3 Singapore REITs with dividend yields of above 6% (April 2026)

REITs

By Gerald Wong, CFA • 15 Apr 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

We look at three Singapore REITs with dividend yields above 6% in April 2026. We assess whether their dividends are sustainable for income investors.

What happened?

Singapore REITs have recovered slightly after the March sell-off.

Last month, we covered 3 Singapore REITs with dividend yields above 6%, as the pullback pushed yields higher.

We also looked at whether the weakness in the REITs sector had created a buying opportunity.

Since then, the iEdge S-REIT Index has rebounded from its low in March.

That made me wonder which Singapore-listed REITs still offer yields above 6%, and whether those payouts are backed by resilient operating performance and balance sheets.

In this article, we look at three REITs that still offer yields above 6% in April 2026 and assess whether their yields are sustainable before adding them to our portfolio for income.

#1 - AIMS APAC REIT (SGX: O5RU)

AIMS APAC REIT is an industrial REIT with a portfolio anchored by Singapore assets and complemented by Australian exposure.

As at 31 December 2025, its Singapore portfolio accounted for 76.4% of gross rental income (GRI), while the rest was supported by Australian assets with longer lease profiles.

AIMS APAC REIT’s latest distribution growth was supported by relatively steady operating performance.

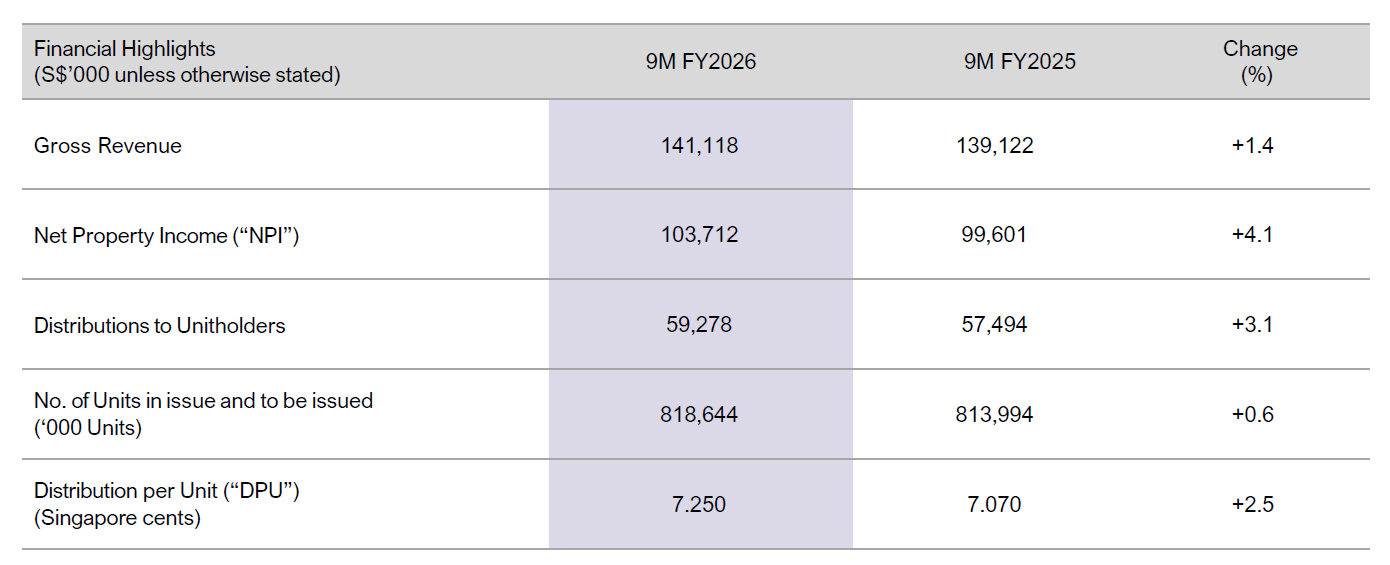

In 9M FY2026, gross revenue increased 1.4% to S$141.1 million, while net property income rose 4.1% to S$103.7 million, helped by higher rental reversions and lower property expenses.

Operationally, the leasing picture was also encouraging.

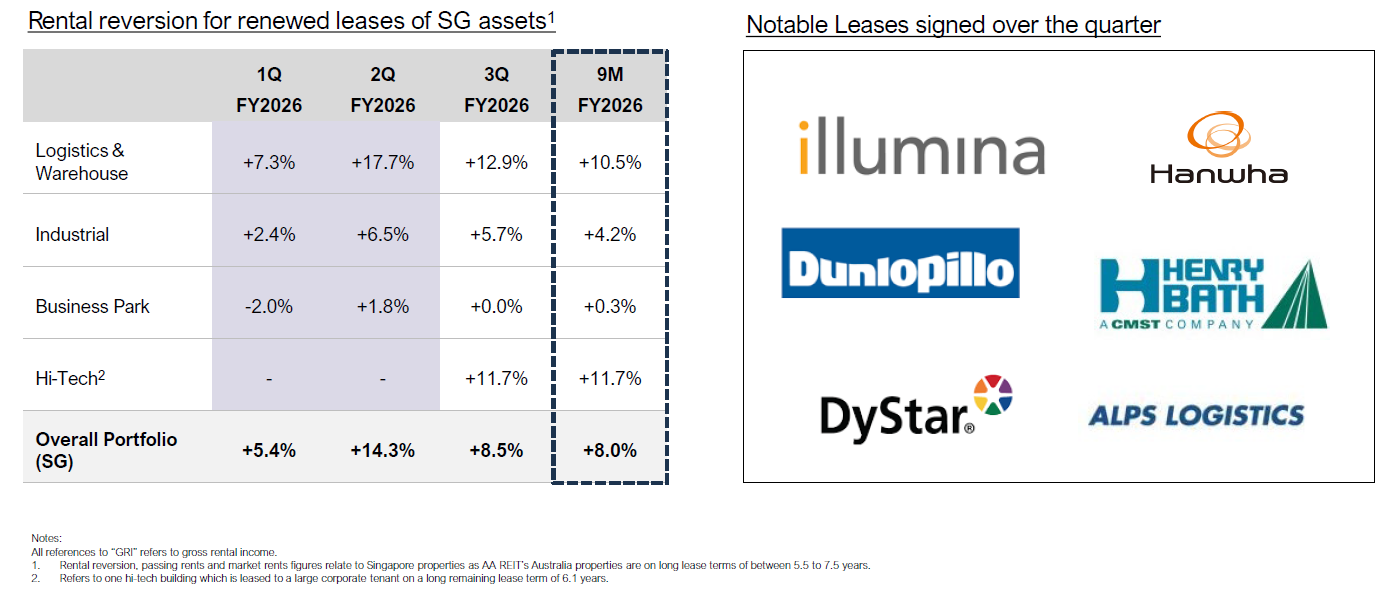

AIMS APAC REIT executed 25 new and 49 renewal leases covering 161,420 square metres, representing 20.5% of portfolio net lettable area, and achieved positive rental reversions of 8.0% in 9M FY2026, led by logistics and warehouse assets at 10.5%.

Portfolio occupancy improved to 95.4% as at 31 December 2025, or 96.6% including committed leases, up from 93.3% at the previous quarter.

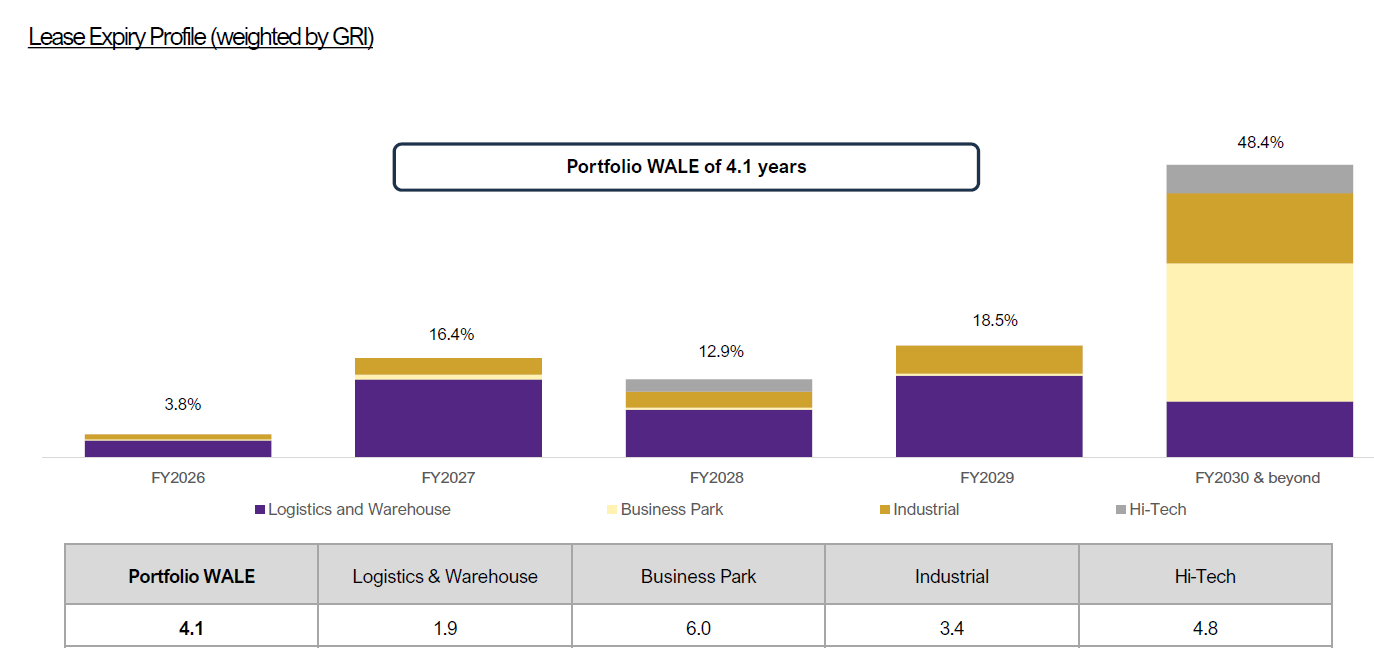

Weighted average lease expiry remained steady at 4.1 years.

The tenant base also remained diversified and defensive, with 188 tenants and 82.7% of gross rental income coming from essential and defensive industries.

AIMS APAC REIT’s balance sheet also looks relatively steady.

Aggregate leverage stood at 36.6% as at 31 December 2025, with no debt refinancing requirement until FY2027.

Its blended cost of debt improved to 4.1%, and the S$150 million perpetual securities issued after quarter end should support a lower cost of capital and greater financial flexibility.

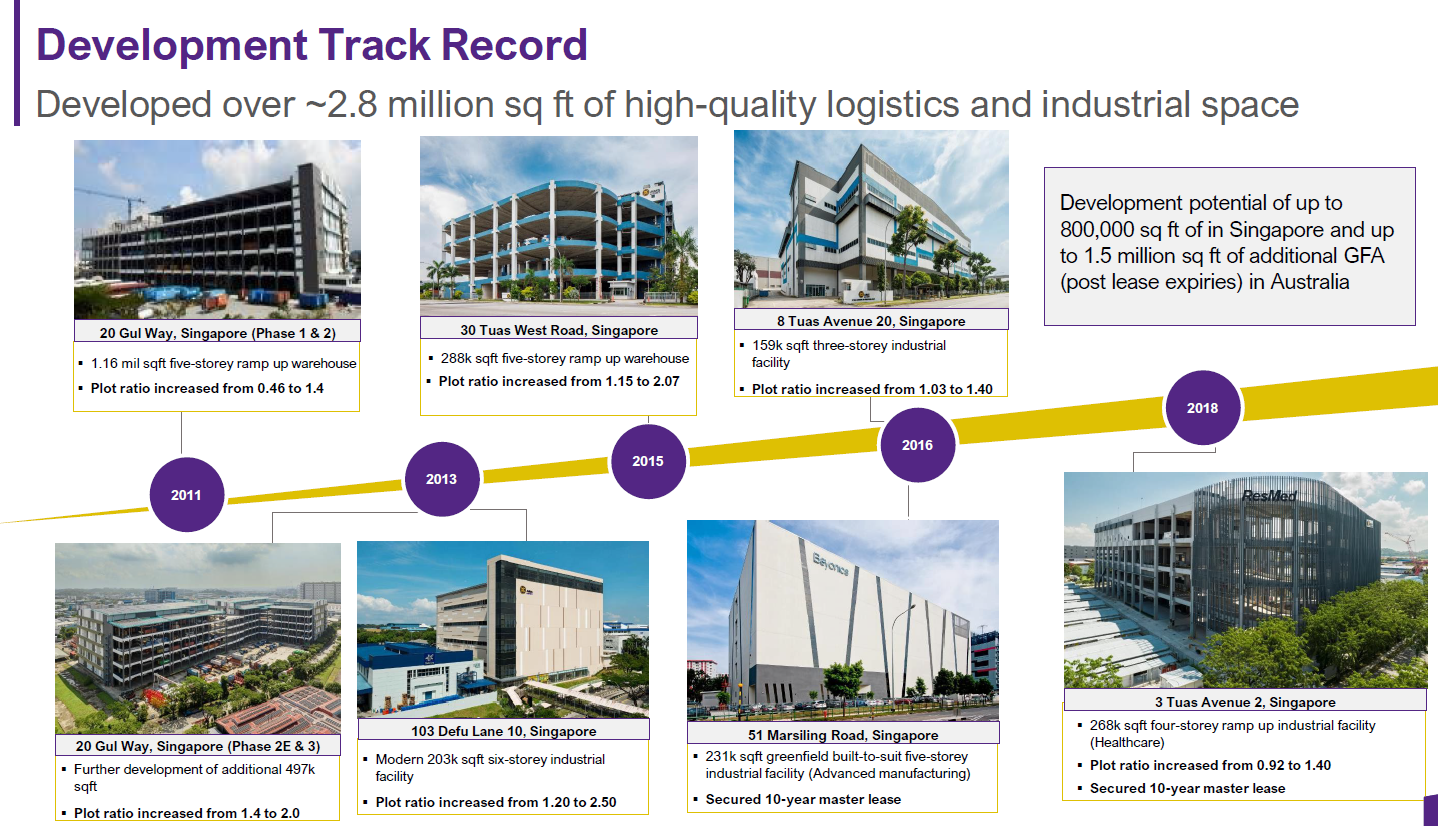

Beyond the current portfolio, the management is mindful of accretive acquisition to drive stronger growth.

They highlighted embedded growth optionality through asset enhancement initiatives and redevelopment.

It estimates further potential of up to about 800,000 square feet in Singapore and around 1.5 million square feet of additional GFA in Australia after lease expiries.This gives it another avenue for growth beyond acquisitions.

For 9M FY2026, AIMS APAC REIT reported DPU of 7.25 Singapore cents, up 2.5% year on year, supported by positive rental reversions, higher occupancy and lower property expenses.

Based on its unit price of S$1.50 as of 14 April 2026, AIMS APAC REIT offers a forward dividend yield of 6.7%.

Find out how much dividends you would have received as a shareholder of AIMS APAC REIT in the past 12 months with the calculator below.

Related links:

- AIMS APAC REIT share price history and share price target

- AIMS APAC REIT dividend history and forecast

- AIMS APAC REIT - Consistent DPU growth with resilient portfolio

#2 - Digital Core REIT (SGX: DCRU)

Digital Core REIT offers exposure to data centre assets, giving it a specialised earnings profile than a traditional office, retail or industrial REIT.

Its latest operating performance was also stronger.

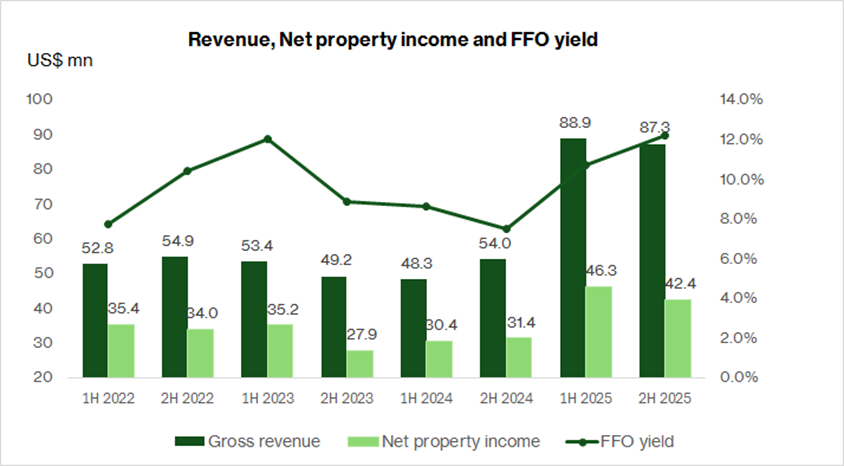

For 2H2025, total property income rose 2.0% year on year to S$145.1 million.

Revenue increased 61.6% year on year to US$87.3 million, while net property income grew 35.1% to S$42.4 million, driven mainly by newly acquired properties, stronger leasing activity and the consolidation of the Frankfurt facility.

After spending much of the past year stabilising operations, management has started to pivot back towards growth, with plans to double its asset base over three years through capital recycling and sponsor-backed opportunities.

This comes as the structural backdrop for data centres remains supportive, helped by AI and cloud demand.

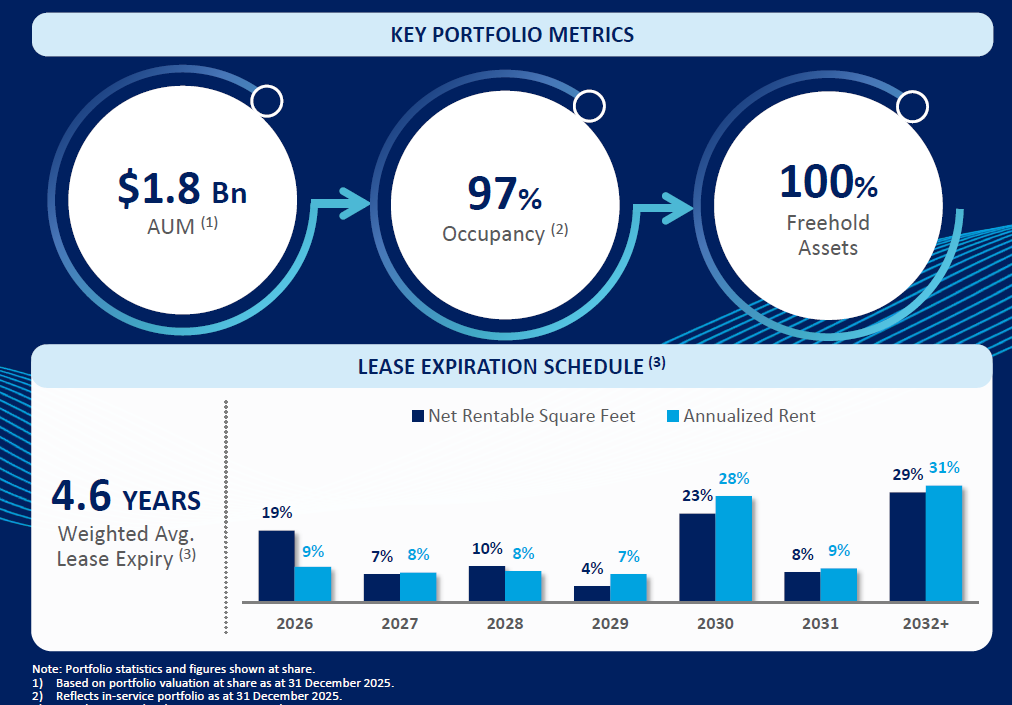

As at 31 December 2025, committed occupancy remained high at 97%, weighted average lease expiry (WALE) stood at 4.6 years.

Assets under management grew 12.5% year on year to US$1.83 billion, partly reflecting the acquired 20% stake in Digital Osaka 3 and improved leasing activity across the portfolio.

The REIT also achieved strong rental reversions of 31% in FY2025.

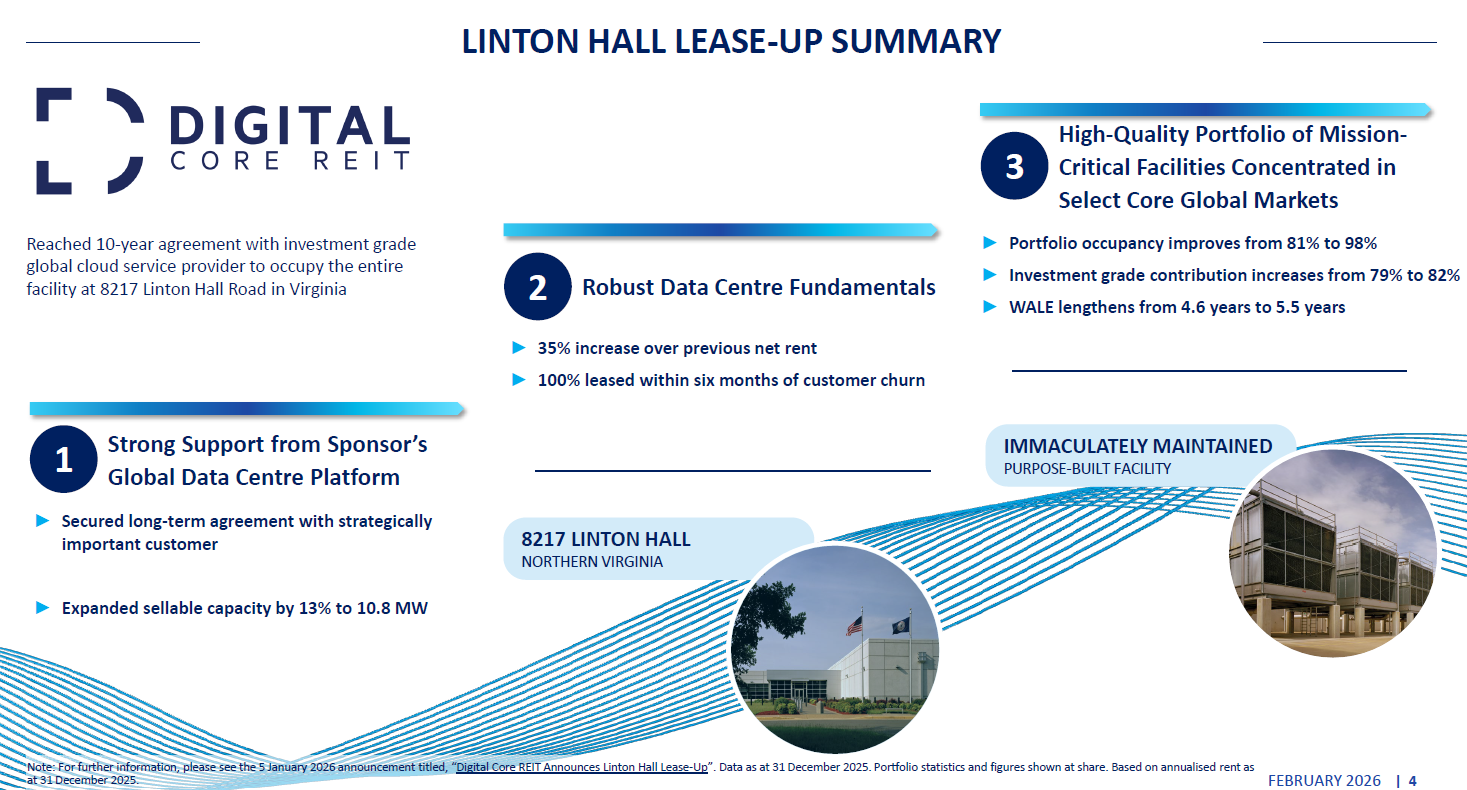

One key development and clearest near-term catalyst was progress at Linton Hall.

Digital Core REIT secured a new 10-year lease with an investment-grade global cloud service provider, which is expected to contribute about US$13.3 million in annualised net property income at the REIT’s 90% share.

Upon commencement, this is expected to lift portfolio occupancy from 81% to 98% and extend WALE from 4.7 years to 5.7 years, improving earnings visibility meaningfully.

Its balance sheet also remains relatively healthy.

Aggregate leverage increased to 37.1% as at 31 December 2025 from 34.0% a year earlier, but cost of debt declined to 3.5% from 3.9%.

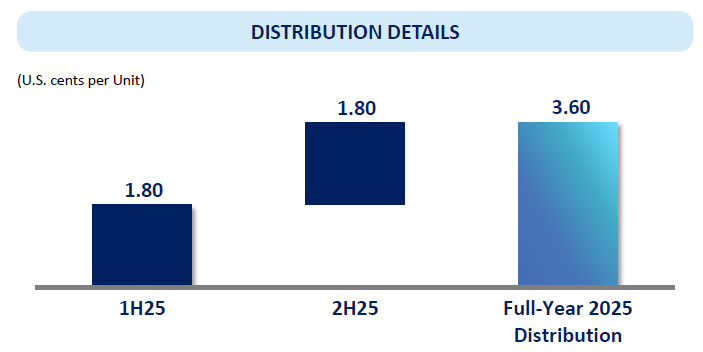

For FY2025, Digital Core REIT’s DPU was stable at 3.60 US cents, unchanged year on year, despite some temporary vacancy and downtime during the year.

Based on its unit price of US$0.520 as of 14 April 2026, Digital Core REIT offers a forward dividend yield of 7.7%.

Find out how much dividends you would have received as a shareholder of Digital Core REIT in the past 12 months with the calculator below.

#3 - Stoneweg Europe Stapled Trust (SGX: SET)

Stoneweg Europe Stapled Trust is one of the few Singapore-listed REITs and stapled trusts offering direct exposure to commercial real estate in Western Europe and the Nordics.

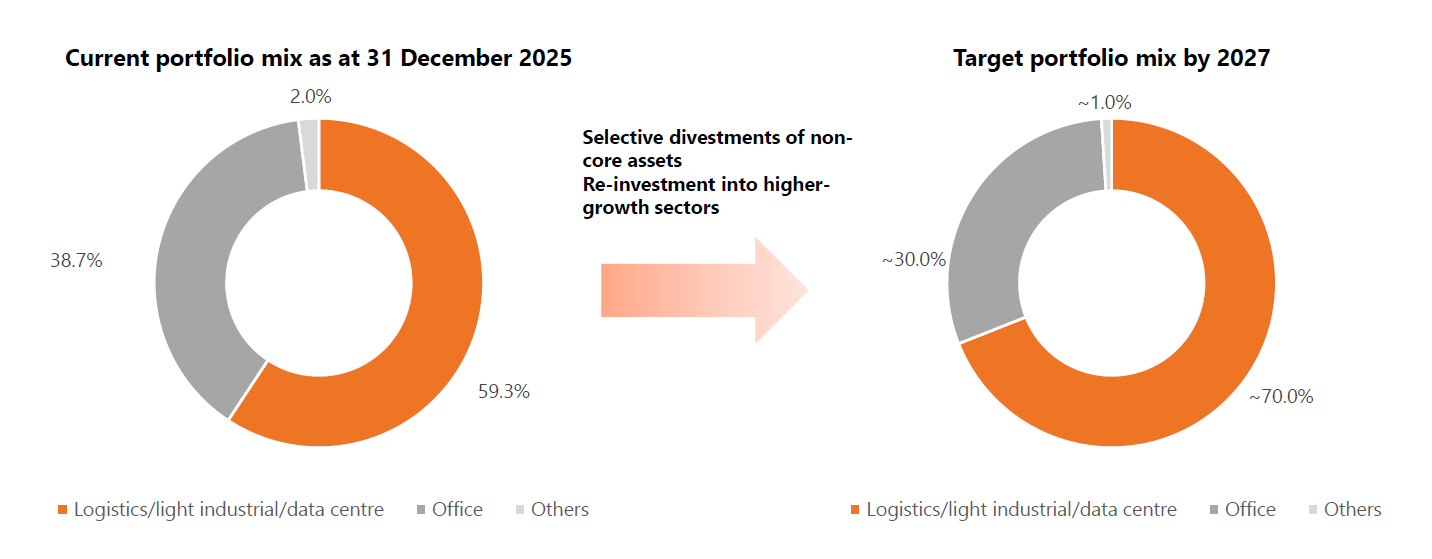

The management is actively repositioning the portfolio away from legacy office assets and towards logistics, light industrial and data centres.

As at 31 December 2025, it had a €2.16 billion portfolio across 96 predominantly freehold properties, with about 60% already in these newer-economy segments. Management has also set a medium-term target to increase this weighting further.

That shift is already showing up more clearly in its capital allocation.

In FY2025, Stoneweg sold eight properties for €120 million, including its entire Slovakia portfolio, and management is aiming to raise exposure to logistics, light industrial and data centres from 59% to closer to 70% by 2027.

It has also committed a total of €100 million into AiOnX, the sponsor’s data centre platform.

Based on its €2.16 billion portfolio, that works out to about 4.6% of assets under management, which is still manageable in size but large enough to give the trust a meaningful foothold in digital infrastructure growth.

Its latest operating performance was still fairly resilient.

In FY2025, revenue rose 0.8% year on year to €214.6 million, while net property income increased 2.5% to €134.4 million. On a like-for-like basis, net property income grew 5.0%, supported by redevelopments and stronger contributions from logistics and light industrial assets.

Portfolio occupancy stood at 92.6%, while WALE was 4.9 years, which remains relatively long for the segment.

The main drag remains financing costs.

Aggregate leverage stood at 42.4% as at 31 December 2025, although 94% of debt is fixed or hedged and there are no debt maturities until 2030.

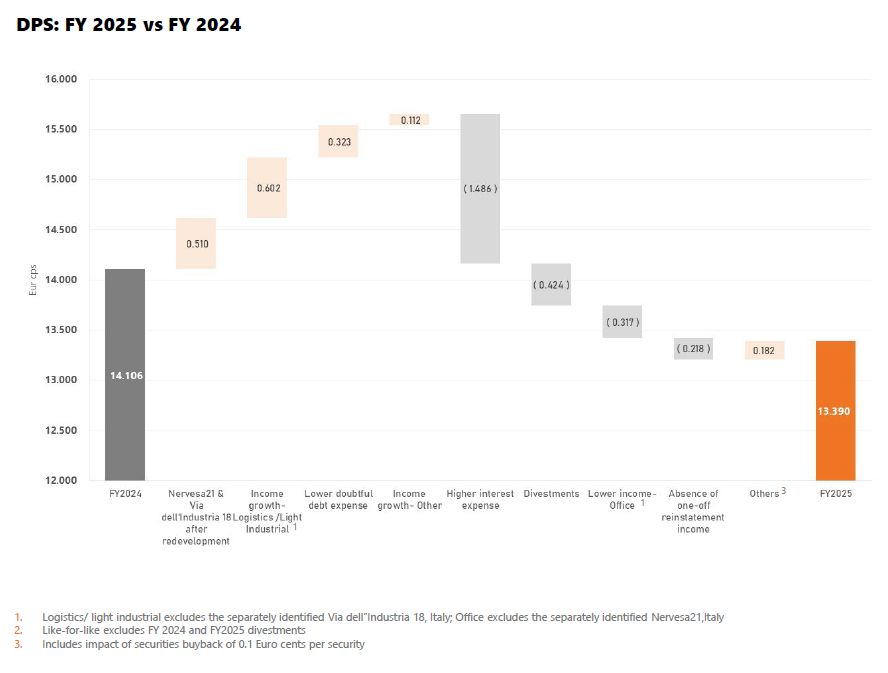

FY2025 distributable income fell 5.7% year on year to €74.8 million, while distribution per stapled security declined 5.1% year on year to 13.39 euro cents as interest expense rose 15.2% to €44.0 million.

Based on its unit price of S$1.50 as of 14 April 2026, Stoneweg Europe Stapled Trust offers a forward dividend yield of 8.7%.

Management has guided that FY2026 DPS is expected to be broadly similar to FY2025.

Find out how much dividends you would have received as a shareholder of Stoneweg Europe Stapled Trust in the past 12 months with the calculator below.

Related links:

- Stoneweg European Stapled Trust share price history and share price target

- Stoneweg Europe Stapled Trust history and dividend forecasts

- Stoneweg Europe Stapled Trust: Positioning for Income and Growth

- kopi-C with Stoneweg Europe Stapled Trust CEO: Europe's real estate recovery, and the management discipline behind it

What would Beansprout do?

All three REITs still offer yields above 6% in April 2026, although the strength of support behind those payouts appears to vary.

If I were looking for a more resilient income name today, I would lean towards AIMS APAC REIT. Its payout appears better supported by steadier operating performance, healthy occupancy, and a balance sheet that looks more manageable. Learn more about AIMS APAC REIT here.

Digital Core REIT would also stand out to me if I were comfortable taking on slightly more execution risk in exchange for a mix of income and growth. Its longer lease visibility, along with structural support from AI-driven demand for data centres, makes it an interesting option. Learn more about Digital Core REIT here.

Stoneweg Europe Stapled Trust offers the highest yield among the three, but its payout may be dependent on its continued ability to recycle capital out of legacy office assets and shift towards new economy assets. Learn more about Stoneweg Europe Stapled Trust here.

| REIT | The good | Key risks |

| Stoneweg Europe Stapled Trust |

|

|

| AIMS APAC REIT |

|

|

| Digital Core REIT |

|

|

One final point I would keep in mind is that REIT yields may change quickly when borrowing costs rise or when capital raisings dilute distributions.

Because of that, I will still consider how I can build a diversified income portfolio beyond Singapore REITs to grow my income. Learn how to build a more dependable stream of passive income that can hold up across cycles here.

To screen for Singapore REITs with lowest price-to-book valuation or highest dividend yield, check out our best Singapore REIT screener.

If you prefer diversification without picking individual REITs, you can also gain exposure through Singapore REIT ETFs.

If you are new to investing in Singapore REITs, you can start to learn more about Singapore REITs here.

Is there a Singapore REIT you are looking out for? Share with us in the comments below or in our Telegram group!

[Beansprout Exclusive Longbridge Promotion] Get bonus S$50 FairPrice voucher within 5 working days, plus 5% p.a. interest boost coupon (worth ~S$100) when you sign up for a Longbridge account via Beansprout. Plus, stand a chance to win S$150 CapitaVouchers weekly! Promo ends on 30 April 2026. Learn more about the Longbridge promo here.

Planning to invest in Singapore REITs? Compare the best Singapore brokerages to find the right trading platform, and see the latest promotions and sign-up rewards available.

Follow Beansprout on Telegram, Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments