3 stocks paying out dividends in April 2026. Are their payouts sustainable?

Stocks

By Gerald Wong, CFA • 30 Mar 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

Here are 3 stocks paying out dividends in April 2026. We look at their latest results and assess whether these payouts are sustainable in the current market backdrop.

What happened?

The search for income has become more tricky in March 2026.

The escalation in the US-Israel-Iran conflict has added fresh uncertainty to markets, with higher oil prices reviving concerns about inflation.

That has led me to look at how Singapore blue chip stocks may be impacted from the recent oil price spike, in which I still managed to find 3 Singapore blue chip stocks that rose despite the oil price surge.

I also examined how the Fed’s latest signal would affect Singapore blue chips, since interest rate expectations remain an important driver for dividend investors.

At the same time, the recent pullback has led to pockets of income opportunities across the market.

I recently shared 3 Singapore REITs with dividend yields above 6% and 3 SGX ETFs with dividend yields above 6% for those looking to strengthen their income portfolio.

In this environment, the next question is not just which stocks are paying dividends in April 2026, but whether those payouts are backed by resilient businesses and sustainable earnings.

In this article, I look at 3 Singapore stocks paying out dividends in April 2026, and whether their payouts look sustainable from here.

3 stocks paying out dividends in April 2026

#1 - DBS Group Holdings Ltd (SGX: D05)

DBS is the largest bank in Singapore and one of the biggest banking groups in Asia.

Its business spans consumer banking, wealth management, corporate banking, treasury and transaction services across 19 markets. That scale matters because it gives DBS multiple earnings drivers, rather than relying only on one segment or one country.

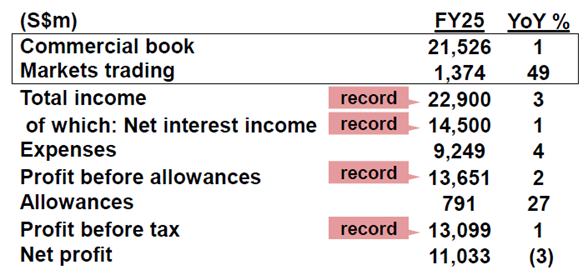

For FY2025, DBS reported record total income of S$22.9 billion, record profit before tax of S$13.1 billion, and net profit of S$11.0 billion.

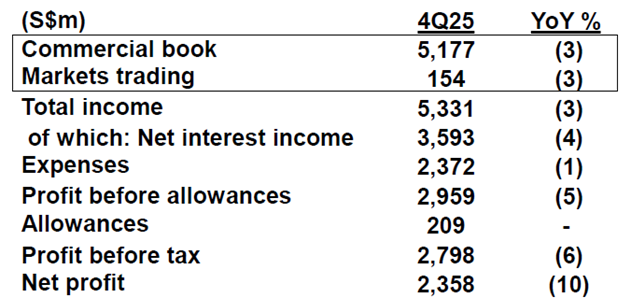

Even though 4Q2025 net profit fell 10.5% year on year to S$2.36 billion, the decline was mainly due to margin pressure, higher allowances linked to a real estate exposure, and the absence of one-off gains from the previous year rather than a breakdown in the core franchise.

Return on equity remained strong at 16.2%, showing that the bank was still generating high profitability even as interest rate tailwinds started to moderate.

Its consumer banking and wealth management franchise continued to be a major support.

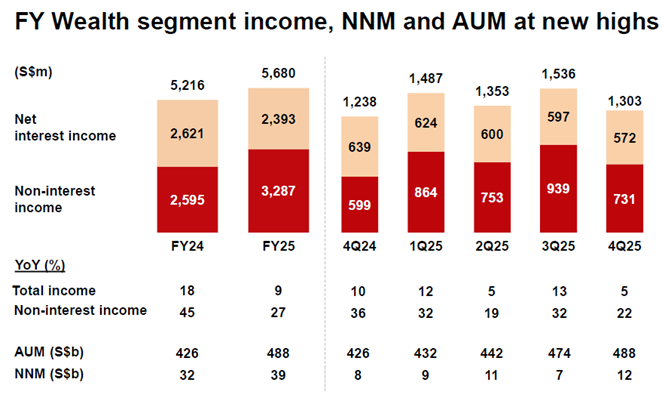

Consumer Banking and Wealth Management income rose to S$10.5 billion, while wealth management income hit a record S$5.7 billion.

In 4Q2025, non-interest income rose 13.5% year on year, helped by stronger wealth management fees and treasury customer sales. For the full year, fee income and treasury customer sales both reached record highs.

Assets under management also climbed to S$488 billion, up 19% in constant-currency terms. This suggests DBS is benefiting from stronger fee income and deeper client relationships.

Asset quality remained resilient too.

The non-performing loan ratio stayed at 1.0%, although the bank also raised specific allowances in 4Q2025, mainly linked to exposures in sectors such as real estate.

At the same time, management guided that 2026 net profit may come in slightly below the 2025 level, reflecting ongoing margin pressure as rates normalise.

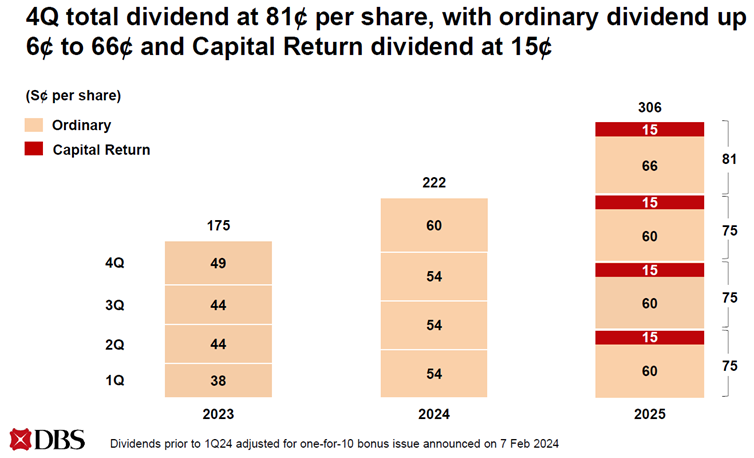

DBS has also committed to maintain its additional S$0.15 quarterly capital return dividend through FY2026 and FY2027, barring unforeseen circumstances.

Alongside its latest results, DBS declared a 4Q final dividend of 66 cents per share and a capital return dividend of 15 cents per share, bringing the total quarterly payout to 81 cents.

DBS will go ex-dividend on 8 April 2026 and pay the dividend on 17 April 2026.

This brings the total dividends for FY2025 to S$3.06 per share.

Based on its share price of S$57.12 as of 26 March 2026 and annualised dividend run rate of S$3.24 per share, this translates to a forward dividend yield of about 5.7%.

Find out how much dividends you would have received as a shareholder of DBS Group Holdings Ltd in the past 12 months with the calculator below.

Related links:

- DBS share price history and share price target

- DBS dividend forecast and dividend yield

- DBS offers 5.9% dividend yield. Better buy than UOB and OCBC after the recent dip?

#2 - City Developments Limited (SGX: C09)

City Developments, or CDL, is one of Singapore’s best-known property groups.

It has exposure across residential development, offices, hotels, serviced apartments, student accommodation, retail malls and integrated developments, with operations spanning multiple countries.

That gives CDL a broader earnings base than a pure developer, although it also means results can be affected by project timing, divestments and the hotel cycle.

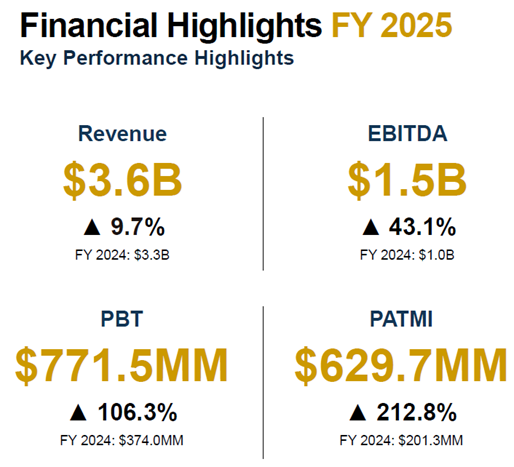

For FY2025, CDL reported revenue of S$3.59 billion, up 9.7% year on year, while PATMI tripled to S$629.7 million. The improvement was driven by robust Singapore residential sales and large capital recycling gains, particularly the sale of its 50.1% stake in South Beach.

A key highlight was its Singapore residential business.

CDL achieved record residential sales value of S$4.35 billion in 2025, the highest in the group’s history.

This was supported by projects such as The Myst, Norwood Grand and Union Square Residences, while The Orie and Zyon Grand were the standout launches, with 95% and 87% sold respectively as of late February 2026.

Management has signalled that bidding discipline will remain important given the competitive land market in Singapore.

At the same time, the group’s recurring businesses also provided support.

In CDL’s FY2025 results, the investment properties segment was the largest contributor to pre-tax profit at S$357.8 million, while hotel operations delivered pre-tax profit of S$256.0 million.

Investment property revenue rose 2.7%, while hotel revenue increased 1.7% and hotel RevPAR rose 1.3%.

This shows that while development gains and divestments were the biggest drivers of the earnings jump, the recurring income base remained reasonably supportive.

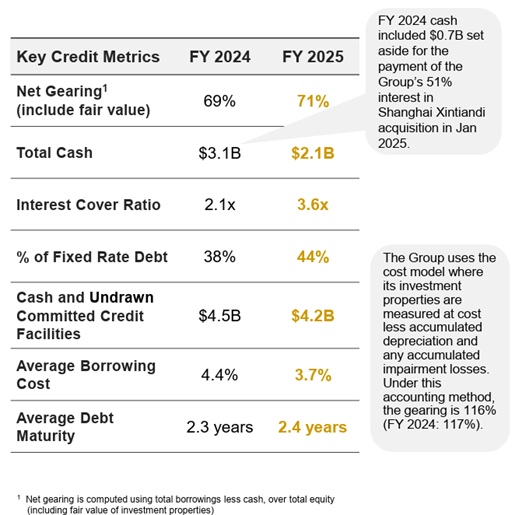

On the balance sheet, the group also ended the year with S$2.1 billion in cash and S$4.2 billion in cash plus undrawn committed credit facilities.

However, net gearing rose to 71%, up from 69%, after a year of acquisitions that included a Shanghai mixed-use site, three Singapore GLS sites and a UK hotel.

This means that while FY2025 earnings were strong, a meaningful part of the uplift came from capital recycling gains rather than purely recurring improvement, and the investment case still depends partly on continued monetisation and balance sheet management.

CDL has said it is targeting net gearing of around 60% over the medium term, with capital recycling expected to support gradual deleveraging.

In terms of capital recycling, the group completed about S$2 billion of contracted divestments globally, which helped unlock value and support earnings.

Looking ahead, further divestments remain an important part of the story.

Management indicated that capital recycling is now a core business activity, with assets across multiple geographies potentially on the block. This includes legacy UK development sites and residential projects worth about GBP800 million, three UK office buildings worth around GBP870 million, and two commercial properties in China.

That said, management also suggested that assets would not be sold at unattractive prices, which means the pace and scale of future divestments may depend on market conditions.

CDL is also looking to unlock value through redevelopment and asset enhancement.

Major projects underway include Union Square and Newport, while redevelopments of Delfi and City House remain in the medium-term pipeline.

The group has also completed major asset enhancement initiatives at Republic Plaza and City Square Mall, with positive leasing and operational outcomes.

This suggests there may still be scope to extract value from the existing portfolio beyond outright divestments.

The key question from here is whether the group can continue to execute on residential launches, asset monetisation and redevelopment while gradually bringing gearing down.

That may matter just as much as the headline earnings rebound, especially as investors continue to watch for an update on the group’s ongoing strategic review, which is expected by June 2026.

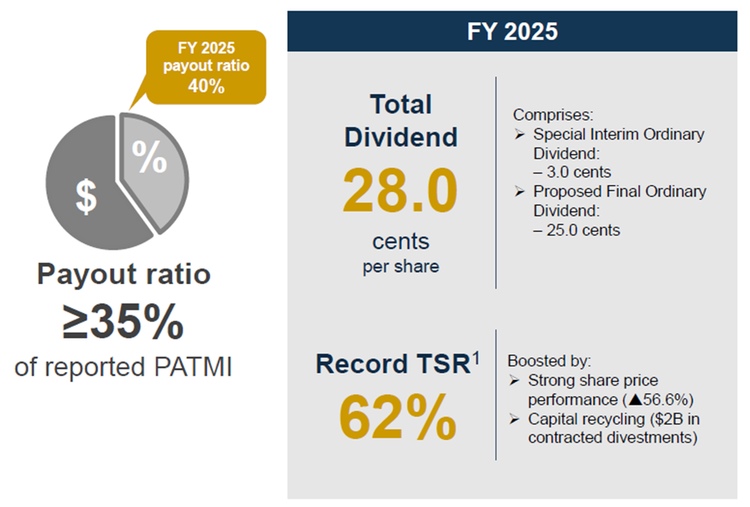

On dividends, CDL has enhanced its dividend policy and now intends to declare ordinary cash dividends at least once annually with a minimum payout ratio of 35% based on reported PATMI.

For FY2025, CDL recommended a final ordinary dividend of 25.0 cents per share. CDL will go ex-dividend on 30 April 2026 and pay the dividend on 19 May 2026.

Together with the 3.0 cent special interim dividend paid in September 2025, total ordinary dividends for FY2025 amount to 28.0 cents per share, representing a payout ratio of 40%.

This was a notable increase from FY2024 and may help reassure investors that management is more focused on shareholder returns, while still keeping the policy anchored to reported profitability.

Based on its share price of S$8.28 as of 26 March 2026 and consensus FY26 dividend per share of S$0.177, this translates to a forward dividend yield of about 2.1%.

Find out how much dividends you would have received as a shareholder of City Developments Limited in the past 12 months with the calculator below.

Related links:

- City Developments share price history and share price target

- City Developments dividend forecast and dividend yield

#3 - APAC Realty Limited (SGX: CLN)

APAC Realty is best known as the owner of the ERA real estate brokerage business in Singapore, and its network spans more than 21,900 advisors across 14 markets.

It also holds the ERA regional master franchise rights for 17 countries and territories in Asia Pacific.

In Singapore, its core earnings still come mainly from brokerage income across new home sales, resale transactions and rentals.

For FY2025, APAC Realty reported revenue of S$675.6 million, up 20.4% year on year.

Profit attributable to shareholders surged to S$20.55 million, supported by a sharp rebound in the primary market.

Management highlighted that stronger project launches and improved brokerage activity were the main reasons for the stronger performance.

The biggest swing factor was new home sales.

New home revenue more than doubled to S$230.2 million in FY2025, while resale and rental brokerage slipped 1.6% to S$437.8 million. Even after that decline, resale and rental still accounted for 64.8% of brokerage revenue.

That mix shift was important because new home brokerage tends to support stronger margins.

The other encouraging sign is that cash flow and balance sheet support improved as well.

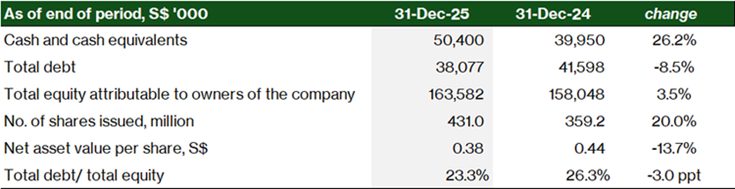

The group generated S$30.2 million in operating cash flow in FY2025 and ended the year with a healthy cash balance of S$50.4 million, up from S$40.0 million a year earlier.

APAC Realty being in a net cash position gives it some financial flexibility even though the business itself remains cyclical.

There are also reasons investors are watching the name more closely.

ERA Singapore was involved in a high number of project launches in 2025, and a healthy pipeline of new residential launches in 2026 could continue to support transaction activity.

ERA Singapore was involved in 27 new residential developments comprising 12,773 units in FY2025, and the company expects a 2026 pipeline of around 23 residential projects representing more than 11,800 units.

Still, APAC Realty’s earnings are directly tied to transaction volumes, project launches and housing sentiment. If the property market slows, earnings and dividends can swing much more sharply.

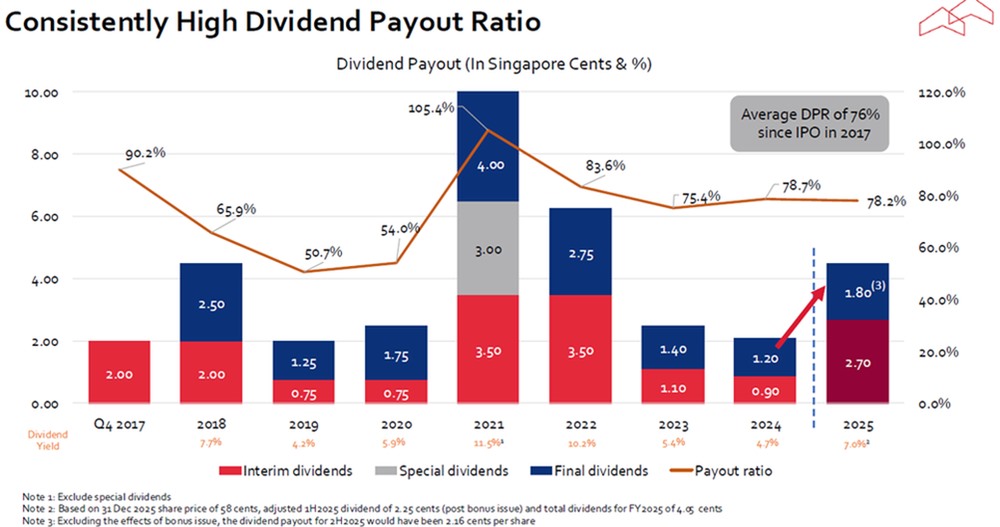

Alongside its latest results, APAC Realty proposed a final dividend of 1.8 cents per share. APAC Realty will go ex-dividend on 28 April 2026 and pay the dividend on 8 May 2026.

Together with its interim dividend, total FY2025 dividend payout was 4.05 cents per share on an adjusted basis after the bonus issue, with a payout ratio of 78.2%.

APAC Realty targets to maintain the dividend payout ratio at the upper end of the 50% - 80% range.

Based on its share price of S$0.565 as of 26 March 2026 and Beansprout’s FY26 dividend forecast of S$0.043, this translates to a forward dividend yield of about 7.6%.

Find out how much dividends you would have received as a shareholder of APAC Realty Limited in the past 12 months with the calculator below.

Related links:

- APAC Realty share price history and share price target

- APAC Realty dividend forecast and dividend yield

- APAC Realty - Strong new home sales drove higher dividends

What would Beansprout do?

With markets turning more volatile in March 2026, I have been paying closer attention not just to which stocks are offering dividends, but whether those payouts can still hold up if the macro backdrop remains uncertain.

That matters more now because higher oil prices, sticky inflation and the risk of interest rates staying elevated for longer could all affect earnings differently across sectors.

For me, the starting point is not the headline dividend yield alone. I would understand what is supporting the payout, whether it is backed by recurring earnings, and how exposed the business may be if market conditions become less favourable.

DBS, City Developments and APAC Realty are all paying out dividends around April 2026, but the strength of those payouts depends on very different business drivers.

Among the three, DBS stands out as offering the highest visibility on dividends in the near term and offers a forward dividend yield of about 5.7%. Even if profit moderates in 2026 from the record level in 2025, the payout still looks the most resilient of the three in the near term.

City Developments offers a lower dividend yield of about 2.1%, but its latest results showed a sharp rebound in earnings, supported by residential sales and capital recycling gains. The business looks to be on firmer footing, but I would still view CDL more as a recovery name with dividend support rather than a stock to own mainly for income.

APAC Realty currently offers the highest forward dividend yield among the three at about 7.6%, and its FY2025 results were supported by a strong year for new home launches. However, its earnings are more cyclical and tied to transaction volumes, which means dividends could be more volatile if the market slows.

For me, the key is not to chase a stock simply because it is paying a dividend in the next month.

What matters more is whether the business can keep generating the earnings and cash flow needed to support that payout, especially if the macro environment remains challenging.

If I am prioritising near term dividend visibility, DBS would stand out. If I am willing to take on more cyclical risk for a higher yield, APAC Realty may be worth considering, while CDL appears more like a turnaround idea rather than a core income holding.

| Stock | The good | Key risks |

| DBS | ● Forward yield of about 5.7% ● Strong and diversified earnings base across multiple business segments ● Clearest guidance on dividends among the three local banks | ● Profit could soften in 2026 ● Net interest margin pressure may persist ● Credit costs could rise if the macro environment weakens |

| City Developments | ● Forward yield of about 2.1% ● FY2025 earnings rebounded strongly ● Supported by improving property market conditions and capital recycling | ● Lowest dividend yield of the three ● Earnings can be lumpy due to project timing and divestments ● Dividend payout may be less predictable |

| APAC Realty | ● Forward yield of about 7.6% ● FY2025 earnings rose sharply, supported by new home sales ● Targets to maintain the dividend payout ratio at the upper end of the 50% - 80% range. | ● Most cyclical business among the three ● Dividend is closely tied to property activity ● Share price may be more volatile |

If you are looking for other stocks with upcoming dividends, explore other Singapore stocks, REITs and ETFs with upcoming dividend payments here.

If you’d like to screen for other Singapore stocks with attractive dividend yields and potential upside, you can explore our Singapore dividend stocks screener.

If you prefer broad exposure to blue chips without picking individual names, you can also learn more about the Straits Times Index (STI).

With higher oil prices, learn more about how Singapore blue chip stocks may be impacted here. As interest rate cut expectations moderate, learn how Singapore blue chip stocks may be impacted here.

As volatility continues, learn more about what we are doing with our portfolios amid the Middle East conflict here.

Is there a Singapore blue chip stock you are looking out for amid the market volatility? Share with us in the comments below or in our Telegram group!

[Beansprout Exclusive Longbridge Promotion] Get bonus S$50 FairPrice voucher within 5 working days, plus 5% p.a. interest boost coupon (worth ~S$100) when you sign up for a Longbridge account via Beansprout. Plus, stand a chance to win 1g of gold bar. Promo ends on 31 March 2026. T&Cs apply. Learn more about the Longbridge promotion here.

Planning to invest in Singapore blue chip stocks? Compare the best Singapore brokers to find the right trading platform, and see the latest promotions and sign-up rewards available.

Follow Beansprout on Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments