Gold turns volatile amid Middle East conflict. What investors should watch next

Commodities

By Ng Hui Min • 26 Mar 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

Gold prices have turned volatile as Middle East tensions rise. We examine what is driving the swings and the key factors that could move gold next.

What happened?

Gold has seen sharp swings in recent weeks.

Gold prices hit a record high of US$5,417 per ounce on 3 March 2026 after geopolitical tensions in the Middle East escalated, before falling below US$4,500 by the end of the month in its steepest weekly decline in decades.

As of 23 March, spot gold is trading around US$4,410, down more than 20% from its recent peak and having erased all its year-to-date gains.

The pullback came as several factors turned less supportive for gold, including rising oil prices and higher inflation expectations with the Middle East conflict, and lower expectations of interest rate cuts by the US Federal Reserve.

In our previous update, we discussed what could happen after gold’s rally paused. Since then, the outlook has become more uncertain, and many in the Beansprout community have asked whether this marks the end of the bull run, or a potential buying opportunity.

In this article, we look at what is driving the recent sell-off, what the data says about long-term demand for gold, and what investors may want to watch next.

What are the recent developments?

#1 — The Iran war is driving inflation fears more than safe-haven demand

When US and Israeli forces launched strikes on Iran on 28 February, markets initially expected a straightforward safe-haven rally in gold as investors got nervous and sought security.

Gold did rise at first, briefly touching US$5,417 an ounce by 3 March. But the longer the conflict dragged on, the more the market focus shifted from geopolitics to inflation and interest rates.

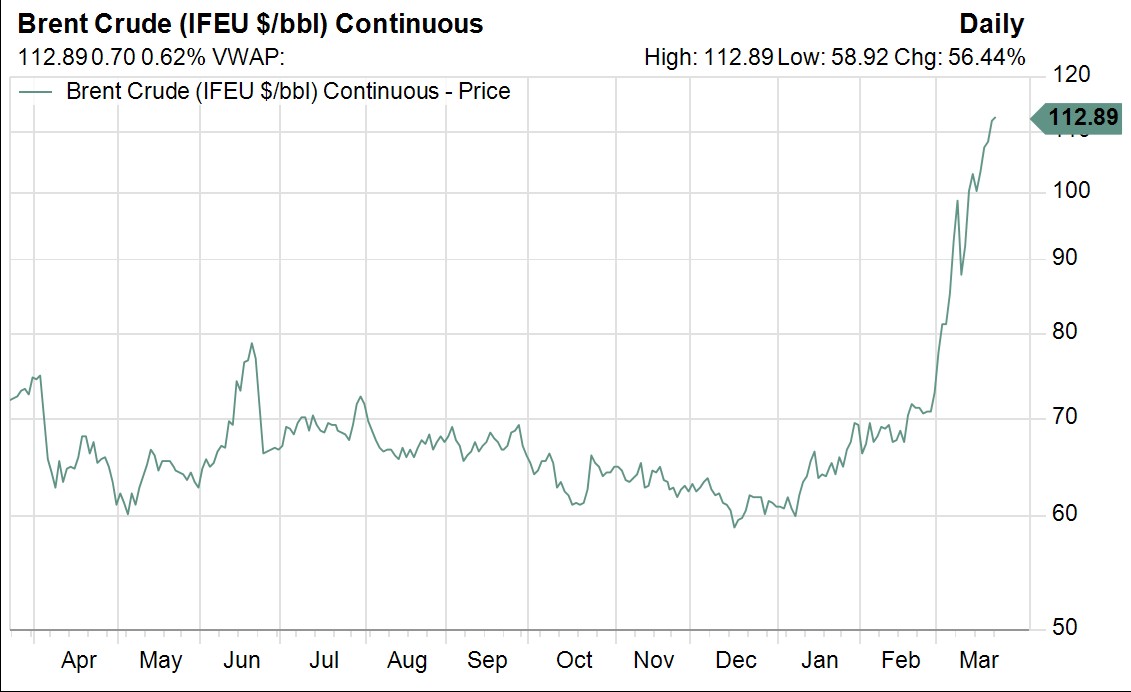

That is because the war has also pushed oil prices sharply higher. Brent crude oil price settled above US$112 on 20 March, up over 40% since the war began, as attacks on energy infrastructure raised fears of supply disruption.

For gold, this created an unexpected problem.

Higher oil prices are feeding into inflation concerns, which in turn makes the Federal Reserve less likely to cut rates.

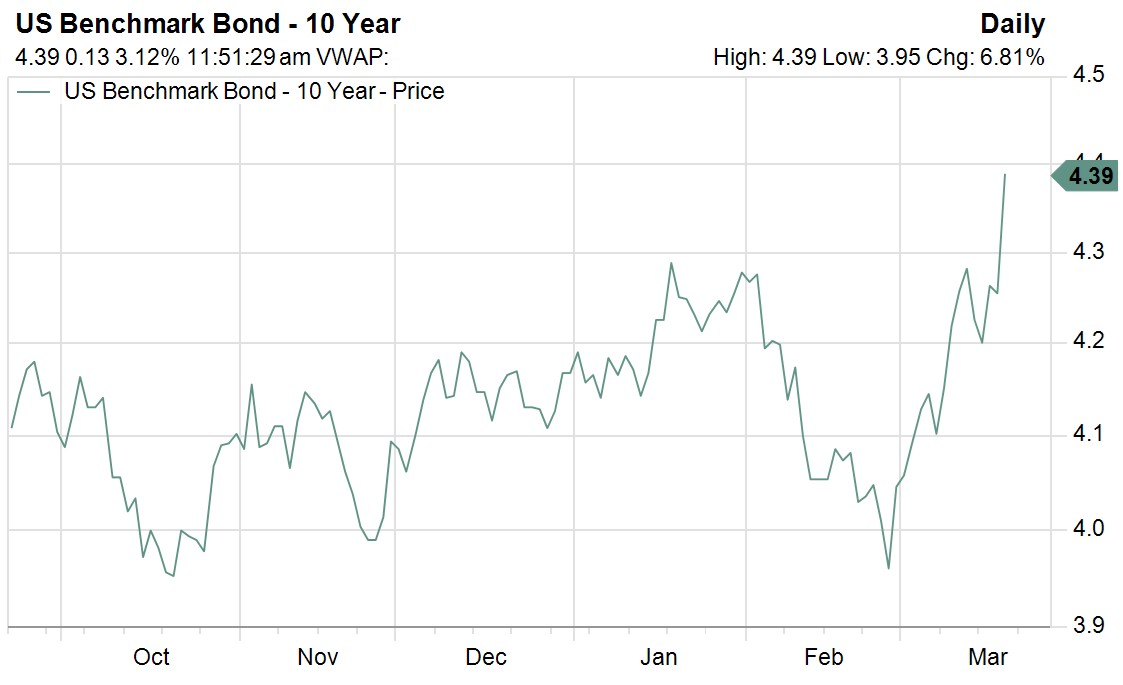

February’s producer price data added to those worries, coming in stronger than expected and pushing bond yields and the US dollar higher.

Wholesale inflation rose +0.7% month-on-month, more than double the 0.3% expected, with annual wholesale inflation at 3.4%.

That matters because gold does not pay interest or dividend. When bond yields rise and the US dollar strengthens, gold tends to face more pressure.

In other words, the same conflict that would normally support gold as a safe haven is also creating the inflation shock that is keeping the Fed hawkish. And for now, that rate headwind appears to be outweighing gold’s safe-haven appeal.

#2 — The Fed’s latest comments pushed gold below US$5,000

The Fed kept rates unchanged at 3.5 to 3.75 percent on 18 March, but the bigger surprise was its warning about higher inflation.

Officials raised their 2026 inflation forecast 2.7% for both headline and core PCE (up from 2.5% in December) and still pointed to only one rate cut this year, while Powell warned that inflation risks remain tilted to the upside.

The Fed was not the only central bank striking a cautious tone.

The ECB, BoE and BoJ also left rates unchanged that same week while warning about inflation risks, and the RBA went a step further by raising rates.

Taken together, the message from global central banks was clear: interest rates are unlikely to less likely to come down soon, and in some cases could still move higher.

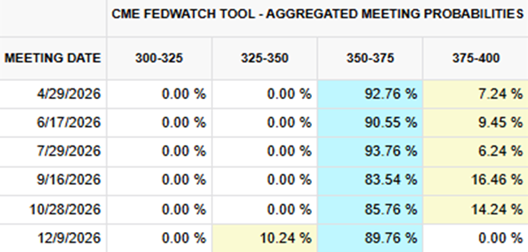

Since then, markets have turned even more cautious. Fed funds futures are now pricing in no cuts at all in 2026, as the oil shock from the Iran conflict has added to already sticky inflation pressures.

Gold fell more than 6 percent in just two days after the Fed meeting.

A big reason was that once gold dropped below the important US$5,000 level, some investors who had borrowed money to buy gold were forced to sell. That extra selling made the price fall even faster.

The World Gold Council said this kind of sharp move is similar to what happened in 2008 and 2020, when investors sold assets quickly to raise cash, even if the long-term reason for owning them had not changed.

What may help to support the price of gold?

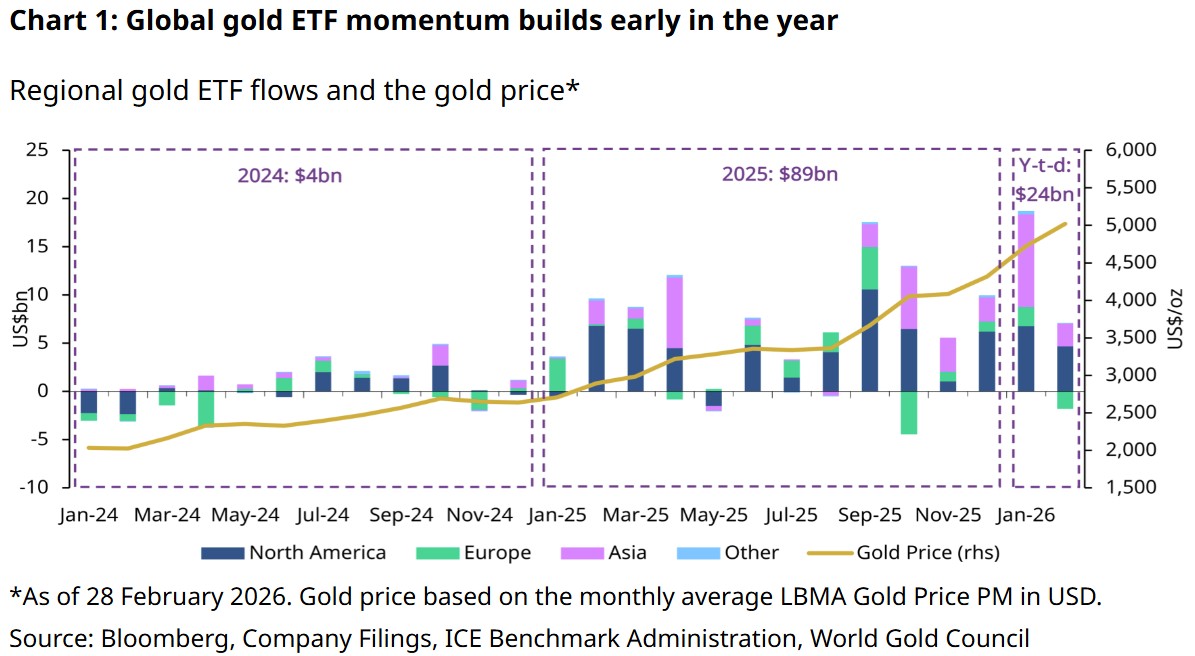

#1 — Gold ETF inflows are still coming in strongly

That marked the ninth straight month of inflows, pushed total holdings to a record 4,171 tonnes, and lifted assets under management to US$701 billion.

This followed an already strong January, suggesting investor conviction in gold remained firm even before the recent pullback.

North America remained the main driver of demand, Asia also stayed supportive, while Europe was the only region to see net outflows.

Source: Bloomberg, Company Filings, ICE Benchmark Administration, World Gold Council

In Singapore, the picture has also remained very strong.

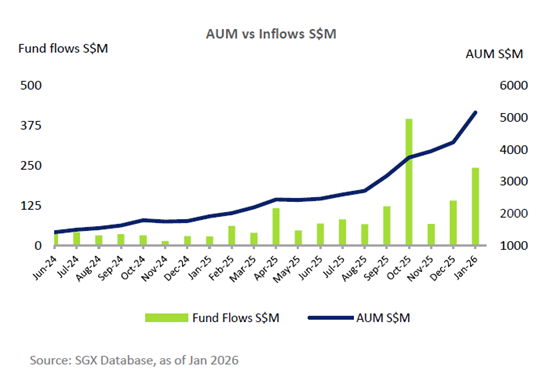

The SPDR Gold Shares ETF listed on SGX recorded its 20th straight month of net inflows in January, with S$1.6 billion added since June 2024.

Assets under management on SGX crossed S$5 billion for the first time, while daily trading turnover surged to the highest level since 2011.

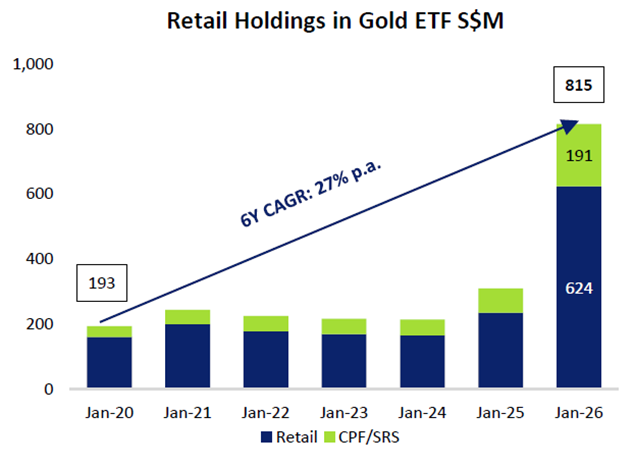

What stands out even more is that retail participation reached a record S$815 million, with a meaningful share funded through SRS or CPF-OA.

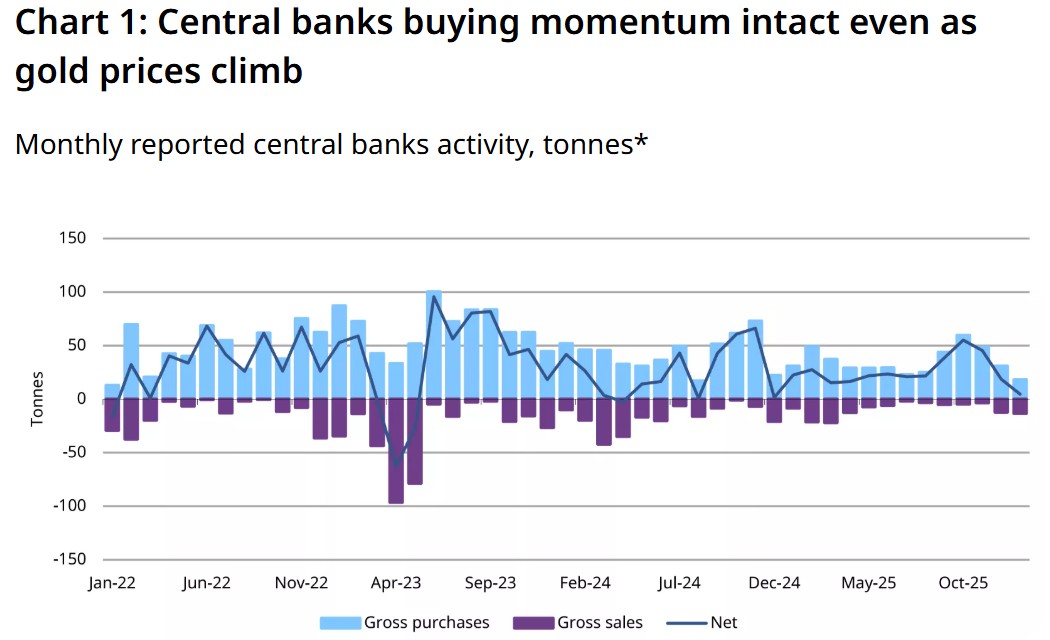

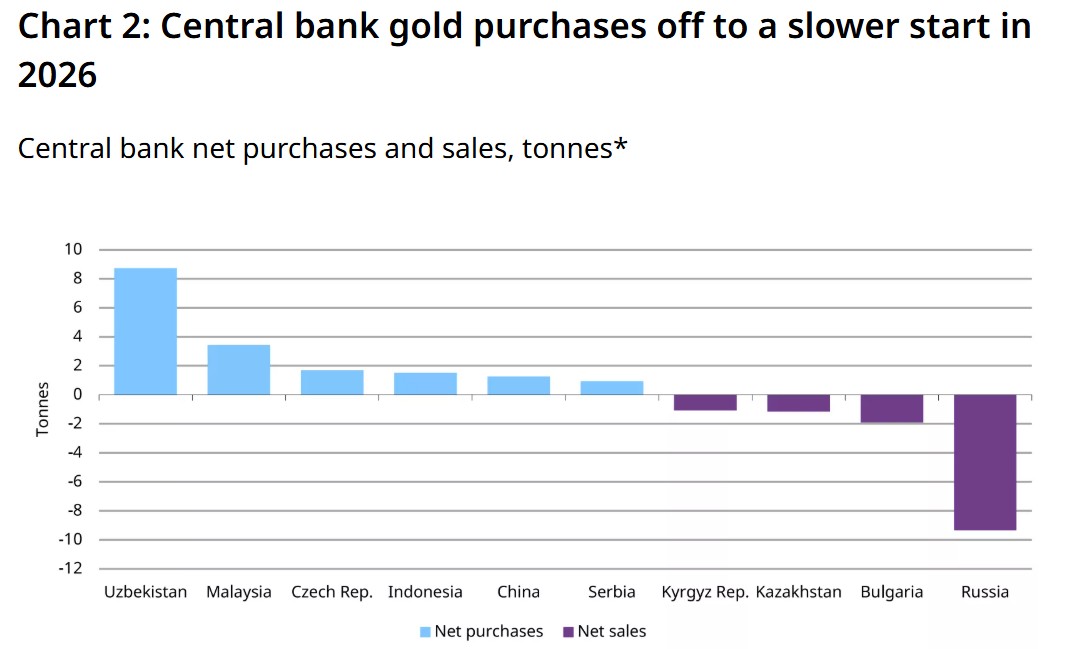

#2 — Central bank demand remains supportive

The latest World Gold Council data showed that central banks bought a net 5 tonnes of gold in January 2026, below the 2025 monthly average of 27 tonnes.

Source: IMF, respective central banks, World Gold Council

But what stands out is that the base of buyers is widening again.

Malaysia returned to the market for the first time since 2018, while South Korea announced plans to gain exposure through overseas-listed physical gold ETFs.

Other buyers included Uzbekistan, the Czech Republic, Indonesia, and China, which extended its buying streak to 15 consecutive months.

That matters more than the softer monthly pace.

Full-year 2025 central bank purchases still reached 863 tonnes, well above the historical average, and survey data suggests most central banks expect global gold reserves to keep rising over the next year.

For investors, this reinforces the idea that official sector demand remains a structural support for gold, even if purchases become more uneven from month to month.

Source: IMF, respective central banks, World Gold Council

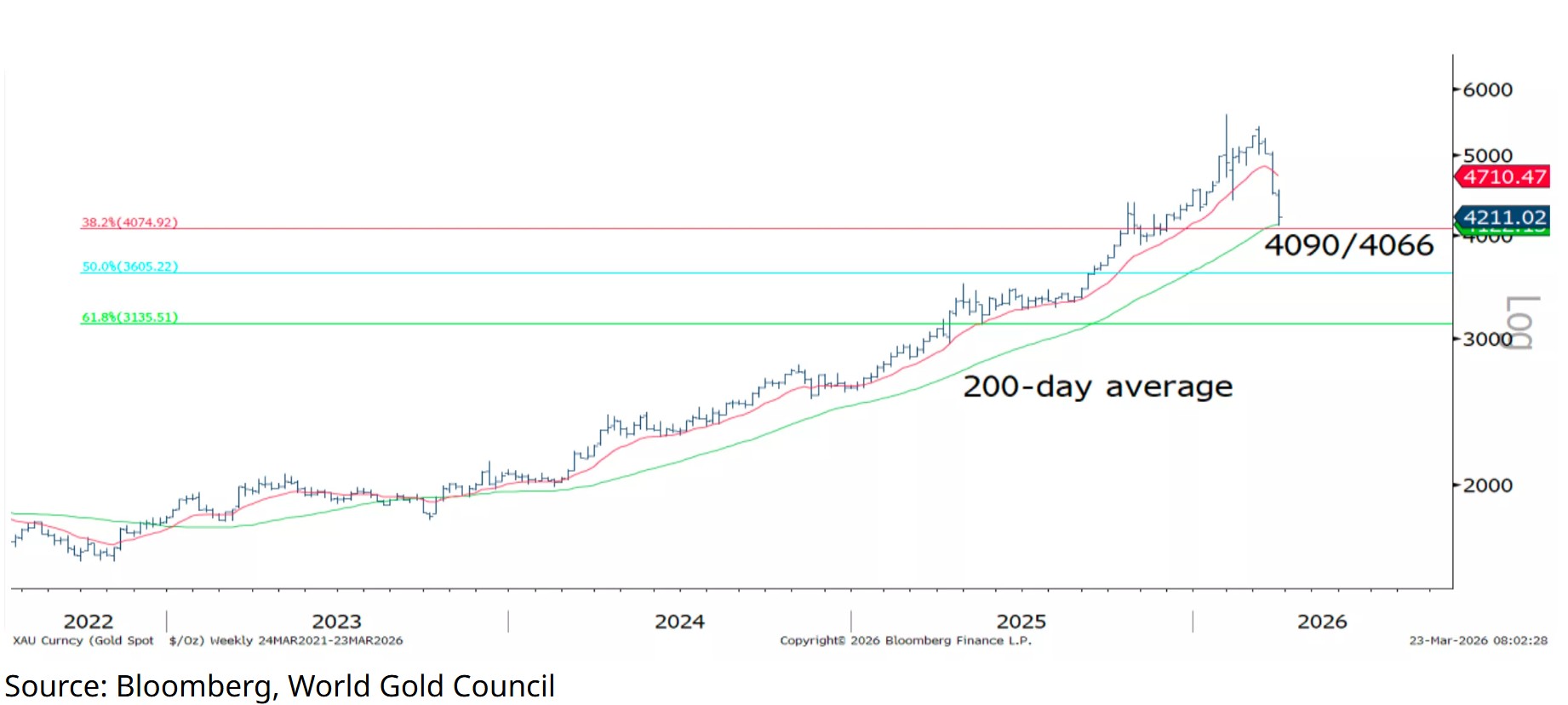

Gold price technicals - Where is the support?

The next key support zone many analysts are watching is around US$4,090 to US$4,066.

This area includes both the 200-day moving average and an important Fibonacci retracement level from gold’s broader rally since 2022.

Gold tested that zone on 23 March and then bounced back to around US$4,490.

But if it were to break clearly below US$4,066, it could open the way for a deeper pullback towards US$3,500, which was roughly where the 2025 to 2026 rally began.

What would Beansprout do?

In the short term, gold is facing several pressures at once. Markets are no longer expecting rate cuts in 2026, oil is still above US$100, the US dollar is strong, and real yields have moved higher.

Those are all negative for gold, and they could keep prices under pressure for a while.

But the longer-term reasons for owning gold have not disappeared.

Central banks are still buying. Investors are still putting money into gold ETFs. US deficits are still large. And the world remains uncertain, with more geopolitical tension and fragmentation.

For longer-term investors, I still see gold as a useful diversifier within our basket of growth assets rather than a short-term trade, but only with patience and a multi-year horizon.

In a volatile market like this, I would be more comfortable building exposure gradually through dollar-cost averaging, rather than trying to guess the perfect entry point with a lump sum.

Spreading purchases out over time can help reduce the risk of buying at the wrong moment, and this recent support zone gives me a useful reference point if I were thinking about starting or adding slowly.

I would also keep the allocation modest, at around 5 to 10 percent. Gold does not generate income, so I would see it mainly as a long-term diversifier alongside equities and index funds, rather than a core return driver.

If you are looking to invest in gold in a simple way, learn more about the LionGlobal Singapore Physical Gold ETF, which is backed by allocated physical gold that is fully insured and vaulted in Singapore, and the SPDR Gold Shares ETF, which is SRS-eligible and CPF-OA approved.

We previously compared the LionGlobal Singapore Physical Gold ETF and the SPDR Gold shares here. You can also find out how to choose best gold ETF for your portfolio here.

For other ways to buy gold, learn how to buy gold in Singapore here. You can also learn how to buy physical gold from UOB with our step by step guide here.

Check out Beansprout's guide to the best stock trading platforms in Singapore with the latest promotions to invest in gold ETFs.

Enjoyed this insight? Follow Beansprout on Telegram, Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments