DBS vs OCBC vs UOB: Which Singapore bank looks best for income investors after the rally

Stocks

By Goh Lay Peng • 22 Jun 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

DBS, OCBC and UOB are near record highs. We compare their earnings growth, capital strength and dividend sustainability to see which bank looks strongest for income.

What happened ?

DBS, OCBC and UOB are trading near their all-time highs.

For much of last year, DBS’ record run drew much of the attention among Singapore’s three local banks.

Since then, OCBC has also become a stronger performer, with its share price catching up against DBS.

Year-to-date, all three Singapore banks have also outperformed the Straits Times Index.

More recently, we looked at how wealth management income could support the banks’ dividends.

This has led to more discussion in the Beansprout community on whether DBS, OCBC or UOB still looks attractive for dividend income after the rally.

In this article, I’ll compare DBS, OCBC and UOB based on their earnings growth, capital strength, dividend payout and return on equity to see which Singapore bank’s dividend looks more sustainable for income investors.

DBS and OCBC delivered stronger 1Q26 results than UOB

The latest 1Q26 results show why Singapore bank stocks have remained in focus.

DBS reported net profit of S$2.93 billion in 1Q26, another record for the bank and up 1% year-on-year.

This was despite a challenging interest rate environment, which led to net interest margin compression and a 5% year-on-year decline in group net interest income to S$3.49 billion.

OCBC reported 1Q26 net profit of S$1.97 billion, up 5% year-on-year.

Notably, OCBC’s total income reached a new high of S$3.83 billion, driven by non-interest income which rose 23% year-on-year.

UOB’s results were more subdued, with 1Q26 net profit declining 4% year-on-year to S$1.44 billion as lower interest rates pressured net interest margin.

Taken together, DBS and OCBC appear to have delivered more resilient 1Q26 earnings, while UOB still needs to show clearer signs of earnings recovery.

DBS and OCBC showed stronger earnings growth among Singapore bank stocks

For income investors, dividend yield alone is not enough.

A dividend is more sustainable when it is supported by earnings growth over time.

One way to assess this is to look at earnings per share growth over the past three years.

If a bank has delivered at least 10% cumulative EPS growth from 2022 to 2025, it suggests that earnings have grown meaningfully across the post-pandemic recovery and the interest rate cycle.

Based on the data, DBS and OCBC passed this screen.

DBS recorded 3-year cumulative EPS growth of 21.3%, while OCBC recorded a stronger 33.6%.

UOB recorded cumulative EPS growth of 2.6% over the same period.

This does not mean UOB is financially weak.

However, it suggests that UOB’s earnings growth has been less consistent than DBS and OCBC over the past three years.

Looking ahead, consensus estimates still point to EPS growth for DBS, OCBC and UOB in 2026 and 2027.

However, these estimates can change if interest rates, loan growth, fee income or credit costs turn out differently from expectations.

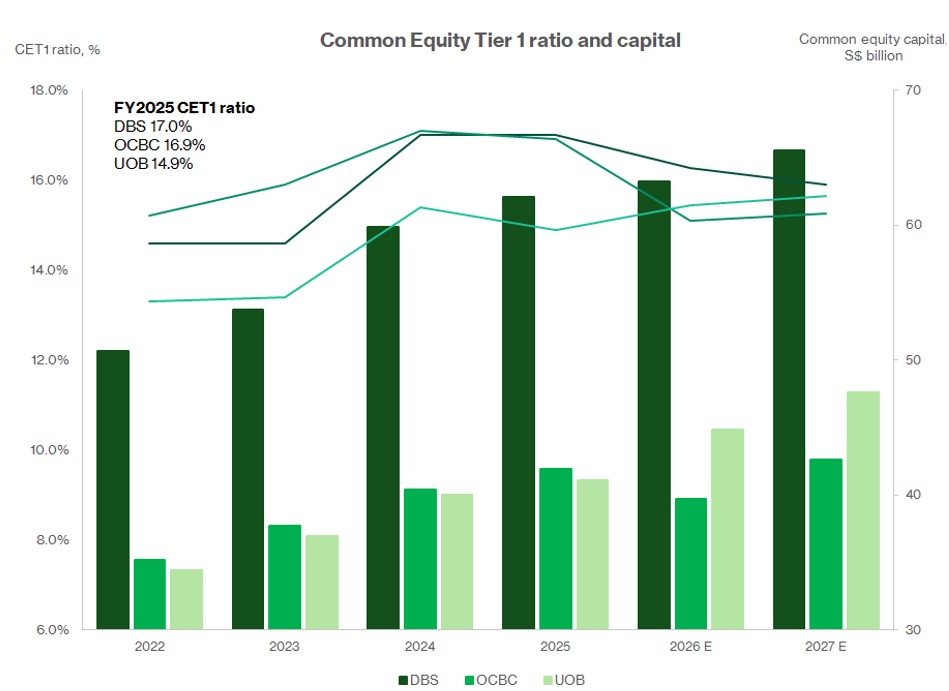

DBS, OCBC and UOB have adequate capital ratios

The second metric I would look at is capital strength.

For banks, the Common Equity Tier 1 ratio, or CET1 ratio, measures the quality of a bank’s capital against its risk-weighted assets.

A higher CET1 ratio gives a bank more room to absorb losses, support lending growth and maintain dividends during tougher periods.

DBS, OCBC and UOB all had sizeable capital buffers as at FY2025.

DBS reported a CET1 ratio of 17.0%, the strongest among the three banks.

OCBC was close behind at 16.9%, while UOB reported a CET1 ratio of 14.9%.

All three banks are well above the minimum regulatory requirement.

This suggests that DBS, OCBC and UOB have strong capital positions to support their businesses and dividend policies.

On this metric, DBS has a slight edge over OCBC, although the gap is narrow.

UOB’s capital position is also healthy, even if it is lower than DBS and OCBC.

However, a high CET1 ratio does not remove earnings risk.

The banks still need recurring profits to support dividends over the long term.

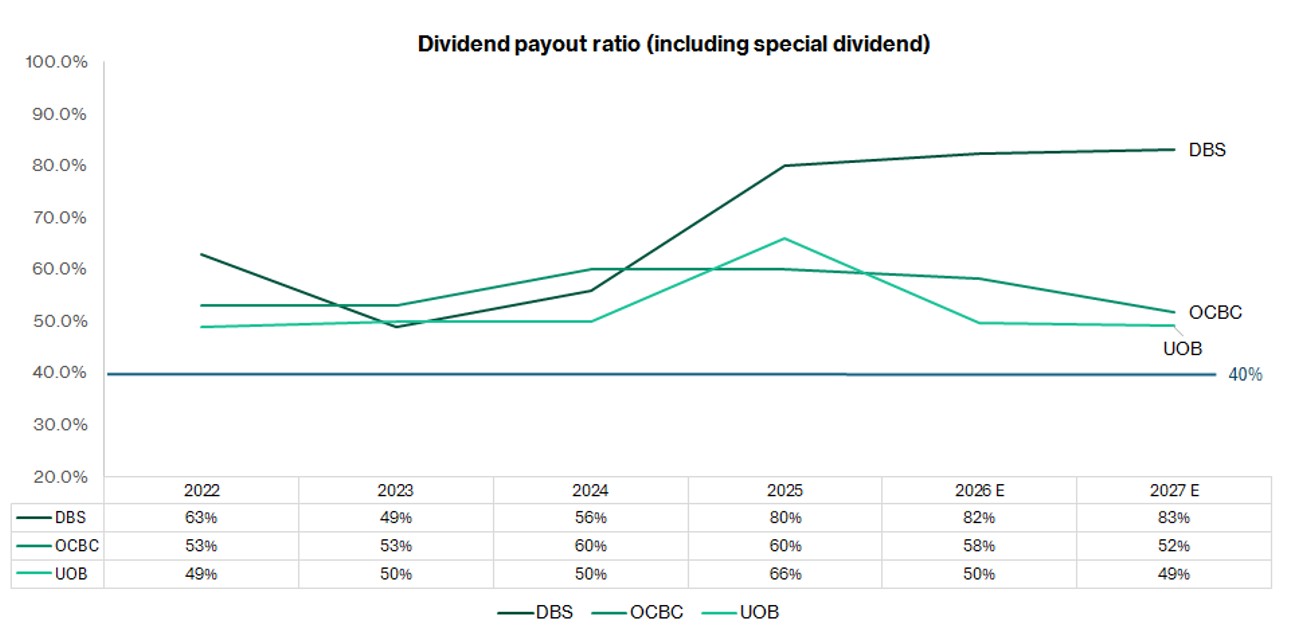

DBS, OCBC and UOB dividends remain supported by healthy payout ratios

Next, I would look at dividend payout ratio.

A payout ratio of at least 40% can indicate that management has a clear commitment to returning profits to shareholders.

All three Singapore banks have historically maintained dividend payout ratios above 40%.

This suggests that DBS, OCBC and UOB have been willing to share a meaningful portion of earnings with shareholders.

DBS had the highest FY2025 dividend payout ratio among the three banks at 80%, up from 56% in FY2024.

This reflects DBS’ higher shareholder returns, including its capital return dividend, supported by strong earnings and capital strength.

Based on estimates, DBS’ dividend payout ratio is expected to remain above 80% in 2026 and 2027.

OCBC’s FY2025 dividend payout ratio was 60%, unchanged from FY2024.

This remains comfortably above the 40% level used in this article, suggesting that OCBC has maintained a steady commitment to returning profits to shareholders.

However, OCBC’s payout ratio is expected to ease to 58% in 2026 and 52% in 2027, based on estimates.

UOB’s FY2025 dividend payout ratio rose to 66%, compared with 50% in FY2024.

This was the second-highest among the three banks, although its payout ratio is expected to normalise to about 50% in 2026 and 49% in 2027.

Income investors should also look at the type of dividend being paid.

DBS has included a capital return dividend for 2026 and 2027, while OCBC has also included a capital return dividend for 2026.

UOB completed its capital return in 2025, and its dividend is expected to revert to ordinary dividends.

This distinction is important because ordinary dividends are more useful when assessing long-term dividend sustainability, while capital return dividends may not continue once the capital return programme ends.

Overall, DBS, OCBC and UOB appear able and willing to maintain dividend payout ratios above 40%.

The key difference is that DBS and OCBC currently have stronger earnings growth and capital positions to support their dividend plans, while UOB’s payout ratio is expected to normalise after FY2025.

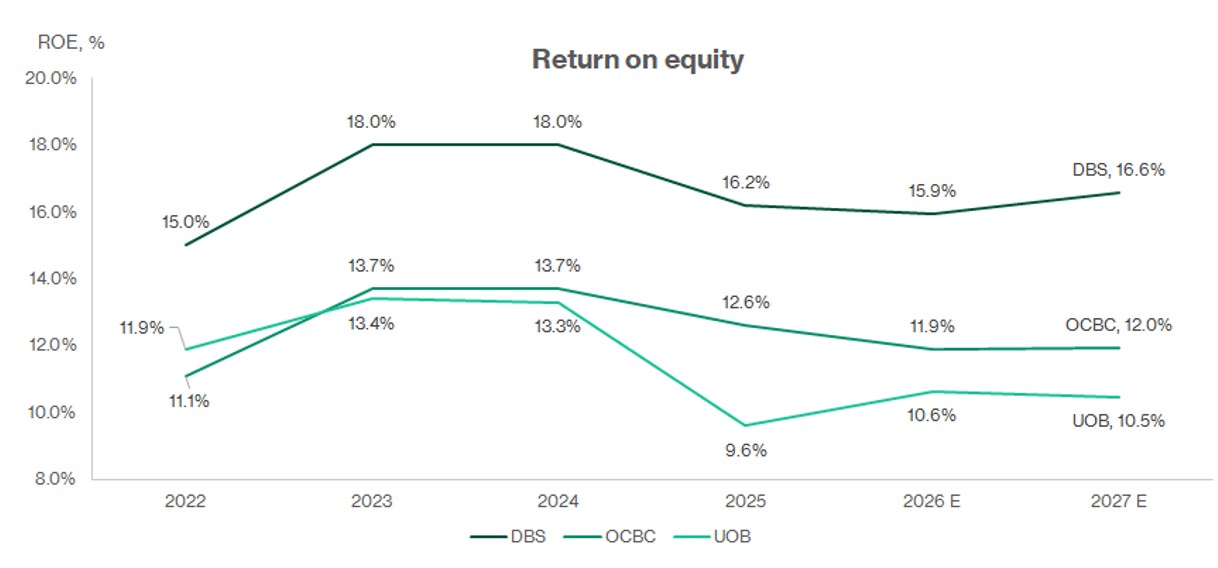

DBS and OCBC continue to generate stronger return on equity

Return on equity, or ROE, shows how efficiently a bank turns shareholder capital into profits.

For income investors, this is useful because a bank that earns a higher ROE may have more room to support dividends while still investing for future growth.

DBS and OCBC have consistently achieved ROE above 10% in recent years.

This points to strong profitability across their businesses.

UOB’s ROE dipped in 2025, although consensus estimates suggest that it could recover to above 10% in 2026 and 2027.

Among the three banks, DBS continues to stand out for its stronger ROE profile.

OCBC also remains solid, supported by its diversified income streams and growing wealth management business.

UOB’s ROE recovery will be an important signpost to watch.

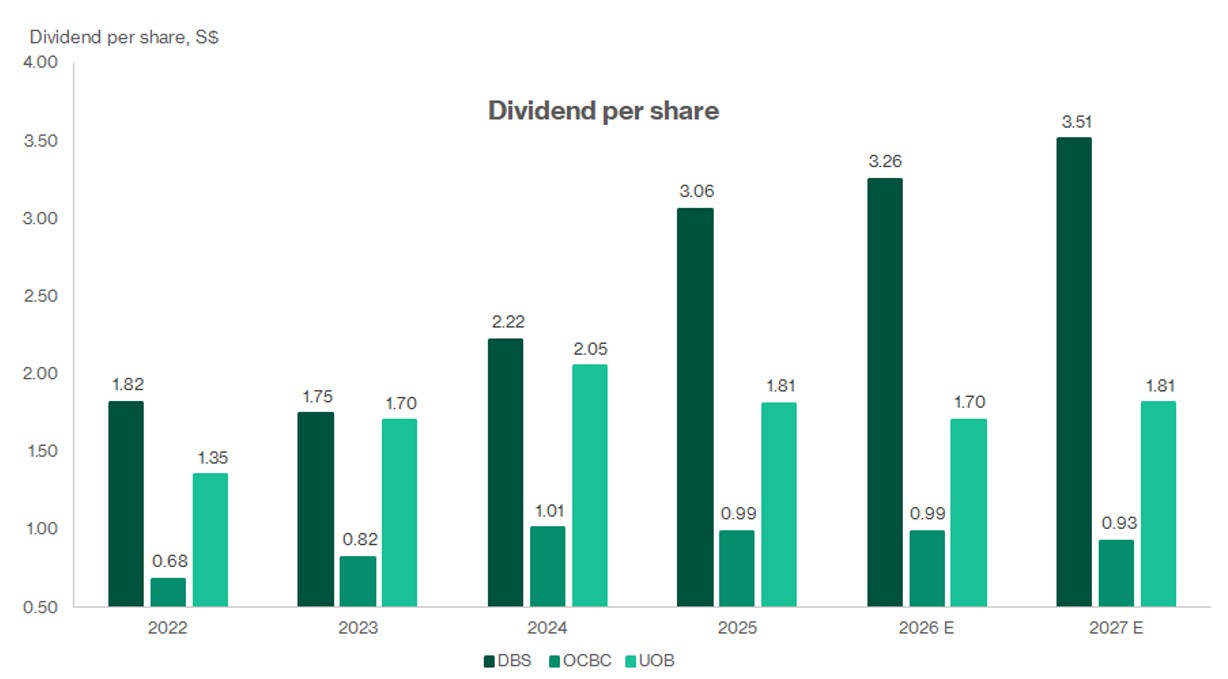

DBS offers the highest estimated dividend yield and strongest dividend per share growth

After the recent share price gains, dividend yield becomes an important question for income investors.

However, I would also look at the dividend per share trend to see whether the expected yield is supported by rising dividends.

Based on the chart, DBS’ dividend per share rose from S$2.22 in FY2024 to S$3.06 in FY2025, and is expected to increase further to S$3.26 in 2026 and S$3.51 in 2027.

This gives DBS the clearest dividend per share growth profile among the three banks.

However, investors should note that DBS’ dividends include capital return dividends for 2026 and 2027.

OCBC’s dividend per share has been steadier, easing slightly from S$1.01 in FY2024 to S$0.99 in FY2025, before staying around S$0.99 in 2026 and easing to S$0.93 in 2027.

UOB’s dividend per share fell from S$2.05 in FY2024 to S$1.81 in FY2025, and is expected to be S$1.70 in 2026 before recovering to S$1.81 in 2027.

Dividend per share should not be compared directly across banks, as their share prices are different.

This is why dividend yield remains useful, as it shows the expected income return relative to the current share price.

As of the closing prices on 17 June 2026, DBS was trading at S$65.01.

Based on FY2026 dividend estimates, this implies a dividend yield of about 5.0%.

OCBC was trading at S$24.62, with an estimated FY2026 dividend yield of about 4.0%.

UOB was trading at S$39.35, with an estimated FY2026 dividend yield of about 4.3%.

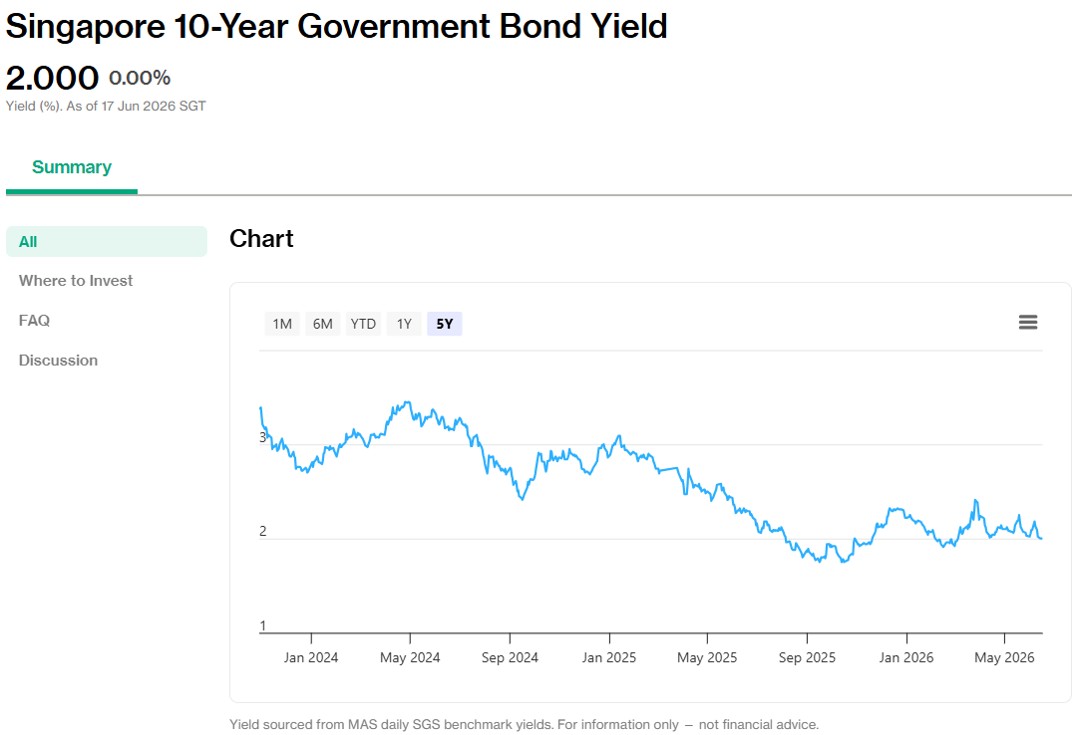

If we compare them with the Singapore 10-year government bond yield of about 2% on 17 Jun 2026, DBS offers an attractive spread of 3% over the risk free rate, which is also the widest spread among the three banks.

This may remain appealing for income investors, especially if interest rates stay higher for longer and bank earnings receive some support from net interest income.

Related links:

- DBS dividend history and dividend forecast

- OCBC dividend history and dividend forecast

- UOB dividend history and dividend forecast

What would Beansprout do?

The higher-for-longer interest rate backdrop may provide some support to the banks’ net interest income, while their estimated dividend yields still offer a spread over the Singapore 10-year government bond yield.

When comparing Singapore bank stocks, dividend yield is often the first metric investors look at. However, a higher yield does not necessarily make a bank the better long-term investment.

When considering stocks for my income pot as part of Beansprout's four pots of wealth, I would first check whether the dividend is supported by earnings growth, capital strength and efficient use of shareholder equity.

| Metric compared | DBS | OCBC | UOB |

| 1Q26 net profit growth | +1% yoy | +5% yoy | -4% yoy |

| 3-year cumulative EPS growth | 21.3% | 33.6% | 2.6% |

| CET1 ratio | 17.0% | 16.9% | 14.9% |

| FY2025 Dividend payout ratio | 80% | 60% | 66% |

| FY2025 Return on equity | 16.2% | 12.6% | 9.6% |

| FY2026 dividend yield | 5.0% | 4.0% | 4.3% |

| Source: Company data, FactSet estimates. Share prices and dividend yield estimates are based on closing prices as of 17 June 2026. | |||

Among the three banks, DBS has delivered solid EPS growth, has the highest CET1 ratio among the three, continues to generate a strong ROE, and offers the highest FY2026 dividend yield.

However, investors should recognise that part of DBS’ dividend in 2026 and 2027 includes a capital return dividend. This makes the near-term income yield attractive, but I would separate recurring ordinary dividends from capital return when assessing the longer-term dividend yield.

OCBC's EPS growth from 2022 to 2025 was stronger than DBS, and its 1Q26 results were supported by record non-interest income and stronger wealth management income. However, its lower dividend yield means the income spread is not as wide as DBS.

UOB remains financially sound, with a healthy capital position and a dividend yield above 4%. However, its weaker EPS growth and softer 1Q26 profit make it harder to rank ahead of DBS and OCBC for now.

Overall, DBS appears to have the strongest income consistency among the three, with OCBC close behind. On the other hand, UOB will have to demonstrate clearer earnings growth and ROE recovery.

The growth in wealth management income is also worth watching across all three banks, as it could provide another source of recurring earnings to support dividends when net interest margins come under pressure.

This is aligned with our view that investors may consider looking beyond Singapore REITs to Singapore blue chip stocks for more diversified dividend income, especially when the dividends are supported by earnings growth, strong balance sheets and sustainable payout ratios.

By combining different sources of dividends, investors may be able to build a more resilient income portfolio over time. Learn how to build a more dependable stream of income that can hold up across cycles here.

If you’d like to screen for other Singapore stocks with attractive dividend yields and potential upside, you can explore our Singapore dividend stocks screener.

Which Singapore bank stock would you prefer for dividend income: DBS, OCBC or UOB? Leave a comment below or share with us in the Beansprout telegram group.

Planning to invest in the Singapore banks? Compare the best Singapore brokers to find the right trading platform, and see the latest promotions and sign-up rewards available.

Follow Beansprout on Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments