Keppel vs Sembcorp Industries: Which blue chip stock is a better buy with the pullback

Stocks

By Goh Lay Peng • 12 Jul 2026

Global Wealth Technology Pte. Ltd. is regulated by the Monetary Authority of Singapore (MAS) as a licensed Financial Adviser.

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

We compare Keppel and Sembcorp Industries after their share price pullback, looking at earnings, debt, ROE and AI infrastructure exposure, to see which the blue chip stock more attractive for growth.

What happened?

Not all Singapore blue-chip stocks have kept pace with the Straits Times Index (STI) rally.

Earlier this year, I was watching both Keppel and Sembcorp Industries as they stood out among the stronger performers in the Singapore market.

Sembcorp was previously one of the top-performing Singapore blue-chip stocks, while Keppel also drew attention after raising its dividend and ranking among the best-performing blue chips earlier in the year.

More recently, the M1-Simba fallout raised questions over whether M1 could continue contributing meaningfully to Keppel’s dividends.

Since then, shares of both Keppel and Sembcorp have lagged the Straits Times Index.

Year-to-date as at 7 July 2026, Keppel gained 5.8% while Sembcorp declined 5.3%. In comparison, the STI rose 14.7%.

This has led to discussions within the Beansprout community on which stock offers the more attractive opportunity following the recent pullback.

In this article, I compare Keppel and Sembcorp across revenue and earnings growth, balance sheet strength, return on equity and AI infrastructure exposure to see which stock looks more attractive after the pullback.

Keppel vs Sembcorp: Which has stronger earnings momentum?

The first metric I look at based on Beansprout's checklist for evaluating growth stocks is whether the company is still delivering growth in both revenue and earnings.

On this front, Keppel appears to have stronger growth momentum.

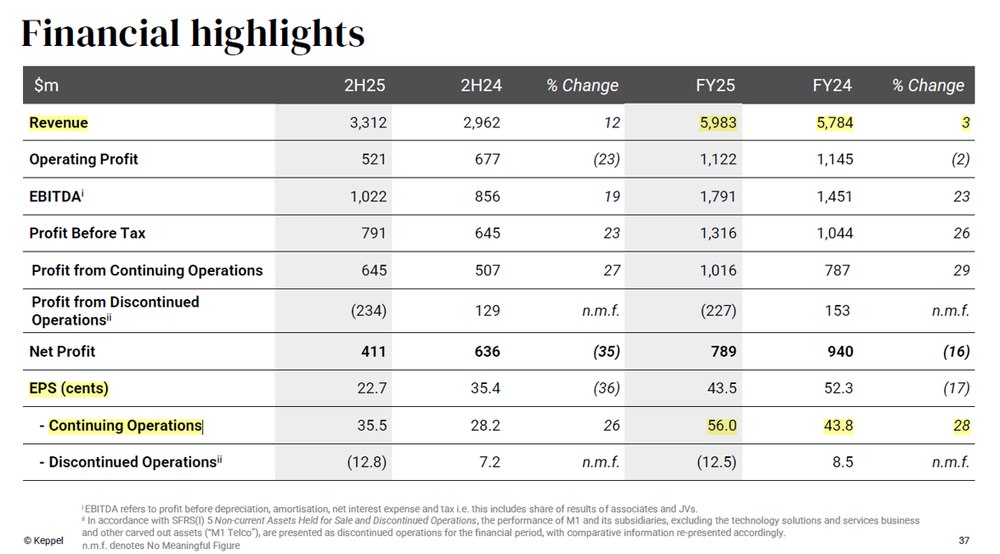

Keppel’s FY2025 revenue increased 3% year-on-year to S$5.98 billion, while earnings per share (EPS) from continuing operations rose 28% year-on-year to S$0.56.

This suggests that Keppel’s earnings grew much faster than revenue, supported by better margins, operating leverage and cost discipline as its asset-light strategy gained traction.

A key contributor was Keppel’s Connectivity segment, where revenue rose 73.9% year-on-year to S$953 million.

.The segment benefited from acquisition-led growth, higher recurring data centre management income, and stronger contributions from asset management fees and performance fees from its data centre funds.

Keppel’s data centre platform also provides a longer runway for growth.

Management has estimated that its fully developed pipeline can support around S$10 billion in data centre funds under management over time.

As demand for AI-related digital infrastructure grows, this may become a more meaningful source of recurring fee income for Keppel.

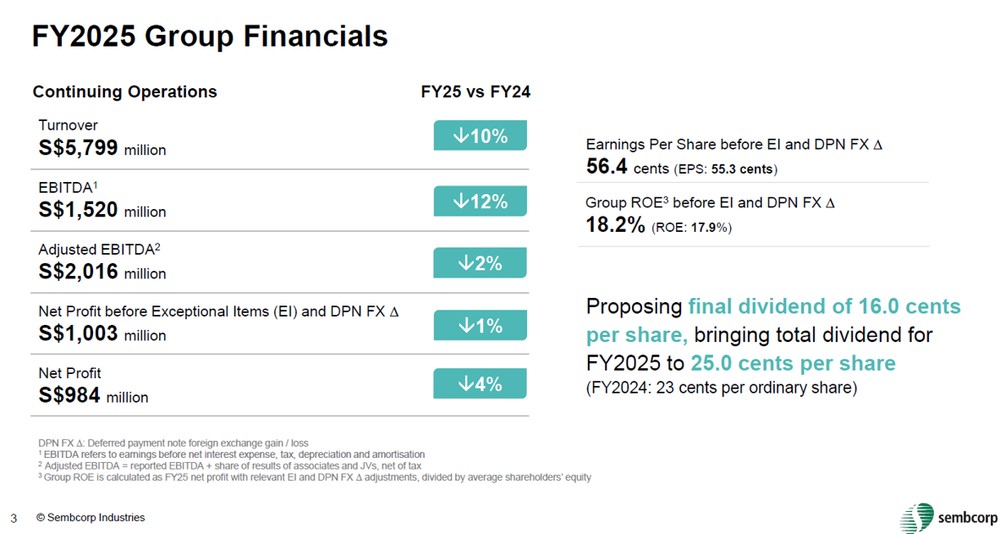

In comparison, Sembcorp reported FY2025 revenue of S$5.8 billion, down 10% year-on-year.

The decline reflected lower electricity and gas prices in Singapore, weaker customer demand in the UK, and a lower contribution from its gas business.

Despite the decline in revenue, Sembcorp demonstrated resilient profitability.

Net profit before exceptional items and foreign exchange movements declined by just 1% year-on-year to S$1.0 billion, while EPS before exceptional items and FX effects slipped marginally by 1% to S$0.564 cents.

The resilience in earnings was supported by growth in its renewables business. Renewable operational capacity increased from 13.1GW to 15.0GW during FY2025, while the company added another 5.4GW of projects under construction to support future growth.

Sembcorp also continues to benefit from structural tailwinds from electrification, decarbonisation and artificial intelligence (AI) infrastructure demand.

While both companies continue to benefit from long-term structural trends, Keppel currently demonstrates stronger earnings momentum, while Sembcorp’s results highlight resilient earnings despite pressure from its gas business.

| Revenue and earnings growth | Keppel | Sembcorp |

| Revenue growth | 3% | -10% |

| EPS growth | 28% | -1% |

| Opportunity Pot screening assessment | Pass | Mixed |

Keppel vs Sembcorp: Which has the stronger balance sheet?

The second Opportunity Pot screen evaluates financial resilience through leverage levels.

For this metric, we prefer companies with net debt-to-equity below 1.0 times. This gives the company more flexibility to fund growth, manage interest costs and navigate periods of market uncertainty.

Keppel reported net debt of S$9.1 billion and total equity of S$11.2 billion as at FY2025, translating into a net debt-to-equity ratio of 0.82x, which is below our preferred threshold.

Keppel’s balance sheet has remained healthy even as the company expands its data centre, infrastructure and connectivity platforms.

Its asset-light model also helps. By recycling capital and bringing in third-party investors for large-scale projects, Keppel can pursue growth opportunities without relying solely on its own balance sheet.

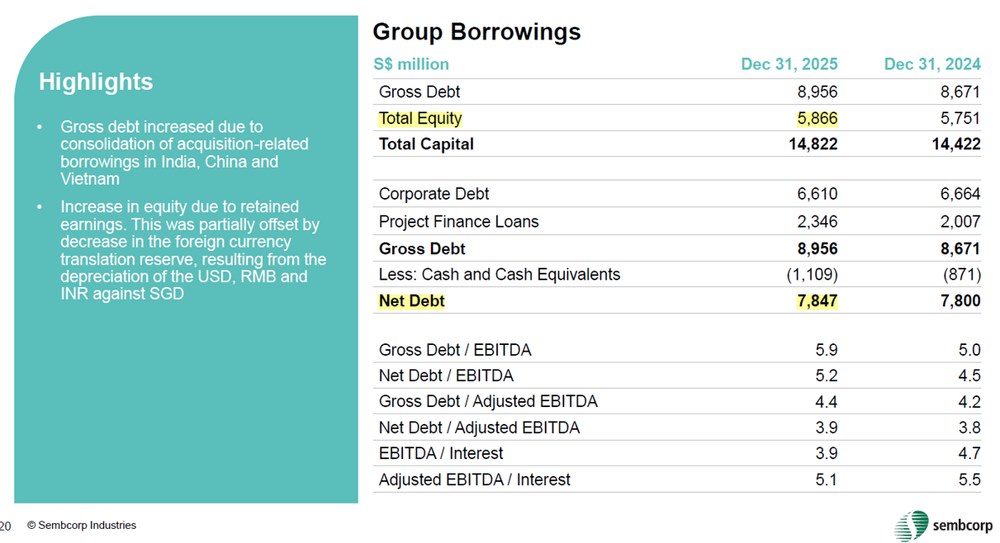

On the other hand, Sembcorp reported net debt of S$7.85 billion against shareholders' equity of S$5.87 billion.

This translates to a net debt-to-equity ratio of about 1.34 times, which is above our preferred threshold.

That said, Sembcorp’s higher leverage needs to be viewed in the context of its business model.

Utilities and renewables are more capital-intensive businesses, and Sembcorp has been investing in growth projects, renewable energy capacity and strategic assets such as Senoko Energy.

The company also has a manageable debt profile, with S$8.2 billion of unutilised borrowing facilities, 76% of borrowings on fixed rates, and an average debt maturity of 5.2 years.

While Sembcorp’s balance sheet does not appear stretched in the near term, it does not meet our balance sheet hurdle under the Opportunity Pot framework.

| Balance sheet strength | Keppel | Sembcorp |

| Net debt-to-equity | 0.82x | 1.34x |

| Opportunity Pot screening assessment | Pass | Fail |

Keppel vs Sembcorp: Which generates better returns for shareholders?

A strong business should not only grow, but also generate healthy returns on the capital invested by shareholders.

For the the third check for the Opportunity Pot, I use return on equity, or ROE, as a key measure. Both companies comfortably exceed our ROE hurdle.

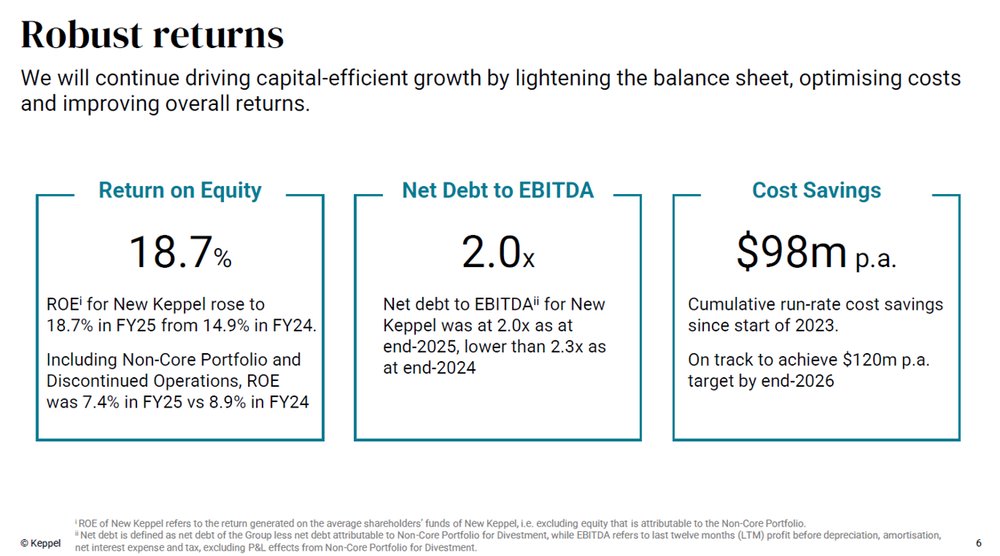

Keppel delivered an ROE of 18.7% in FY2025, improving from 14.9% in FY2024 as its asset-light strategy continued to gain traction.

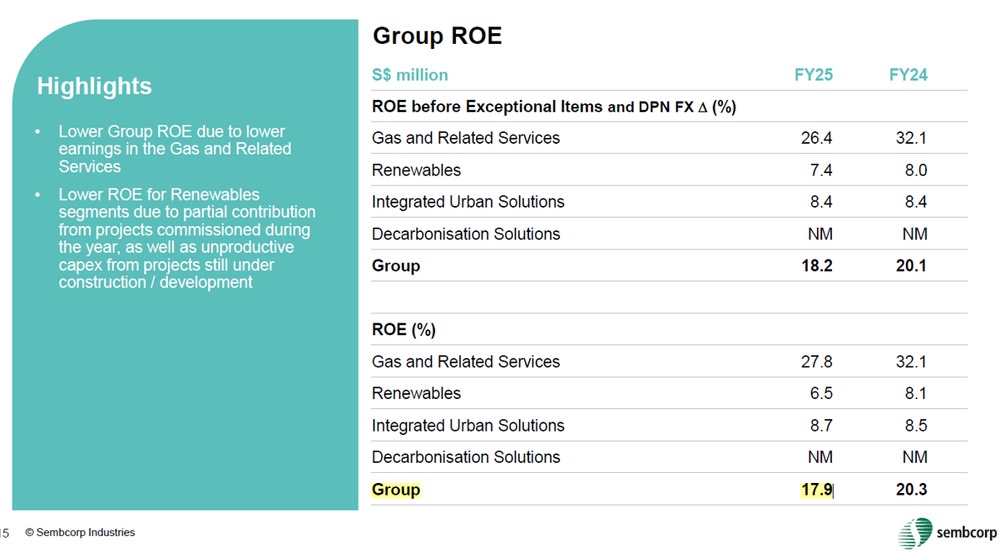

Sembcorp generated an ROE of 17.9%, slightly below the 20.3% achieved in FY2024 due to softer gas margins and earnings dilution from projects under development.

However, Sembcorp’s reported ROE may understate its longer-term earnings potential.

Management noted that after annualising the contribution from projects commissioned during FY2025 and excluding capital tied up in projects under development, normalised group ROE would have been around 20%.

As more renewable projects are completed and start contributing a full year of earnings, Sembcorp’s returns could improve over time.

| Return on equity | Keppel | Sembcorp |

| FY2025 ROE | 18.7% | 17.9% |

| Opportunity Pot screening assessment | Pass | Pass |

Overall, Keppel passes all three Opportunity Pot screens, while Sembcorp passes two out of three.

You can learn more about how to find better growth stocks using Beansprout's checklist here.

Keppel vs Sembcorp: Which has better AI infrastructure exposure?

Passing the quantitative screens is only the first step.

After screening them through the quantitative metrics, we then dive deeper into Keppel and Sembcorp to assess the quality of the business model, competitive advantages and long-term growth opportunities.

Both Keppel and Sembcorp stand to benefit from the growth in AI infrastructure. However, their exposure to this theme is different.

AI infrastructure is not just about electricity demand. It also requires data centres, power solutions, cooling systems, connectivity assets, financing structures and operating expertise.

This is where Keppel’s broader platform gives it a more diversified way to participate in the AI infrastructure value chain.

Keppel: Broader exposure across the AI infrastructure value chain

#1 - Power and energy infrastructure

Keppel’s Infrastructure division gives it exposure to the power generation, cooling systems and energy infrastructure needed to support AI deployment.

As digital infrastructure becomes more power-intensive, demand for reliable and cleaner energy solutions is likely to grow.

To stay relevant, Keppel has been expanding generation capacity, cross-border renewable energy imports and lower carbon energy.

Keppel’s hydrogen-compatible Keppel Sakra Cogen Plant is a 600 MW state-of-the-art advanced combined cycle gas turbine power plant. It is the first in Singapore and will deliver top-tier energy efficiency and performance.

Keppel has positioned itself early across the digital infrastructure value chain, through cleaner energy, data centre and subsea connectivity.

#2 - Data centres and connectivity

Keppel is also directly involved in developing, owning and operating data centres across key markets globally.

During FY2025, Keppel expanded its data centre powerbank across Asia Pacific to more than 1.0GW, including securing a prime site near Melbourne earmarked for a future 720MW AI data centre campus.

Beyond providing physical space for AI computing, the company also develops supporting infrastructure such as power and cooling systems that are critical for high-density AI workloads.

As demand for AI computing accelerates, Keppel stands to benefit from rising demand for data centre capacity from hyperscalers and enterprise customers.

#3 - Capital recycling and asset management

One of Keppel's biggest competitive advantages is its ability to mobilise third-party capital to fund growth opportunities.

Rather than relying solely on its own balance sheet, Keppel can develop assets, recycle capital and bring in institutional investors through its funds platform. This allows the company to continue expanding while earning recurring asset management and performance fees.

This capability is particularly important in AI infrastructure, where projects are increasingly large and capital intensive.

Sembcorp: Direct exposure to power demand and renewables

#1 - Spark spreads and Singapore power demand

Sembcorp’s AI exposure is more directly linked to electricity demand.

For its Singapore gas-fired power business, profitability is heavily influenced by spark spreads, which measure the difference between electricity selling prices and fuel costs.

While demand from data centres may increase electricity consumption over time, earnings remain sensitive to movements in electricity prices, fuel costs and the pricing of contracts that are renewed.

For example, management has guided that FY2026 earnings from its gas business will be affected by lower margins on newly contracted volumes in Singapore as existing contracts are renewed at lower spreads.

This highlights the cyclical nature of earnings in the power generation business.

#2 - Renewable energy

Sembcorp has built one of Asia's largest renewable energy platforms, with 15.0GW of installed renewable capacity and a further 5.4GW under construction as at the end of FY2025.

This gives Sembcorp exposure to long-term trends such as electrification, decarbonisation and demand for cleaner power.

However, future earnings growth will therefore depend heavily on the successful execution and commissioning of these projects.

The company is also exposed to factors such as curtailment risk, regulatory changes and tariff pressures, particularly in markets such as China where profitability has recently come under pressure.

#3 - Power purchase agreements

A significant portion of Sembcorp's earnings visibility comes from long-term power purchase agreements and contracted electricity sales.

These agreements provide stability and recurring cash flows, supporting investments in new projects and helping to reduce earnings volatility.

Examples include long-term renewable energy agreements with customers such as data centre operators and industrial users, as well as long-duration contracts supporting its gas and renewable assets.

While these contracts improve earnings visibility, growth remains dependent on Sembcorp’s ability to secure new contracts and deploy capital into additional projects at attractive returns.

Sembcorp supplies power to industrial customers and data centres and has secured additional power supply agreements with major semiconductor manufacturers such as Micron, which indirectly benefits from AI demand.

In the long term, Sembcorp benefits from supplying significant amounts of electricity to power data centres, semiconductor manufacturing and industrial facilities. Management has also highlighted AI-driven data centre demand as an important future growth driver for Singapore's power market.

Overall, Sembcorp remains more exposed to commodity cycles and project execution risks compared to Keppel's asset-light, fee-based growth model.

| Underlying business drivers | Keppel | Sembcorp |

| Main AI exposure | Data centres, power, cooling, connectivity and capital recycling | Power demand from data centres, semiconductor manufacturing and industrial users |

| Key growth drivers | Data centre platform, infrastructure assets and asset management fees | Spark spreads, renewable energy and power purchase agreements |

| Business model | More asset-light and fee-based | More capital-intensive |

| Key risks | Execution and valuation | Commodity cycles, tariff pressure and project execution |

Keppel vs Sembcorp valuation: Have share prices priced in the growth?

Although both stocks have lagged the STI recently, valuations are still above their historical averages.

This suggests that the market may already be pricing in a fairly positive outlook for earnings growth, dividends and exposure to long-term themes such as AI infrastructure, data centres and energy demand.

Keppel is currently trading at a price-to-earnings ratio of 19.2x, above its historical average of 9.4x. Its price-to-book ratio of 1.86x is also above its historical average of 0.86x.

Sembcorp is currently trading at a price-to-earnings ratio of 11.5x, above its historical average of 9.8x. Its price-to-book ratio of 2.03x is also above its historical average of 1.14x.

Based on valuation alone, Sembcorp appears cheaper on a price-to-earnings basis.

However, Keppel’s higher valuation may partly reflect its more asset-light business model, capital recycling capabilities and broader exposure across the AI infrastructure value chain.

What would Beansprout do?

Both Keppel and Sembcorp are high-quality Singapore companies with attractive long-term growth prospects.

Keppel offers exposure to AI infrastructure, data centres, connectivity and asset management, while Sembcorp is more directly linked to power demand, renewable energy and Singapore’s energy security needs.

However, after screening both companies, I would lean towards Keppel if I were looking to add a stock to the Opportunity Pot within Beansprout’s four pots of wealth today.

This is based on Beansprout's checklist for evaluating growth stocks which looks at revenue and earning momentum, balance sheet strength, and return on equity.

Keppel has shown stronger earnings momentum, with revenue and EPS growth in FY2025.

It also has a stronger balance sheet, with net debt-to-equity below our preferred threshold.

Sembcorp still generates attractive returns on equity and remains well positioned for long-term demand from electrification, renewables and data centre power needs.

However, its higher leverage and more capital-intensive business model mean that it does not screen as cleanly under our Opportunity Pot screening framework.

The key difference for me is the business model.

Keppel has a broader and more capital-efficient way to participate in the AI infrastructure theme through data centres, power solutions, connectivity assets and capital recycling.

Sembcorp’s exposure is also attractive, but it remains more tied to spark spreads, renewable project execution and capital deployment.

This does not mean I would ignore Sembcorp. I would continue to watch whether its renewables pipeline can translate into stronger earnings growth, and whether power market conditions remain supportive.

As for Keppel, I would watch whether its valuation can be justified by continued earnings growth and successful execution of its data centre and infrastructure pipeline.

| Factor | Keppel | Sembcorp |

| Share price YTD | 5.80% | -5.30% |

| Revenue growth | 3% | -10% |

| EPS growth | 28% | -1% |

| Net debt-to-equity | 0.82x | 1.34x |

| ROE | 18.70% | 17.90% |

| AI infrastructure exposure | Broader value chain | Power demand and renewables |

| Key risk | Execution and valuation | Leverage, commodity cycles, project execution |

| Source: Company data, data as of 7 July 2026. | ||

Looking at the Singapore market as a whole, we still think Singapore stocks are worth looking at in 2026.

Keppel and Sembcorp reflect two structural themes we are watching in Singapore stocks: AI and data centre growth, as well as energy security.

Keppel offers broader exposure across the AI infrastructure value chain, while Sembcorp is more directly linked to power demand and renewable energy.

But these are not the only themes we are watching. Beyond these themes, we are also watching other long-term opportunities in the Singapore market, including food security, Singapore’s rise as a wealth management hub, and continued infrastructure spending. Find out more about the 4 growth themes we are watching in Singapore stocks here.

For investors looking for more higher-conviction ideas, you can explore our curated stock opportunities here.

Are you invested in Keppel or Sembcorp? Share your thoughts with us in the comments below or in the Beansprout Telegram community.

Follow Beansprout on YouTube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Important Disclosures

Analyst Certification and Disclosures

The analyst(s) named in this report certifies that (i) all views expressed in this report accurately reflect the personal views of the analyst(s) with regard to any and all of the subject securities and companies mentioned in this report and (ii) no part of the compensation of the analyst(s) was, is, or will be, directly or indirectly, related to the specific views expressed by that analyst herein. The analyst(s) named in this report (or their associates) does not have a financial interest in the corporation(s) mentioned in this report.

An associate is defined as (i) the spouse, or any minor child (natural or adopted) or minor step-child, of the analyst; (ii) the trustee of a trust of which the analyst, his spouse, minor child (natural or adopted) or minor step-child, is a beneficiary or discretionary object; or (iii) another person accustomed or obliged to act in accordance with the directions or instructions of the analyst.

Company Disclosure

Global Wealth Technology Pte Ltd (“Beansprout”) does not have any financial interest in the corporation(s) mentioned in this report.

Disclaimer

This report is provided by Beansprout for the use of intended recipients only and may not be reproduced, in whole or in part, or delivered or transmitted to any other person without our prior written consent. By accepting this report, the recipient agrees to be bound by the terms and limitations set out herein.

You acknowledge that this document is provided for general information purposes only. Nothing in this document shall be construed as a recommendation to purchase, sell, or hold any security or other investment, or to pursue any investment style or strategy. Nothing in this document shall be construed as advice that purports to be tailored to your needs or the needs of any person or company receiving the advice. The information in this document is intended for general circulation only and does not constitute investment advice. Nothing in this document is published with regard to the specific investment objectives, financial situation and particular needs of any person who may receive the information.

Nothing in this document shall be construed as, or form part of, any offer for sale or subscription of or solicitation or invitation of any offer to buy or subscribe for any securities. The data and information made available in this document are of a general nature and do not purport, and shall not in any way be deemed, to constitute an offer or provision of any professional or expert advice, including without limitation any financial, investment, legal, accounting or tax advice, and shall not be relied upon by you in that regard. You should at all times consult a qualified expert or professional adviser to obtain advice and independent verification of the information and data contained herein before acting on it. Any financial or investment information in this document are intended to be for your general information only. You should not rely upon such information in making any particular investment or other decision which should only be made after consulting with a fully qualified financial adviser. Such information do not nor are they intended to constitute any form of financial or investment advice, opinion or recommendation about any investment product, or any inducement or invitation relating to any of the products listed or referred to. Any arrangement made between you and a third party named on or linked to from these pages is at your sole risk and responsibility.

You acknowledge that Beansprout is under no obligation to exercise editorial control over, and to review, edit or amend any data, information, materials or contents of any content in this document. You agree that all statements, offers, information, opinions, materials, content in this document should be used, accepted and relied upon only with care and discretion and at your own risk, and Beansprout shall not be responsible for any loss, damage or liability incurred by you arising from such use or reliance.

This document (including all information and materials contained in this document) is provided “as is”. Although the material in this document is based upon information that Beansprout considers reliable and endeavours to keep current, Beansprout does not assure that this material is accurate, current or complete and is not providing any warranties or representations regarding the material contained in this document. All opinions contained herein constitute the views of the analyst(s) named in this report, they are subject to change without notice and are not intended to provide the sole basis of any evaluation of the subject securities and companies mentioned in this report. Any reference to past performance should not be taken as an indication of future performance. To the fullest extent permissible pursuant to applicable law, Beansprout disclaims all warranties and/or representations of any kind with regard to this document, including but not limited to any implied warranties of merchantability, non-infringement of third-party rights, or fitness for a particular purpose.

Beansprout does not warrant, either expressly or impliedly, the accuracy or completeness of the information, text, graphics, links or other items contained in this document. Neither Beansprout nor any of its affiliates, directors, employees or other representatives will be liable for any damages, losses or liabilities of any kind arising out of or in connection with the use of this document. To the best of Beansprout’s knowledge, this document does not contain and is not based on any non-public, material information. The information in this document is not intended for distribution to, or use by, any person or entity in any jurisdiction where such distribution or use would be contrary to law or regulation, or which would subject Beansprout to any registration requirement within such jurisdiction or country. Beansprout is not licensed or regulated by any authority in any jurisdiction or country to provide the information in this document.

As a condition of your use of this document, you agree to indemnify, defend and hold harmless Beansprout and its affiliates, and their respective officers, directors, employees, members, managing members, managers, agents, representatives, successors and assigns from and against any and all actions, causes of action, claims, charges, cost, demands, expenses and damages (including attorneys’ fees and expenses), losses and liabilities or other expenses of any kind that arise directly or indirectly out of or from, arising out of or in connection with violation of these terms, use of this document, violation of the rights of any third party, acts, omissions or negligence of third parties, their directors, employees or agents. To the extent permitted by law, Beansprout shall not be liable to you, any other person, or organization, for any direct, indirect, special, punitive, exemplary, incidental or consequential damages, whether in contract, tort (including negligence), or otherwise, arising in any way from, or in connection with, the use of this document and/or its content. This includes, without limitation, liability for any act or omission in reliance on the information in this document. Beansprout expressly disclaims and excludes all warranties, conditions, representations and terms not expressly set out in this User Agreement, whether express, implied or statutory, with regard to this document and its content, including any implied warranties or representations about the accuracy or completeness of this document and the content, suitability and general availability, or whether it is free from error.

If these terms or any part of them is understood to be illegal, invalid or otherwise unenforceable under the laws of any state or country in which these terms are intended to be effective, then to the extent that they are illegal, invalid or unenforceable, they shall in that state or country be treated as severed and deleted from these terms and the remaining terms shall survive and remain fully intact and in effect and will continue to be binding and enforceable in that state or country.

These terms, as well as any claims arising from or related thereto, are governed by the laws of Singapore without reference to the principles of conflicts of laws thereof. You agree to submit to the personal and exclusive jurisdiction of the courts of Singapore with respect to all disputes arising out of or related to this Agreement. Beansprout and you each hereby irrevocably consent to the jurisdiction of such courts, and each Party hereby waives any claim or defence that such forum is not convenient or proper.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments