SATS, DBS and OCBC in focus: Weekly Review with SIAS

Stocks

Powered by

By Gerald Wong, CFA • 02 Jun 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

We look at SATS and the Singapore Banks in the latest Weekly Market Review.

What happened?

In this week’s Weekly Market Review in partnership with the Securities Investors Association Singapore (SIAS), we discuss the continued rally in global markets as the S&P 500, NASDAQ and Dow Jones all reached fresh record highs amid easing oil prices and declining bond yields. We also look at the strong earnings performance of SATS, the growing contribution of wealth management to Singapore banks, and the technical outlook for the STI and major US indices.

Watch the video to learn more about what we are looking out for this week.

Weekly Market Review

1:23 - Macro Update

- US markets continued their rally last week, with the S&P 500 reaching a fresh record high of around 7,580 while the NASDAQ gained 2.4%, supported by continued optimism around AI-related technology stocks.

- Sentiment improved following progress towards a ceasefire between the US and Iran, raising hopes of a broader resolution to the Middle East conflict.

- Oil prices fell closer to the US$90 per barrel level as expectations grew that the Strait of Hormuz could reopen and supply disruptions would ease.

- Investors also became more optimistic about inflation, with US bond yields declining. The US 10-year Treasury yield fell to around 4.4% after reaching close to 4.7% earlier in the month.

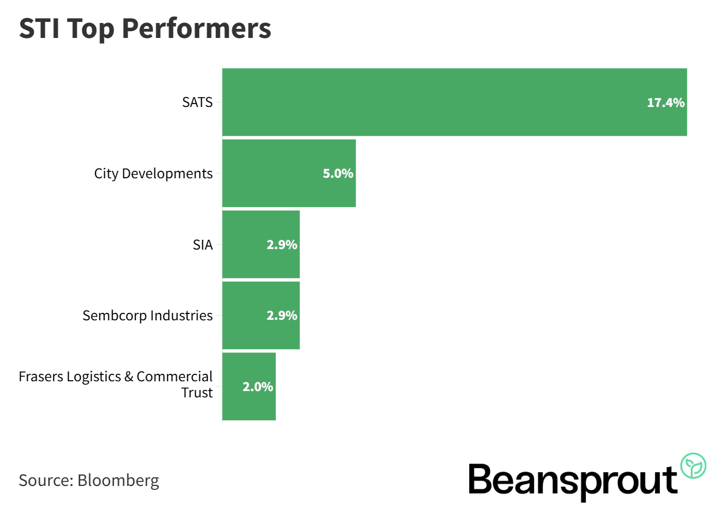

- In Singapore, market performance remained mixed, although selected stocks delivered strong gains. SATS rose 17.4% to become the top-performing STI constituent, while City Developments gained 5.0%.

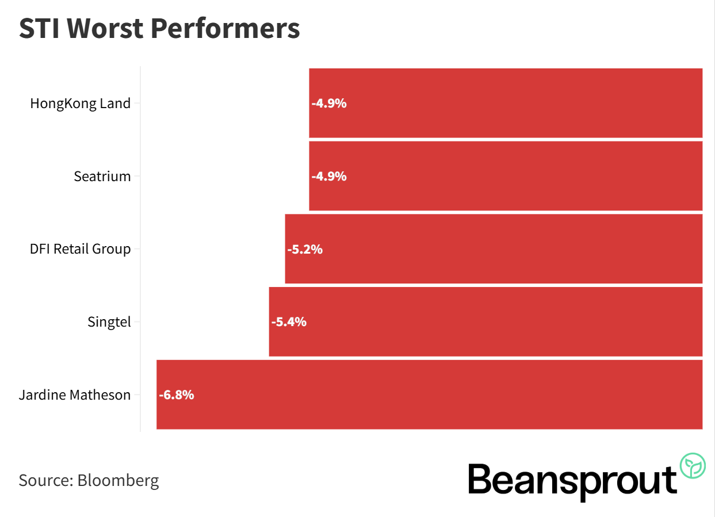

- On the weaker side, Jardine Matheson fell 6.8%, DFI Retail Group declined 5.2%, Hongkong Land lost 4.9%, while Singtel fell 5.4% following its latest earnings release.

STI Top Performers:

STI Worst Performers:

Companies in Focus:

SATS (SGX: S58)

- SATS reported record FY2026 revenue of S$6.35 billion, up 9% year on year, supported by continued strength across both its Gateway Services and Food Solutions segments.

- Fourth-quarter revenue rose 9.8% year on year to S$1.62 billion, while net profit jumped 31% to S$50.7 million. The company also proposed a final dividend of 5 cents per share, up 43% from 3.5 cents a year earlier.

- SATS’ cargo business continued to outperform industry benchmarks for the tenth consecutive quarter, with cargo tonnage increasing 7% year on year to 9.7 million tonnes.

- Operational metrics remained healthy across the group, with flights handled rising 3.2%, aviation meals served increasing 4.1%, and non-aviation meals growing 2.1%.

- Despite disruptions from the Middle East conflict, management highlighted opportunities from cargo rerouting and expects a post-conflict recovery to support regional trade volumes and air cargo demand.

- SATS also continues progressing towards its FY2029 targets, with EBITDA margin improving to 18.1% and profit-after-tax margin reaching 4.5%.

Related Links:

- SATS (SGX:S58) latest valuation, share price and analysis

- SATS (SGX:S58) dividend history and dividend forecast

DBS (SGX: D05)

- DBS has continued to outperform the STI in 2026, with the share price reaching fresh all-time highs as investors increasingly focus on the bank’s wealth management franchise.

- While net interest income remains under pressure from lower interest rates, DBS has benefited from strong growth in wealth management fees and rising assets under management.

- The bank recorded close to S$10 billion in net new money inflows during the first quarter of 2026, supporting continued growth in fee income.

- Wealth management income now accounts for approximately 27% of group income, highlighting the increasing importance of non-interest income as a growth driver.

Read also: DBS and OCBC hit record highs. How wealth management could support bank dividends

Related Links:

- DBS (SGX:D05) latest valuation, share price and analysis

- DBS (SGX:D05) dividend history and dividend forecast

OCBC (SGX: O39)

- OCBC has been the best-performing Singapore bank in 2026, with the stock gaining approximately 18% year to date and reaching fresh record highs.

- A key driver of its performance has been the strong growth in wealth management income, which increased 11% year on year in the first quarter of 2026.

- Wealth-related income now contributes about 39% of group income, making OCBC the most wealth-management-oriented among the three Singapore banks.

- Rising assets under management and continued net inflows have helped offset pressure on net interest margins from lower interest rates.

- Despite its strong share price performance, OCBC is trading at around 14 times earnings, which remains broadly in line with UOB and below DBS.

Read also: DBS and OCBC hit record highs. How wealth management could support bank dividends

Related Links:

- OCBC (SGX:O39) latest valuation, share price and analysis

- OCBC (SGX:O39) dividend history and dividend forecast

Technical Analysis

Straits Times Index

- The STI remains firmly above the 5,000 psychological level and is trading near its all-time high after reaching 5,102 points last week.

- Immediate resistance is around 5,100, while support is seen near 5,041 to 5,050, corresponding to the previous breakout level. Stronger support remains around 4,920.

- The RSI is hovering around 59 to 60, suggesting that the STI remains in a healthy uptrend without entering overbought territory.

- The MACD remains slightly positive, indicating that upward momentum is still intact and that the STI could retest the 5,100 level in the near term.

Learn more about the Straits Times Index (STI) here.

Dow Jones Industrial Average

- The Dow Jones reached a fresh all-time high above 51,100, continuing its recovery from the earlier Middle East-related market selloff.

- Immediate resistance is around 51,500, while support is seen near the previous high of 50,512.

- The RSI has risen to around 68, approaching overbought territory and suggesting that the rally may be becoming stretched.

- While the longer-term trend remains positive, the Dow may enter a period of consolidation as investors wait for new catalysts.

S&P 500

- The S&P 500 climbed to a fresh record high above 7,600 as optimism surrounding AI and easing geopolitical tensions continued to support risk appetite.

- Immediate support is around 7,500, followed by stronger support near 7,333 and the 7,200 level.

- The RSI has moved above 74, indicating that the index is now firmly in overbought territory and vulnerable to short-term profit-taking.

- Investors are likely to focus on Broadcom’s earnings and US non-farm payroll data this week, which could introduce additional volatility.

Learn more about the S&P 500 index here.

Nasdaq Composite Index

- The NASDAQ continued to lead US markets, reaching a new all-time high above 27,000 following continued strength in AI-related stocks and Nvidia’s latest announcements.

- Immediate support is around 26,700, followed by stronger support near 25,700 should a pullback occur.

- The RSI has climbed to around 75, indicating that the index is overbought and increasingly susceptible to a technical correction.

- The MACD has turned slightly negative and is pointing towards a potential consolidation phase around the 27,000 level after the recent strong rally.

Learn more about the Nasdaq Composite index here.

What to look out for this week

Key dates

- Monday, 1 June: Singapore Public Holiday

- Tuesday, 2 June: Singapore Savings Bonds application open

- Wednesday, 3 June: Broadcom earnings

- Thursday, 4 June: Singapore 6-month T-bill auction

- Friday, 5 June: US Nonfarm Payrolls

Get the full list of stocks with upcoming earnings and upcoming dividends.

Follow Beansprout on Telegram, Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments