DBS, OCBC and UOB hit record highs in July 2026. What could drive them higher beyond dividends

Stocks

By Gerald Wong, CFA • 09 Jul 2026

Global Wealth Technology Pte. Ltd. is regulated by the Monetary Authority of Singapore (MAS) as a licensed Financial Adviser.

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

DBS, OCBC and UOB have hit record highs again in July. We look at what could drive Singapore bank stocks higher beyond dividend and which bank stands out.

What happened?

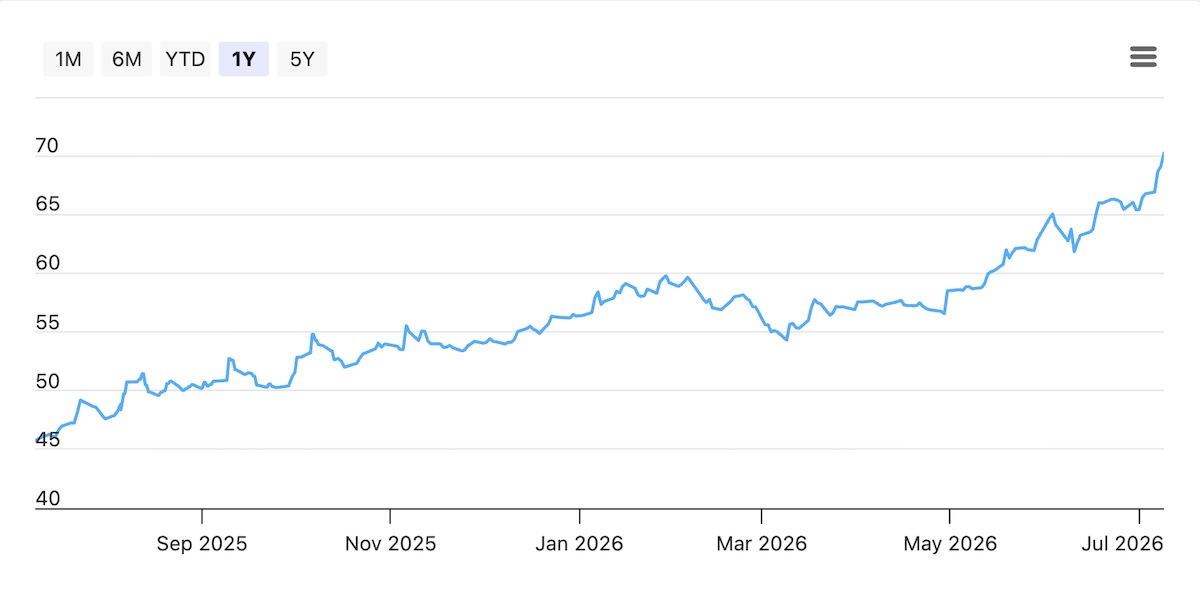

Singapore bank stocks have been making new all-time highs.

DBS was one of the three best-performing Singapore blue chips in May, and the momentum has continued with the share price reaching a new all-time high of above S$70 recently.

Earlier, we had also looked at how DBS and OCBC's record run has been supported by wealth management income, as fee income from Singapore's growing wealth hub has helped cushion the drag from lower interest rates on net interest income.

This ties into a broader theme we flagged, that Singapore's rise as a wealth management hub could support Singapore banks over the long run, as more family offices, private banking assets and cross-border wealth flow through Singapore's financial system.

More recently, we compared DBS, OCBC and UOB on earnings growth, capital strength and dividend sustainability, and found that DBS and OCBC continue to stand out on EPS growth, ROE and capital ratios, while UOB still needs to show a clearer earnings recovery.

Now, with all three banks trading at or near record highs and sentiment continuing to improve, the question many in the Beansprout community are asking is whether the rally has further room to run.

In this article, I look at what could drive DBS, OCBC and UOB next, and which Singapore bank looks more attractive after the rally.

Why DBS, OCBC and UOB may still have potential upside

The rally in Singapore bank stocks has not been driven by dividends alone.

It also reflects improving investor expectations around bank margins, fee income, capital returns and regional growth.

The key question now is whether these drivers can continue to support earnings, even with DBS, OCBC and UOB trading at or near record highs.

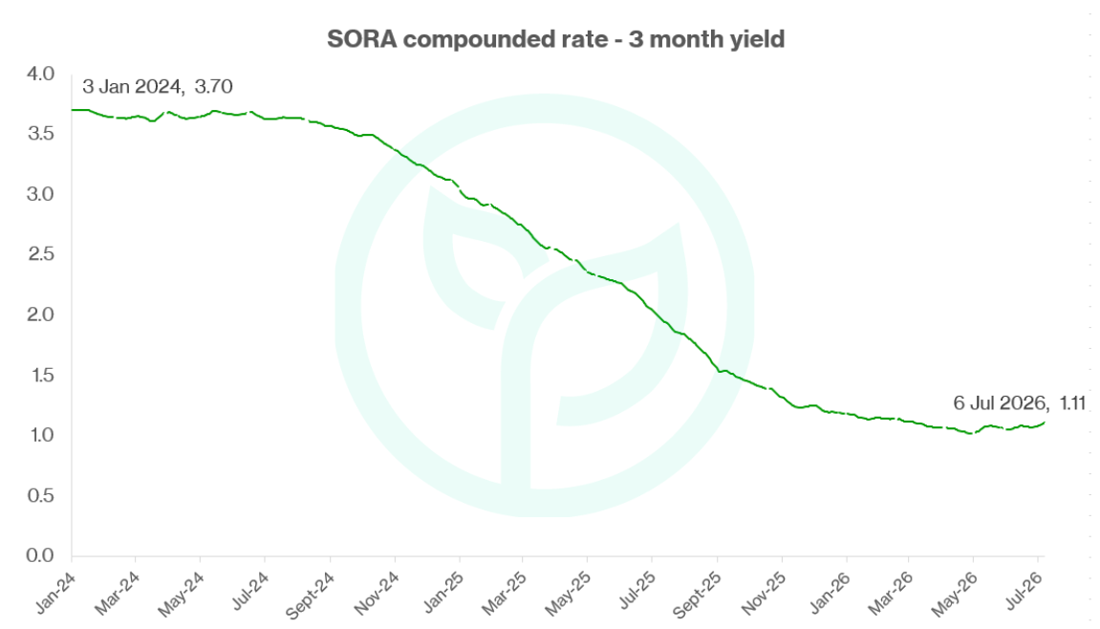

#1 - SORA may have bottomed, easing pressure on bank margins

One reason investors are paying closer attention to Singapore banks is that the Singapore Overnight Rate Average, or SORA, may have found a floor.

SORA affects loan yields and net interest margins, which are key drivers of bank earnings.

After falling by about 2.6 percentage points through 2024 and 2025, 3-month SORA now appears to be stabilising. This was a bigger decline than the 1.75 percentage point fall in US interest rates, suggesting that excess liquidity had built up in Singapore’s banking system.

That now appears to be reversing.

In May 2026, banking system loans grew 8.7% year-on-year, ahead of deposit growth of 6.8%. This pushed the loan-to-deposit ratio back up to 68.7%, while the CASA ratio slipped by 50 basis points to 54%.

If consumer and corporate loan demand continues to absorb excess liquidity, SORA could find stronger support from here.

This would help ease the net interest margin pressure that has weighed on Singapore banks over the past year.

More importantly, this could support the view that the worst of the margin compression may be behind us.

If net interest income and net interest margins begin to recover in FY2027, this could become an important re-rating catalyst for the sector.

#2 - Wealth management income is helping Singapore banks offset lower interest rates

The second support comes from wealth management and other fee income.

For Singapore banks, this includes fees earned from private banking, investment products, insurance, advisory services and other wealth-related activities.

This is becoming one of the cleanest growth angles for Singapore banks, especially as lower interest rates put pressure on net interest margins.

DBS’s wealth income rose from S$4.43 billion in FY2023 to a record S$5.70 billion in FY2025, an increase of about 29% over two years. In 1Q2026, DBS’s wealth management fees also reached a record S$907 million.

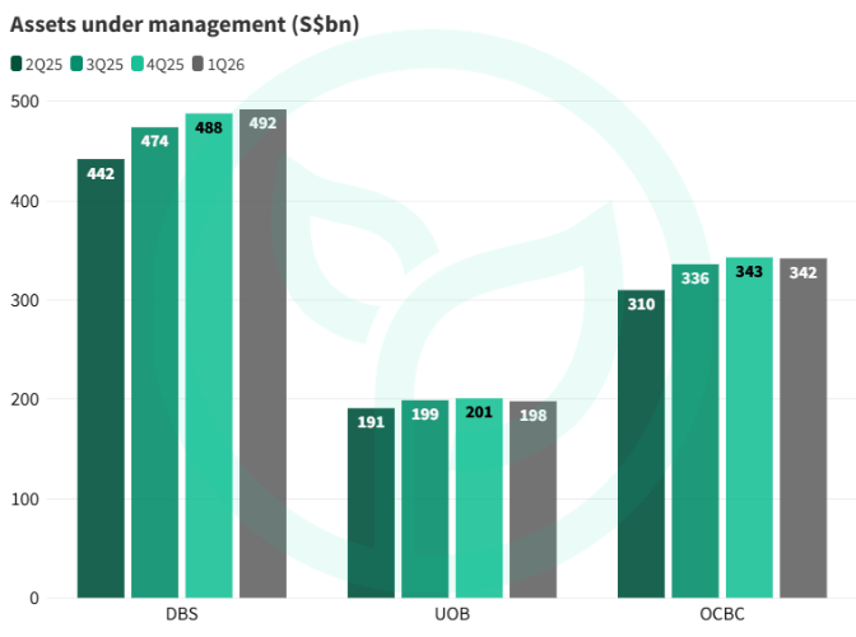

OCBC’s wealth management income now accounts for about 37% of group income, making it a major contributor to the bank’s earnings base.

UOB is also trying to scale up this part of its business, with a target to roughly double wealth income to S$2.5 billion by 2030.

This matters because wealth management income is fee-based and relatively capital-light. It can help banks defend return on equity (ROE) even when loan margins are under pressure.

It also gives investors another reason to look beyond net interest margin (NIM) trends alone.

If wealth management fees, trading income, card fees, insurance and transaction banking income continue to grow, DBS, OCBC and UOB would have a broader earnings base that is less dependent on the interest rate cycle.

For DBS and OCBC in particular, this has helped support earnings resilience and may partly explain why they continue to trade at valuation premiums compared with UOB.

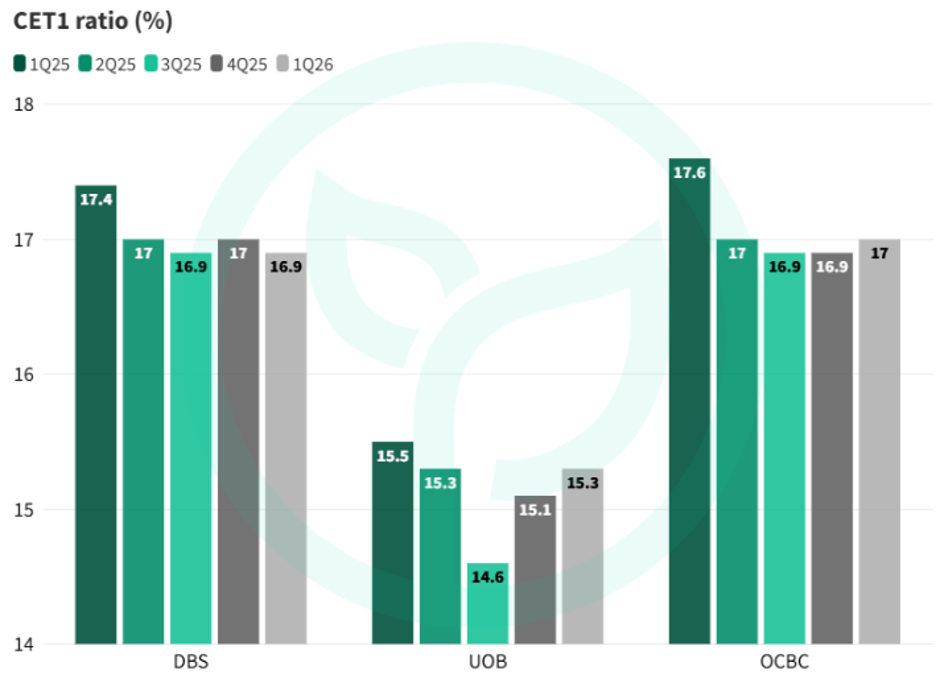

#3 - Strong capital ratios are supporting bank dividends, buybacks and capital returns

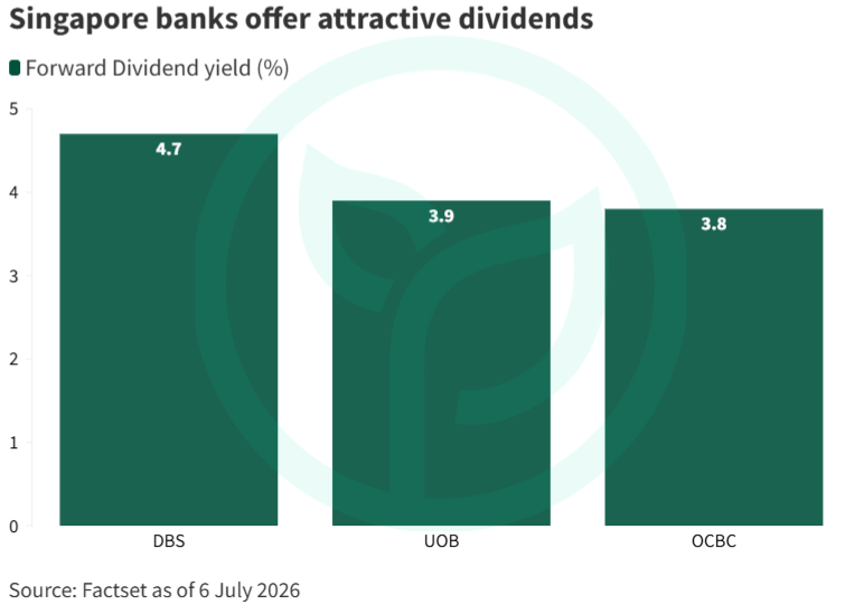

A third driver for Singapore bank stocks is their attractive dividend yields, supported by their strong capital position.

Capital returns have become a bigger part of the shareholder return story, especially as DBS, OCBC and UOB remain well capitalised despite a more challenging interest rate environment.

DBS also continues to offer a dividend yield with a meaningful spread over the Singapore 10-year government bond yield.

DBS, OCBC and UOB all have Common Equity Tier 1, or CET1, ratios comfortably above regulatory minimums.

CET1 is a key measure of how much high-quality capital a bank has to absorb losses.

For investors, a strong CET1 ratio gives the banks more flexibility to return excess capital through ordinary dividends, special dividends and share buybacks.

Related links:

What are the risks to DBS, OCBC and UOB?

#1 - Increase in Fed rate cut expectations may pressure net interest margin again

With the rally in the share prices of Singapore banks driven by rising expectations of Fed rate hikes, one key risk to the share prices of Singapore banks would be a reversal of such rate hike expectations.

If the SIBOR were to decline again, this could put renewed pressure on net interest margins, especially as asset yields reprice lower while deposit costs may not fall as quickly.

Since net interest income remains a major earnings driver for DBS, OCBC and UOB, a sharper than expected decline in margins could weigh on earnings growth.

#2 - Sharp economic slowdown may pressure wealth management fee growth and lead to increase in credit cost

While the global economy has been resilient, an unexpected sharp economic slowdown may reduce customer investment activity, which could slow wealth management fee growth.

Also, slower economic growth may affect borrowers’ repayment ability, leading to higher credit costs and more provisions for potential bad loans.

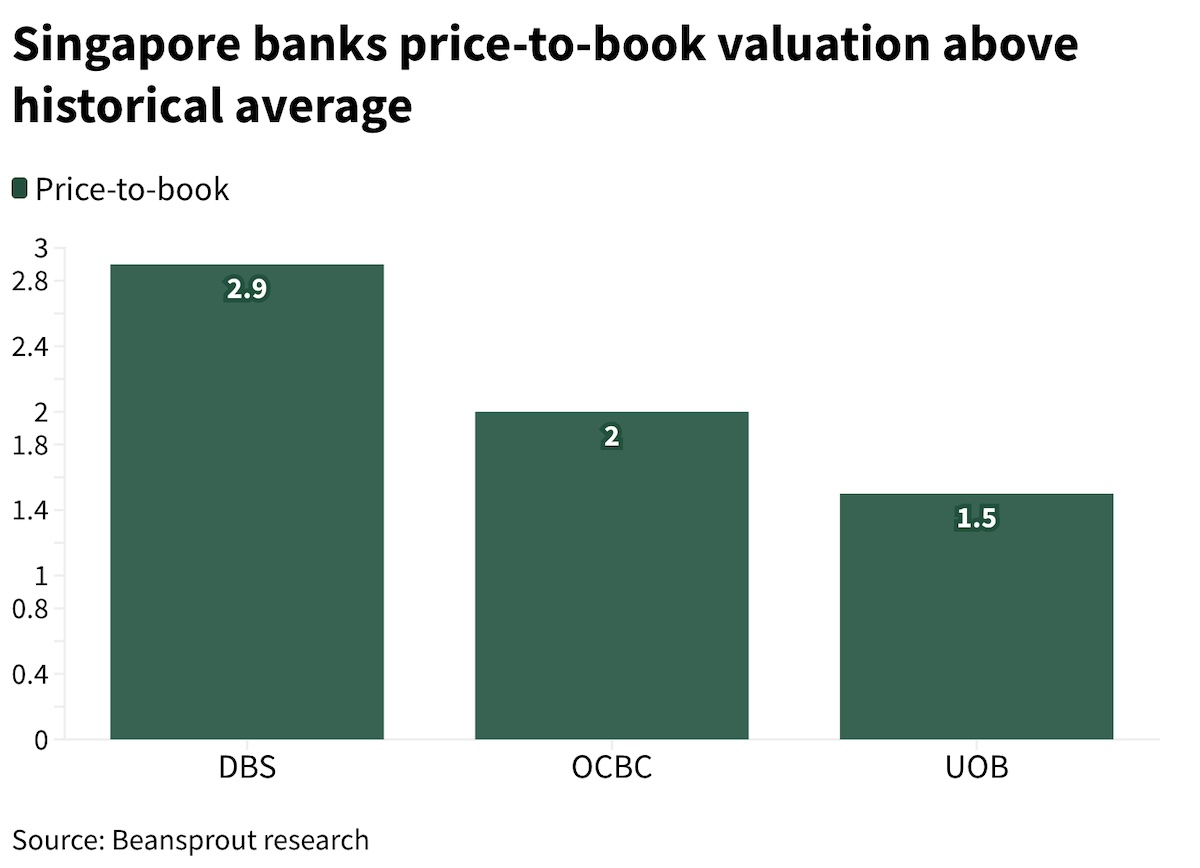

#3 - Valuations are higher than historical averages

DBS, OCBC and UOB are also trading at valuations that are higher than their historical averages.

This suggests that the market has already priced in a fairly positive outlook for earnings, dividends and capital returns.

DBS is currently trading at a price-to-book valuation of 2.9x, above its historical average of 1.9x.

If earnings growth slows, interest rates fall faster than expected, or asset quality weakens, the valuation of Singapore banks may be impacted.

What would Beansprout do?

DBS, OCBC and UOB have appealed to investors due to their attractive dividend yields.

However, with DBS, OCBC and UOB trading near record highs, the key question is whether the higher valuations can be supported by earnings growth.

A bottoming SORA, stronger wealth management income and ongoing capital returns may support profit growth and total shareholder returns for the DBS, OCBC and UOB.

This is where I would consider the banks as Opportunity Pot candidates within Beansprout four pots of wealth.

To screen for stocks for my opportunity, I would evaluate their revenue and earnings momentum, balance sheet strength and return on equity based on our opportunity pot screening framework

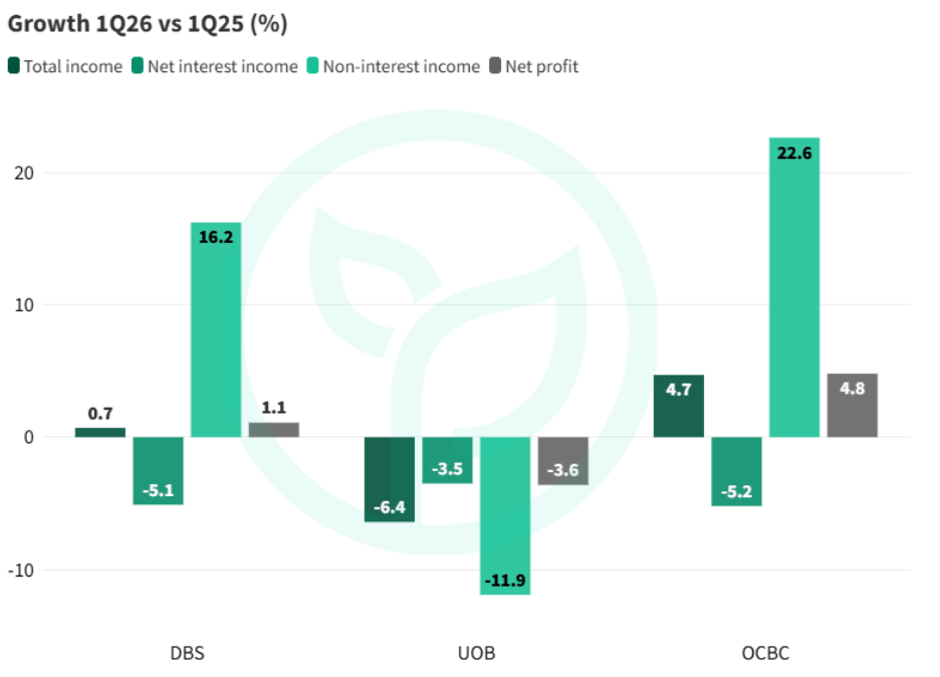

DBS and OCBC have shown stronger momentum through wealth management, fee income and non-interest income, while UOB’s 1Q26 results were more subdued.

All three banks are well capitalised, with enough excess capital to support dividends, buybacks and special capital returns.

Return on equity also separates the banks. DBS and OCBC have consistently delivered ROE above 10%, while UOB’s ROE dipped in 2025 and would need to recover more clearly.

Overall, DBS and OCBC look better positioned because they have stronger fee income momentum, higher return on equity and more consistent earnings delivery.

OCBC also has a clearer re-rating angle if capital returns and wealth expansion continue to deliver.

UOB remains cheaper and could offer catch-up potential, but it still needs to show clearer earnings recovery and better returns from its regional integration.

However, with the strong performance year-to-date, I would not chase the rally aggressively at current levels.

Instead, I would look to add gradually on pullbacks, while watching whether fee income growth can continue to offset net interest margin pressure.

Overall, the rally in DBS, OCBC and UOB reinforces our view on why Singapore stocks are still worth looking at in 2026.

Singapore’s rise as a wealth management hub is one of the structural themes that could continue to support the local banks over time. But it is not the only theme we are watching.

Beyond the banks, there may be other areas of the Singapore market supported by long-term trends, including energy and food security, AI and data centre growth, and continued infrastructure spending. Find out more about the 4 growth themes we are watching in Singapore stocks here.

For investors looking for more higher-conviction ideas, you can explore our curated stock opportunities here.

Which Singapore bank are you backing at these levels: DBS, OCBC or UOB? Share your thoughts with us in the Beansprout Telegram community.

Follow Beansprout on YouTube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Important Disclosures

Analyst Certification and Disclosures

The analyst(s) named in this report certifies that (i) all views expressed in this report accurately reflect the personal views of the analyst(s) with regard to any and all of the subject securities and companies mentioned in this report and (ii) no part of the compensation of the analyst(s) was, is, or will be, directly or indirectly, related to the specific views expressed by that analyst herein. The analyst(s) named in this report (or their associates) does not have a financial interest in the corporation(s) mentioned in this report.

An associate is defined as (i) the spouse, or any minor child (natural or adopted) or minor step-child, of the analyst; (ii) the trustee of a trust of which the analyst, his spouse, minor child (natural or adopted) or minor step-child, is a beneficiary or discretionary object; or (iii) another person accustomed or obliged to act in accordance with the directions or instructions of the analyst.

Company Disclosure

Global Wealth Technology Pte Ltd (“Beansprout”) does not have any financial interest in the corporation(s) mentioned in this report.

Disclaimer

This report is provided by Beansprout for the use of intended recipients only and may not be reproduced, in whole or in part, or delivered or transmitted to any other person without our prior written consent. By accepting this report, the recipient agrees to be bound by the terms and limitations set out herein.

You acknowledge that this document is provided for general information purposes only. Nothing in this document shall be construed as a recommendation to purchase, sell, or hold any security or other investment, or to pursue any investment style or strategy. Nothing in this document shall be construed as advice that purports to be tailored to your needs or the needs of any person or company receiving the advice. The information in this document is intended for general circulation only and does not constitute investment advice. Nothing in this document is published with regard to the specific investment objectives, financial situation and particular needs of any person who may receive the information.

Nothing in this document shall be construed as, or form part of, any offer for sale or subscription of or solicitation or invitation of any offer to buy or subscribe for any securities. The data and information made available in this document are of a general nature and do not purport, and shall not in any way be deemed, to constitute an offer or provision of any professional or expert advice, including without limitation any financial, investment, legal, accounting or tax advice, and shall not be relied upon by you in that regard. You should at all times consult a qualified expert or professional adviser to obtain advice and independent verification of the information and data contained herein before acting on it. Any financial or investment information in this document are intended to be for your general information only. You should not rely upon such information in making any particular investment or other decision which should only be made after consulting with a fully qualified financial adviser. Such information do not nor are they intended to constitute any form of financial or investment advice, opinion or recommendation about any investment product, or any inducement or invitation relating to any of the products listed or referred to. Any arrangement made between you and a third party named on or linked to from these pages is at your sole risk and responsibility.

You acknowledge that Beansprout is under no obligation to exercise editorial control over, and to review, edit or amend any data, information, materials or contents of any content in this document. You agree that all statements, offers, information, opinions, materials, content in this document should be used, accepted and relied upon only with care and discretion and at your own risk, and Beansprout shall not be responsible for any loss, damage or liability incurred by you arising from such use or reliance.

This document (including all information and materials contained in this document) is provided “as is”. Although the material in this document is based upon information that Beansprout considers reliable and endeavours to keep current, Beansprout does not assure that this material is accurate, current or complete and is not providing any warranties or representations regarding the material contained in this document. All opinions contained herein constitute the views of the analyst(s) named in this report, they are subject to change without notice and are not intended to provide the sole basis of any evaluation of the subject securities and companies mentioned in this report. Any reference to past performance should not be taken as an indication of future performance. To the fullest extent permissible pursuant to applicable law, Beansprout disclaims all warranties and/or representations of any kind with regard to this document, including but not limited to any implied warranties of merchantability, non-infringement of third-party rights, or fitness for a particular purpose.

Beansprout does not warrant, either expressly or impliedly, the accuracy or completeness of the information, text, graphics, links or other items contained in this document. Neither Beansprout nor any of its affiliates, directors, employees or other representatives will be liable for any damages, losses or liabilities of any kind arising out of or in connection with the use of this document. To the best of Beansprout’s knowledge, this document does not contain and is not based on any non-public, material information. The information in this document is not intended for distribution to, or use by, any person or entity in any jurisdiction where such distribution or use would be contrary to law or regulation, or which would subject Beansprout to any registration requirement within such jurisdiction or country. Beansprout is not licensed or regulated by any authority in any jurisdiction or country to provide the information in this document.

As a condition of your use of this document, you agree to indemnify, defend and hold harmless Beansprout and its affiliates, and their respective officers, directors, employees, members, managing members, managers, agents, representatives, successors and assigns from and against any and all actions, causes of action, claims, charges, cost, demands, expenses and damages (including attorneys’ fees and expenses), losses and liabilities or other expenses of any kind that arise directly or indirectly out of or from, arising out of or in connection with violation of these terms, use of this document, violation of the rights of any third party, acts, omissions or negligence of third parties, their directors, employees or agents. To the extent permitted by law, Beansprout shall not be liable to you, any other person, or organization, for any direct, indirect, special, punitive, exemplary, incidental or consequential damages, whether in contract, tort (including negligence), or otherwise, arising in any way from, or in connection with, the use of this document and/or its content. This includes, without limitation, liability for any act or omission in reliance on the information in this document. Beansprout expressly disclaims and excludes all warranties, conditions, representations and terms not expressly set out in this User Agreement, whether express, implied or statutory, with regard to this document and its content, including any implied warranties or representations about the accuracy or completeness of this document and the content, suitability and general availability, or whether it is free from error.

If these terms or any part of them is understood to be illegal, invalid or otherwise unenforceable under the laws of any state or country in which these terms are intended to be effective, then to the extent that they are illegal, invalid or unenforceable, they shall in that state or country be treated as severed and deleted from these terms and the remaining terms shall survive and remain fully intact and in effect and will continue to be binding and enforceable in that state or country.

These terms, as well as any claims arising from or related thereto, are governed by the laws of Singapore without reference to the principles of conflicts of laws thereof. You agree to submit to the personal and exclusive jurisdiction of the courts of Singapore with respect to all disputes arising out of or related to this Agreement. Beansprout and you each hereby irrevocably consent to the jurisdiction of such courts, and each Party hereby waives any claim or defence that such forum is not convenient or proper.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments