.

- The moving average convergence divergence (MACD) remains negative, but the downside reading has started to ease. If the MACD line crosses back above the signal line, it could point to another rebound towards the year-to-date high.

- For now, the STI appears to be holding around the 4,900 range, with support at 4,800 likely to remain important in the near term.

Learn more about the Straits Times Index (STI) here.

Dow Jones Industrial Average

- The Dow Jones underperformed the other major US indices last Friday, slipping about 150 points and ending near 49,499.

- Immediate support is around 48,431, while the index is currently hovering near the 49,500 level. The next major upside level appears to be the year-to-date high at around 50,500.

- The RSI is at around 62, which still points to healthy upward momentum, although it is not as strong as before.

- The MACD remains positive, but momentum has started to moderate as the MACD line converges towards the signal line. A bearish crossover could suggest a near-term technical pullback.

- For now, the Dow still looks constructive, but some consolidation may emerge after its recent run-up.

S&P 500

- The S&P 500 continued to climb last week and closed at a fresh all-time high, with resistance now shifting to the 7,300 psychological level.

- Support is seen around 7,002, which marks the previous breakout zone and is now likely to act as a floor if the index pulls back.

- The RSI has risen to around 71, suggesting that the index is now in overbought territory and may be approaching a near-term peak.

- The MACD remains positive, but the histogram has started to narrow and the MACD line is moving closer to the signal line, indicating that the pace of the uptrend is slowing.

- For now, the S&P 500 may still test 7,300, but the setup suggests that some short-term profit-taking or retracement could emerge soon.

Learn more about the S&P 500 index here.

Nasdaq Composite Index

- The Nasdaq remained the strongest major US index and reached a fresh all-time high of 25,223 last week, before closing at 25,114.

- The next major resistance level is around 26,000, while support is seen around 24,000 following the recent breakout.

- The RSI is at around 72, which is above the overbought threshold and suggests that the index may be due for a near-term technical pullback.

- The MACD is still positive, but the MACD line is beginning to converge towards the signal line, which points to slowing upside momentum after the strong rally over the past month.

- If a retracement takes place, the Nasdaq could retest the 24,000 level, which now looks like the nearest support zone.

What to look out for this week

Key dates

- Monday, 4 May: CapitaLand Investment Limited, ComfortDelGro Corporation Limited, Frasers Centrepoint Trust, Sheng Siong Group ex-dividend

- Tuesday, 5 May: Frasers Logistics & Commercial Trust earnings, UOL, Venture, Seatirum ex-dividend

- Wednesday, 6 May: Mapletree Industrial Trust, Sembcorp Industries, Yangzijiang Shipbuilding ex-dividend, Beansprout webinar: How I invest with clarity

- Thursday, 7 May: UOB earnings, SGX ex-dividend

- Friday, 8 May: OCBC Bank earnings, Mapletree Logistics Trust ex-dividend, US non-farm payroll data

Check out the full list of Singapore stocks, REITs and ETFs with upcoming dividend payments with our dividend calendar.

Follow Beansprout on Telegram, Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments