DBS, OCBC, UOB and SIA in focus: Weekly Review with SIAS

Stocks

Powered by

By Gerald Wong, CFA • 18 May 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

We look at DBS, OCBC, UOB and SIA in the latest Weekly Market Review.

What happened?

In this week’s Weekly Market Review in partnership with the Securities Investors Association Singapore (SIAS), we discuss renewed inflation concerns amid elevated oil prices, rising bond yields, and the latest earnings updates from DBS, OCBC, UOB and Singapore Airlines (SIA). We also look at the technical outlook for the STI and major US indices following renewed volatility after the Beijing summit.

Watch the video to learn more about what we are looking out for this week.

Weekly Market Review

1:23 - Macro Update

- US markets continued to trade near record highs last week, with the S&P 500 briefly climbing above the 7,500 level before pulling back towards the end of the week following disappointment from the Beijing summit discussions.

- The STI outperformed with a 1.4% weekly gain to 4,989 points, supported mainly by strength in the Singapore banks, particularly OCBC and DBS following their latest earnings updates.

- Oil prices remained elevated above US$100 per barrel as the Iran conflict remained unresolved and the Strait of Hormuz stayed closed, renewing concerns around inflation and global economic growth.

- US inflation for April came in at 3.8% year on year, above market expectations and among the highest readings seen in recent years, reinforcing expectations that interest rates may remain higher for longer.

- US government bond yields continued to rise, with the 10-year Treasury yield climbing above 4.5% and the 30-year Treasury yield crossing the 5% level.

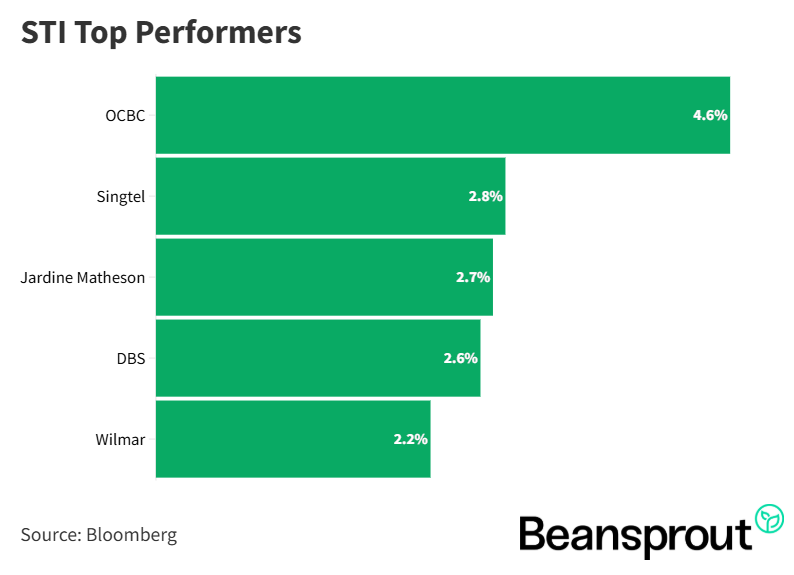

- Among the stronger-performing Singapore stocks last week, OCBC rose 4.6% while DBS gained 2.6% following their quarterly earnings announcements.

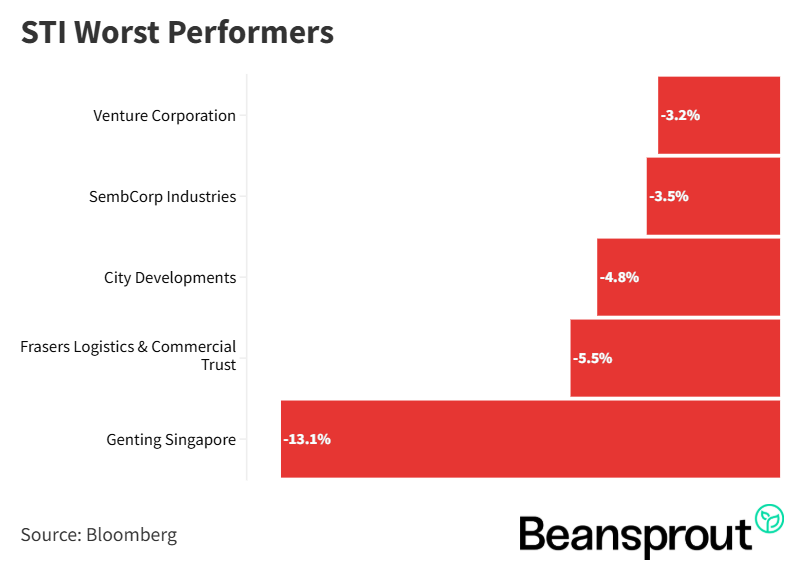

- On the weaker side, Genting Singapore fell 13.1% after reporting its latest earnings results, along with laggards Frasers Logistics & Commercial Trust, City Developments, Sembcorp Industries, and Venture.

STI Top Performers:

STI Worst Performers:

Companies in Focus:

OCBC (SGX: O39)

- OCBC has been the strongest-performing Singapore bank stock year-to-date, gaining 16% as of 15 May and outperforming the STI’s 7% gain.

- The bank reported first-quarter 2026 net profit growth of 5% year on year, outperforming DBS and UOB in terms of earnings growth. OCBC also led the Singapore banks in loan growth during the quarter.

- Like the other banks, OCBC experienced a decline in net interest margin due to lower interest rates, with NIM falling to 1.76% from 2.04% a year earlier. However, stronger fee-related income helped offset the decline in net interest income.

- OCBC also recorded the strongest fee income growth among the three Singapore banks, supported by resilient wealth management activity and stable credit quality.

- At current levels, OCBC is expected to offer a forward dividend yield of around 4.4%, while investors continue to focus on its stronger earnings momentum relative to peers.

Related Links:

- OCBC (SGX:039) latest valuation, share price and analysis

- OCBC (SGX:039) dividend history and dividend forecast

- OCBC reports 5% rise in net profit: Our Quick Take

DBS (SGX: D05)

- DBS continued to trade near record highs after reporting resilient first-quarter 2026 earnings, with the stock gaining 7% year-to-date and performing broadly in line with the STI.

- The bank reported a 1.1% year-on-year increase in first-quarter net profit, supported by continued growth in fee-related income despite lower net interest margins.

- Net interest margin declined to 1.89% from 2.12% a year earlier as interest rates eased. However, DBS achieved record fee income during the quarter, supported by continued strength in wealth management and treasury customer sales.

- DBS’ assets under management also reached a record high of S$492 billion in the first quarter of 2026, reflecting continued inflows into its wealth management platform.

- Credit quality remained stable, with no significant deterioration in credit costs despite the uncertain global macro environment. At current levels, DBS is expected to offer the highest forward dividend yield among the Singapore banks at around 5.7%.

Related Links:

- DBS (SGX:D05) latest valuation, share price and analysis

- DBS (SGX:D05) dividend history and dividend forecast

- DBS profit rises 1% and declares S$0.81 in total dividends in 1Q26: Our Quick Take

- DBS and OCBC near all-time highs as UOB lags. Are bank dividends still attractive?

UOB (SGX: U11)

- UOB reported weaker first-quarter earnings performance compared to OCBC and DBS, with net profit declining year on year.

- Net interest margin declined to 1.82% from 2.0% a year earlier as interest rates eased, while fee income growth also lagged behind OCBC and DBS.

- Despite the softer earnings performance, UOB’s asset quality remained stable, with no significant deterioration in credit costs across the Singapore banks.

- At current levels, UOB is expected to offer a forward dividend yield of about 4.6%, below DBS but slightly above OCBC.

Related Links:

- UOB (SGX: U11) latest valuation, share price and analysis

- UOB (SGX: U11) dividend history and dividend forecast

- UOB reports 4% decline in 1Q26 profit: Our Quick Take

Singapore Airlines (SGX: C6L)

- Singapore Airlines reported resilient full-year FY2025/26 operating performance, with revenue rising 5% year on year driven mainly by stronger passenger traffic and higher flight capacity.

- Passenger-related revenue remained strong across both Singapore Airlines and Scoot, while cargo revenue declined 2% year on year.

- Operating profit improved during the year as higher passenger volumes helped offset rising non-fuel expenditure. At the same time, fuel costs declined year on year over most of the financial year.

- However, net profit declined compared to the previous year due mainly to the absence of the one-off Vistara disposal gain and losses from associated companies, particularly Air India.

- Singapore Airlines proposed a final ordinary dividend of 22 cents alongside a final special dividend of 7 cents, bringing total special dividends for the fiscal year to 10 cents per share.

Related Links:

- Singapore Airlines (SGX: C6L) latest valuation, share price and analysis

- Singapore Airlines (SGX: C6L) dividend history and dividend forecast

- How SIA’s 5.8% dividend yield may be affected by Air India’s capital raising

Technical Analysis

Straits Times Index

- The STI remains near the psychologically important 5,000 level after briefly touching 5,015 points last week before pulling back following disappointment from the Beijing summit outcome.

- Immediate support is around 4,900 to 4,920, while stronger support is seen near 4,790 to 4,800. Resistance remains at the all-time high around 5,041 points.

- The RSI has moderated to around 52 after reaching near 60 previously, suggesting that momentum has eased but remains slightly positive.

- The MACD remains positive in the medium term, although near-term signals suggest consolidation may continue. For now, the STI is likely to remain range-bound around the 4,900 level as investors monitor geopolitical risks and elevated oil prices.

Learn more about the Straits Times Index (STI) here.

Dow Jones Industrial Average

- The Dow Jones pulled back by more than 1% last Friday following the Beijing summit, with investors disappointed by the lack of concrete outcomes from the discussions.

- Immediate support is around 48,800, followed by stronger support near 48,400. Resistance remains at the year-to-date high around 50,512 points.

- The RSI has weakened to around 55 from recent highs above 60, indicating that upward momentum has moderated.

- The MACD has turned negative following a bearish crossover, suggesting the Dow may see further technical pullback towards the 49,000 level in the near term.

S&P 500

- The S&P 500 briefly climbed to a fresh all-time high above 7,500 before retreating after optimism surrounding the Beijing summit faded.

- Immediate support is around 7,200, while stronger support may emerge closer to the 7,000 level if market weakness continues.

- The RSI reached as high as 77 last week before easing back to around 67, indicating that the market had entered overbought territory and may now be entering a period of consolidation.

- The MACD remains positive for now, although a potential bearish crossover could indicate growing downside momentum in the coming sessions.

Learn more about the S&P 500 index here.

Nasdaq Composite Index

- The Nasdaq Composite remained volatile after reaching a fresh high around 26,700 before pulling back sharply alongside broader US technology stocks.

- Immediate support is seen near the previous double-top region around 24,000, while resistance remains near the recent highs.

- The RSI moved into heavily overbought territory over the past week before starting to ease, suggesting that the rally may be stretched in the near term.

- The MACD remains positive, although a potential crossover could signal increasing downside momentum and raise the risk of a pullback towards the 24,000-support region.

Learn more about the Nasdaq Composite index here.

What to look out for this week

Key dates

- Monday, 18 May: Baidu earnings, NAHB Housing Market Index

- Tuesday, 19 May: NTT DC REIT, Yanlord ex-dividends

- Wednesday, 20 May: Singtel earnings, Geo Energy ex-dividend, NVIDIA earnings, Analog Devices earnings, FOMC meeting minutes

- Thursday, 21 May: US Housing Starts, Continuing Jobless Claims, Walmart earnings

- Friday, 22 May: US Consumer Sentiment Index

Check out the full list of Singapore stocks, REITs and ETFs with upcoming dividend payments with our dividend calendar.

Follow Beansprout on Telegram, Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments