SRS in Singapore: How to unlock tax savings with Supplementary Retirement Scheme

Retirement

By Beansprout • 05 Dec 2025

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

Learn how the Supplementary Retirement Scheme (SRS) in Singapore helps you unlock tax savings while growing your retirement funds. Understand the key benefits and investment options.

What happened?

With the end of 2025 fast approaching, many of us are likely looking for ways to save on taxes and hold onto more of our hard-earned money.

One of the most effective tools available is the Supplementary Retirement Scheme (SRS).

The Supplementary Retirement Scheme (SRS) allows us to grow our retirement nest egg and enjoy some tax savings along the way.

In this guide, I’ll break down everything you need to know about the SRS in Singapore.

We will cover how the SRS works, why it’s worth considering, and how to maximise its benefits.

To make it even easier, I've also included an SRS tax savings calculator to help you estimate how much you can save by contributing. Let's dive in!

What is the SRS and how does it work?

The Supplementary Retirement Scheme, or SRS, is a voluntary savings scheme that encourages you to save for retirement while reducing taxable income.

It is basically a complementary scheme to the Central Provident Fund (CPF) system open to Singaporeans, PRs, or foreigners residing in Singapore.

The voluntary contributions made to your SRS account are eligible for tax relief, and the funds within your SRS account can be invested in a wide range of financial instruments such as stocks, unit trusts, and exchange-traded funds (ETFs).

Here are some of the key features of the SRS:

- Contributions to SRS are eligible for tax relief

- You can invest using the funds in SRS in a wide range of instruments, including stocks, REITs, ETFs, and bonds.

- Investment returns are tax-free before withdrawal

- Only 50% of withdrawal sum from SRS is subject to tax at retirement

- The maximum withdrawal period is 10 years

How much tax savings can we get with SRS?

Let’s be honest - nobody enjoys paying taxes.

One way we can reduce our income tax bill is through SRS.

For Singaporeans and PRs, you can claim up to $15,300 in income tax relief when you contribute to your SRS account.

For foreigners, the yearly maximum SRS contribution is S$35,700.

The higher your income, the more income tax you will have to pay, and the more tax savings you can potentially enjoy by contributing to the SRS.

Let's look at an example based on the income tax rate for the Year of Assessment 2026 (YA 2026).

| Chargeable Income | Income Tax Rate (%) | Gross Tax Payable ($) |

| First $20,000 | 0 | 0 |

| Next $10,000 | 2 | 200 |

| First $30,000 | - | 200 |

| Next $10,000 | 3.5 | 350 |

| First $40,000 | - | 550 |

| Next $40,000 | 7 | 2,800 |

| First $80,000 | - | 3,350 |

| Next $40,000 | 11.5 | 4,600 |

| First $120,000 | - | 7,950 |

| Next $40,000 | 15 | 6,000 |

| First $160,000 | - | 13,950 |

| Next $40,000 | 18 | 7,200 |

| First $200,000 | - | 21,150 |

| Next $40,000 | 19 | 7,600 |

| First $240,000 | - | 28,750 |

| Next $40,000 | 19.5 | 7,800 |

| First $280,000 | - | 36,550 |

| Next $40,000 | 20 | 8,000 |

| First $320,000 | - | 44,550 |

| Next $180,000 | 22 | 39,600 |

| First $500,000 | - | 84,150 |

| Next $500,000 | 23 | 115,000 |

| First $1,000,000 | - | 199,150 |

| In excess of $1,000,000 | 24 | |

| Source: IRAS for YA2026 | ||

For example, if your chargeable income is S$40,000, you will need to pay an income tax of S$550.

If you were to contribute S$10,000 to your SRS, you will be able to enjoy a tax relief on the S$10,000 contribution, effectively lowering your tax bill by S$350.

However, if your chargeable income is S$320,000, you will need to pay an income tax of $44,550.

If you were to contribute S$10,000 to your SRS, you will be able to enjoy a tax relief on the S$10,000 contribution, effectively lowering your tax bill by $2,000.

The illustration above is based on the prevailing income tax for Singaporeans and Permanent Residents (PRs) for the year of assessment 2026 (YA 2026), and assumes $0 for current eligible tax relief.

Do note that the personal income tax relief cap of S$80,000 applies for each year, including relief on SRS contributions.

SRS Tax Savings Calculator

To calculate out how much you can save on your tax bill, check out our SRS tax savings calculator below.

The numbers may not look significant now but let’s put things into perspective. Assuming we work 30 years in our lifetime and contribute to SRS yearly, the tax savings will add up.

Why I would invest my SRS funds

Now before you start thinking that SRS is going to automatically grow your money for you, it isn’t.

Unlike your CPF ordinary account (OA) which offers an interest rate of 2.5% p.a., your SRS account only earns you 0.05% interest per annum.

Unfortunately, this means that the return is unlikely to be sufficient to help you combat inflation over the long term.

If you have $100,000 sitting in your SRS account for 20 years, this will just turn into a modest $101,004.76 at the end of the period.

Therefore, you can consider various options to earn a potentially higher return after you contribute to your SRS.

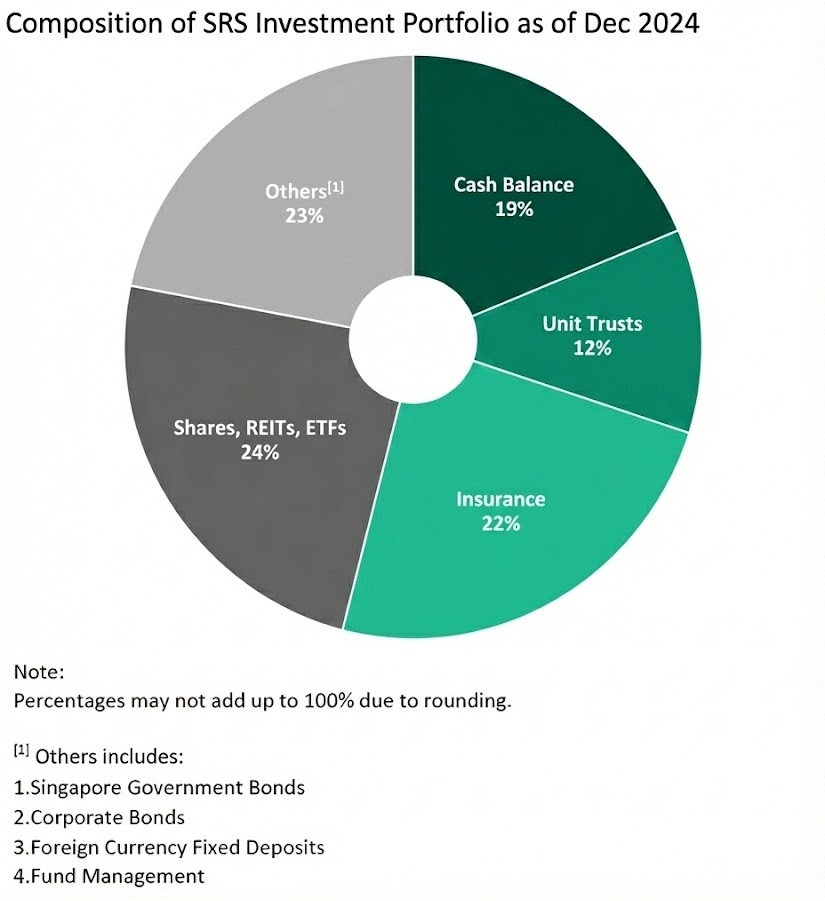

There are various investment options available for you to invest the money in your SRS account, including

- Shares, REITs and ETFs

- Endowment insurance plans

- Unit trusts

- Singapore Government Securities (bonds and T-bills)

Shares, REITs and ETFs are the most popular option amongst SRS investors, representing 24% of all investments as of December 2024.

Likewise, insurance also represents 22% of all investments as of December 2024.

Close to 19% of all SRS funds are kept as cash, earning a return of just 0.05% p.a.

Learn more about how to choose the best investment option for your SRS funds here.

How do I perform SRS withdrawals at withdrawal age without paying taxes?

When you withdraw on or after the retirement age from your SRS accounts, only 50% of the withdrawals are taxed.

Here’s an illustration on what this would mean for how much you would have to pay in taxes at withdrawal.

If you put aside $7,000 each year into SRS and use it for investment, after 30 years you will have about $408,000 in your SRS account assuming an average return of 4% per annum.

Based on the income tax rate for Year of Assessment (2026), the first $20,000 of your chargeable income is tax-free.

This would mean that we can withdraw up to $40,000 per year from our SRS account each year tax-free on or after our retirement age.

The maximum period over which you can spread your withdrawals is 10 years. The 10-year period will start from the date of your first such withdrawal.

This means that you can safely withdraw S$400,000 of your SRS funds tax-free over the maximum period of 10 years.

The amount in excess of $400,000 is still taxable. In this case, 50% of the remaining S$8,000 would be subject to the prevailing income tax rate.

Hence, the Ministry of Finance considers the SRS to be a tax deferral scheme. This is because up to $400,000 withdrawal is tax free based on current tax brackets but you are required to pay tax for your withdrawal amount beyond $400,000 at a lower tax bracket in the future.

The withdrawal amount that is subject to tax comprises your capital, dividend/interest/distribution and any capital gains, all of which are currently not taxable for individuals under non-SRS scheme.

However, you will not be worse off compared to if your SRS contributions were taxed upfront and all subsequent capital gains were exempt from tax.

What else I would consider before putting money into SRS

Note that SRS is ultimately meant for retirement. There are penalties if you were to withdraw before the retirement age.

Early withdrawals are fully subject to tax and will incur a 5% penalty.

While the current statutory retirement age stands at 63, it is scheduled to rise to 64 on 1 July 2026.

Of course, there will be no penalties if you withdraw on reasonable reasons such as medical grounds, terminal illness and bankruptcy.

Hence, you should make sure that the funds you are contributing towards your SRS are not needed for emergency use or near-term needs such as buying a property.

Withdrawals Subject to Penalty

- Early Withdrawals (Before Prescribed Retirement Age):

- Tax: 100% of the withdrawal sum is subject to tax.

- Penalty: Yes (5%).

Penalty-Free Withdrawals

- After the Prescribed Retirement Age:

- Tax: 50% of the withdrawal sum is subject to tax.

- Penalty: No.

- (Can be spread over 10 years).

- Medical Grounds (e.g., physical/mental incapacity or terminal illness):

- Tax: 50% of the withdrawal sum is subject to tax.

- Penalty: No.

- Full Withdrawal Due to Terminal Illness:

- Tax: 50% of the full withdrawal sum is subject to tax, with an exempt amount of up to $400,000.

- Penalty: No.

- Bankruptcy:

- Tax: 100% of the withdrawal sum is subject to tax.

- Penalty: No.

- Foreigners (After at Least 10 Years of Holding):

- Tax: 50% of the lump sum is subject to tax.

- Penalty: No.

Who is eligible for SRS?

You are eligible to sign up for an SRS account if you fulfill the following requirements:

- You are a Singaporean, Permanent Resident (PR) or foreigner;

- At least 18 years old and not an undischarged bankrupt

- Have no existing or pending SRS account or account application with any bank

- Can contribute varying amounts, subjected to a cap

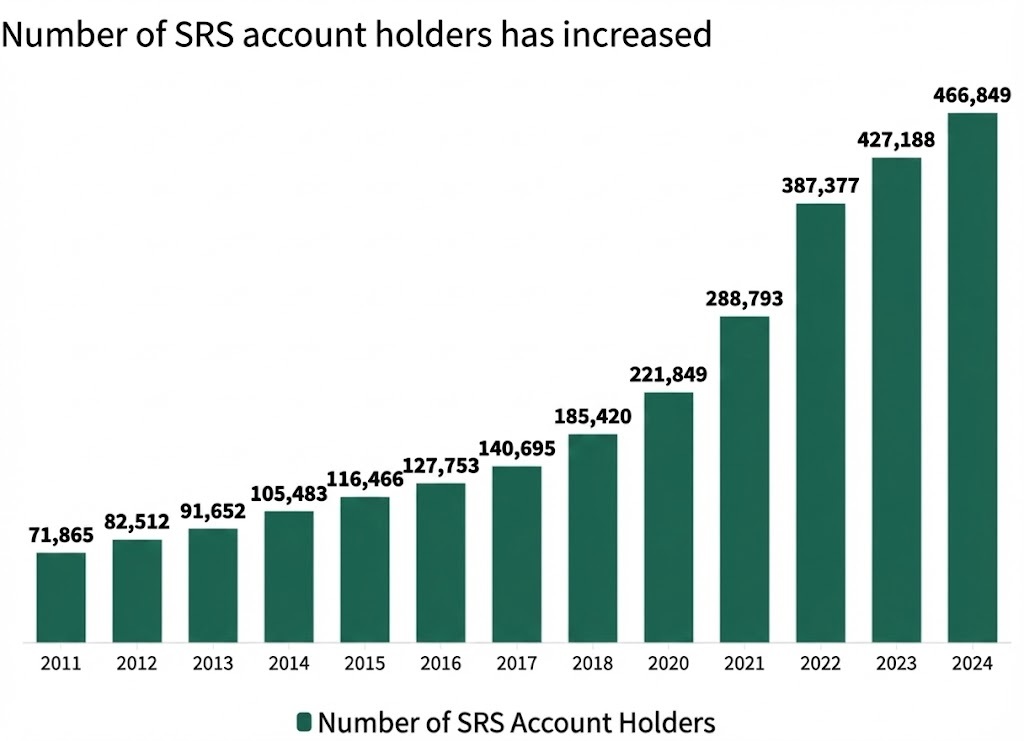

With the tax savings offered, it is not a surprise that more and more people are opting into the Supplementary Retirement Scheme (SRS).

There were 466,849 SRS account holders as of December 2024, an increase from less than 100,000 prior to 2013, according to figures from the Ministry of Finance (MOF).

How do I set up a SRS account?

You can apply for a SRS account with any of the three SRS operators – DBS/POSB, UOB and OCBC.

You will need the following documents to open a SRS account:

- Identity card/Passport

- Completed Declaration Form for SRS (For Foreigners)

How do I invest with my SRS funds?

Before you start investing using your SRS funds, you’ll need to satisfy the following criteria

- At least 18 years old,

- Not an undischarged bankrupt, and

- Not mentally disordered and therefore capable of managing yourself and your affairs.

Thereafter, you can invest your SRS funds with a few simple steps:

- Apply for a SRS account

- Link your SRS account and trading account

- Execute your trade

What would Beansprout do?

The Supplementary Retirement Scheme (SRS) is a great tool to consider if you are looking to save on taxes and grow your retirement fund.

By contributing up to $15,300 annually, you can lower your taxable income significantly, especially if you're in a higher tax bracket.

However, I would make sure that my SRS funds are invested for long-term growth, as cash sitting idle will only have an interest rate of 0.05% p.a. You can learn about the ways to invest your SRS to grow your retirement savings here.

I would also consider my need to access this pool of money in the short term, as early withdrawals come with a 5% penalty and full taxation.

For customers to be eligible for tax relief in 2026, contributions must be made by Wednesday, 31st December 2025.

If you are keen to start making use of SRS, do check out the list of ongoing promotions below.

Are there any ongoing promotions for SRS?

Tigers Brokers SRS Promotion: Receive ~S$20 worth of STI ETF shares (ES3.SI) when you link your SRS account and make your first trade. Learn more about Tiger Brokers’ SRS solutions here.

Syfe Promotion: Earn up to S$1,500 in fee credits when investing in SRS-eligible portfolios. Both new and existing users of Syfe are eligible for this promotion. Valid until 31 December 2025. Learn more about Syfe's SRS solutions here.

Endowus Promotion (New Users): Get S$100 in Endowus Fee Credits by investing at least S$1,000 (via Cash, CPF, or SRS). Valid until 31 December 2025. Learn more about Endowus' SRS solutions here.

Stashaway SRS Promotion (New Users): Get up to 12 months of management fee waivers and a +0.2% p.a. return booster on Simple Plus when you deposit fresh SRS funds. Learn more about Stashaway here.

OCBC SRS Promotion: Enjoy up to S$30 cash reward when you invest a minimum of S$15,000 of your SRS funds into eligible Unit Trusts via the OCBC app using the promo code “BYE25UT”. Valid until 31 December 2025. Learn more about OCBC 360 savings account here.

FSMOne Promotion: Receive up to S$200 worth of cash account credits when you invest SRS monies in Unit Trusts or ETFs. Valid from 1 Nov 2025 to 30 January 2026. Learn about FSMOne here.

Follow us on Telegram, Youtube, Facebook and Instagram to get the latest financial insights on growing your wealth.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments