3 Singapore REITs buying assets that could lift dividends

REITs

By Gerald Wong, CFA • 24 Apr 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

CapitaLand Integrated Commercial Trust (CICT), CapitaLand Ascendas REIT (CLAR), and Lendlease REIT recently made acquisitions. We break down what these deals may mean for their dividends.

What happened?

Singapore Real Estate Investment Trusts (S-REITs) continued their acquisition spree in 2026.

Recently, I have shared that CapitaLand Integrated Commercial Trust (CICT) agreed to buy Paragon, CapitaLand Ascendas REIT (CLAR) announced acquisitions in Singapore and Japan, and Lendlease REIT moved to take full ownership of PLQ Mall.

With Singapore REITs making acquisitions again, many income investors in the Beansprout Telegram group are asking what these asset purchases mean for unitholders.

In this article, I look at three Singapore REITs making acquisitions recently and what these deals may mean for distribution per unit (DPU) and dividend yields.

#1 – CapitaLand Integrated Commercial Trust (SGX: C38U)

CapitaLand Integrated Commercial Trust (CICT) announced two linked transactions in April 2026.

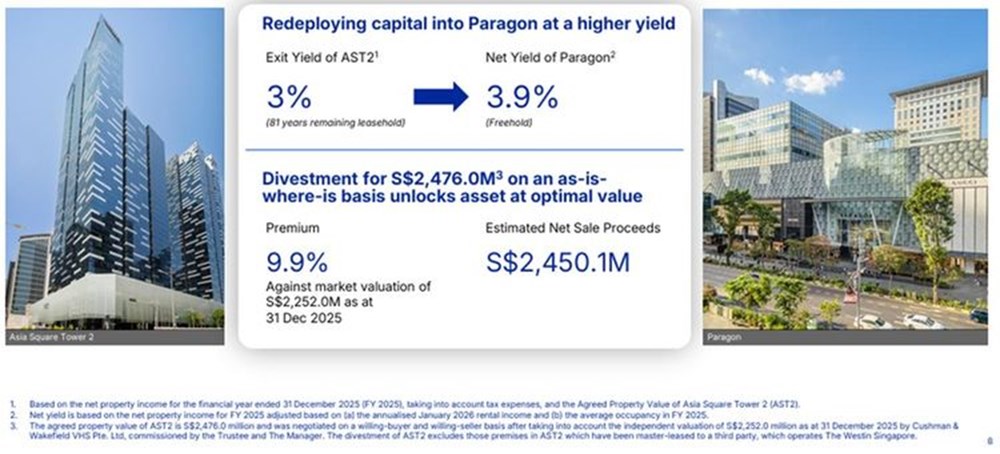

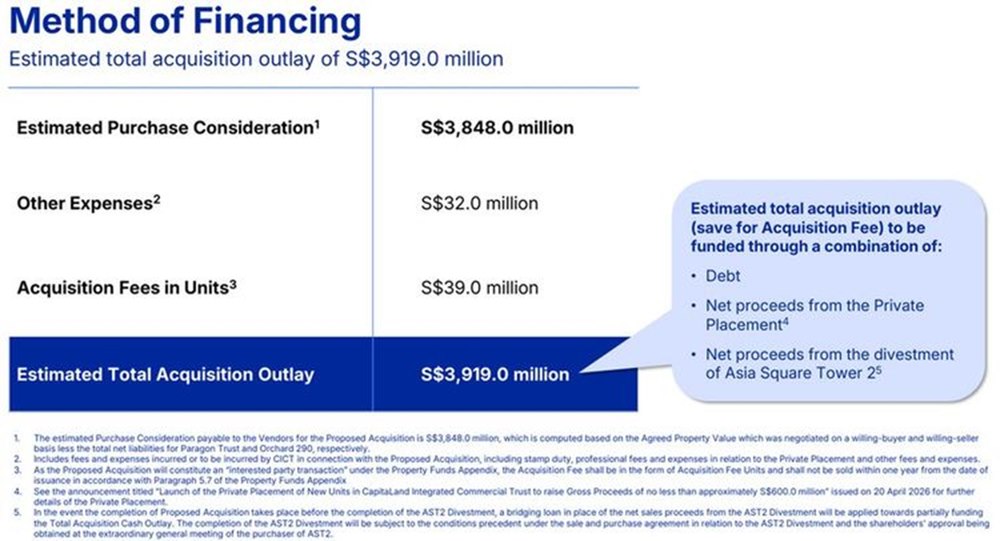

It agreed to acquire 100% of Paragon for S$3.9 billion and divest Asia Square Tower 2 for S$2.476 billion.

Paragon is a freehold integrated development along Orchard Road with retail, office and medical suites.

Asia Square Tower 2 is a leasehold office asset, so the transaction represents a capital recycling move into a larger Singapore asset with a higher entry yield of 3.9%, compared with the 3.0% exit yield on Asia Square Tower 2.

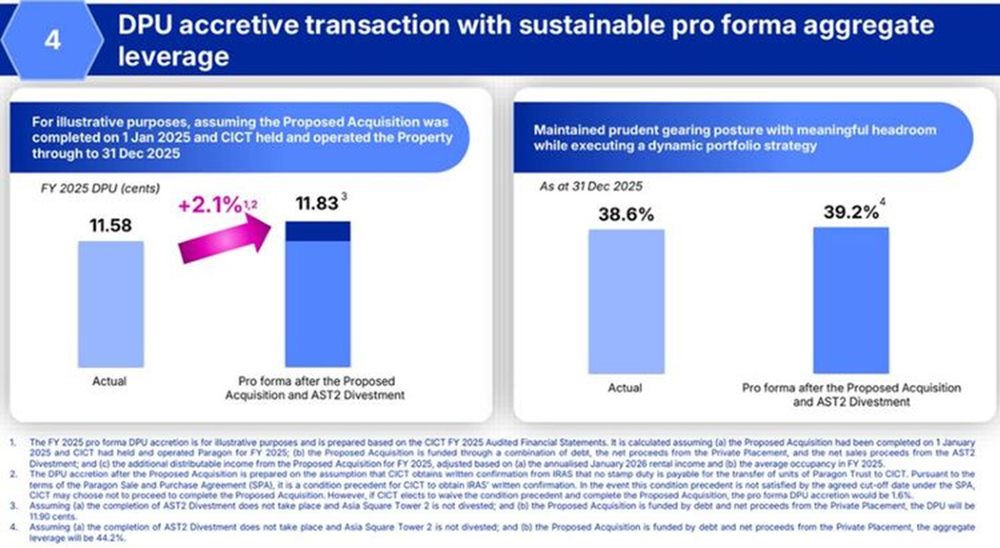

The transaction is expected to be DPU-accretive.

On a pro forma basis, CICT's FY2025 DPU would have increased from 11.58 cents to 11.83 cents, implying an uplift of about 2.1%.

The impact on the balance sheet also appears manageable.

Following the Paragon acquisition and Asia Square Tower 2 divestment, CICT’s pro forma aggregate leverage is expected to be 39.2%, and it has launched a private placement to raise at least S$600 million in new equity.

CICT trades at about 1.15x book as of 22 April 2026, which is above its historical average P/B of 1.03x.

It offers a forward dividend yield of about 4.8%, which is below its historical average dividend yield of 5.1%.

Find out how much dividends you would have received as a shareholder of CapitaLand Integrated Commercial Trust (CICT) in the past 12 months with the calculator below.

Related links:

- CapitaLand Integrated Commercial Trust (CICT) latest valuation, share price and analysis

- CapitaLand Integrated Commercial Trust (CICT) dividend history and dividend forecast

- CapitaLand Integrated Commercial Trust buys Paragon and sells Asia Square Tower 2

#2 – CapitaLand Ascendas REIT (SGX: A17U)

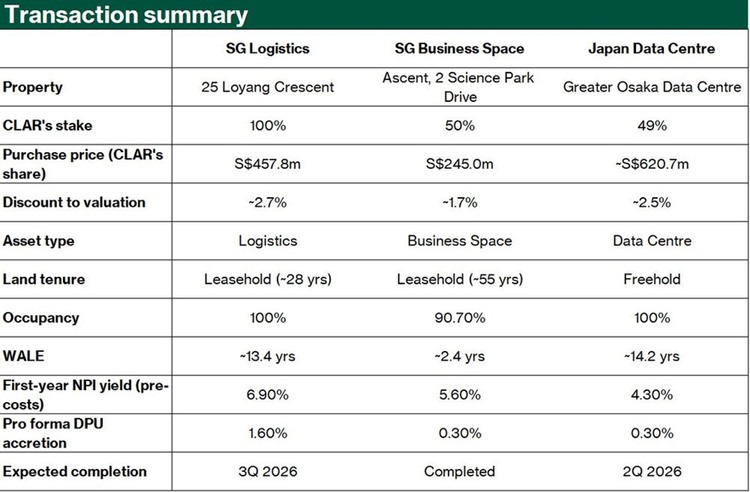

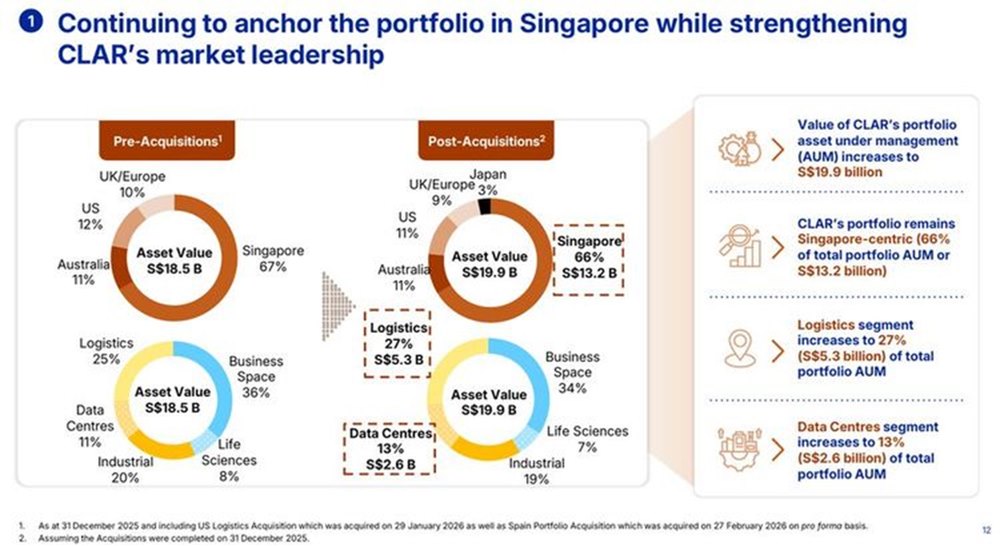

CapitaLand Ascendas REIT (CLAR) announced a S$1.4 billion acquisition exercise across Singapore and Japan.

It is acquiring 100% of 25 Loyang Crescent for S$504.2 million, 50% of Ascent at 2 Science Park Drive for S$245.0 million, and 49% of a Tier III hyperscale data centre in Greater Osaka for S$620.7 million.

These acquisitions expand CLAR’s exposure across logistics, business space and data centres.

They also keep Singapore as the core of the portfolio, with Singapore making up about 66% of total assets under management after the transactions.

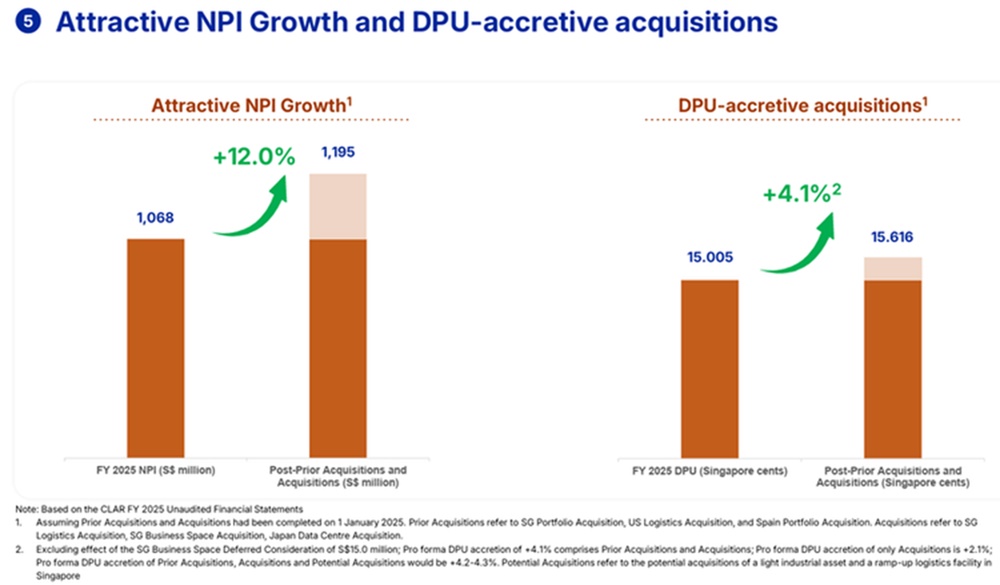

The transactions are expected to be DPU-accretive.

On a pro forma basis, CLAR's DPU accretion would be around 2.1%, while portfolio occupancy and weighted average lease expiry are expected to improve to 91.5% and 4.3 years respectively.

Including the acquisitions announced since October 2025, total pro forma DPU accretion rises to about 4.1%.

CLAR partly funded the acquisitions through an equity fund raising. Investor response was supportive, with the preferential offering oversubscribed overall as total applications reached 244.24% of the units available.

Following the transactions, pro forma aggregate leverage is expected to increase to 39.7% from 39.0% as at 31 December 2025.

CLAR trades at about 1.14x book as of 22 April 2026, which is below its historical average P/B of 1.24x.

It offers a forward dividend yield of about 6.0%, which is above its historical average dividend yield of 5.5%.

Find out how much dividends you would have received as a shareholder of CapitaLand Ascendas REIT in the past 12 months with the calculator below.

Related links:

- CapitaLand Ascendas REIT latest valuation, share price and analysis

- CapitaLand Ascendas REIT dividend history and forecast

- Capitaland Ascendas REIT invests S$1.4 billion in Singapore and Japan assets

- CapitaLand Ascendas REIT Preferential Offering - What should unitholders do?

#3 – Lendlease REIT (SGX: JYEU)

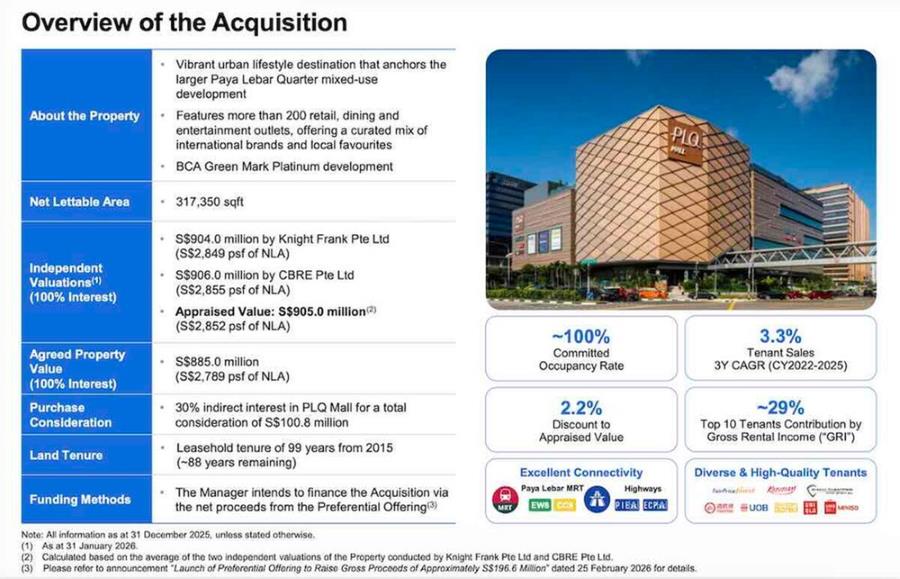

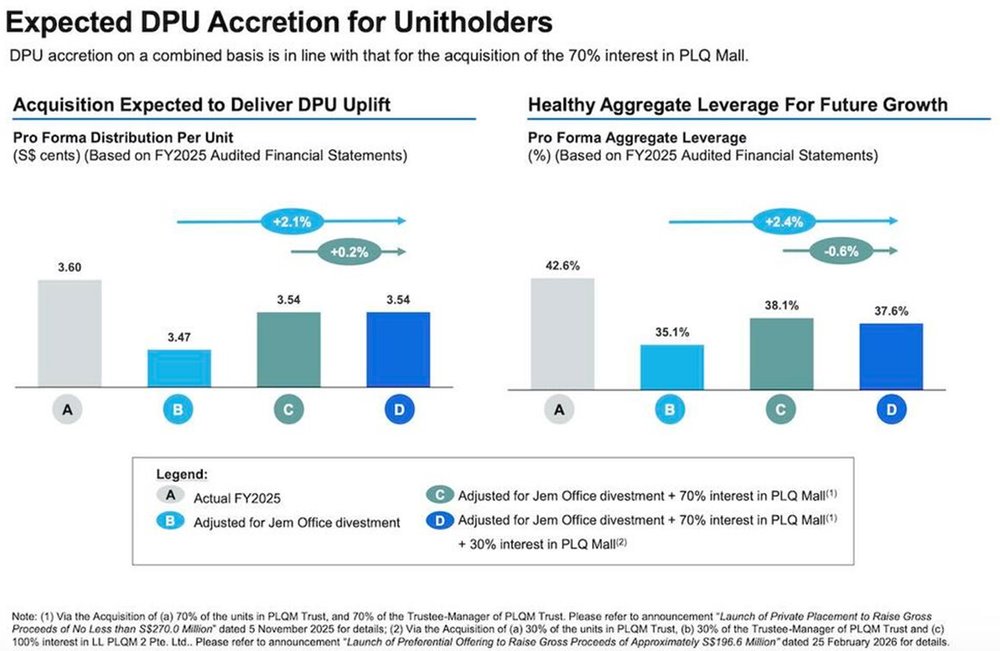

Lendlease REIT announced in February 2026 that it would acquire the remaining indirect 30% stake in PLQ Mall, taking its ownership to 100%.

The agreed property value of PLQ Mall was S$885.0 million, which was stated to be a 2.2% discount to appraised value.

The acquisition gives Lendlease REIT full ownership and control of one of its key Singapore retail assets.

Management also highlighted greater flexibility for asset initiatives and debt refinancing, with potential savings of about S$2 million per year in all-in debt costs.

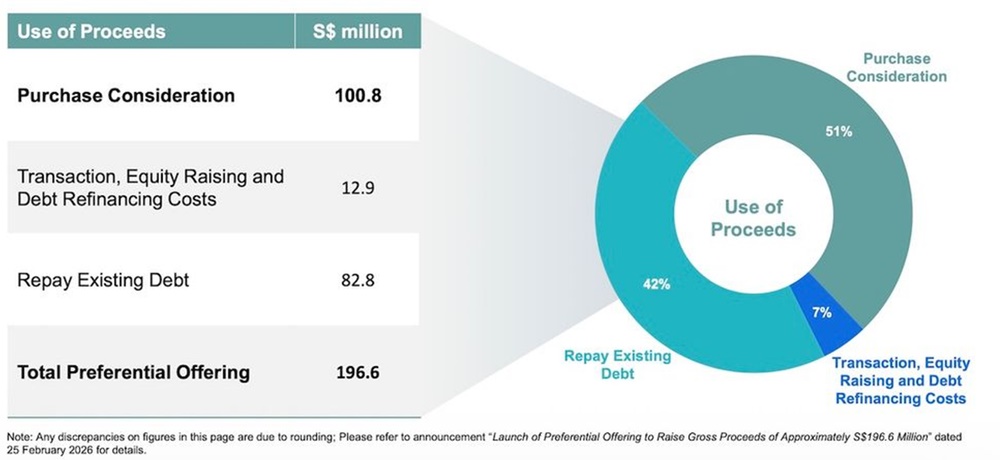

To fund the acquisition, Lendlease REIT launched an underwritten non-renounceable preferential offering to raise about S$196.6 million.

Entitled unitholders were offered 119 new units at S$0.558 for every 1,000 units held.

The remaining 30% acquisition is expected to be only marginally DPU-accretive on its own, with DPU projected to increase only by about 0.2%.

On a combined basis with the earlier 70% acquisition, the full transaction is estimated to be 2.1% DPU-accretive, while aggregate leverage is expected to edge down to about 37.6% after part of the proceeds is used for debt repayment.

Investor response was more muted for Lendlease REIT’s preferential offering.

Total applications came up to only about 62.19% of the new units available, which suggests more cautious demand for a deal that was only marginally DPU-accretive.

Lendlease REIT trades at about 0.80x book as of 22 April 2026, which is above its historical average P/B of 0.69x.

It offers a forward dividend yield of about 7.0%, which is above its historical average dividend yield of 6.6%.

Find out how much dividends you would have received as a shareholder of Lendlease REIT in the past 12 months with the calculator below.

Related links:

- Lendlease REIT latest valuation, share price and analysis

- Lendlease REIT dividend history and forecast

- Lendlease REIT Preferential Offering - What should unitholders do?

What would Beansprout do?

In our view, this latest round of acquisitions shows that not all REIT acquisitions are equally attractive for unitholders.

While all three transactions may help the REITs grow their portfolios, the quality of the assets acquired and the likely benefit to DPU look quite different.

Among the three, CICT’s Paragon deal looks the clearest to us. It appears to improve portfolio quality, keeps gearing manageable, and is expected to lift DPU.

CLAR’s acquisitions also look meaningful, as they broaden exposure across logistics, business space, and data centres. But the deal is more complex, so execution will matter more.

For Lendlease REIT, the acquisition looks easier to understand from a strategic perspective than from a return perspective. Full ownership of PLQ Mall may give it more control and flexibility, but the uplift to DPU from the remaining 30% stake appears modest.

Overall, we would focus less on the headline size of the deal and more on whether it improves DPU, balance sheet strength, and portfolio quality over time.

More broadly, these deals also reinforce why I would be cautious about relying too heavily on REITs alone for income.

Even when acquisitions are DPU-accretive, they are often funded through debt or new equity. That means investors still need to watch dilution and balance sheet risk closely.

That is also why we have been diversifying across to other high-quality dividend-paying stocks as well.

REITs can still play a role, especially for investors who want exposure to property-backed income. But I would look to build a more diversified income portfolio beyond Singapore REITs to grow my Income Pot. Explore other income ideas here.

Which of these three REIT acquisitions stands out most to you? Share with us in the comments below or in our Telegram group!

To screen for Singapore REITs with lowest price-to-book valuation or highest dividend yield, check out our best Singapore REIT screener.

If you are new to investing in Singapore REITs, you can start to learn more about Singapore REITs here.

If you prefer diversification without picking individual REITs, you can also gain exposure through Singapore REIT ETFs.

[Beansprout Exclusive Longbridge Promotion] Get bonus S$50 FairPrice voucher within 5 working days, plus 5% p.a. interest boost coupon (worth ~S$100) when you sign up for a Longbridge account via Beansprout. Plus, stand a chance to win S$150 CapitaVoucher weekly, with S$600 in total up for grabs. Promo ends on 30 April 2026. T&Cs apply. Learn more about the Longbridge promotion here.

Check out Beansprout's guide to the best stock trading platforms in Singapore with the latest promotions to invest in REITs and blue-chip stocks.

Enjoyed this insight? Follow Beansprout on Telegram, Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments