4 Singapore data centre REITs with dividend yields of up to 8%. What income investors may want to watch

REITs

By Goh Lay Peng • 09 Jun 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

We take a closer look at four Singapore data centre REITs offering dividend yields of up to 8% as AI drives demand for data centres.

What happened?

Data centre REITs are back in focus.

As AI demand grows, investors have been looking for ways to gain exposure to the theme without investing directly in technology stocks.

We previously looked at how data centres could offer a way to participate in the AI trend through income-generating REITs, as data centres receive rental income from tenants that use capacity for cloud, artificial intelligence and enterprise workloads.

At the same time, Singapore REITs have lagged the market and present income opportunities for investors looking for dividend income.

However, not all data centre REITs are seeing their distributions grow at the same pace.

In this article, I look at four Singapore-listed REITs with data centre exposure, their dividend yields, and the key things investors should watch.

4 Singapore data centre REITs with dividend yields of up to 8% as AI demand grows

#1 - Keppel DC REIT (SGX: AJBU)

Keppel DC REIT is one of the clearest pure-play data centre REITs listed in Singapore.

As at 31 March 2026, the REIT had assets under management of about S$6.3 billion, with 25 data centres across 10 countries.

Its portfolio is also strongly tilted towards Asia Pacific, which made up 84.7% of AUM. Singapore alone accounted for 62.7%, while Japan accounted for 13.6%.

This matters because Singapore and Japan remain key data centre markets in Asia, supported by demand from cloud, enterprise and AI-related workloads.

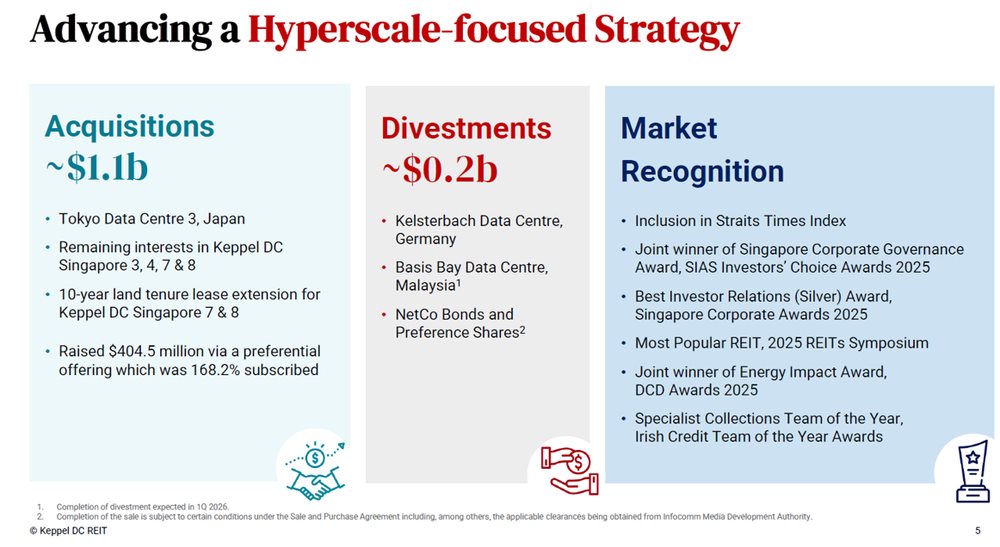

Keppel DC REIT has also been actively increasing its exposure to hyperscale data centres.

In FY2025, the REIT completed or announced about S$1.1 billion of acquisitions, including Tokyo Data Centre 3, the remaining interests in Keppel DC Singapore 3 and 4, and the 10-year land tenure lease extension for Keppel DC Singapore 7 and 8.

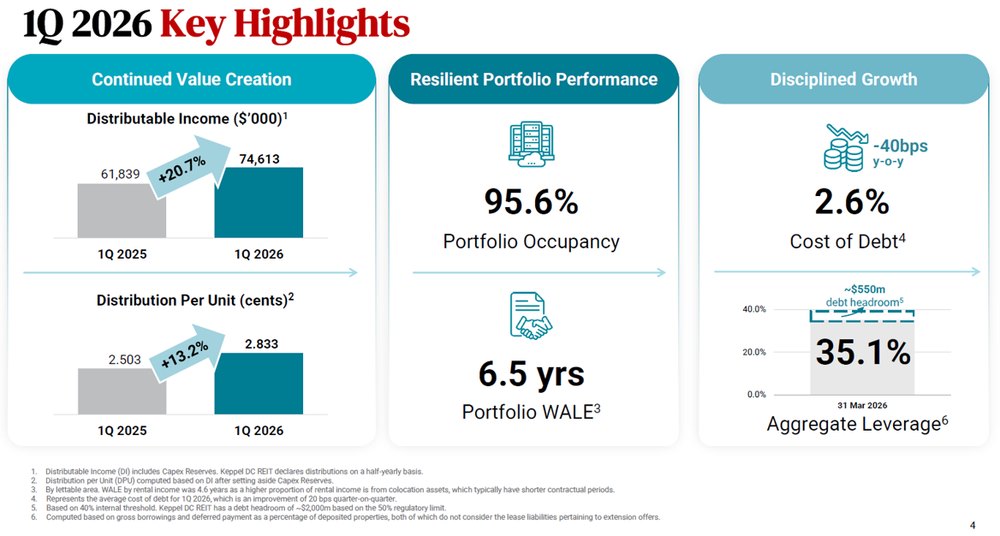

The latest 1Q 2026 update also showed that demand for its data centre assets remained healthy.

Portfolio occupancy stood at 95.6%, while portfolio weighted average lease expiry (WALE) was 6.5 years. Keppel DC REIT also reported portfolio reversion of about 51% in 1Q 2026, following about 45% portfolio reversion for FY2025.

Its balance sheet also appears manageable, with aggregate leverage of 35.1%, an average cost of debt of 2.6%, and interest coverage of 7.2 times.

Notably, it has one of the lowest cost of debt among the listed REITs in Singapore.

Keppel DC REIT also noted that global data centre demand continues to be supported by cloud adoption, digital transformation and rising AI workloads.

In particular, AI inference could become a bigger driver of data centre demand over time, as AI applications are increasingly deployed in search, chatbots, recommendation engines and other real-time use cases.

On distributions, Keppel DC REIT’s DPU trend is the strongest among the four REITs in this list.

For FY2025, Keppel DC REIT reported DPU of 10.381 Singapore cents, up 9.8% year on year, supported by acquisitions and higher contributions from contract renewals and rental escalations.

In 1Q 2026, Keppel DC REIT’s DPU rose 13.2% year-on-year to 2.833 Singapore cents, supported by strong portfolio performance and contributions from Tokyo Data Centre 3 and the remaining interests in Keppel DC Singapore 3 and 4.

Based on its unit price of S$2.27 as of 9 June 2026, Keppel DC REIT offers a forward dividend yield of 4.4%.

However, Keppel DC REIT’s forward dividend yield is lower than the other REITs in this list, which suggests that investors may already be pricing in some of its stronger portfolio quality and DPU growth profile.

For Keppel DC REIT, I would watch whether it can continue to deliver positive rental reversions and make accretive acquisitions without stretching its balance sheet.

Find out how much dividends you would have received as a shareholder of Keppel DC REIT in the past 12 months with the calculator below.

Related links:

- Keppel DC REIT latest valuation, share price and analysis

- Keppel DC REIT dividend history and forecast

#2 - Mapletree Industrial Trust (SGX: ME8U)

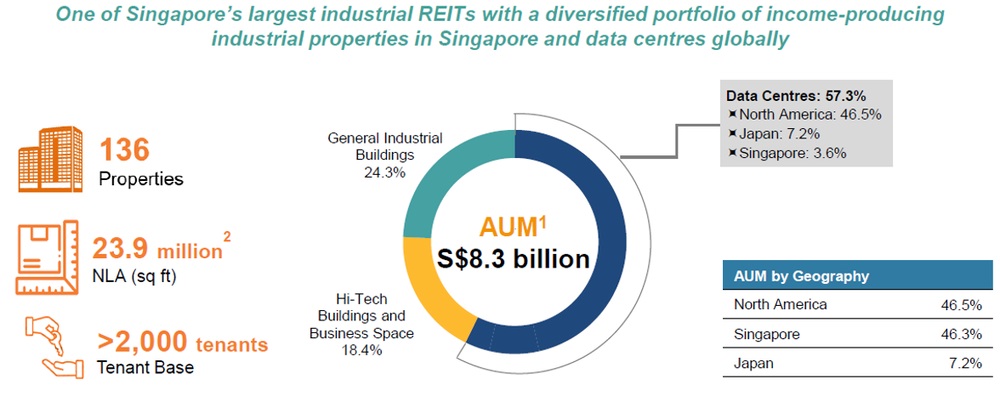

Mapletree Industrial Trust, or MIT, is not a pure data centre REIT.

It owns a diversified portfolio of industrial properties and data centres across Singapore, North America and Japan.

As at 31 March 2026, MIT had 136 properties, with assets under management of about S$8.3 billion. Data centres made up 57.3% of its AUM which is now its largest portfolio segment.

This gives MIT meaningful exposure to the data centre sector, while still retaining a diversified income base across industrial properties.

MIT owns 55 data centres across North America, with 8.3 million sq ft of net lettable area. The North American data centre portfolio had an occupancy rate of 86.1% and a WALE of 6.3 years as at 31 March 2026.

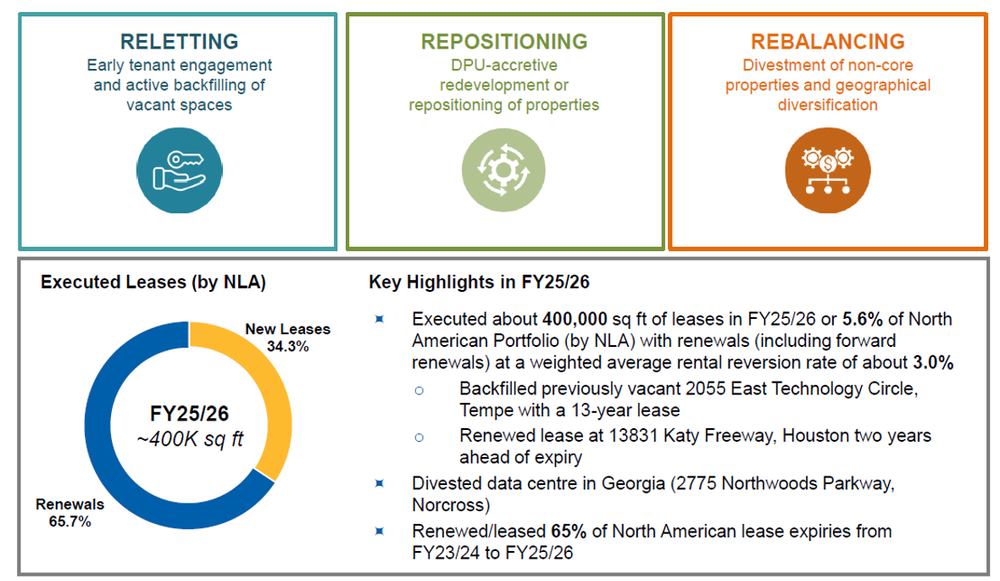

The key development for MIT is not just its size, but how it is reshaping its data centre portfolio.

Management has said that it is targeting selective divestments of S$500 million to S$600 million in North America.

The aim is to rebalance the data centre portfolio towards cloud, hyperscale and colocation providers, and redeploy capital into higher-quality data centres in key markets across Asia Pacific and Europe.

This is important because not all data centre assets benefit from the AI boom equally.

Older or lower-specification assets may face leasing pressure if they cannot support higher power density, cooling needs or large-scale cloud deployments.

MIT’s latest update showed both progress and pressure.

The REIT executed about 400,000 sq ft of leases in FY25/26, or 5.6% of its North American portfolio by net lettable area. Renewals, including forward renewals, achieved a weighted average rental reversion of about 3.0%.

It also backfilled previously vacant space at 2055 East Technology Circle in Tempe with a 13-year lease, and renewed a lease at 13831 Katy Freeway in Houston two years ahead of expiry.

After the quarter, MIT secured a replacement tenant from the aerospace technology industry for 2301 West 120th Street in Hawthorne on a 10-year lease with annual rental escalations.

These leasing wins help to reduce near-term vacancy risk, although the North American portfolio remains a key area to watch.

For MIT, the AI and data centre angle is therefore more mixed than Keppel DC REIT.

It offers meaningful data centre exposure, but investors also need to watch how quickly management can recycle capital, improve occupancy and upgrade the portfolio mix towards stronger demand areas.

This is also reflected in MIT’s latest DPU trend.

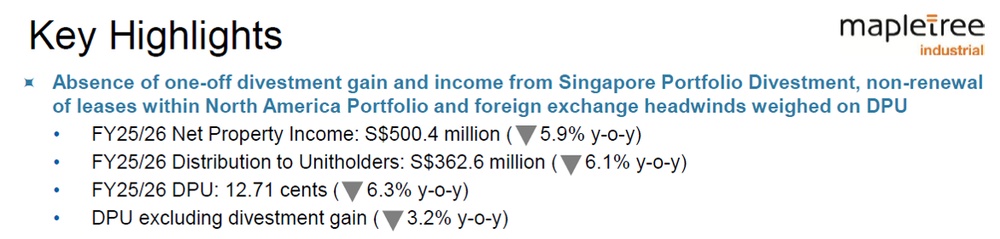

For FY25/26, Mapletree Industrial Trust reported DPU of 12.71 Singapore cents, down 6.3% year on year, weighed down by the absence of income from divested Singapore properties, non-renewal of leases in its North American portfolio and foreign exchange headwinds.

Based on its unit price of S$1.92 as of 9 June 2026, Mapletree Industrial Trust offers a forward dividend yield of 6.8%.

That said, MIT’s balance sheet remains relatively healthy, with aggregate leverage at 37.5% as at 31 March 2026. This includes the drawdown of debt to redeem existing perpetual securities.

For MIT, I would watch whether occupancy stabilises, whether its North American data centre portfolio improves, and whether borrowing costs remain manageable.

Find out how much dividends you would have received as a shareholder of Mapletree Industrial Trust in the past 12 months with the calculator below.

Related links:

- Mapletree Industrial Trust latest valuation, share price and analysis

- Mapletree Industrial Trust dividend history and forecast

#3- Digital Core REIT (SGX: DCRU)

Digital Core REIT is another pure-play data centre REIT listed in Singapore.

It is sponsored by Digital Realty and owns a portfolio of data centres across markets such as the US, Canada, Germany and Japan.

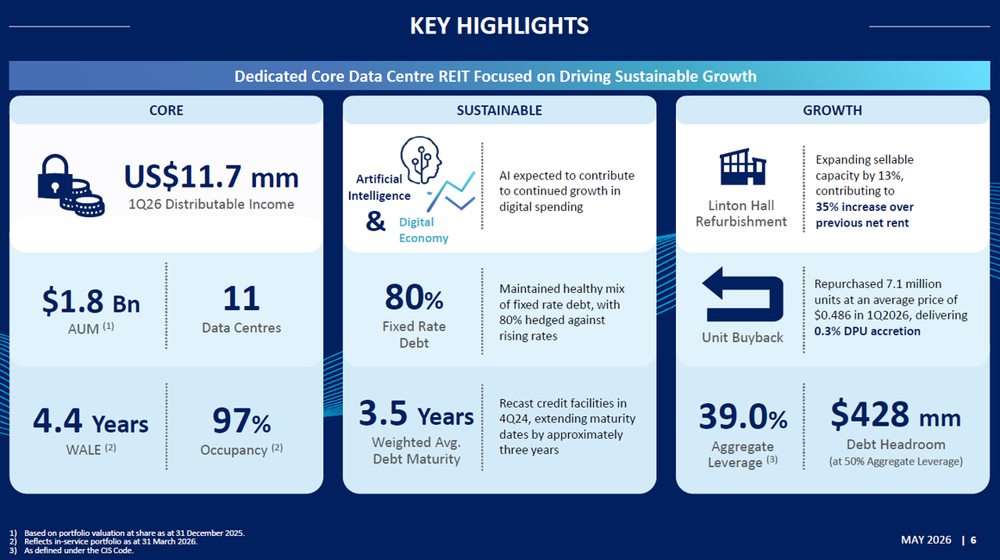

As at 31 March 2026, Digital Core REIT had 11 data centres, assets under management of US$1.8 billion, and portfolio occupancy of 97%.

Its WALE stood at 4.4 years, while 79% of its cash flows came from investment-grade customers.

This gives the REIT a fairly resilient starting point, although it has gone through a more challenging period because of tenant-related issues in the past.

The latest update offers some signs of improvement.

In 1Q 2026, Digital Core REIT signed new and renewal leases representing US$3 million of annualised rent, with cash rental reversion of 44%.

One of the more important data centre-related developments is the Linton Hall refurbishment.

The REIT said the refurbishment would expand sellable capacity by 13%, contributing to a 35% increase over previous net rent.

This is meaningful because data centre growth is not only about owning more assets.

Existing facilities may also need to be upgraded to support higher power density, better cooling and the resilience required by cloud and AI workloads.

Digital Core REIT’s sponsor platform could also be an important longer-term advantage.

Digital Realty is one of the largest global data centre operators, and Digital Core REIT has a potential acquisition pipeline through its sponsor.

However, future acquisitions would still need to be funded prudently and be accretive to DPU.

For FY2025, Digital Core REIT reported DPU of 3.60 US cents, up 15% year on year, with recent leasing momentum and the Linton Hall refurbishment offering signs of improvement in its portfolio.

Based on its unit price of US$0.485 as of 9 June 2026, Digital Core REIT offers a forward dividend yield of 8.2%.

This is the highest yield among the four REITs in this list. However, I would not look at the yield in isolation.

The data centre fundamentals appear supportive, but investors would still need to watch tenant concentration, gearing, refinancing costs and whether leasing momentum translates into more stable distributions.

Find out how much dividends you would have received as a shareholder of Digital Core REIT in the past 12 months with the calculator below.

Related links:

- Digital Core REIT latest valuation, share price and analysis

- Digital Core REIT dividend history and forecast

#4 - NTT DC REIT (SGX: NTDU)

NTT DC REIT is the newest REIT in this list. The REIT was listed on the SGX Mainboard in July 2025 and invests in stabilised, income-producing data centre assets globally.

It is backed by NTT, which is one of the largest data centre providers globally outside China.

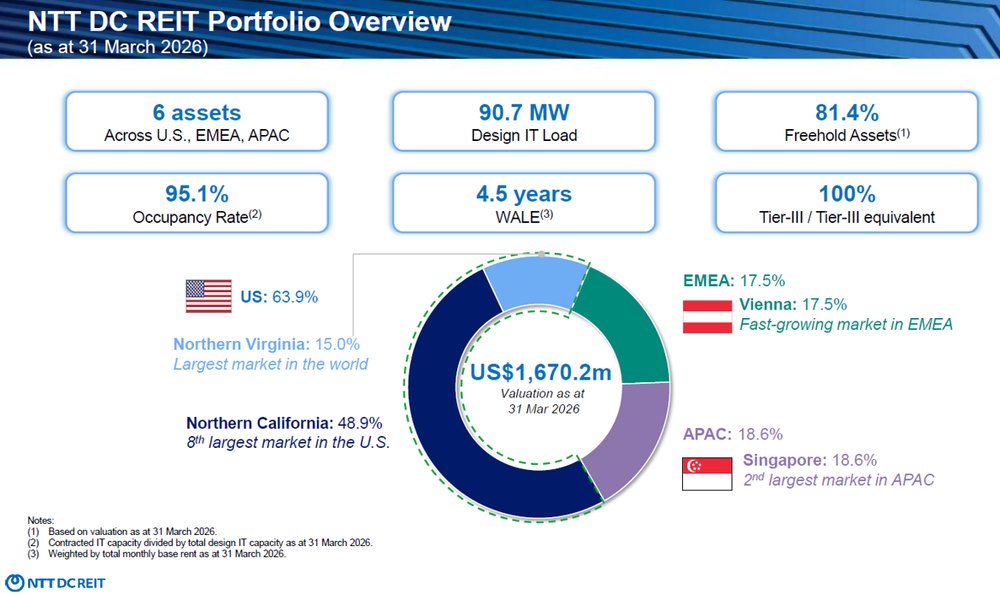

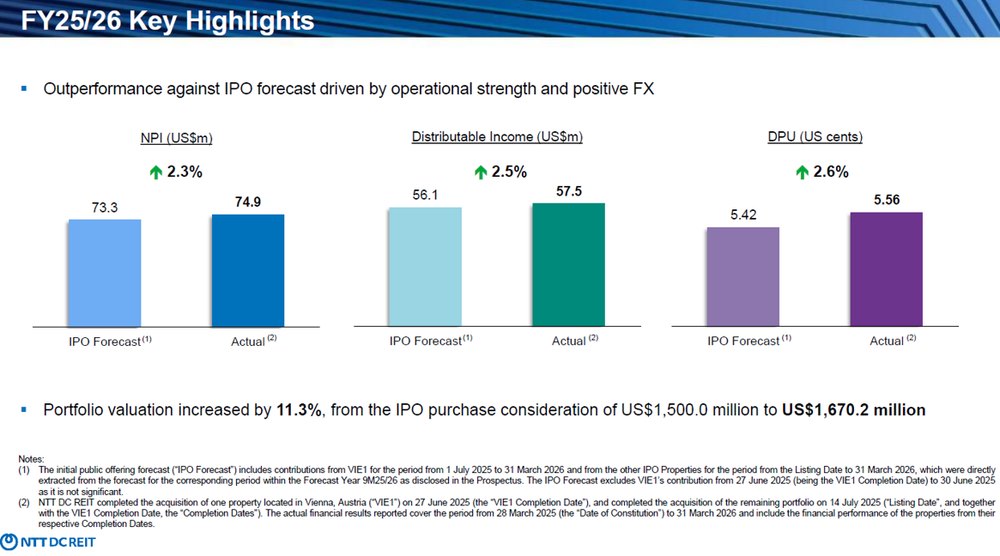

As at 31 March 2026, NTT DC REIT’s portfolio was valued at about US$1.67 billion, up 11.3% from its IPO purchase consideration. Its portfolio consists of six data centre assets across the US, Austria and Singapore.

The portfolio has 90.7 MW of design IT load, 95.1% occupancy, 98.5% committed occupancy and a WALE of 4.5 years.

All of its assets are Tier-III or Tier-III equivalent, which is important because enterprise and hyperscale customers typically require high levels of resilience and uptime.

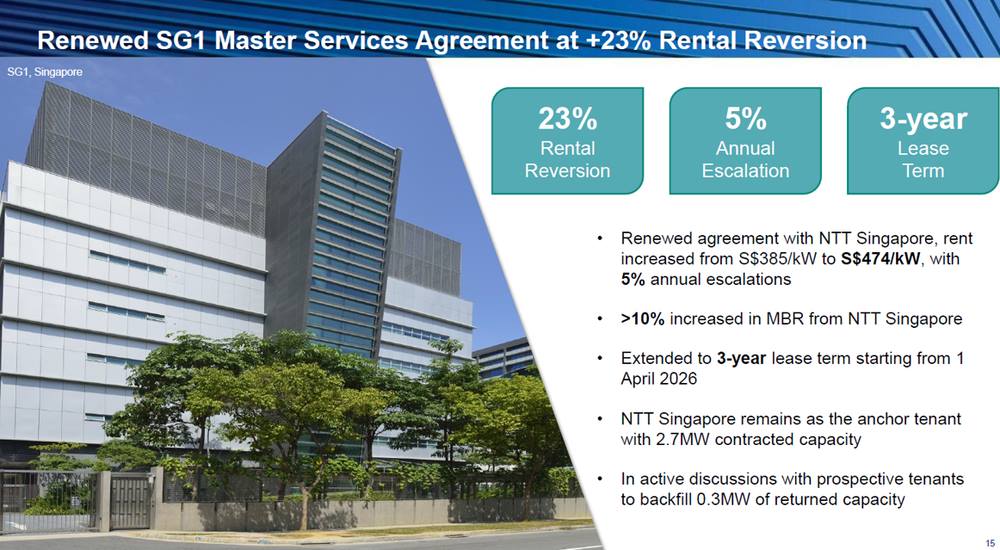

One of the key developments was the renewal of the SG1 Master Services Agreement with NTT Singapore.

The renewed agreement secured a 23% rental uplift, with rent rising from S$385 per kW to S$474 per kW.

The renewed lease also includes 5% annual escalations and a three-year lease term from 1 April 2026.

NTT Singapore remains the anchor tenant at SG1 with 2.7 MW of contracted capacity, while management is in active discussions to backfill 0.3 MW of returned capacity.

This is a useful example of how demand for data centre capacity can translate into higher rents when leases are renewed.

Across the portfolio, NTT DC REIT achieved rent reversion of 8.5% for FY25/26, or 13.7% including the NTT Singapore renewal at SG1.

The portfolio is also positioned across several key data centre markets.

Northern California accounted for 48.9% of portfolio valuation, Northern Virginia accounted for 15.0%, Singapore accounted for 18.6%, and Vienna accounted for 17.5%.

The Singapore exposure is notable because Singapore remains one of the largest data centre markets in Asia Pacific, while Northern Virginia remains the largest data centre market globally.

NTT DC REIT also benefits from sponsor backing.

The REIT has said that it is looking to capitalise on its sponsor’s right-of-first-refusal pipeline to pursue accretive acquisitions and strengthen portfolio quality over time.

The main watch point is that NTT DC REIT has a short listed track record.

Its first set of results came in above IPO forecast, but investors have not yet seen how the REIT performs across a full market cycle.

NTT DC REIT delivered its maiden DPU of 5.56 US cents for FY25/26, which was 2.6% above its IPO forecast.

Based on its unit price of US$0.96 as of 9 June 2026, NTT DC REIT offers a forward dividend yield of 8.1%.

However, the main thing to note is that NTT DC REIT still has a shorter listed track record compared to the other REITs.

For investors, this means there are fewer years of public market data to assess how the REIT performs across different market cycles.

For NTT DC REIT, I would watch whether future acquisitions are DPU-accretive, whether the SG1 backfilling progresses well, and whether rental reversions remain positive across the portfolio.

Find out how much dividends you would have received as a shareholder of NTT DC REIT in the past 12 months with the calculator below.

Related links:

What would Beansprout do?

Data centre REITs may benefit from stronger demand from cloud and AI workloads, but the more important question is whether this demand can translate into stable occupancy, positive rental reversions and sustainable DPU.

For income investors, WALE is also worth watching as it gives some visibility on future rental income. Among the four, Keppel DC REIT has the longest comparable portfolio WALE at 6.5 years, while MIT’s North American data centre portfolio also has a fairly long WALE of 6.3 years.

However, a longer WALE should still be assessed together with tenant quality, occupancy and balance sheet strength.

Among the four, Keppel DC REIT has the clearest DPU growth trend, with DPU rising 13.2% year-on-year in 1Q 2026 and portfolio reversion of about 51%. However, its lower dividend yield of 4.4% may suggest that its stronger portfolio quality may already be reflected in the price. Learn more about Keppel DC REIT here.

Mapletree Industrial Trust offers a higher yield and the largest AUM base, but its DPU fell 6.3% in FY25/26. While its data centre exposure is meaningful, I would watch whether its North American portfolio can stabilise and whether the planned portfolio rebalancing can improve the quality of its data centre assets over time. Learn more about Mapletree Industrial Trust here.

Digital Core REIT and NTT DC REIT offer higher forward dividend yields of 8.2% and 8.1% respectively, but I would treat them differently.

Digital Core REIT looks more like a recovery income idea. Its leasing momentum and Linton Hall refurbishment are encouraging, but tenant concentration, gearing and refinancing costs remain key risks. Learn more about Digital Core REIT here.

NTT DC REIT has delivered an encouraging first set of results, with its SG1 renewal securing a 23% rental uplift and 5% annual escalations. However, it is still newly listed, so there is limited public track record to assess how resilient its DPU might be across different market cycles.Learn more about NTT DC REIT here.

Overall, I would not simply pick the REIT with the highest yield.

For a data centre REIT to work well in the Income Pot with Beansprout's four pots of wealth, I would want to see a combination of strong tenant demand, healthy occupancy, reasonable WALE, manageable gearing and a DPU that can be sustained over time. Learn more about how I invest with clarity with Beansprout's four pots of wealth here.

| REIT | The good | Key risks |

| Keppel DC REIT |

|

|

| Mapletree Industrial Trust |

|

|

| Digital Core REIT |

|

|

| NTT DC REIT |

|

|

To screen for Singapore REITs with lowest price-to-book valuation or highest dividend yield, check out our best Singapore REIT screener.

If you prefer diversification without picking individual REITs, you can also gain exposure through Singapore REIT ETFs.

If you are new to investing in Singapore REITs, you can start to learn more about Singapore REITs here.

Which Singapore data centre REIT are you watching as the AI boom continues? Share your thoughts in the comments below or join the discussion in our Telegram group!

Planning to invest in Singapore REITs? Compare the best Singapore brokerages to find the right trading platform, and see the latest promotions and sign-up rewards available.

Follow Beansprout on Telegram, Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

1 comments

- CHAN CHOON YUAN • 10 Jun 2026 09:12 AM