Fed signals higher rates. What it means for Singapore REIT yields and income

REITs

By Goh Lay Peng • 24 Jun 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

Singapore REITs fell after the Fed turned hawkish. We assess what is the impact, which REIT subsectors stand out, and what income investors should watch.

What happened?

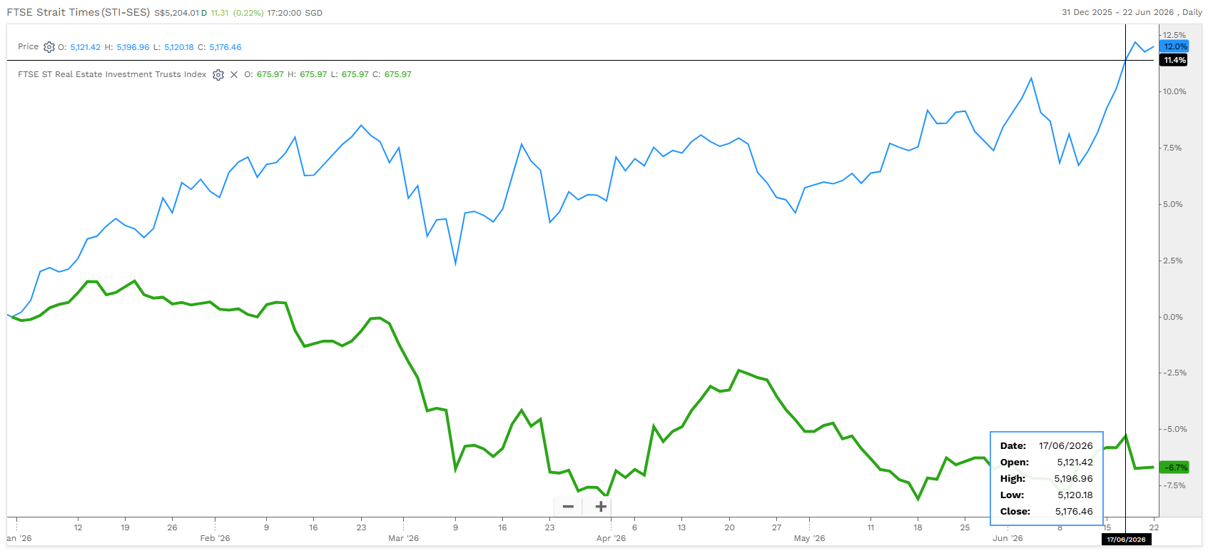

Singapore REITs are under pressure again.

Following the latest US Federal Reserve meeting, the Straits Times Index gained about 0.7%, while the FTSE ST All-Share REIT Index fell about 1.8%, reflecting the sector’s sensitivity to higher-for-longer interest rate expectations.

The Fed kept interest rates unchanged at 3.50% to 3.75%, which was widely expected by investors.

However, the bigger surprise came from the Fed’s more hawkish projections, with officials raising their inflation forecasts and signalling that interest rates may stay elevated for longer.

This follows earlier concerns we highlighted when the Fed warned that inflation could rise, and when we looked at how the Iran conflict could push oil prices and bond yields higher.

We also recently shared that investors were no longer just debating the timing of rate cuts, but whether the Fed may need to raise rates again.

This matters for Singapore REITs, as they are often held for income and are among the more interest rate-sensitive parts of the Singapore market.

In this article, I look at why Singapore REITs (S-REITs) reacted negatively, what higher-for-longer rates could mean for distributions, and which parts of the S-REIT market may be worth watching.

Why did Singapore REIT prices fall after the latest FOMC decision?

#1 - Elevated inflation supports higher-for-longer interest rates

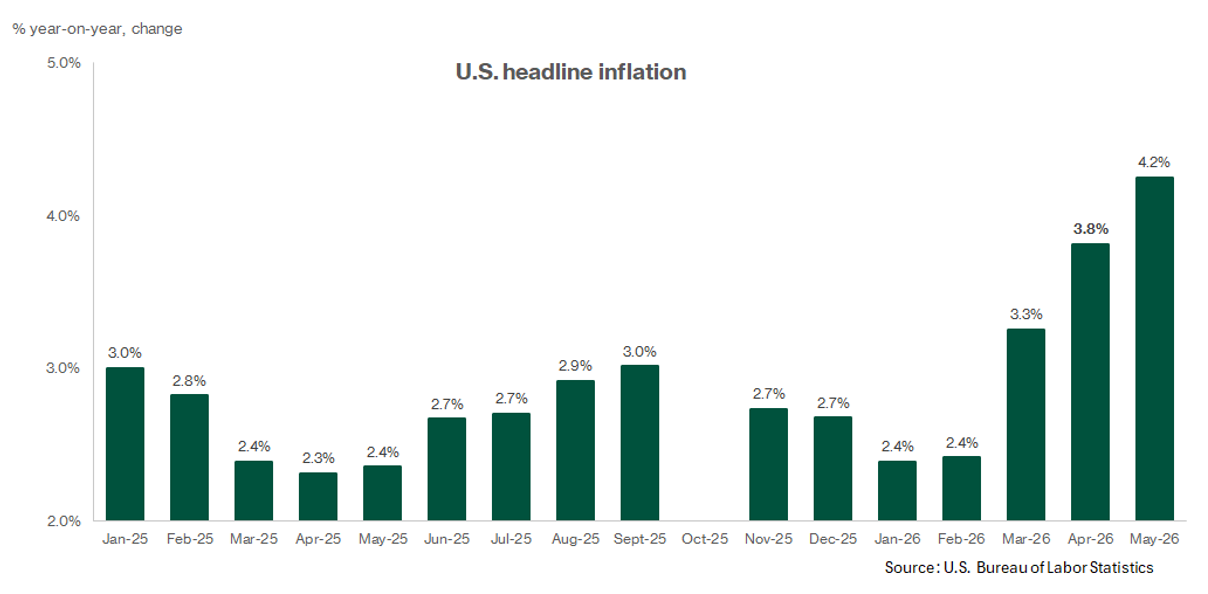

US inflation has picked up again.

For May 2026, US headline CPI rose by 4.2% year-on-year, the first reading above 4% since 2023.

Core CPI, which excludes food and energy prices, rose by 2.9% year-on-year.

A key driver was the sharp rise in energy prices following the Middle East conflict.

This has complicated the Federal Reserve's policy response.

Higher energy prices can push inflation up, but monetary policy is less effective in dealing with supply-driven inflation compared to demand-driven inflation.

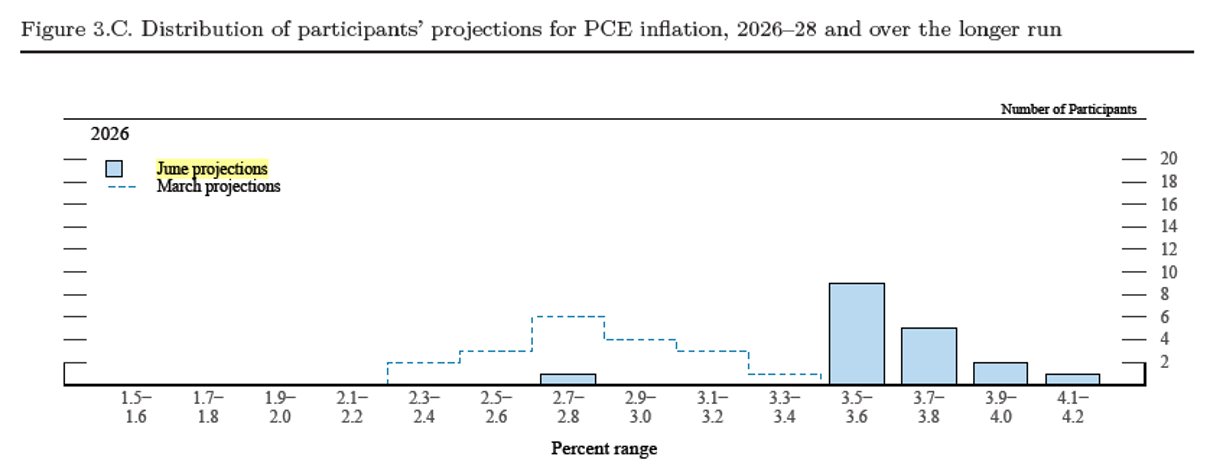

The Fed’s latest Summary of Economic Projections (SEP) also showed a notable change in its inflation outlook.

Officials raised their 2026 PCE inflation forecast to 3.6%, from 2.7% in March.

Core PCE inflation, which is the Fed’s preferred gauge of underlying inflation, was also revised up to 3.3%, from 2.7% previously.

For Singapore REITs, the concern is not just inflation itself. The bigger issue is what persistent inflation could mean for future interest rates.

If inflation stays above the Fed’s target, investors may expect interest rates to remain higher for longer, or even rise again.

#2 - FOMC members projected a higher path for interest rates

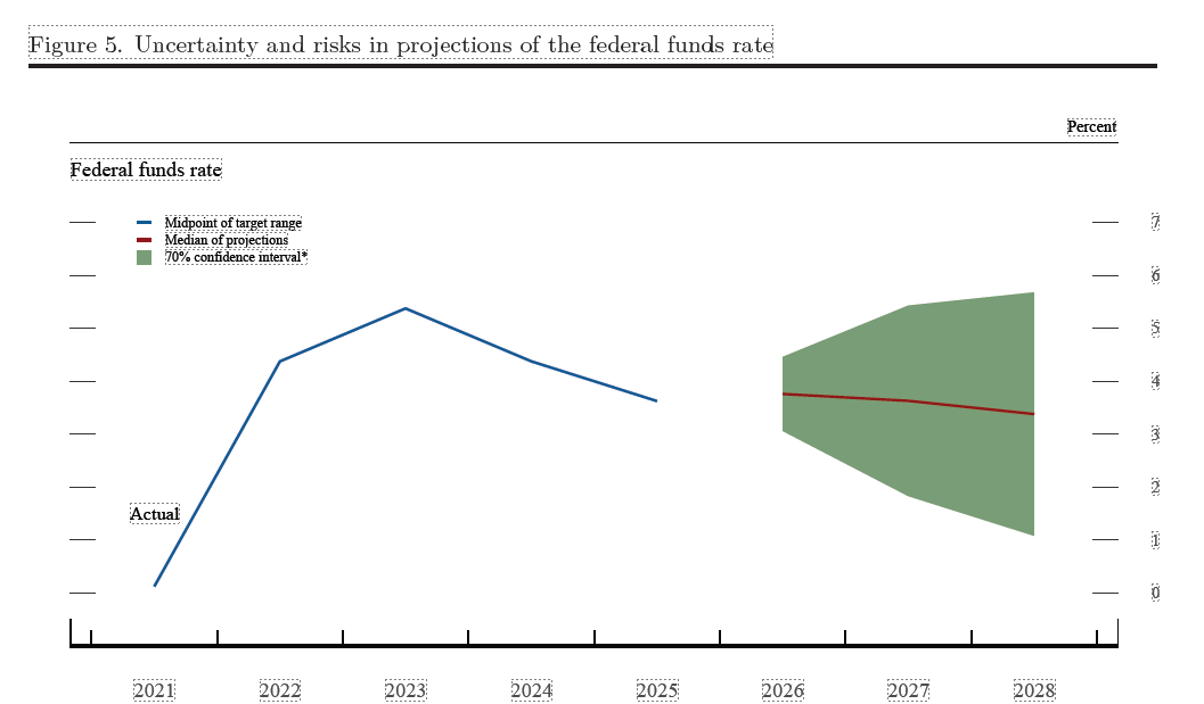

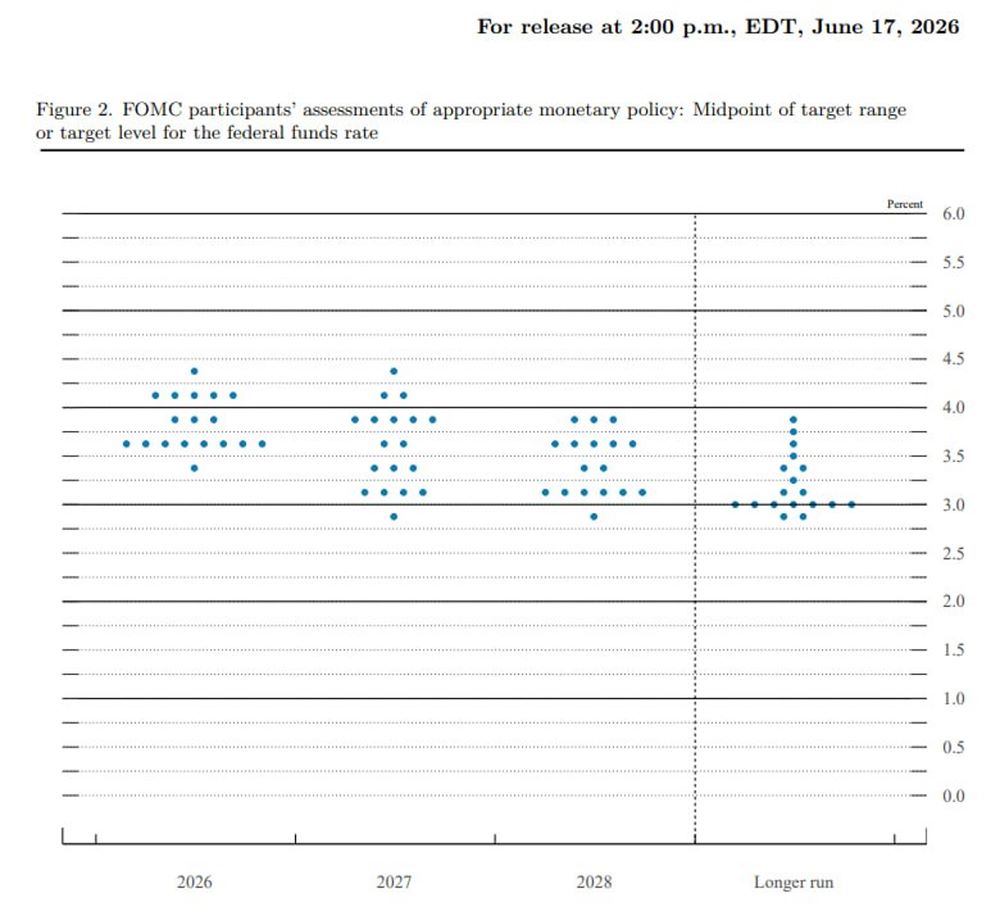

The Fed’s dot plot also shifted in a more hawkish direction.

The median 2026 year-end federal funds rate projection rose to 3.8%, from 3.4% in March.

This suggests that Fed officials now expect interest rates to be higher at the end of 2026 than they previously thought.

Note : The blue and red lines are based on actual values and median projected values, respectively, of the Committee’s target for the federal funds rate at the end of the year indicated. The actual values are the midpoint of the target range; the median projected values are based on either the midpoint of the target range or the target level.

The dot plot also showed a wide range of views among policymakers.

Nine out of 18 officials submitted projections above the current midpoint of the federal funds rate range, suggesting that half of the committee saw a higher policy rate as appropriate by year-end.

Eight officials saw rates staying around the current midpoint, while only one official projected a lower rate.

This does not mean a rate hike is certain.

However, it does suggest that the market can no longer assume that rate cuts are coming soon.

For REIT investors, that matters because REIT prices are often supported when investors expect interest rates and bond yields to fall.

When that expectation changes, REIT valuations can come under pressure.

#3 - The Fed’s communication style may add uncertainty

Another change investors are watching is the communication style of new Fed Chair Kevin Warsh.

At his first FOMC meeting as Fed Chair, Warsh signalled a different approach from his predecessor.

He has indicated a preference for less reliance on forward guidance and has announced reviews into areas such as the Fed’s communications, balance sheet and data sources.

This could make future policy signals less predictable for markets.

For investors, less explicit guidance may mean more focus on incoming inflation and labour market data.

It could also mean more volatility in bond yields if markets have to adjust quickly to new information.

For interest rate-sensitive assets such as Singapore REITs, this is another reason why investor sentiment may stay cautious in the near term.

During the Federal Reserve’s Press Conference Opening Statement, Chair Kevin Warsh reaffirmed that the Fed remains focused on restoring price stability and bringing inflation back to its 2% target.

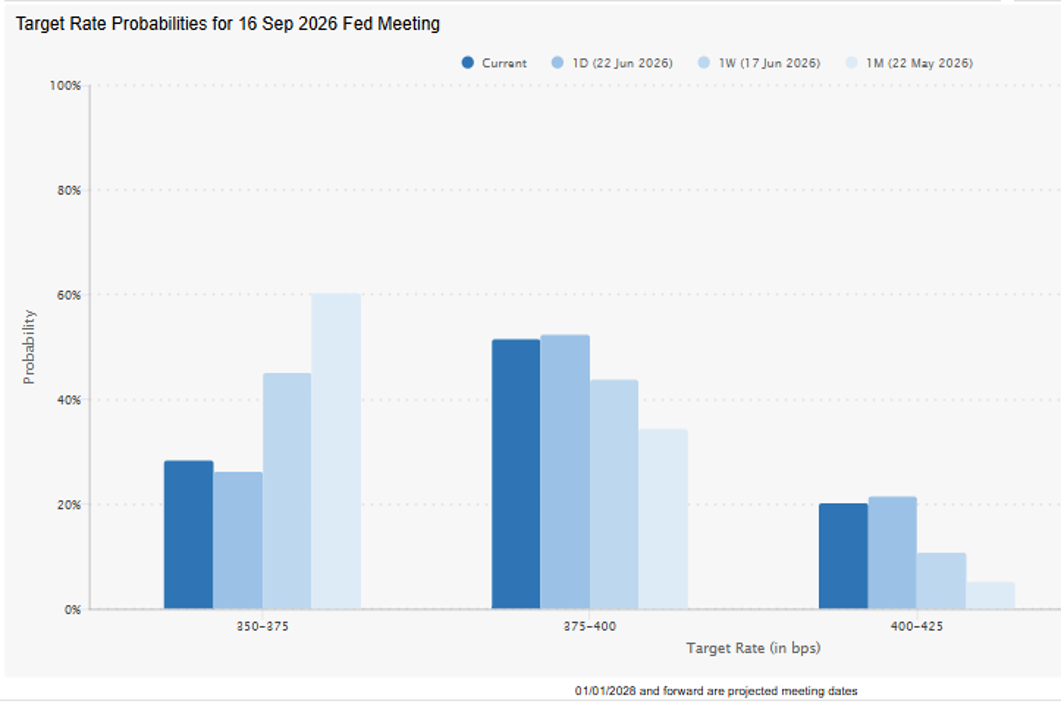

Following the meeting, the CME FedWatch Tool showed that futures traders had brought forward expectations for the next potential Fed rate hike to September 2026.

Why higher bond yields can put pressure on S-REIT prices

Singapore REITs are often bought for income.

When bond yields rise, investors compare REIT yields against safer income assets such as government bonds.

If the yield spread between REITs and government bonds narrows, some investors may demand a higher return from REITs to compensate for the additional risks.

This can put downward pressure on REIT prices.

When REIT prices fall, their distribution yields rise.

That is why higher interest rate expectations can lead to lower REIT unit prices, even if the underlying properties continue to perform reasonably well.

This helps explain why Singapore REITs have underperformed even though many underlying assets, such as Singapore malls, logistics parks, offices and data centres, are still seeing resilient demand.

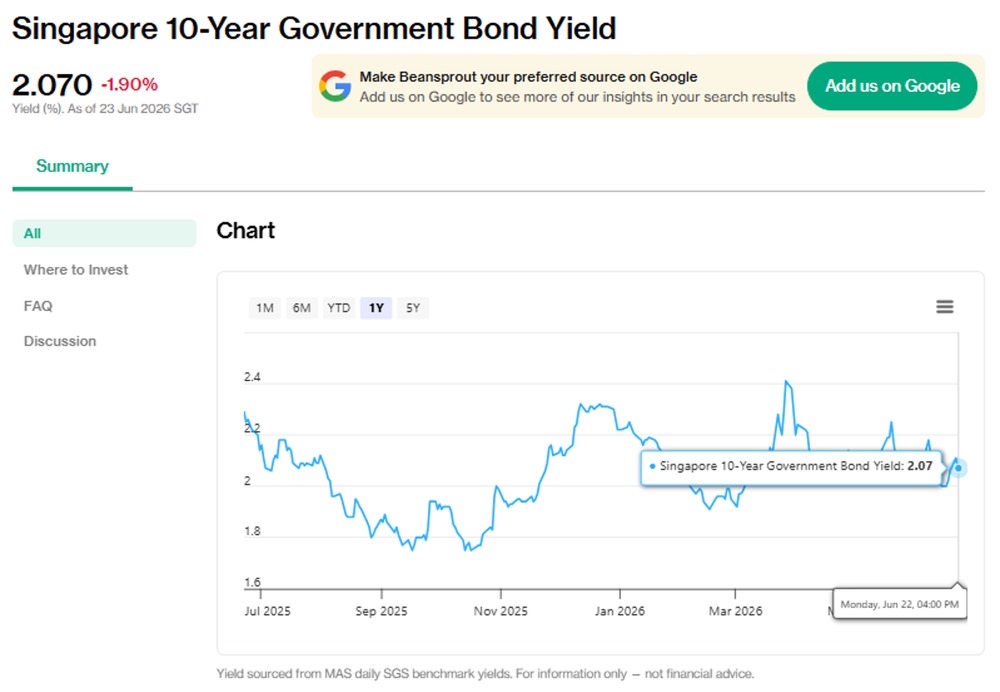

In Singapore, the 10-year government bond yield has remained around 2.0%, supported partly by the relative strength of the Singapore dollar versus the regional currencies.

However, global bond yields still matter.

Higher US Treasury yields can affect investor risk appetite, valuation assumptions and funding conditions across markets.

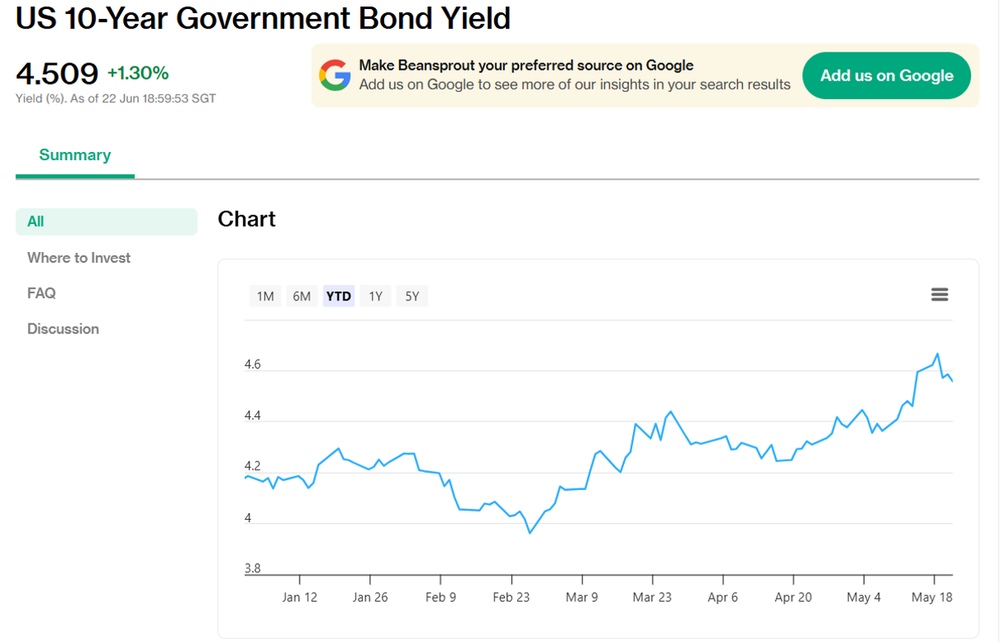

Following the FOMC decision on 17 Jun 2026, the US 10-year Treasury yield rose to settle at above 4.5%, up 35 basis points year-to-date.

How borrowing costs may affect S-REIT distributions

Higher interest rate expectations can also affect REITs through funding costs.

Many Singapore REITs use debt facilities linked to the Singapore Overnight Rate Average, or SORA which serves as Singapore's primary floating-rate reference rate.

Larger REITs with overseas assets may also have borrowings denominated in foreign currencies, making US dollar funding costs directly relevant.

Even for predominantly SGD-funded REITs, SORA tends to follow broader global interest rate trends over time, albeit with some lag and periodic divergence due to differences in monetary policy and liquidity conditions.

As interest rate expectations rise, investors anticipate higher refinancing costs and lower distributable income, placing downward pressure on S-REIT valuations.

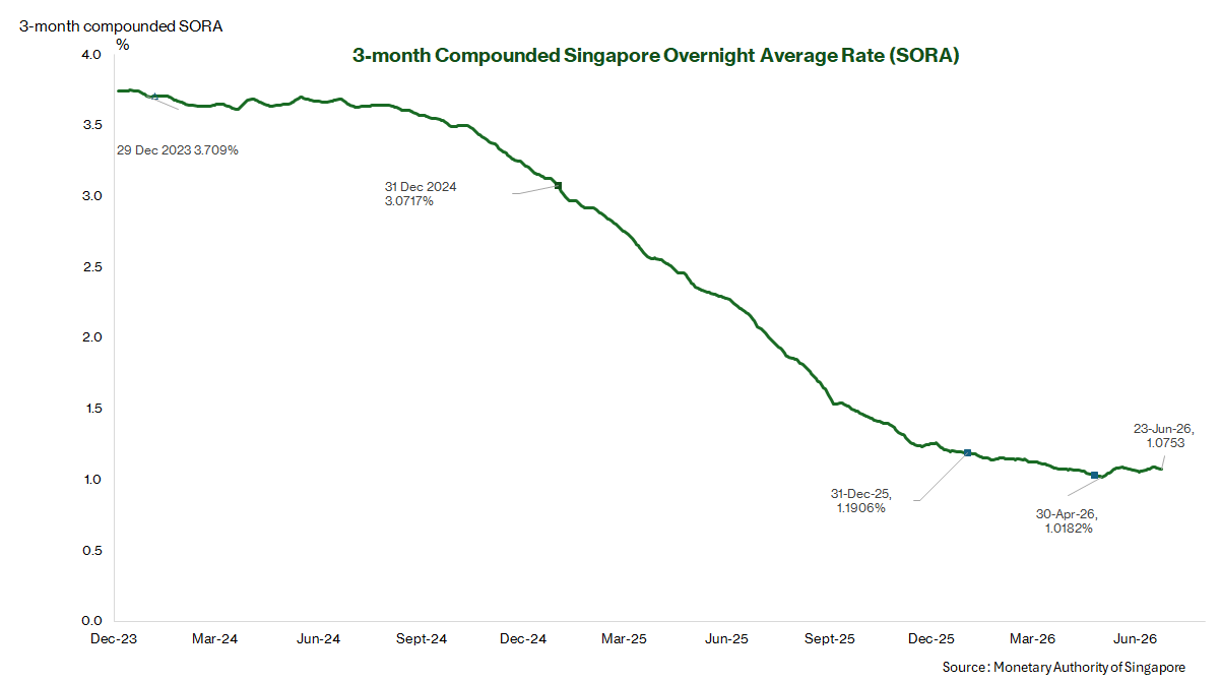

We observe that the compounded 3-month SORA, the rate most directly links to S-REITs’ SGD-denominated debt, remains anchored at near 1.10%.

For REITs refinancing Singapore dollar loans that were taken when SORA was much higher, this could provide some relief to borrowing costs.

This may support distributions for REITs with mostly Singapore dollar debt and well-managed refinancing schedules.

However, investors should still watch the debt profile carefully.

REITs with higher gearing, more floating-rate debt, or large debt maturities due in the near term could face more pressure if borrowing costs rise again.

REITs with longer debt tenors, a high proportion of fixed-rate borrowings and strong interest coverage ratios should be better positioned.

How higher rates may affect S-REIT valuations and acquisitions

The longer-term risk is that US Treasury yields move higher again if the Fed raises rates more than expected.

In that scenario, the relative attractiveness of Singapore REIT yields could weaken as investors may demand a higher return from REITs to compensate for the additional risk.

This would put downward pressure on S-REIT prices, even if Singapore borrowing costs remain relatively stable.

Higher interest rates which leads to higher financing costs would also make it more difficult for REITs to grow through acquisitions.

REITs typically grow distributions by acquiring properties using a mix of debt and equity.

However, when borrowing costs are high and equity prices are weak, fewer acquisitions are likely to be distribution per unit accretive.

This could slow one of the key sources of long-term DPU growth for the sector.

Which Singapore REIT sectors may hold up better?

In a higher-for-longer rate environment, I would focus less on headline yield and more on the quality of the underlying assets.

As we highlighted in our recent look at Singapore REITs with higher dividend yields, the sector now offers a wide range of yields after the recent pullback.

However, higher yield alone does not necessarily mean better value.

These include those focused on Singapore data centres, office, logistics and purpose-built accommodation, where demand has been relatively more stable. REITs with overseas assets that actively manage currency risks may also be better positioned.

At the same time, many REITs have taken steps in recent years to manage their debt, such as locking in borrowing costs at attractive levels and over a longer tenor. This provides support from higher interest rates if they persist.

Data centre REITs are relatively well protected from higher interest rates. The rapid expansion of artificial intelligence and cloud computing has created strong demand for data centre capacity.

For example, Digital Core REIT reported cash rental reversions of 44% in 1Q2026, while Keppel DC REIT achieved portfolio rental reversions of 51%.

This suggests that some data centre landlords may still have pricing power when leases are renewed.

We took a closer look at four Singapore data centre REITs offering dividend yields of up to 8% as AI drives demand for data centres here.

In the retail segment, CapitaLand Integrated Commercial Trust reported retail rental reversion of 4.4% in 1Q2026.

Its suburban malls performed better than downtown malls, with rental reversions of 5.1% compared to 3.9%.

CICT’s retail portfolio occupancy stood at 97.8% as at March 2026, which remained resilient against the broader retail market.

Singapore office assets have also benefited from limited new supply and tight vacancy in the CBD.

For example, Keppel REIT reported rental reversion of 17.2% across its Singapore office portfolio in 1Q2026.

However, investors should avoid treating the whole REIT sector as one single trade.

Performance may differ across REITs depending on asset class, geography, lease structure, debt profile and currency exposure.

A REIT with a high yield may still be risky if its DPU is falling, gearing is elevated, or refinancing needs are high.

What to watch next for Singapore REITs

For now, the key question is whether the pressure from higher interest rates continues, or whether the market starts to price in rate cuts again.

There are a few macro indicators I would watch.

#1 - US inflation data

The first is US inflation.

If headline inflation and core PCE remain elevated, the Fed may have less room to cut rates.

This could keep US Treasury yields high and weigh on sentiment towards income assets such as REITs.

#2 - Oil prices and geopolitical risks

Oil prices are another important signpost.

A further increase in energy prices could add to inflation pressure, especially if supply disruptions from the Middle East become more serious.

This would make it harder for the Fed to turn less hawkish.

#3 - US 10-year Treasury yield

The US 10-year Treasury yield is also worth watching closely.

A sustained move higher would make government bonds more attractive relative to REITs.

This could put pressure on REIT valuations, as investors may demand a higher yield to compensate for the additional risk of owning REITs.

#4 - Singapore dollar interest rates

Closer to home, the 3-month compounded SORA remains an important benchmark for many Singapore REITs’ floating-rate borrowings.

If SORA stays relatively low, some REITs may still benefit when refinancing Singapore dollar debt.

However, funding cost pressure could return if global rate expectations push SORA higher again, or if the Monetary Authority of Singapore changes its policy stance.

#5 - The Singapore dollar

The Singapore dollar is another factor to watch.

A stronger Singapore dollar may help keep domestic inflation contained.

However, it can also reduce translated income for REITs with overseas assets, especially if rental income is collected in foreign currencies but distributions are paid in Singapore dollars.

Beyond these macro indicators, I would also watch the upcoming REIT results.

The key operating metrics are rental reversions, occupancy rates and refinancing updates.

These will give investors a clearer sense of whether higher yields are backed by resilient cash flows, or whether distributions may come under pressure.

What would Beansprout do?

The latest FOMC meeting did not bring an interest rate hike.

However, the Fed’s higher inflation forecasts and more hawkish rate projections have made the outlook less favourable for interest rate-sensitive assets such as Singapore REITs.

Despite the headwinds from higher interest rates, I think investors can build exposure into S-REITs with high quality assets and predictable cash flows.

One mitigating factor is that Singapore dollar borrowing costs remain relatively low.

The 3-month compounded SORA remains close to 1.1%, which may provide an opportunity for some S-REITs to refinance Singapore dollar debt at lower costs compared to the 2023 to 2024 peak.

That said, balance sheet quality and debt maturity profiles are more important than ever in this environment.

S-REITs with well-staggered debt maturities, a high proportion of fixed-rate borrowings and strong interest coverage ratios are better placed to absorb uncertainty.

Those with near-term refinancing needs, higher gearing or greater exposure to floating-rate debt in a rising-rate environment face greater risk to their distributions.

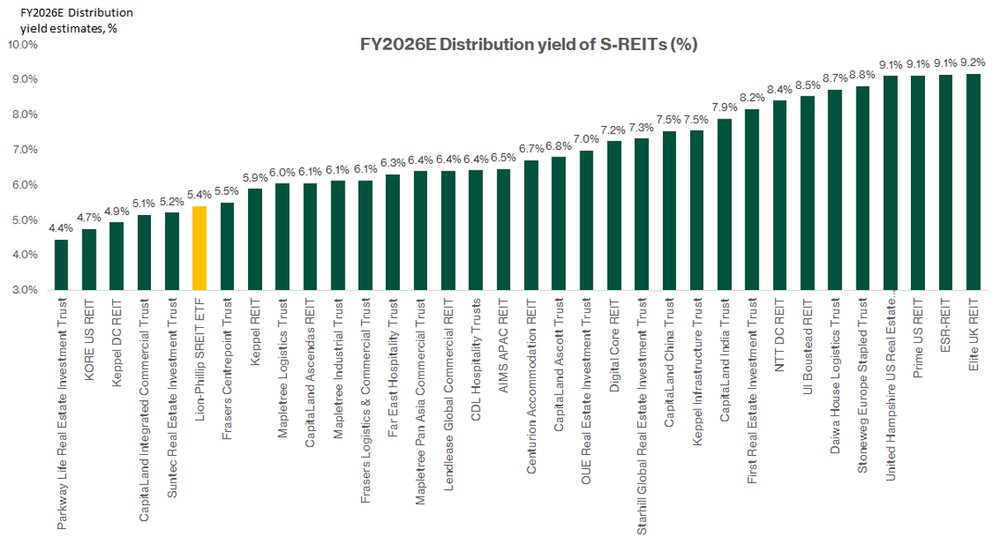

Valuations have also become more reasonable after the recent pullback. The Lion-Phillip S-REIT ETF (SGX : CLR) is offering a distribution yield of 5.45% (at close 22 Jun 2026).

As shown in the chart below, there are several REITs that offer higher distribution yield, suggesting some of the risk may already be priced in.

Among mid-cap names, CapitaLand India Trust, Digital Core REIT and Stoneweg Europe Stapled Trust offer growth opportunities, while AIMS APAC REIT and Parkway Life REIT have shown resilient distribution. However, I would be careful not to chase the highest yield alone.

For my Income Pot, I would focus on REITs with strong assets, healthy occupancy, visible rental growth, manageable gearing and well-spread debt maturities.

To screen for Singapore REITs with lowest price-to-book valuation or highest dividend yield, check out our best Singapore REIT screener.

Singapore REITs can still play a useful role in an income portfolio, especially for investors seeking steady distributions, property exposure or potential upside if interest rates fall, but they also come with risks such as refinancing costs, changes in asset values and potential dilution from capital raising.

Rather than relying too heavily on REITs alone, I would build a broader mix of income sources, including quality Singapore blue-chip stocks with sustainable dividends, resilient earnings and strong balance sheets.

For my Income Pot, the key is not just to chase the highest yield. It is to build an income portfolio that can hold up across different market conditions. Learn more about how to build passive income streams with our income pot here.

By combining quality dividend stocks with selected REITs, investors may be better placed to grow dividends over time, while improving the resilience of their portfolio.

You can find out some of our investment ideas to capture opportunities in the market here.

Which part of the Singapore REIT market are you watching most closely now: data centres, retail malls, offices, logistics or overseas REITs? Share with us in the comments below or in our Telegram group!

If you are new to investing in Singapore REITs, you can start to learn more about Singapore REITs here.

If you prefer diversification without picking individual REITs, you can also gain exposure through Singapore REIT ETFs.

Planning to invest in Singapore REITs? Compare the best Singapore brokers to find the right trading platform, and see the latest promotions and sign-up rewards available.

Follow Beansprout on Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments