4 Singapore REITs selling assets that may impact dividends. Which REIT looks more attractive for income

REITs

By Goh Lay Peng • 15 Jul 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

We look at four Singapore REITs selling assets above valuation and assess the impact on DPU, gearing, dividend yields and their income appeal.

What happened?

Singapore REITs are stepping up their asset recycling efforts.

We previously looked at three REITs making acquisitions that could lift their dividends in 2026.

More recently, there are also many REITs that have announced the sale or proposed sale of properties from their portfolios.

Selling an asset can help a REIT unlock value, reduce debt, avoid future capital expenditure or redeploy its proceeds into properties with stronger growth prospects.

However, a disposal may also reduce rental income, especially when the property being sold is income-producing.

With Singapore REITs selling assets at a premium to valuation, many income investors in the Beansprout community are asking what these disposals could mean for unitholders.

In this article, I look at four Singapore REITs making recent disposals and how the deals could affect their distribution per unit, or DPU, and dividend yields, and which REIT may look more attractive for income.

#1 - Elite UK REIT (SGX: MXNU) sells vacant Edinburgh property

Elite UK REIT owns a portfolio of predominantly freehold commercial properties across the United Kingdom.

A large part of its rental income comes from UK government-related tenants, although the REIT is also repositioning selected assets for alternative uses.

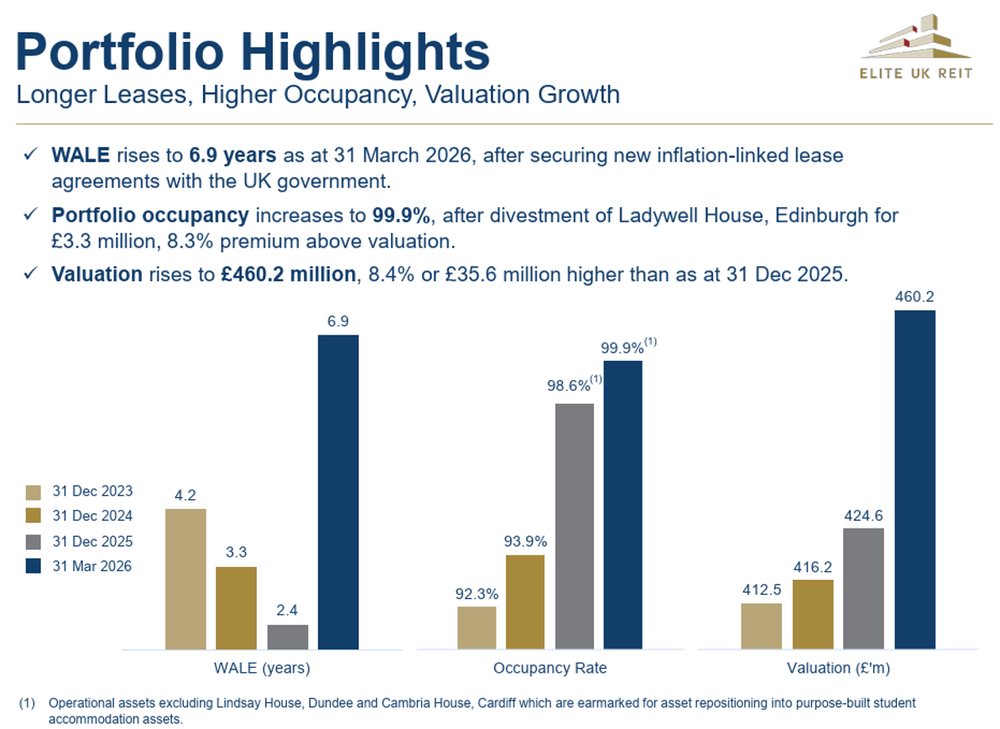

Elite UK REIT completed the sale of Ladywell House in Edinburgh for £3.3 million in March 2026.

The sale price was 8.3% above the property’s independent valuation of about £3.0 million as at February 2026.

Ladywell House was vacant when it was sold. This means that Elite UK REIT was able to raise proceeds from the sale without giving up existing rental income.

The disposal follows Elite UK REIT’s broader strategy of selling selected vacant properties while repositioning other assets for alternative uses.

Following the disposal, the occupancy rate of Elite UK REIT’s operational portfolio increased to 99.9% as at 31 March 2026.

As Ladywell House was vacant, its disposal is unlikely to have a significant negative impact on Elite UK REIT’s rental income.

Instead, the transaction could help the REIT reduce property holding costs and provide additional funds for debt repayment or its asset repositioning projects.

Elite UK REIT’s distributable income rose by 9.8% year-on-year in the first quarter of 2026.

Adjusted net property income, which excludes straight-line rent adjustments, lease incentives and vacant property holding costs, also increased by 4.0% year-on-year.

This was partly supported by lower borrowing costs and lower property holding expenses following earlier asset disposals.

However, Elite UK REIT does not declare a distribution for the first and third quarters. We would therefore have to wait for its half-year results to see whether the improvement in distributable income translates into higher DPU.

For FY2025, Elite UK REIT’s DPU rose by 5.6% to 3.03 pence from 2.87 pence in FY2024.

It meets the first criterion in Beansprout’s REIT income screening framework, which looks for stable or growing DPU.

Elite UK REIT’s net gearing declined to 37.4% as at 31 March 2026, from 40.7% at the end of 2025.

Its aggregate leverage stood at 37.7%, while about 92% of its interest-rate exposure was fixed.

Its interest coverage ratio remained at 2.6 times, and it had no debt refinancing requirements until 2027.

With gearing below 45%, Elite UK REIT would also meet the balance sheet criterion under Beansprout’s REIT income screening framework.

However, I would continue to watch the costs associated with its asset repositioning strategy.

Elite UK REIT is exploring alternative uses for selected properties, including student accommodation and data centres. While these projects could unlock value, they may also require additional capital before generating income.

Elite UK REIT was trading at £0.310 as of 13 July 2026.

Based on the consensus forecast DPU of £0.030 for 2026, Elite UK REIT offers a forward dividend yield of approximately 9.7%. This is slightly above its historical average dividend yield of 9.6%.

The yield is also significantly higher than those offered by many larger Singapore REITs, as well as the latest yields on T-bills, Singapore Savings Bonds and fixed deposits.

Based on the Beansprout REIT income screening framework, the yield would offer a sizeable premium over lower-risk alternatives.

However, the higher yield also reflects the risks faced by the REIT.

These include tenant concentration, lease expiries, foreign exchange exposure and uncertainty over the returns from its asset repositioning plans.

Overall, the Ladywell House sale appears constructive because Elite UK REIT has removed a vacant property without giving up meaningful rental income.

The transaction alone is unlikely to cause a large jump in DPU, but lower holding and borrowing costs could support its distributions over time.

Find out how much dividends you would have received as a shareholder of Elite UK REIT in the past 12 months with the calculator below.

Related links:

#2 - OUE REIT (SGX: TS0U) proposes to sell Crowne Plaza Changi Airport

OUE REIT owns a diversified portfolio of commercial and hospitality properties in Singapore and Australia.

Its assets include office buildings, retail space and hotels, giving it exposure to both recurring commercial rents and the hospitality sector.

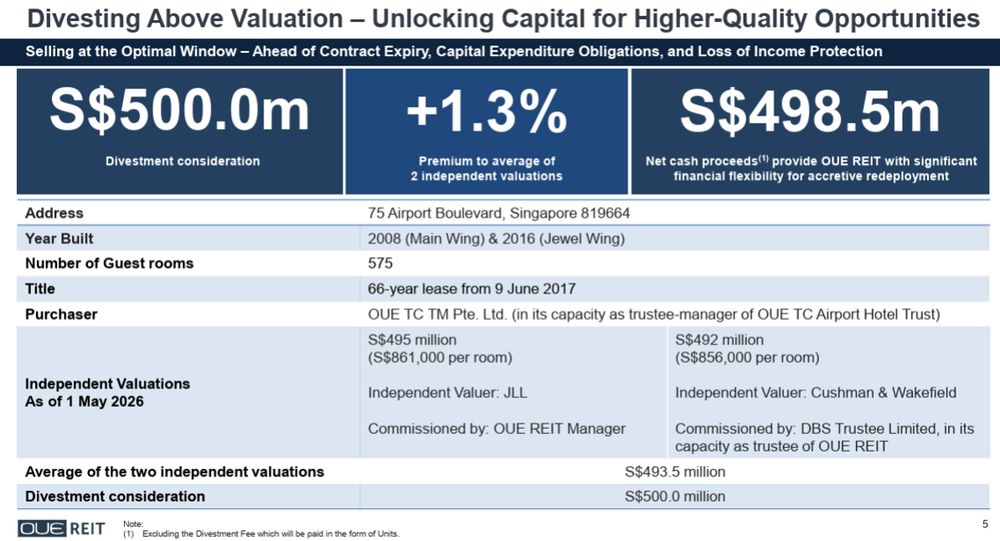

In June 2026, OUE REIT has proposed selling Crowne Plaza Changi Airport for S$500 million.

The 575-room hotel is located next to Changi Airport Terminal 3 and is connected to both Terminal 3 and Jewel Changi Airport.

The sale price represents a premium of about 1.3% to the average of two independent valuations.

OUE REIT expects to receive net cash proceeds of approximately S$498.5 million after transaction costs, excluding the divestment fee that will be paid in units.

As the proposed buyer is linked to OUE REIT’s sponsor, the disposal is subject to approval from independent unitholders.

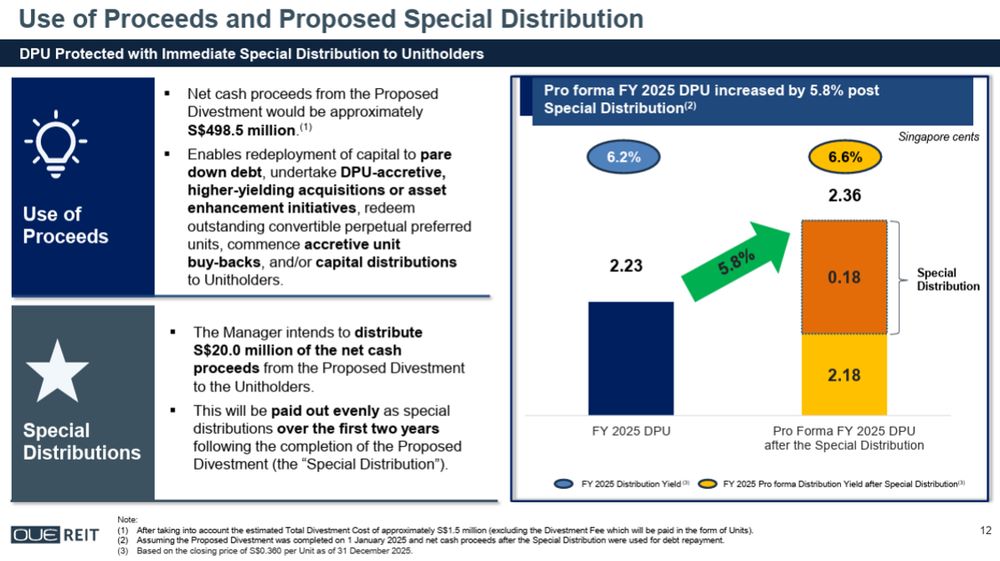

OUE REIT intends to return approximately S$20 million of the disposal proceeds to unitholders.

The amount is expected to be paid evenly as special distributions over the first two years following completion of the sale.

Based on OUE REIT’s pro forma figures, its FY2025 DPU would have fallen from 2.23 cents to 2.18 cents after accounting for the disposal and debt repayment.

However, including the first S$10 million special distribution, pro forma DPU would have risen to 2.36 cents.

This represents a 5.8% increase compared with its reported FY2025 DPU.

However, it is important to separate this special distribution from OUE REIT’s recurring DPU.

Crowne Plaza Changi Airport is an income-producing property. After selling it, OUE REIT will no longer receive the hotel’s net property income.

Hence, the disposal could lift the total distribution received by unitholders during the first two years, but the underlying recurring DPU would have been slightly lower.

This distinction is important under the Beansprout REIT income screening framework, as I would focus on whether recurring DPU can be sustained after the special distributions end.

OUE REIT’s FY2025 DPU increased by 4.7% to 2.23 cents, supported by lower finance costs and stronger contributions from its commercial properties.

Its first-quarter 2026 revenue and net property income also rose by 6.7% and 8.4% year on year respectively.

This means that OUE REIT entered the proposed transaction with improving operating momentum.

However, under the Beansprout REIT income screening framework, I would focus on the recurring DPU of 2.18 cents after the disposal rather than the higher payout that includes the temporary special distribution.

OUE REIT may use the remaining proceeds to repay debt, fund acquisitions or asset enhancement initiatives, redeem its convertible perpetual preferred units, buy back units or make further capital distributions.

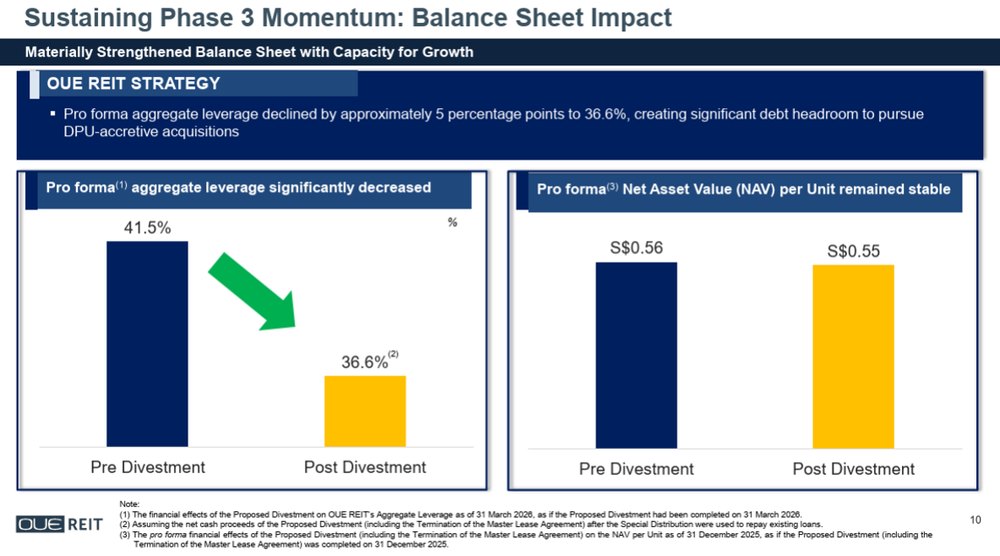

If the proceeds after the special distribution were used to repay existing debt, OUE REIT’s aggregate leverage would fall from 41.5% to 36.6%, based on its balance sheet as at March 2026.

Its net asset value per unit would remain broadly stable at S$0.55, compared with S$0.56 before the transaction.

This would bring its gearing comfortably below the 45% level used in Beansprout’s REIT income screening framework.

It would also provide OUE REIT with more debt headroom to pursue future acquisitions or asset enhancement initiatives.

The balance sheet improvement is significant because OUE REIT’s gearing had risen following its acquisition of a stake in Salesforce Tower in Sydney.

However, the final impact will depend on how much of the proceeds is actually used to repay debt.

OUE REIT was trading at S$0.365 as of 13 July 2026.

Based on the consensus forecast DPU of S$0.025 for 2026, OUE REIT offers a forward dividend yield of approximately 6.8%. This is broadly in line with the 6.9% forward yield shown on Beansprout based on a share price of S$0.360 on 10 July 2026.

This forecast yield does not include the proposed special distributions from the sale of Crowne Plaza Changi Airport.

Based on OUE REIT’s pro forma estimates, including the first S$10 million special distribution would have lifted its FY2025 distribution yield from 6.2% to 6.6%, based on a unit price of S$0.360.

However, I would use OUE REIT’s underlying forward yield when assessing whether its distributions are sustainable, as the special distributions are expected to last for only two years.

OUE REIT’s forward yield offers a premium over T-bills, Singapore Savings Bonds and fixed deposits.

However, part of the potential uplift comes from the temporary special distribution.

However, OUE REIT will need to replace Crowne Plaza Changi Airport’s income contribution to maintain its recurring DPU after the special distributions end.

Overall, OUE REIT offers the clearest near-term distribution uplift among the four transactions.

The proposed sale could also materially strengthen its balance sheet. However, the REIT will still need to replace the hotel’s contribution to support recurring DPU growth over the longer term.

Find out how much dividends you would have received as a shareholder of OUE REIT in the past 12 months with the calculator below.

Related links:

#3 - Frasers Centrepoint Trust (SGX: J69U) proposes to sell White Sands

Frasers Centrepoint Trust, or FCT, owns a portfolio of suburban retail malls in Singapore.

Its properties are generally located near transport nodes and residential areas, which helps support steady shopper traffic and tenant demand.

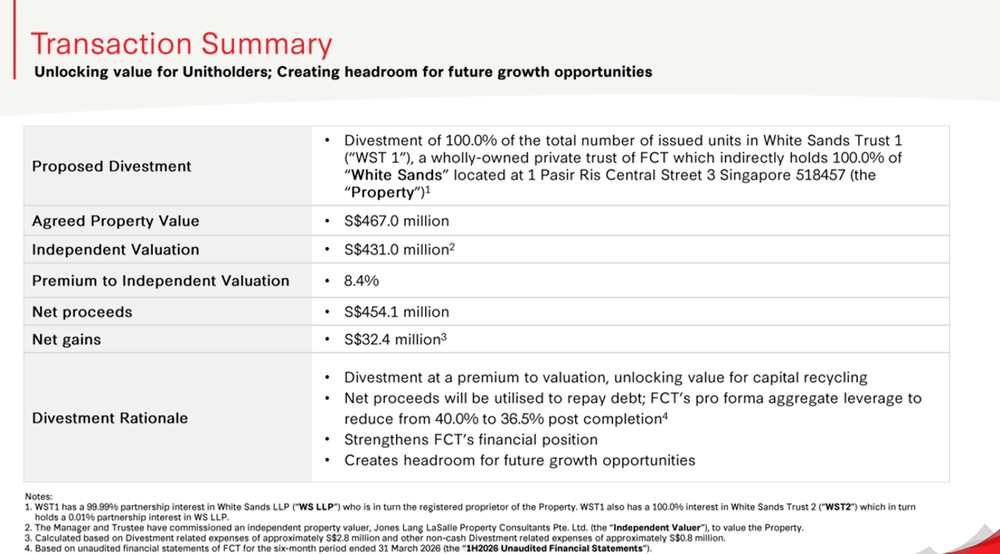

In June 2026, Frasers Centrepoint Trust has proposed selling White Sands mall in Pasir Ris for S$467 million.

The agreed property value represents an 8.4% premium to the mall’s independent valuation of S$430.7 million as at May 2026.

After deducting transaction costs and the divestment fee, FCT expects to receive net proceeds of approximately S$454.1 million.

The transaction is also expected to generate a net gain of approximately S$32.4 million.

FCT intends to use the net proceeds mainly to repay debt.

White Sands is an established suburban retail mall with committed occupancy of 100% as at 31 March 2026.

Unlike Elite UK REIT’s sale of a vacant property, FCT would lose the rental income generated by White Sands after completing the transaction.

Based on FCT’s pro forma estimates, FY2025 DPU would have declined from 12.113 cents to 11.889 cents if the disposal and debt repayment had taken place at the start of the financial year. This represents a decline of 1.9%.

Hence, while FCT is selling White Sands above valuation, the transaction is not expected to immediately lift recurring DPU.

Before accounting for the disposal, FCT’s DPU rose by 1.4% year on year to 6.136 cents in the first half of FY2026.

Net property income increased by 20.2%, while its portfolio achieved positive rental reversions of 6.5% and committed occupancy of 99.8%.

FCT’s remaining suburban retail portfolio continues to perform well.

Based on its latest DPU growth, FCT would meet the first criterion in Beansprout’s REIT income screening framework.

However, I would monitor whether FCT can maintain this growth once the contribution from White Sands is removed.

The longer-term impact will depend on whether FCT can reinvest its additional debt headroom into assets that generate a higher return than the income it gives up.

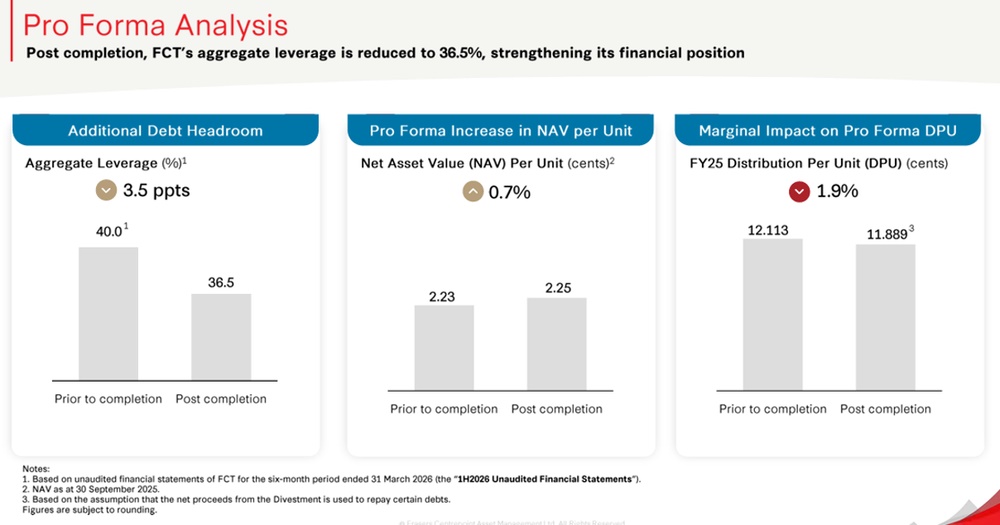

Assuming the proceeds are used to repay debt, FCT’s aggregate leverage would decline from 40.0% to 36.5%.

Its net asset value per unit would also increase by 0.7%, from S$2.23 to S$2.25.

The lower gearing would give FCT more room to fund acquisitions and ongoing asset enhancement initiatives, including the redevelopment work at Hougang Mall and NEX.

FCT would continue to meet Beansprout’s preferred gearing criterion of below 45%, with a larger buffer following the transaction.

The balance sheet improvement could also lower interest expenses.

However, the interest savings are not expected to fully replace White Sands’ rental contribution in the near term, based on the pro forma DPU figures.

The transaction therefore appears to be more focused on strengthening FCT’s balance sheet and creating capacity for future growth.

FCT was trading at S$2.260 as of 13 July 2026. Based on the consensus forecast DPU of S$0.120 for FY2026, FCT offers a forward dividend yield of approximately 5.3%. This is slightly below its historical average dividend yield of 5.4%.

Its forward dividend yield also remains above the latest yields offered by T-bills, Singapore Savings Bonds and fixed deposits. However, the yield premium is narrower than that offered by Elite UK REIT and OUE REIT.

Overall, FCT’s proposed sale of White Sands is more of a balance sheet and capital recycling exercise than an immediate DPU-accretive transaction.

The REIT is selling the mall at a healthy premium to valuation and lowering its gearing, but it will need to deploy the capital effectively to replace the lost income.

Find out how much dividends you would have received as a shareholder of Frasers Centrepoint Trust in the past 12 months with the calculator below.

Related links:

- Frasers Centrepoint Trust latest valuation, share price and analysis

- Frasers Centrepoint Trust dividend history and forecast

#4 - Parkway Life REIT (SGX: C2PU) sells older Japanese nursing home

Parkway Life REIT owns healthcare properties across Singapore, Japan and France.

Its portfolio includes private hospitals, nursing homes and other healthcare-related assets, supported by long leases and rental escalation mechanisms.

Parkway Life REIT has sold Etoile Suma Rikyu, a nursing home in Hyogo Prefecture, Japan, for JPY1.17 billion, or approximately S$9.4 million.

The property was completed in 1989 and was acquired by Parkway Life REIT in 2008.

The sale price was 5% above the property’s latest independent valuation and 38% above its original purchase price.

The disposal is expected to generate an estimated gain of approximately S$0.6 million before tax.

Parkway Life REIT said the property had reached a mature stage in its life cycle.

Selling it would allow the REIT to unlock value while reducing future capital expenditure commitments.

The REIT expects to receive approximately S$9.2 million in net proceeds, which it intends to use to pursue higher-growth opportunities.

However, Parkway Life REIT does not expect the disposal to have a material impact on its net tangible assets or DPU for the financial year ending 31 December 2026.

The transaction is relatively small compared with Parkway Life REIT’s overall portfolio. It is therefore unlikely to impact distributions.

Instead, the potential benefit comes from avoiding future capital expenditure and redeploying the proceeds into assets with stronger growth prospects.

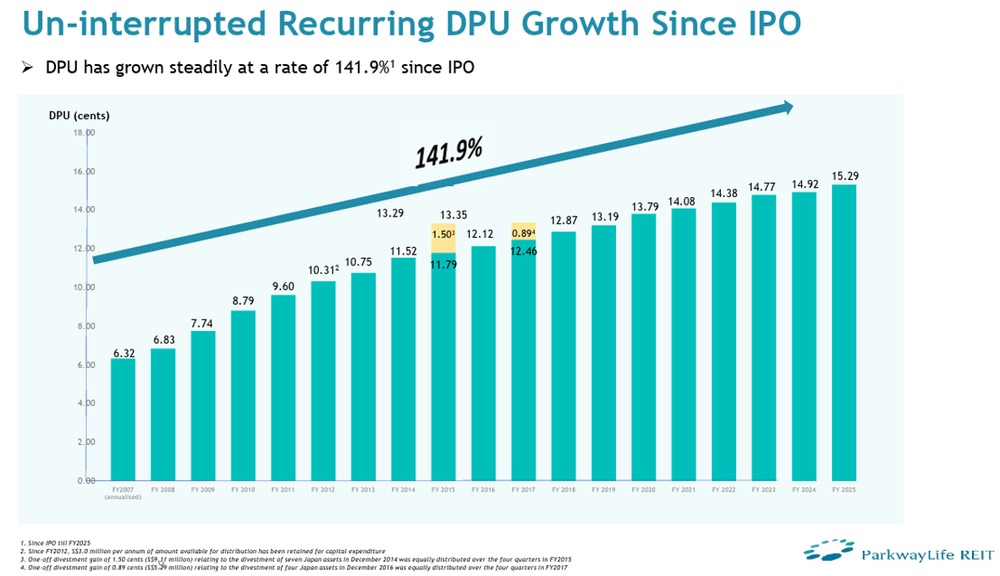

Parkway Life REIT’s DPU has demonstrated a consistent growth record.

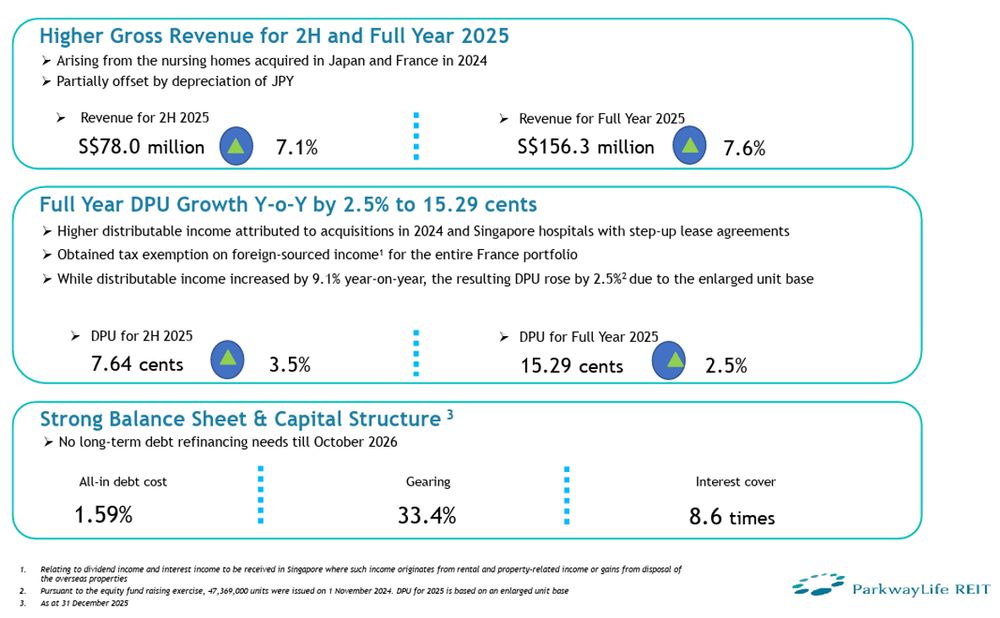

Parkway Life REIT’s FY2025 DPU rose by 2.5% to 15.29 cents, from 14.92 cents in FY2024. It has also delivered uninterrupted recurring DPU growth since its listing in 2007.

Its first-quarter 2026 DPU also increased to 4.42 cents, compared with 3.84 cents in the same period in 2025.

The increase was supported by contributions from recent acquisitions and higher rental income from its Singapore hospital properties.

Parkway Life REIT would therefore meet the DPU-growth criterion under Beansprout’s REIT income screening framework.

Parkway Life REIT’s gearing stood at 33.4% as at 31 December 2025.

Its all-in debt cost was 1.59%, while its interest coverage ratio stood at 8.6 times. About 93% of its interest-rate exposure was hedged as at the end of 2025.

This remains below the 45% level used in Beansprout’s REIT income screening framework.

Its gearing has risen in recent years as the REIT expanded its healthcare portfolio in Japan and France.

Nevertheless, Parkway Life REIT benefits from long leases and built-in rental escalation mechanisms, which provide visibility over its rental income.

The disposal of Etoile Suma Rikyu is too small to materially change the REIT’s gearing on its own.

However, it shows that the manager is willing to recycle capital from older properties instead of retaining every asset indefinitely.

Based on the consensus forecast DPU of 18.0 cents for 2026 and a unit price of S$4.12 as of 13 July 2026, Parkway Life REIT offers a forward dividend yield of approximately 4.4%. This is above its historical average dividend yield of 3.9%.

Parkway Life REIT has historically traded at a lower yield than many other Singapore REITs.

This reflects its long record of DPU growth, long lease terms and exposure to healthcare properties.

More recently, its unit price has declined as higher interest rates and acquisition-related debt weighed on investor sentiment, lifting its distribution yield.

Based on the Beansprout REIT income screening framework, I would assess whether the REIT’s consistent DPU growth and defensive lease structure justify its lower yield.

I would also consider risks such as foreign exchange exposure and the higher debt taken on to fund recent acquisitions.

Overall, the sale of Etoile Suma Rikyu is unlikely to impact Parkway Life REIT’s DPU in the near term.

However, disposing of a mature asset with increasing capital expenditure requirements could help protect portfolio returns and support distribution growth over a longer period.

Find out how much dividends you would have received as a shareholder of Parkway Life REIT in the past 12 months with the calculator below.

Related links:

- Parkway Life REIT latest valuation, share price and analysis

- Parkway Life REIT dividend history and forecast

What would Beansprout do?

With asset disposals potentially impacting dividends in different ways, I would look beyond the sale price to assess which REIT appears more attractive for income.

I would focus on the income being given up, how the proceeds will be used and whether the transaction strengthens the REIT’s DPU outlook and balance sheet.

| REIT | Asset sold | Sale price versus valuation | Potential DPU impact | Balance sheet impact |

| Elite UK REIT | Ladywell House | 8.3% premium | Potentially positive as the asset was vacant and incurring holding costs | Proceeds provide added financial flexibility |

| OUE REIT | Crowne Plaza Changi Airport | 1.3% premium to average valuation | Special distributions impact total payout temporarily, but recurring pro forma DPU falls | Gearing could fall from 41.5% to 36.6% |

| Frasers Centrepoint Trust | White Sands | 8.4% premium | Pro forma DPU falls by 1.9% before reinvestment | Gearing could fall from 40.0% to 36.5% |

| Parkway Life REIT | Etoile Suma Rikyu | 5.0% premium | No material near-term DPU impact expected | Limited immediate impact due to the transaction’s small size |

Among the four, Elite UK REIT’s disposal appears the most supportive of recurring income because Ladywell House was vacant. The sale may reduce holding costs without removing an existing source of rental income. Elite UK REIT also offers the highest forward dividend yield among the four at about 9.7%, although this reflects risks such as tenant concentration, foreign exchange exposure and its asset repositioning plans.

OUE REIT offers the clearest near-term distribution uplift through its planned special distributions with its forward dividend yield at about 6.8%, excluding the proposed special distributions. However, I would focus on its recurring DPU after Crowne Plaza Changi Airport is sold, as the special distributions are expected to last for only two years.

FCT’s sale of White Sands strengthens its balance sheet significantly, but its pro forma figures show that DPU would decline before the proceeds are reinvested. Its forward dividend yield of about 5.3%. I would watch whether FCT can deploy its additional debt headroom into acquisitions or asset enhancements that replace the lost income.

Parkway Life REIT continues to screen well for DPU growth, while its latest disposal reflects a disciplined approach to managing older assets. Its forward dividend yield of about 4.4% is the lowest among the four. The transaction is unlikely to materially change its DPU or gearing because of its small size.

One-off disposal gains and special distributions may provide additional income, but they should not replace the need for a sustainable underlying rental income stream.

Overall, I would only consider these REITs as Income Pot candidates within Beansprout’s Four Pots of Wealth when they demonstrate recurring DPU growth, manageable gearing and an attractive distribution yield.

You can learn more about how I check the three simple checks I use to screen Singapore REITs for passive income here.

To screen for Singapore REITs with lowest price-to-book valuation or highest dividend yield, check out our best Singapore REIT screener.

We still see Singapore stocks as a core part of a globally diversified portfolio, especially for investors looking for dividend income.

However, rather than relying too heavily on REITs alone, I would build a broader mix of income sources, including quality Singapore blue-chip stocks with sustainable dividends, resilient earnings and strong balance sheets. Learn more about how to build passive income streams with our income pot here.

If you are looking for more Singapore stock ideas linked to long-term growth themes, you can explore our high-conviction curated stock opportunities here.

Is there a Singapore REIT you are looking out for in the second half of 2026? Share with us in the comments below or in our Telegram group!

If you are new to investing in Singapore REITs, you can start to learn more about Singapore REITs here.

If you prefer diversification without picking individual REITs, you can also gain exposure through Singapore REIT ETFs.

Planning to invest in Singapore blue chip REITs? Compare the best Singapore brokers to find the right trading platform, and see the latest promotions and sign-up rewards available.

Follow Beansprout on YouTube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments