DBS and OCBC hit record highs. How wealth management could support bank dividends

Stocks

By Gerald Wong, CFA • 29 May 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

DBS, OCBC and UOB are earning more from wealth management. Here’s what Singapore’s wealth boom means for dividends of local banks.

What Happened?

Singapore bank stocks have done well in recent years.

DBS and OCBC's share prices have climbed to record highs as investors continued to favour the sector.

For much of this period, investors saw Singapore banks as beneficiaries of higher interest rates, which lifted net interest margins and earnings.

That tailwind is now starting to fade as benchmark interest rates decline. This could put pressure on net interest income, which has been a major driver of bank profits.

Yet the latest results of DBS, OCBC and UOB showed that earnings remained resilient, helped by stronger wealth management income across the three banks.

With Singapore becoming one of Asia’s key wealth hubs, more high-net-worth individuals, family offices and institutions are using the country as a base to manage their assets.

For the local banks, this creates another source of income beyond lending.

In this article, I look at how DBS, OCBC and UOB are growing their wealth management businesses, why this matters for bank earnings, and what investors should watch next as interest rates decline.

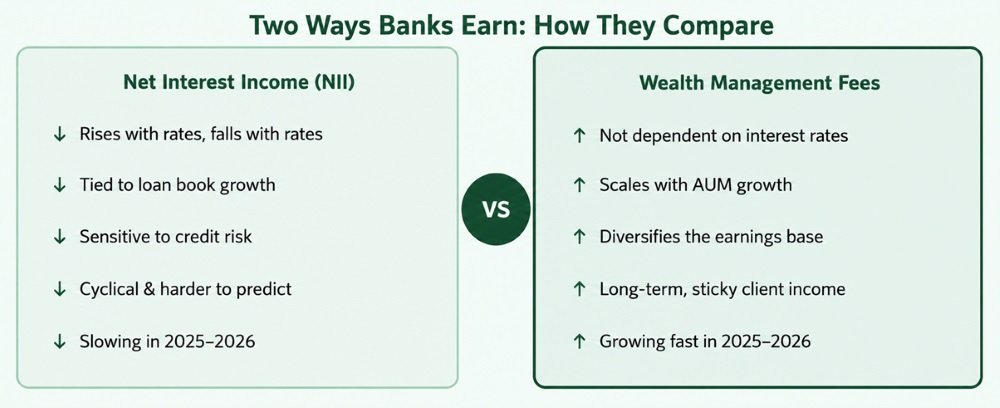

Why Singapore bank earnings are no longer just about interest rates

For much of the past three years, the investment case for Singapore bank stocks was straightforward: interest rates rose, banks earned more from lending, and profits climbed.

When interest rates rose, DBS, OCBC and UOB benefited.

Higher interest rates allowed banks to earn more from the difference between what they charged borrowers and what they paid depositors. This helped push earnings to record levels in recent years.

But the reverse can also happen.

When interest rates fall, net interest margins may narrow. This can put pressure on net interest income, which has traditionally been one of the biggest drivers of bank profits.

That is why falling rates would usually be a concern for investors in bank stocks.

In Q1 2026, this pressure started to show.

All three Singapore banks reported weaker net interest income as benchmark rates declined.

However, their overall earnings held up better than some investors may have expected.

One key reason was wealth management.

As more affluent individuals, family offices and institutions manage their assets through Singapore, DBS, OCBC and UOB are earning more from fees linked to investment products, advisory services, insurance, asset management and brokerage activities.

This means Singapore bank stocks may no longer be viewed only through the lens of interest rates.

The banks are still affected by the rate cycle. But wealth management is becoming a more important earnings buffer as lending income comes under pressure.

The new profit engine behind DBS, OCBC and UOB

Singapore’s rise as a global wealth management centre has been years in the making.

According to the Monetary Authority of Singapore, total assets under management reached S$5.41 trillion at the end of 2023, up 10% from the year before.

The number of single-family offices has also grown sharply, rising more than fivefold since 2020 to exceed 2,000 by end-2024.

For DBS, OCBC and UOB, this creates a larger pool of potential clients.

A family office, high-net-worth individual or institution that manages money out of Singapore may use local banks for investment products, treasury solutions, loans, insurance, stockbroking or advisory services.

These activities generate fee income.

This is different from net interest income, which depends more directly on the interest-rate cycle.

When a bank lends money, its net interest income can rise or fall depending on rates, funding costs and loan demand.

But wealth management income can come from clients buying funds, investing through managed portfolios, purchasing insurance products, trading securities or seeking financial advice.

As assets under management grow, fee income can also grow.

This does not remove the impact of lower rates entirely. But it gives the banks another way to defend earnings when lending income weakens.

That is why the wealth management story matters.

Singapore’s wealth boom is no longer just a macro trend. It is already showing up in the results of DBS, OCBC and UOB.

DBS, OCBC and UOB wealth management business compared

All three Singapore banks are benefiting from the growth of wealth management. But they are positioned differently.

DBS has the largest wealth management franchise.

OCBC has the most diversified earnings mix, supported by private banking, insurance and asset management.

UOB has the clearest ASEAN growth angle.

Here is how the three banks compare.

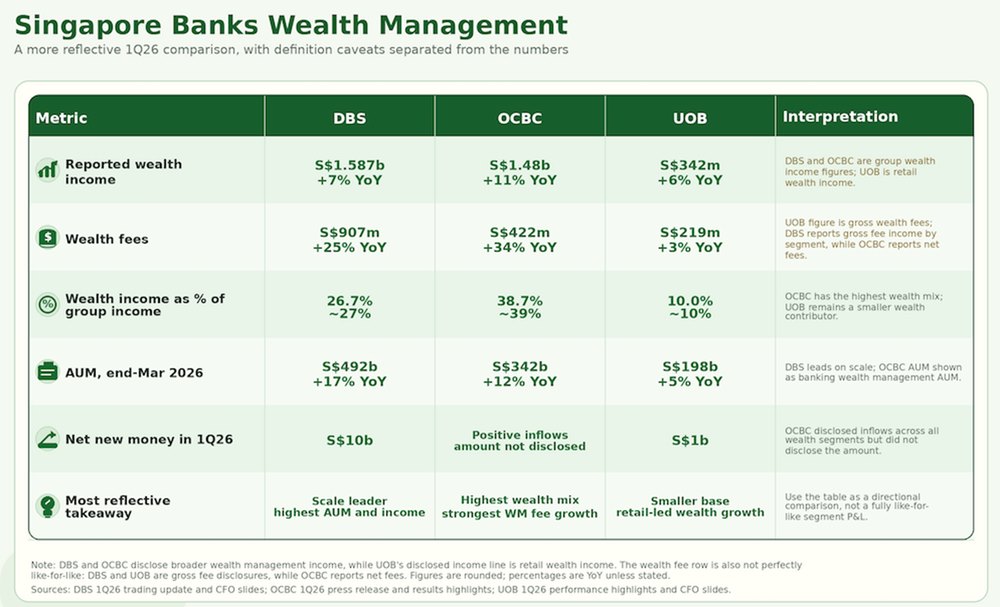

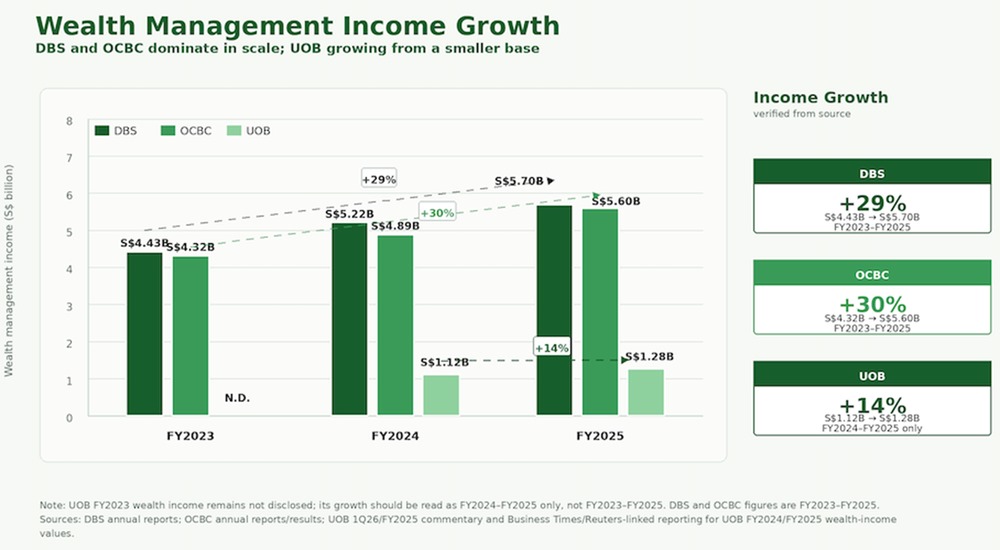

DBS (SGX: D05) - the undisputed scale leader

DBS has built the largest wealth management franchise among the Singapore banks.

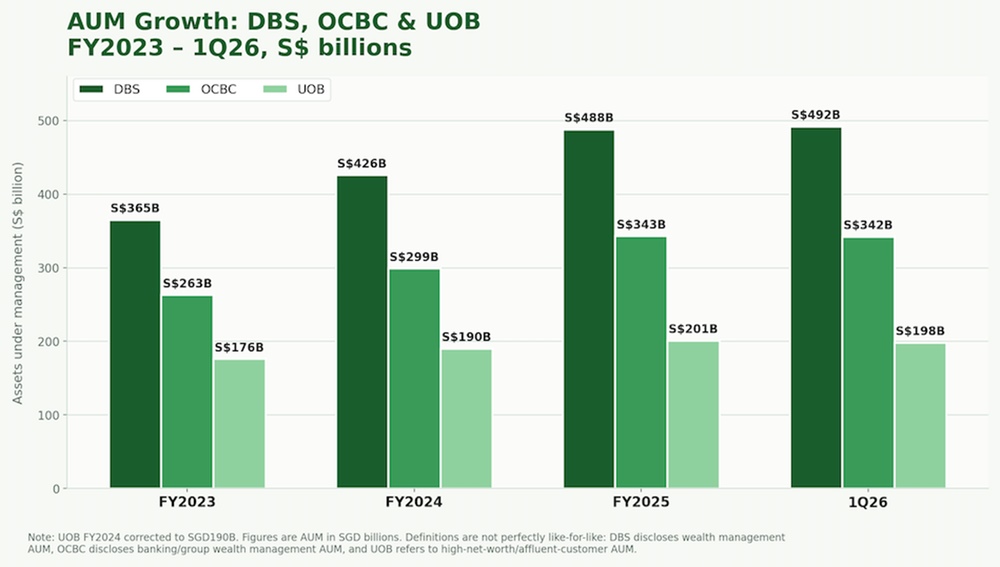

Its wealth management income rose from S$4.43 billion in FY2023 to a record S$5.70 billion in FY2025. This represents an increase of about 29% over two years.

Assets under management also grew from S$365 billion at end-FY2023 to S$488 billion at end-FY2025.

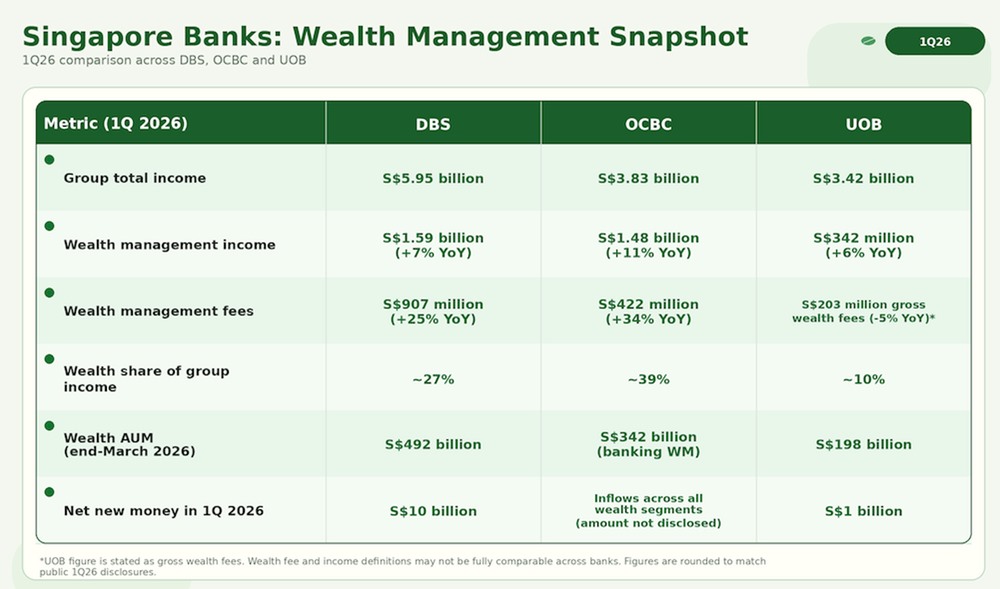

The momentum continued in 1Q 2026.

DBS reported record wealth management fees of S$907 million, up 25% year-on-year. Total wealth segment income reached S$1.59 billion, up 7% year-on-year.

Its AUM rose further to S$492 billion at end-March 2026, while the bank attracted S$10 billion of net new money during the quarter.

That run rate works out to roughly S$10 million in wealth management fees every day in 1Q 2026.

As interest rates decline and net interest income comes under pressure, DBS’ growing wealth franchise is helping to diversify its earnings base.

OCBC (SGX: O39) - the most transformed earnings mix

If DBS leads in scale, OCBC stands out for how much wealth management has reshaped its earnings mix.

OCBC defines wealth management income to include private banking, premier private client, premier banking, insurance, asset management and stockbroking.

This means its wealth business is not just about private banking.

It also includes Bank of Singapore, Great Eastern and its asset management capabilities.

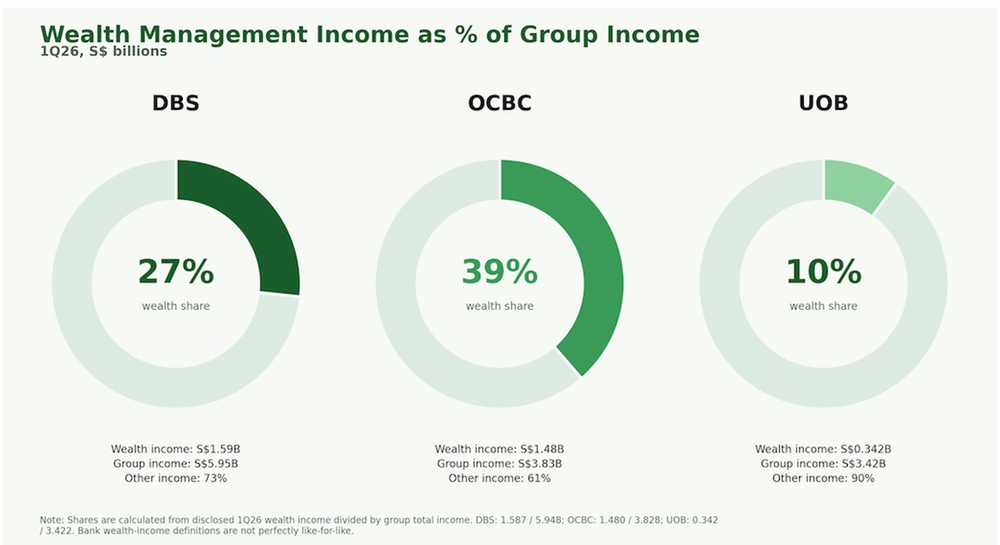

In Q1 2026, wealth management contributed about 39% of OCBC’s total group income, up from 37% a year earlier.

That makes OCBC less dependent on the interest rate cycle than before.

Its wealth management income reached a record S$5.60 billion in FY2025, up about 30% from S$4.32 billion in FY2023.

The momentum continued in Q1 2026.

Wealth management income rose 11% year-on-year to S$1.48 billion. Wealth management fees grew even faster, jumping 34% year-on-year to S$422 million.

Banking wealth AUM reached S$342 billion, up 12% year-on-year.

OCBC also noted that net new money inflows continued across all wealth segments.

For investors, OCBC’s wealth franchise is becoming an increasingly important earnings buffer.

The key attraction is not just the size of its wealth business, but how deeply it is now embedded across the group.

UOB (SGX: U11) - the regional growth bet

UOB has the smallest wealth management franchise among the three local banks, but it is growing steadily.

High-net-worth AUM rose from S$176 billion in FY2023 to S$190 billion in FY2024 and S$201 billion in FY2025.

It eased slightly to S$198 billion at end-March 2026 on a quarter-on-quarter basis, but was still up 5% year-on-year.

Group wealth management fees increased from S$698 million in FY2024 to S$822 million in FY2025, an increase of about 18%.

Total wealth income reached S$1.28 billion in FY2025, up about 14% from FY2024.

In Q1 2026, UOB’s Group Retail wealth income grew 6% year-on-year to S$342 million. This was supported by AUM expansion and conversion into investments.

Net new money totalled S$1 billion during the quarter.

Management has also set an ambitious target to roughly double wealth income by 2030, to at least about S$2.5 billion.

UOB’s key advantage is its ASEAN footprint, spanning markets such as Thailand, Malaysia, Indonesia and Vietnam.

This gives the bank exposure to rising wealth across Southeast Asia, where affluent individuals and business owners may increasingly seek trusted regional banking partners.

What wealth management growth means for Singapore bank investors

The 1Q 2026 results tell a consistent story across all three Singapore banks: wealth management is becoming a more important earnings buffer as interest rates fall.

DBS delivered record wealth management fees of S$907 million and attracted S$10 billion of net new money.

OCBC grew wealth management income by 11% year-on-year, with wealth management fees rising 34%.

UOB’s Group Retail wealth income grew 6% year-on-year despite softer market conditions, with S$1 billion in net new money during the quarter.

Importantly, all three banks reported wealth AUM growth and at least some net new money activity (with DBS and UOB disclosing explicit NNM figures and OCBC describing inflows across all segments). This suggests clients are actively moving assets onto these platforms, rather than the banks simply benefiting from market movements on existing assets.

For investors, this changes how we think about Singapore bank stocks.

The old framework was simple: when interest rates rise, banks benefit; when rates fall, net interest income comes under pressure.

That framework is now incomplete.

As wealth management grows, DBS, OCBC and UOB are becoming less dependent on interest income alone.

Wealth management provides recurring fee income that can compound as AUM grows, without requiring the banks to take on more lending risk.

It is also supported by a structural tailwind, as Singapore continues to attract high-net-worth individuals, family offices and institutional capital.

Q1 2026 showed why this matters. Net interest income came under pressure, but profits remained resilient because wealth-related income continued to grow.

For long-term investors, the key question is no longer just where interest rates are headed.

It is also how much wealth will continue flowing into Singapore, and which bank is best positioned to capture it.

DBS remains the scale leader, OCBC has the most transformed earnings mix, and UOB offers the clearest ASEAN wealth growth angle.

Singapore banks Q1 2026 at a glance

What Would Beansprout Do?

Singapore’s wealth boom is no longer just a macro story. It is already showing up in bank earnings, and is becoming a key reason for long-term investors to stay constructive on Singapore banks.

For investors, this means Singapore banks should not be viewed only through the lens of interest rates. In a lower-rate world, the banks that grow fee income fastest may be better positioned to defend earnings.

DBS remains the anchor for scale and income visibility, with the largest wealth franchise and record wealth management fees helping to offset net interest income pressure. Management has guided to a wealth management AUM of around S$500 billion in 2026.

OCBC stands out for earnings diversification, with wealth-related income now making up about 39% of total group income in 1Q 2026 across private banking, insurance and asset management. Management has said it aims to roughly double the wealth business by 2029, accelerated from the earlier 2030 target.

UOB offers the longer-term ASEAN growth angle, with management targeting to roughly double wealth income by 2030 to at least about S$2.5 billion.

That said, valuations still matter. After the strong share price performance, investors should avoid chasing the banks purely for recent momentum.

DBS currently trades at a price-to-book ratio of 2.6x, OCBC trades at a price-to-book ratio of 1.8x, and UOB trades at a price=to-book ratio of 1.3x, all above their historical averages.

DBS offers an annualised dividend yield of 5.2%, OCBC offers a historical dividend yield of 4.2%, while UOB offers a historical dividend yield of 4.8%.

Hence for income investors, DBS still offers a higher forward dividend yield, stronger franchise quality and market leadership.

If I am looking to diversify my portfolio beyond DBS by adding another Singapore bank, then I may consider OCBC through its exposure to banking, wealth management and insurance in one name, albeit with a lower yield.

More broadly, this fits with our view that Singapore should remain a core part of a portfolio, supported by the market's relative resilience, dividend support, and safe haven appeal.

Beyond Singapore's rise as a wealth hub, there may also be other avenues to capture structural growth in the Singapore market, including companies linked to infrastructure, data centres, energy security and regional expansion. Explore four growth themes to watch in Singapore stocks here.

If you are looking for more Singapore stock ideas linked to long-term growth themes, you can explore our high-conviction curated stock opportunities here.

You can also screen for stocks that meet Beansprout’s 4-factor Opportunity framework here.

[Beansprout Exclusive Longbridge Promotion] Get bonus S$50 FairPrice voucher within 5 working days, plus 10% p.a. interest boost coupon (worth ~S$100) when you sign up for a Longbridge account via Beansprout. Plus, S$1,200 of CapitaVouchers to be won. Promo ends on 31 May 2026. T&Cs apply. Learn more about the Longbridge promotion here.

All three banks are also among the largest Singapore blue chip stocks, making them a natural starting point for investors looking to build exposure to Singapore's economy.

If you prefer broad exposure to all 3 banks and blue chips, you can learn more about the Straits Times Index (STI).

If you could only invest in one Singapore bank today, would you pick DBS, OCBC or UOB? Share your thoughts with us in the comments below or in our Telegram group!

Planning to invest in OCBC, UOB or DBS? Compare the best Singapore brokers to find the right trading platform, and see the latest promotions and sign-up rewards available.

Enjoyed this insight? Follow Beansprout on Telegram, Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments