Beyond blue chips: 3 best-performing Singapore Next 50 stocks in 1H 2026. What to watch after the rally

Stocks

By Ng Hui Min • 07 Jul 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

We look at the three best-performing iEdge Singapore Next 50 stocks in the first half of 2026 that saw more gains compared to blue chips in 1H 2026, what has driven their rally, and what we are watching as we head into the second half of the year.

What happened?

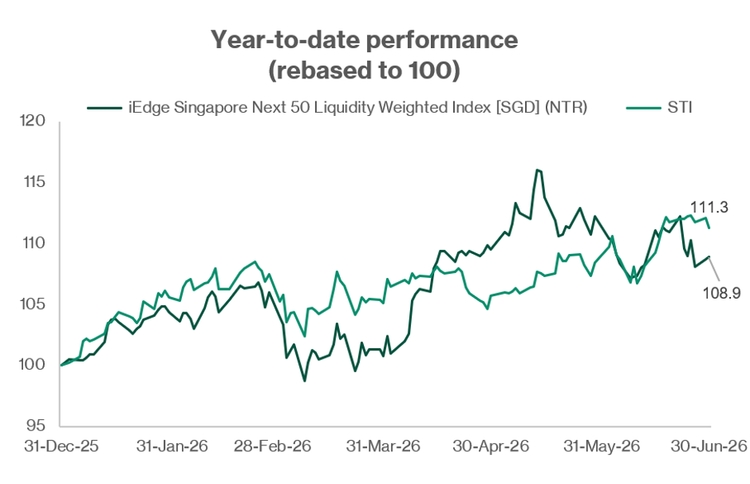

Singapore's mid-cap space has had an eventful first half of 2026.

The iEdge Singapore Next 50 Liquidity Weighted Index initially outperformed the STI from January to May, after several names delivering stronger gains than blue chips in the first quarter of 2026.

However, the lead faded in June, and by 30 June 2026, the Next 50 index ended 1H2026 with a total return of 8.9%, behind the STI’s 11.3%.

At the same time, selected Singapore tech stocks have continued to benefit from the AI and data centre infrastructure cycle, even as some Next 50 names lagged in June 2026.

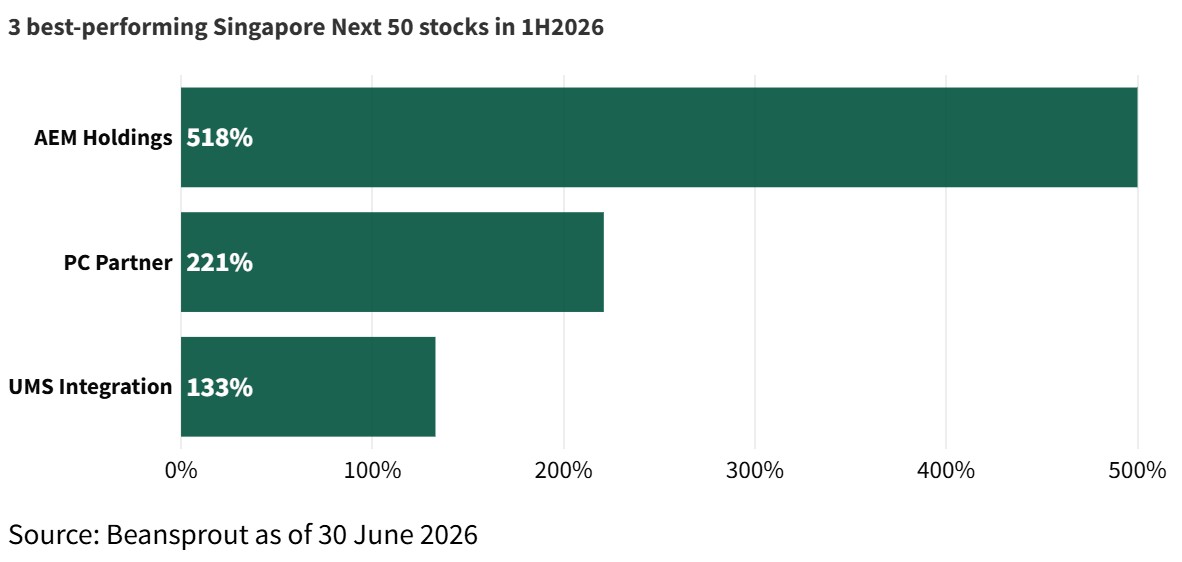

In this article, we look at three of the best-performing iEdge Singapore Next 50 stocks in 1H2026 which are AEM Holdings, PC Partner Group and UMS Integration, and what we are watching as we head into the second half of the year.

Notably, AEM Holdings and PC Partner Group were only added to the index in the June 2026 quarterly review, helping lift the index’s technology weighting to 26.2% from 16.6%, while UMS Integration remains one of its largest constituents.

All three stocks have exposure to semiconductors, AI infrastructure or related technology demand, but the strength and sustainability of their rallies differ meaningfully.

We also assess each stock using Beansprout's Opportunity framework, which screens for size and liquidity, revenue and earnings momentum, returns, and balance sheet strength.

3 best-performing Singapore Next 50 stocks in 1H2026

#1 - AEM Holdings Ltd (SGX: AWX)

AEM Holdings is a global provider of semiconductor test and handling solutions.

It serves customers in artificial intelligence and high-performance computing, personal computer and foundry, memory, and outsourced semiconductor assembly and test markets.

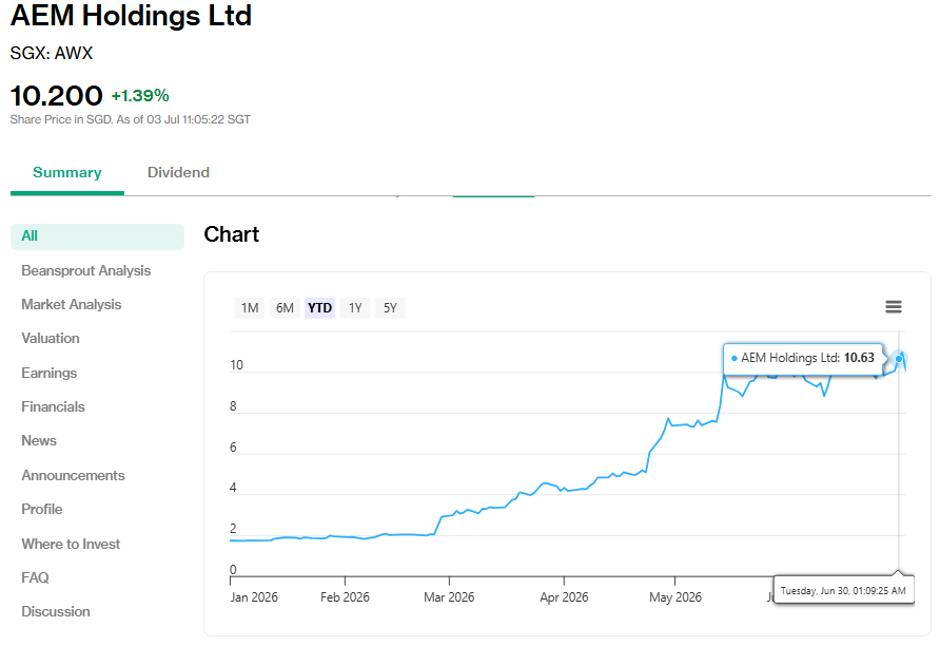

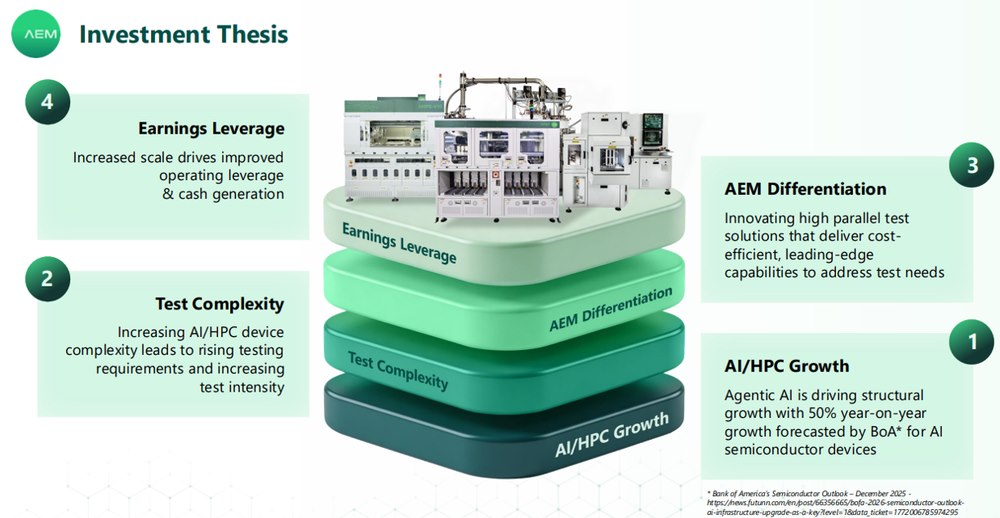

AEM has been one of Singapore’s strongest-performing mid-cap stocks in 2026.

As of 30 June 2026, its share price has risen 518% year-to-date, as investors became more positive on its exposure to the artificial intelligence and high-performance computing testing cycle.

Importantly, the rally has been backed by stronger business performance, not just market sentiment.

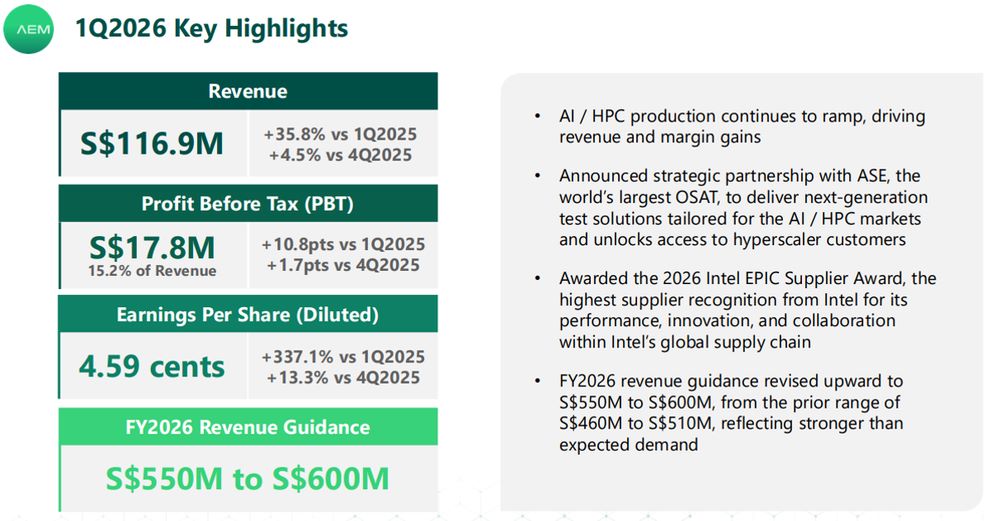

In the first quarter of 2026, revenue rose 35.8% year-on-year to S$116.9 million. Profit before tax jumped 370% to S$17.8 million, while profit before tax margin improved to 15.2% from 4.4% a year earlier.

Diluted earnings per share rose 337.1% year-on-year to 4.59 Singapore cents.

The core Test Cell Solutions segment was the main driver of growth. Revenue from the segment grew 72.0% year-on-year to S$88.1 million, making up 75.4% of group revenue.

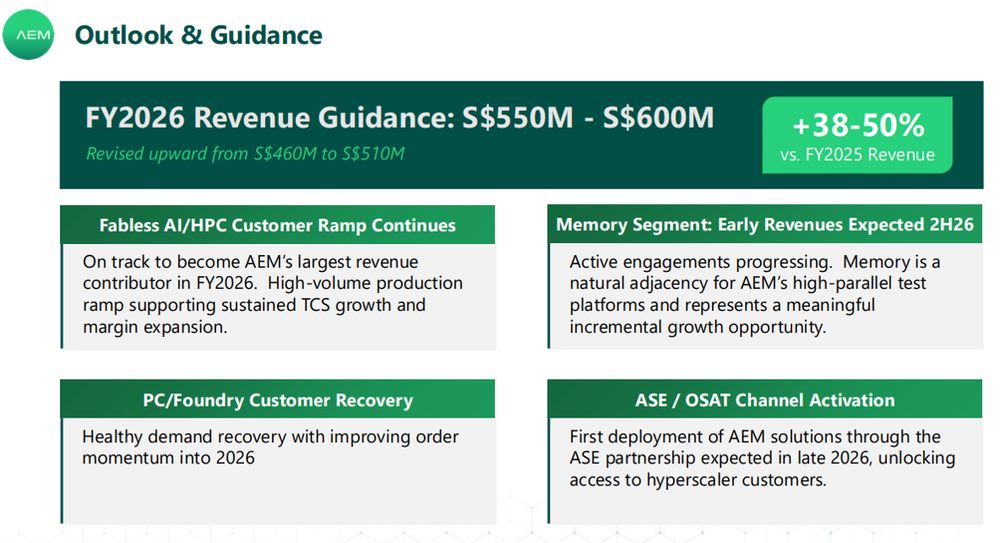

This was driven by high-volume production deployments for AEM’s fabless artificial intelligence and high-performance computing customer. Management expects this customer to become AEM’s largest customer this year.

The strong growth in Test Cell Solutions more than offset weakness in the smaller Contract Manufacturing segment.

Revenue from Contract Manufacturing fell 15.7% year-on-year due to softer demand from oil and gas customers.

AEM has also raised its financial year 2026 revenue guidance.

It first guided FY2026 revenue to be between S$460 million and S$510 million. It later raised guidance again by around 20% to S$550 million to S$600 million.

This would represent growth of 38% to 50% compared with the financial year 2025.

Two other developments add to the growth story.

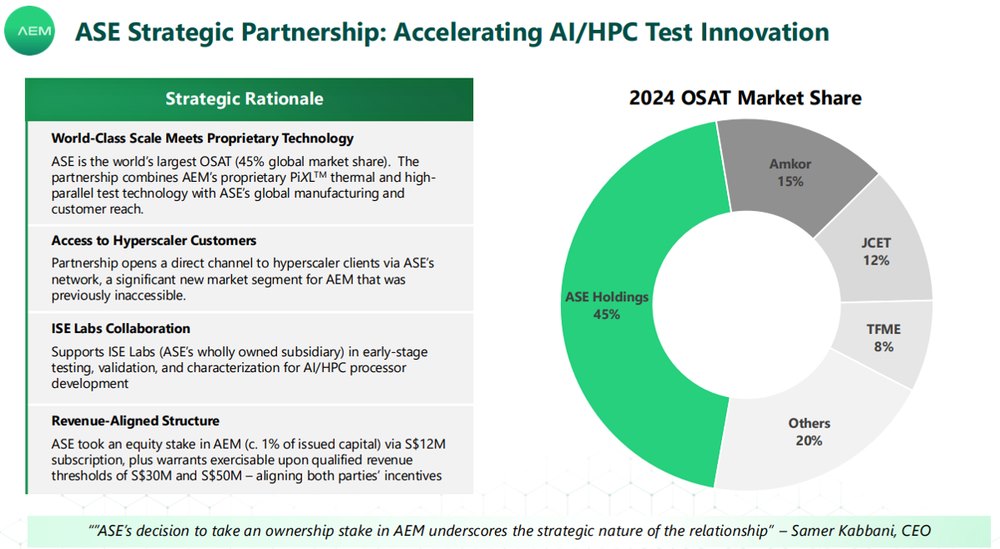

First, AEM announced a strategic partnership with ASE Technology, the world’s largest outsourced semiconductor assembly and test provider. The partnership combines AEM’s PiXL thermal and high-parallel test technology with ASE Technology’s manufacturing scale.

As part of the deal, ASE Technology subscribed for about a 1% equity stake in AEM for S$12 million. It also received warrants tied to future revenue milestones. This aligns both companies’ incentives and could help AEM reach more outsourced semiconductor assembly and test customers, as well as hyperscaler customers.

Second, AEM received the 2026 Intel Excellence, Partnership, Inclusion and Continuous Improvement Supplier Award. This is Intel’s top supplier recognition. It reinforces AEM’s position in Intel’s supply chain, even as its newer artificial intelligence and high-performance computing customer scales up.

AEM also received a favourable update on the legal front.

In October 2025, Advantest Test Solutions filed a patent infringement complaint against AEM in the United States District Court for the Southern District of California. The complaint alleged infringement of two United States patents.

In an order dated 29 June 2026, the court dismissed Advantest’s complaint. The court ruled that Advantest had not adequately pleaded direct or indirect infringement. However, Advantest has been granted permission to file an amended complaint.

AEM has said it does not expect the ruling to have a material impact on its business or financial position. It also said it remains prepared to defend its patents and intellectual property.

The matter is not fully closed, as Advantest can still file an amended complaint. Even so, the dismissal helps reduce an overhang that had affected the stock since October 2025.

For financial year 2025, AEM’s revenue grew 5% to S$399.3 million. Profit before tax rose at a faster pace of 52% to S$21.3 million, supported by better margins and cost discipline.

AEM also reinstated a dividend of 1.3 Singapore cents per share for financial year 2025, after paying no dividend in financial year 2024.

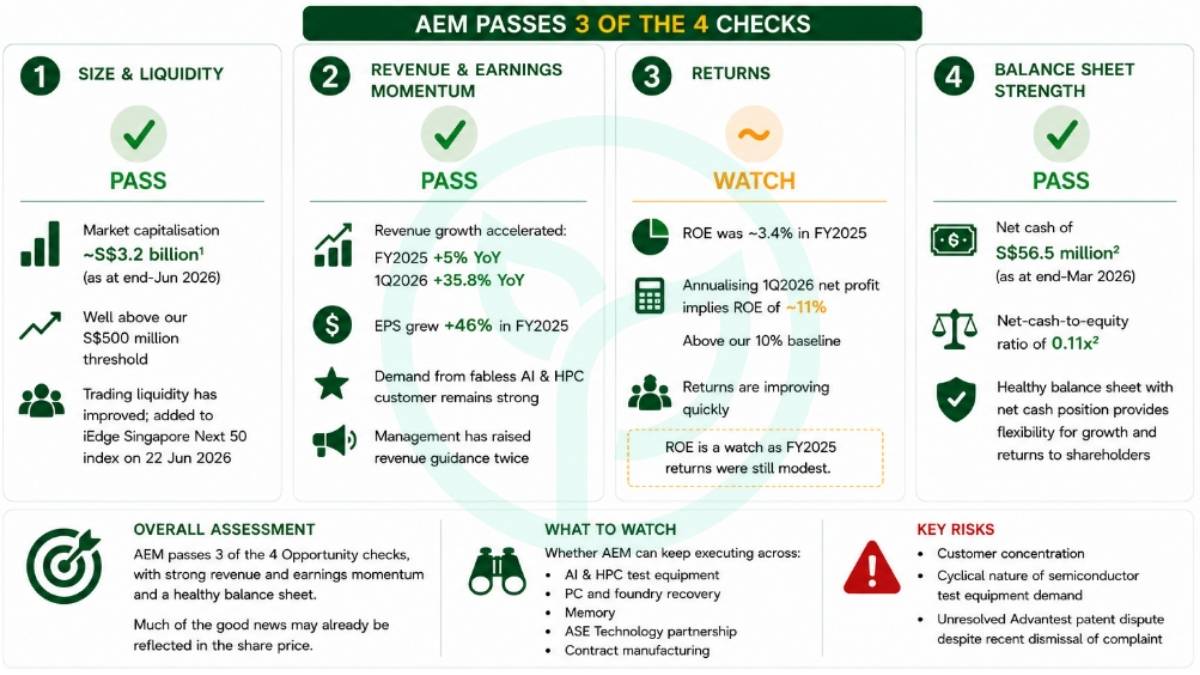

AEM screens well on Beansprout’s Opportunity framework and passes three of four checks.

Its market capitalisation of around S$3.2 billion as of end-June 2026 is well above our S$500 million threshold. Trading liquidity has also improved and AEM was added to the iEdge Singapore Next 50 index on 22 June 2026.

Revenue and earnings momentum is the strongest factor. Revenue growth accelerated from 5% in the financial year 2025 to 35.8% year-on-year in the first quarter of 2026. EPS grew 46% in FY25.

Demand from its fabless artificial intelligence and high-performance computing customer remains strong, and management has raised revenue guidance twice.

Returns are improving quickly.

Return on equity was still modest at around 3.4% in financial year 2025, but annualising first quarter 2026 net profit would imply return on equity of around 11%, above our 10% baseline.

AEM’s balance sheet is also healthy. It had net cash of S$56.5 million as at end-March 2026 and a net-cash-to-equity ratio of 0.11 times.

Overall, AEM passes three of the four checks, but much of the good news may already be reflected in the share price.

Investors should watch whether AEM can keep executing across artificial intelligence and high-performance computing testing, personal computer and foundry recovery, memory, the ASE Technology partnership and contract manufacturing.

Key risks include customer concentration, the cyclical nature of semiconductor test equipment demand, and the unresolved Advantest patent dispute despite the recent dismissal of the complaint.

Related links:

#2 - PC Partner Group Limited (SGX: PCT)

PC Partner Group designs, manufactures and sells graphics cards and other personal computer components.

It sells own-brand graphics cards under ZOTAC, Inno3D and Manli. It also manufactures products for other brands through original equipment manufacturing and original design manufacturing arrangements.

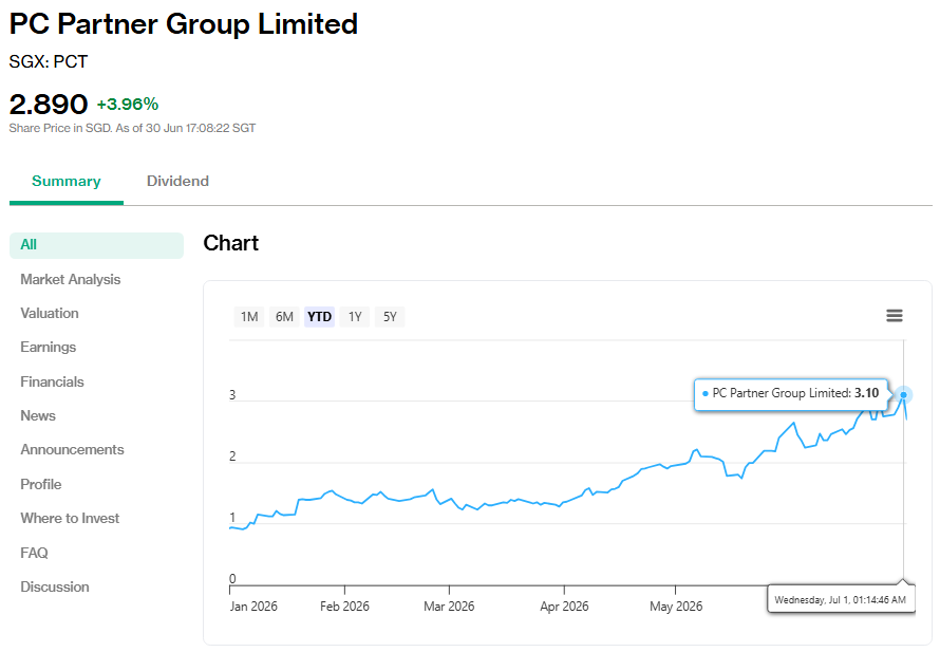

PC Partner was listed on the Hong Kong Stock Exchange in 2012 and secondary-listed on the Singapore Exchange Mainboard in November 2024. It later delisted from Hong Kong on 14 January 2026, making Singapore its sole primary listing.

This was part of its plan to diversify its business and shareholder base beyond Greater China.

PC Partner’s share price performed strongly in the first half of 2026, up 221% as of 30 June 2026.

The rally was supported by the artificial intelligence-driven demand cycle for graphics processing units, as well as the group’s own artificial intelligence-related product launches.

It was also added to the iEdge Singapore Next 50 index on 22 June 2026, in the same review as AEM Holdings.

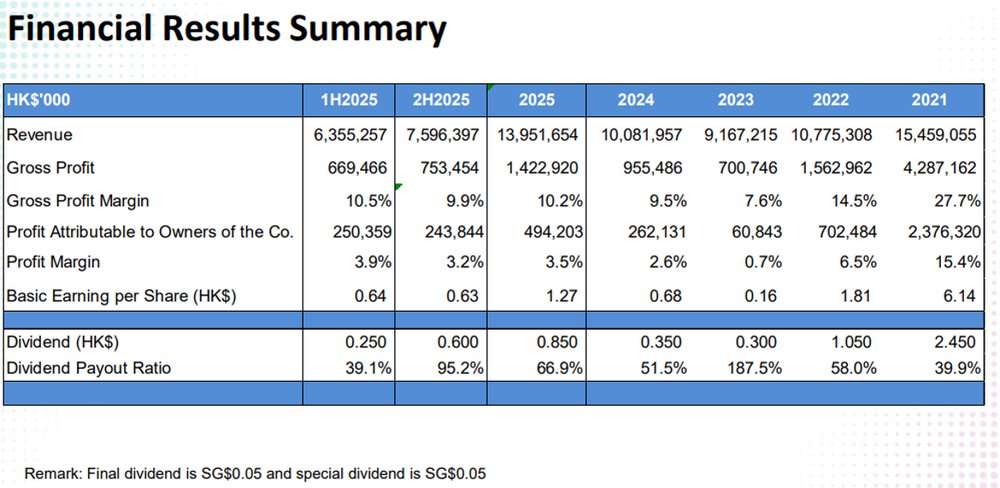

The business delivered a strong financial year 2025. Revenue rose 38.4% year-on-year to HK$13.95 billion, while profit attributable to owners increased 88.5% to HK$494.2 million. Gross profit margin also improved to 10.2% from 9.5%.

The key driver was Nvidia’s RTX5090 graphics card. It contributed HK$1.69 billion in revenue in financial year 2025, or 16% of PC Partner’s own-brand graphics card business. Higher-priced Blackwell-series gaming cards also lifted average selling prices.

This helped offset weaker performance in other areas, including the lower-margin original equipment manufacturing and original design manufacturing graphics card segment.

PC Partner also rewarded shareholders with higher dividends. For financial year 2025, it declared a final dividend of S$0.05 per share and a special dividend of S$0.05 per share to mark the first anniversary of its Singapore listing. This brought its total payout to HK$0.85 per share, or 66.9% of earnings. Management has also reiterated a minimum dividend payout policy of 30% to 40% of profits.

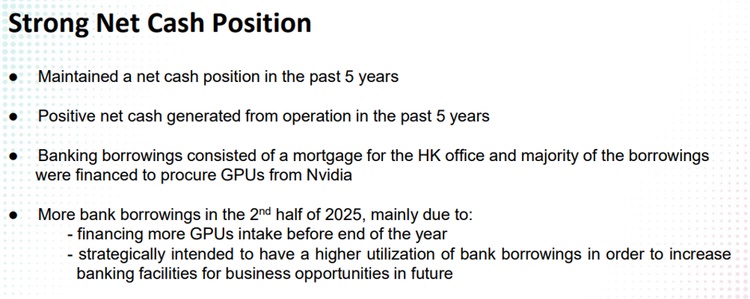

A few risks are worth watching.

PC Partner’s inventories doubled from HK$842 million in FY2024 to HK$1.69 billion in FY2025, as the group bought more GPUs ahead of expected supply constraints and faced longer logistics lead times for its Batam plant. Bank borrowings also rose in 2H2025 to fund this inventory build-up.

There were also one-off tax and tariff-related costs. These included additional tax and penalty interest in Hong Kong, as well as a US tariff classification dispute with a contingent liability of about US$25 million, of which US$11.8 million has already been paid while litigation continues.

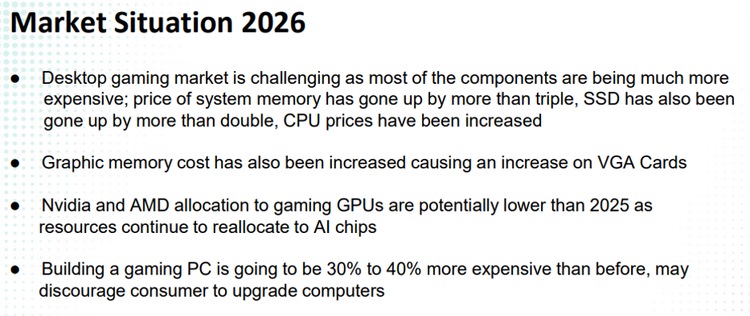

For 2026, the outlook is more mixed. Prices of memory, solid-state drives and central processing units have risen sharply, which could discourage consumers from upgrading their personal computers. Nvidia and Advanced Micro Devices are also expected to allocate fewer graphics processing units to gaming, as more supply is diverted to artificial intelligence chips.

In response, PC Partner plans to focus on higher-priced premium cards, raise average selling prices and discontinue lower-end models. Management still expects double-digit revenue growth in 2026, but this is likely to be driven more by pricing than volume.

Beyond gaming graphics, PC Partner is also building an artificial intelligence server integration business as an approved Nvidia partner.

Management expects this business to contribute little to no revenue in 2026, but is targeting a larger contribution from 2027 onwards. This could become a new growth area if execution is successful, though it remains early-stage today.

Despite its strong share price rally, PC Partner still trades at a lower valuation than AEM’s 50x and UMS’ 39.0x.

Its next-twelve-month price-to-earnings ratio has recovered from around 3 times in March 2026 to about 6.6 times currently.

Even after this re-rating, PC Partner’s valuation remains well below AEM’s and UMS’ current multiples.

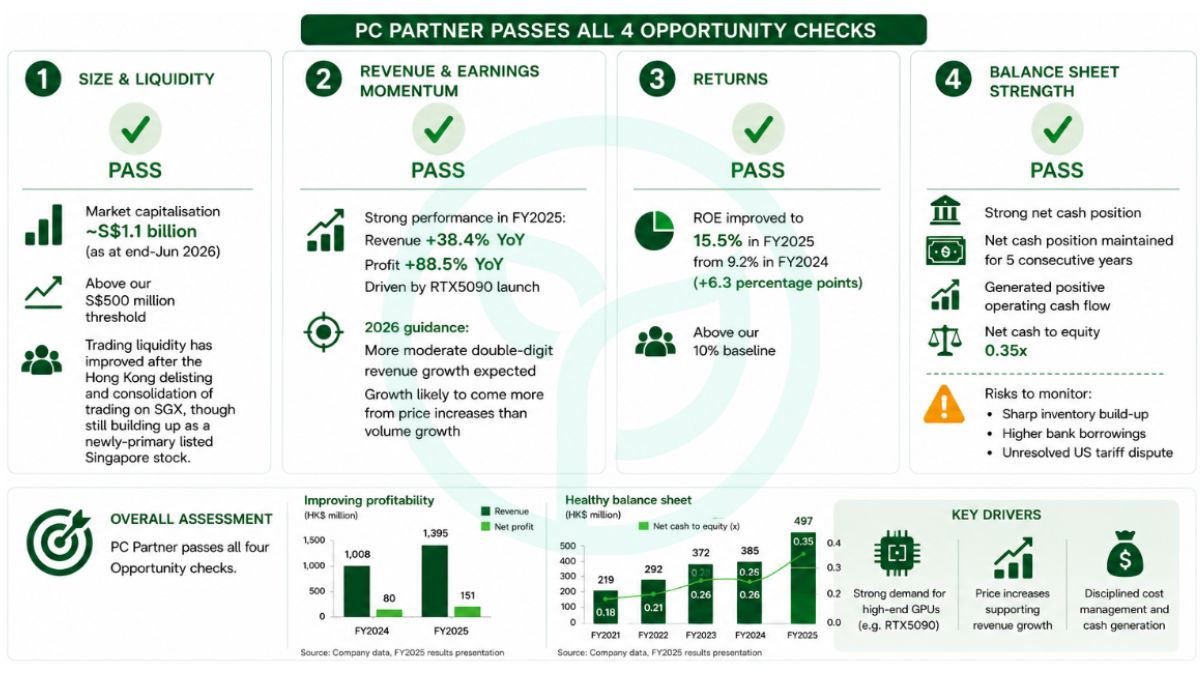

PC Partner screens well on Beansprout’s Opportunity framework.

Its market capitalisation was around S$1.1 billion as of end-June 2026, above our S$500 million threshold. Trading liquidity has improved after the Hong Kong delisting consolidated trading on the Singapore Exchange, although liquidity is still building up as a newly-primary listed Singapore stock.

Revenue and earnings momentum was strong in the financial year 2025. Revenue rose 38.4%, while profit increased 88.5%, driven by the RTX5090 launch. However, management’s 2026 guidance points to more moderate double-digit revenue growth, with growth likely to come more from price increases than volume growth.

Return on equity improved to 15.5% in FY2025, up 6.3 percentage points from 9.2% in FY2024, above our 10% baseline.

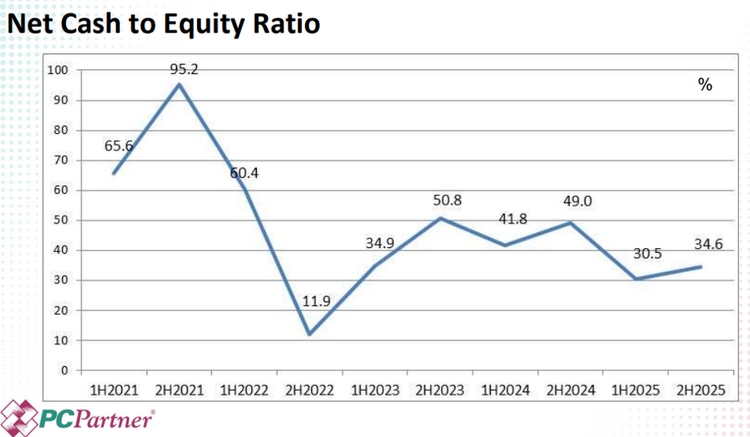

The balance sheet remains acceptable.

PC Partner has maintained a net cash position for five consecutive years and has generated positive operating cash flow. Its current net cash to equity stands at 0.35x.

Still, the sharp inventory build-up, higher bank borrowings and unresolved United States tariff dispute are risks to monitor.

Source: Company data, FY2025 results presentation

Overall, PC Partner passes around four of our four Opportunity checks. The stock's rally has been real and backed by improving profitability, but 2026 guidance suggests the pace of revenue growth is normalising, and the one-off tax charges and tariff dispute add a layer of complexity that investors should factor into any valuation.

Related links:

- PC Partner Group latest valuation, share price and analysis

- PC Partner Group dividend history and forecast

#3 - UMS Integration Limited (SGX: 558)

UMS Integration provides precision machining components and equipment modules for semiconductor equipment manufacturers.

It also has a smaller Aerospace segment and other precision engineering businesses, including JEP Holdings, which it recently consolidated.

Unlike AEM Holdings and PC Partner, UMS has been a long-standing member of the iEdge Singapore Next 50 index. It is also one of the index’s larger constituents, with a weight of around 4.8% as of end-June 2026.

As of 30 June 2026, UMS’ share price was up 133% in the first half of 2026. The rally was supported by artificial intelligence-driven semiconductor capital expenditure and steady execution.

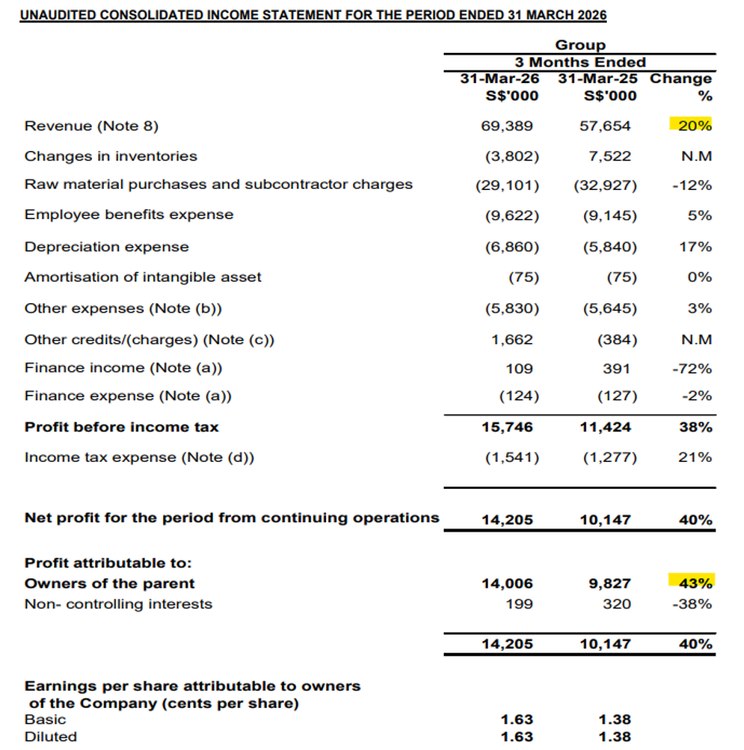

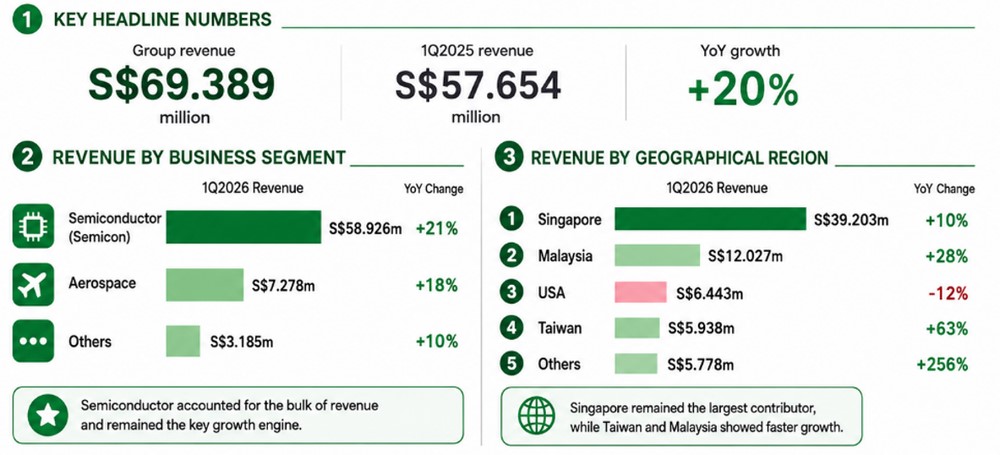

In the first quarter of 2026, revenue rose 20% year-on-year to S$69.4 million. Net profit attributable to shareholders increased 43% to S$14.0 million, while profit before tax rose 38% to S$15.7 million.

The Semiconductor segment remained the key growth driver. Revenue from the segment grew 21% year-on-year to S$58.9 million. Aerospace revenue also rose 18% to S$7.3 million.

Within Semiconductor, growth was broad-based. Component sales rose 26% to S$36.5 million, driven by higher demand from a newer customer. Integrated Systems sales grew 14% to S$22.4 million.

Sales to Taiwan, Malaysia and other markets outside the United States also grew strongly. This reflected increased shipments to the manufacturing locations of UMS’ newer major customer.

Management sounded positive on the outlook. It noted that both key customers had reported results that beat revenue expectations. One customer also expects its semiconductor equipment business to grow by more than 20% in 2026.

UMS also highlighted strong order flow from its newer key customer, which is diversifying its supply base from the United States to Asia. The Aerospace segment should also continue to benefit from strong global aircraft order backlogs.

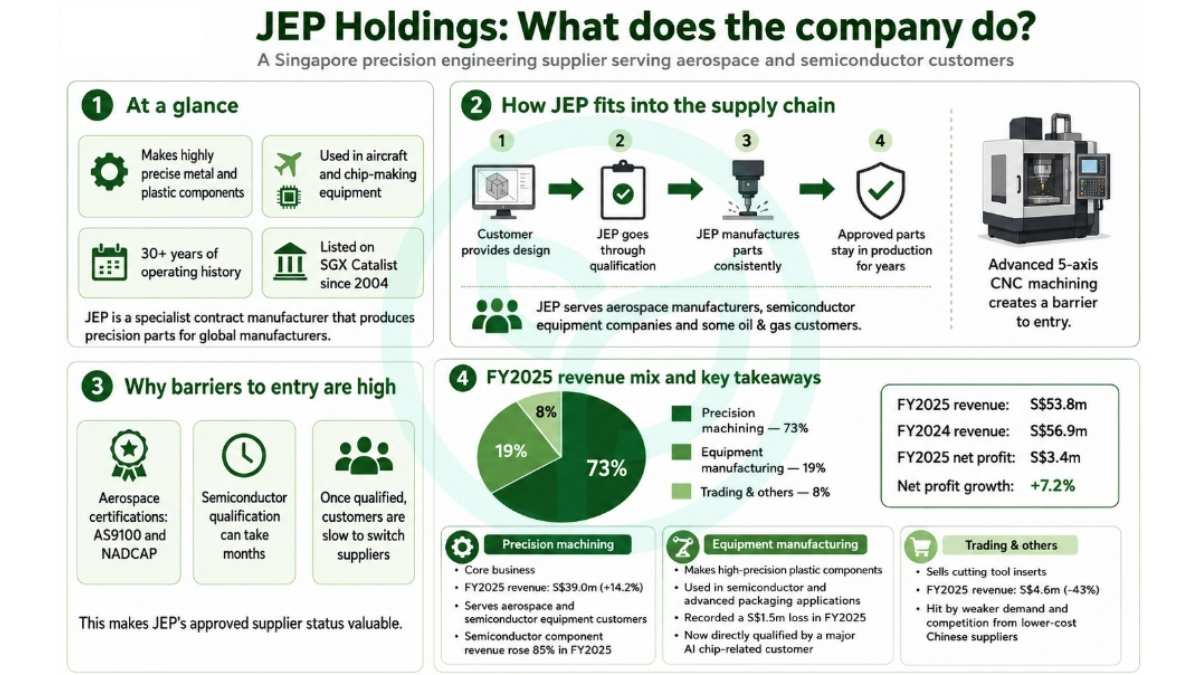

UMS’ roughly 80%-owned subsidiary, JEP Holdings, is also worth watching as a supporting growth driver.

JEP remains a relatively small contributor today, making up around 17% of UMS’ financial year 2025 revenue and less than 10% of net profit. However, it broadens UMS’ exposure across both semiconductors and aerospace.

JEP supplies complex semiconductor components and also serves aerospace customers through its specialised aerospace and plastic fabrication capabilities. Around 55% of JEP’s revenue comes from semiconductors, while 45% comes from aerospace.

Management expects JEP to deliver double-digit revenue and profit growth from financial year 2026, as components qualified between 2023 and 2025 move into mass production.

JEP has also invested early in long lead-time equipment, which could help it capture the next demand upcycle ahead of peers still waiting to expand capacity. Margins could improve further as the business shifts toward front-end semiconductor and advanced packaging work.

If this plays out, JEP could provide a modest but meaningful earnings uplift for UMS, while also adding useful diversification beyond UMS’ core semiconductor equipment exposure.

There are two housekeeping items to note.

First, UMS issued 177.6 million bonus shares in January 2026. This increased its share count from 710.5 million to 888.2 million shares. As a result, net asset value per share fell mechanically, even though total equity rose 3.5% to S$443.8 million.

Second, UMS completed the acquisition of the remaining 30% stake in Starke Singapore for S$8.2 million in March 2026. This was partly funded by a new S$8.3 million short-term bank loan, which was its first bank borrowing in some time.

Operating cash flow was negative S$4.9 million in the first quarter of 2026, compared with positive S$11.7 million a year earlier. This was due partly to the Starke acquisition payment, higher working capital needs and a temporary payment delay from one customer. Management said the delay has since been resolved, with all overdue balances collected.

UMS maintained its interim dividend at 1 Singapore cent per share for the quarter.

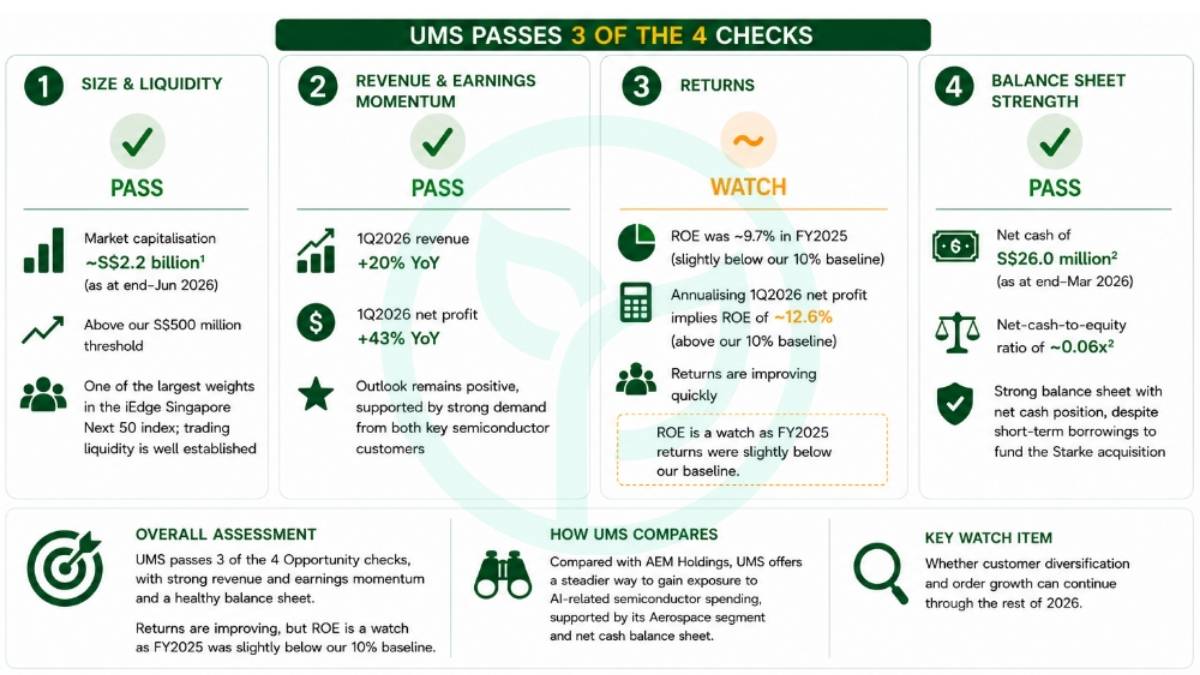

UMS screens well on Beansprout’s Opportunity framework and passes 3 of our 4 checks.

Its market capitalisation was around S$2.2 billion as of end-June 2026, above our S$500 million threshold. As one of the largest weights in the iEdge Singapore Next 50 index, trading liquidity is also well established.

Revenue and earnings momentum is healthy. First quarter 2026 revenue grew 20%, while net profit rose 43%. The outlook also remains positive, supported by strong demand from both key semiconductor customers.

Return on equity was around 9.7% in the financial year 2025, slightly below our 10% baseline. But annualising first quarter 2026 net profit would imply an improved return on equity of around 12.6%.

The balance sheet remains strong. UMS had net cash of S$26.0 million as at end-March 2026, with a net-cash-to-equity ratio of around 0.06 times. This is despite taking on short-term borrowings to fund the Starke acquisition.

Overall, UMS passes three of our four Opportunity checks.

Compared with AEM Holdings, UMS offers a steadier way to gain exposure to artificial intelligence-related semiconductor spending, supported by its Aerospace segment and net cash balance sheet.

The key watch item is whether customer diversification and order growth can continue through the rest of 2026.

Related links:

- UMS Integration latest valuation, share price and analysis

- UMS Integration dividend history and forecast

What would Beansprout do?

AEM Holdings, PC Partner Group and UMS Integration have benefited from the artificial intelligence and semiconductor capital expenditure wave in the first half of 2026.

As market conditions stay volatile, I would be careful not to evaluate these stocks based on share price momentum alone, especially after their sharp rallies.

When evaluating these growth stocks for my Opportunity Pot as part of Beansprout’s four pots of wealth, I would use our Opportunity framework as a first filter. This means looking at their size and liquidity, revenue and earnings momentum, return on equity, and balance sheet strength before doing a deeper dive.

Among the three, AEM Holdings appears to have the strongest operating momentum, supported by faster revenue growth, improving earnings and two upgrades to its FY2026 revenue guidance. However, after its sharp rally, I would watch whether it can sustain demand from its AI and high-performance computing customers, manage customer concentration risk, and justify its higher valuation. Learn more about AEM Holdings here.

PC Partner Group looks more attractively valued than AEM and UMS, with stronger FY2025 profitability and a net cash position. Its AI server integration business could provide a new growth driver over time, but I would monitor its inventory build-up, reliance on Nvidia GPU supply, and unresolved tax and tariff disputes. Learn more about PC Partner Group here.

UMS Integration offers another way to gain exposure to the semiconductor cycle. Growth is supported by both its Semiconductor and Aerospace segments, while its roughly 80%-owned subsidiary, JEP Holdings, adds further exposure to complex semiconductor components and aerospace manufacturing. The key watch items are whether UMS can sustain return on equity above our 10% baseline and manage customer concentration risk. Learn more about UMS Integration here. Learn more about UMS Integration here.

In short, AEM looks operationally the strongest, but its valuation now reflects much of the good news after the sharp rally.

PC Partner offers improving returns, the lowest valuation among the three names, and a potential new growth driver in artificial intelligence servers, although legal overhangs remain.

UMS provides a steadier exposure to Singapore’s artificial intelligence-linked semiconductor theme, with JEP adding a smaller but useful diversification angle.

For the Opportunity Pot, I may put all three stocks on a refined watchlist, but I would still be selective on valuation, position size and execution risk.

You can learn more about the four checks I use to screen growth stocks for the Opportunity Pot here.

Key strengths and risks at a glance

| Stock | The Good | Key Risks |

| AEM Holdings |

|

|

| PC Partner Group |

|

|

| UMS Integration |

|

|

Overall, these Singapore Next 50 stocks are aligned with our view on why Singapore stocks are still worth looking at in 2026.

There may also be other avenues to capture structural growth in the Singapore market, including companies linked to infrastructure, data centres, energy and food security as well as Singapore's rise as a wealth hub. Find out more about the 4 growth themes we are watching in Singapore stocks here.

If you are looking for more Singapore stock ideas linked to long-term growth themes, you can explore our high-conviction curated stock opportunities here.

Learn more about Beansprout's four pots of wealth framework to grow your wealth with clarity here.

Are there any Singapore Next 50 stocks you are looking at now? Share with us in the comments below or in our Telegram group!

Planning to invest in Singapore stocks? Compare the best Singapore brokers to find the right trading platform, and see the latest promotions and sign-up rewards available.

Follow Beansprout on YouTube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments