3 Singapore blue chip stocks paying dividends in July. Where yields look attractive

Stocks

By Goh Lay Peng • 28 Jun 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

We look at 3 Singapore blue chip stocks paying out dividends in July 2026, and whether their payouts appear sustainable for income investors.

What happened?

The search for income has become less straightforward.

The Fed’s latest signal on higher-for-longer rates has kept pressure on income assets such as REITs. That said, we were still able to find pockets of opportunity in the REIT sector.

Beyond REITs, I also shared three Singapore blue chip dividend stocks with yields above 4%, and what to watch before buying them for income.

I also compared DBS, OCBC and UOB for income as they are near record highs, as the banks remain an important source of dividends in the Singapore market.

At the same time, with the STI reaching an all-time high, I looked at 3 SGX ETFs to diversify dividend income beyond Singapore.

In this environment, the next question is not just which stocks are paying dividends in July 2026, but whether those payouts are backed by resilient businesses and sustainable earnings.

In this article, I look at 3 Singapore blue chip stocks paying out dividends in July 2026, and whether their payouts look sustainable from here.

| Stock | Ex-date | Payment date | Dividend yield |

| SIA Engineering (SGX: S59) | 29-Jul-26 | 14-Aug-26 | 3.10% |

| SATS (SGX: S58) | 22-Jul-26 | 6-Aug-26 | 1.60% |

| Singtel (SGX: Z74) | 31-Jul-26 | 19-Aug-26 | 4.20% |

#1 - Singtel (SGX: Z74)

Singtel is Singapore's largest telecommunications company, with operations spanning Singapore, Australia (Optus), and significant associate stakes in India (Airtel), Thailand (AIS), and Indonesia (Telkomsel).

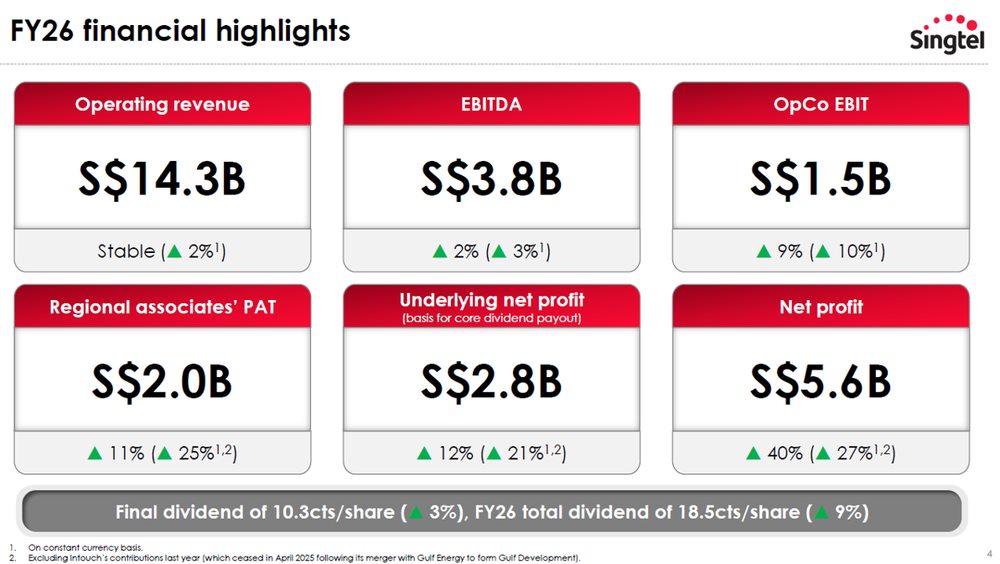

For FY2026 ended March, operating revenue was stable at S$14.3 billion, up 2% year-on-year. EBITDA rose 2% year-on-year to S$3.8 billion.

OpCo EBIT grew 9% year-on-year to S$1.5 billion.

Underlying net profit rose steadily at 12% year-on-year to S$2.8 billion.

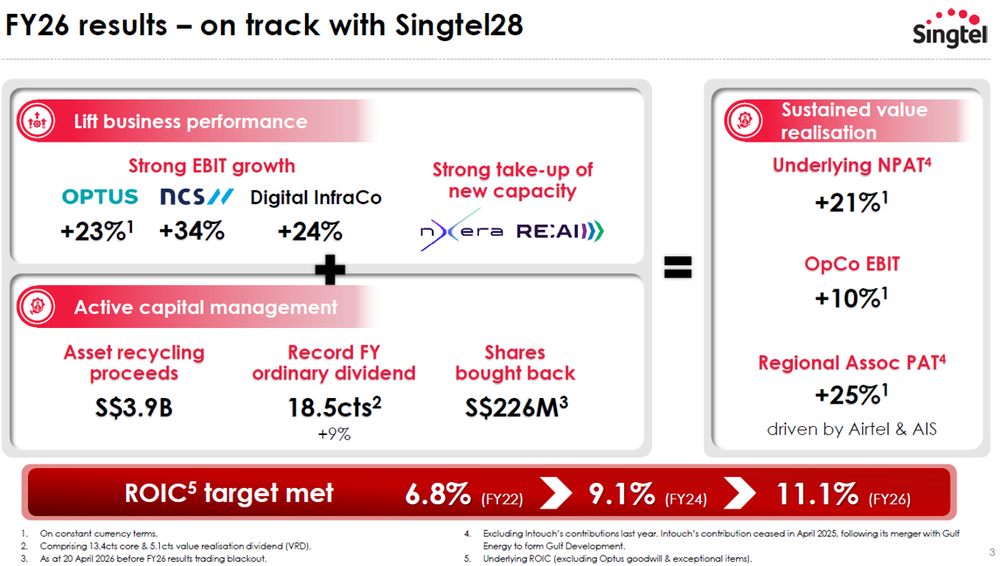

Growth engines performed strongly. NCS achieved record bookings of S$3.8 billion with EBIT up 34% year-on-year.

Digital InfraCo grew EBIT 24% year-on-year, driven by Nxera's improved data centre utilisation.

RE:AI, Singtel's GPU-as-a-service business, began commercialisation with S$600 million in long-term contracts already secured.

Regional associates also contributed strongly, with Airtel India's PAT up 32% year-on-year.

In terms of capital recycling, Singtel has raised around S$5.8 billion since April 2024. Based on the S$9 billion mid-term target, Singtel has another S$3.2 billion of recycling headroom remaining.

Management has guided for up to S$1 billion of Value Realisation Share Buybacks (VRSB) in FY27, and another S$0.7 billion in special dividends from AIS and Gulf Development has already been received. On 23 June 2026, Singtel announced the sale of 2.8% in Gulf Development for S$1.0 billion.

Singtel estimated the VRD framework has the potential to sustain payouts of 3 to 6 cents per year for at least four years.

As the industry evolves, the core business was negatively impacted. Singtel Singapore saw revenue decline 3% year-on-year and EBIT fall 5% year-on-year in FY26, reflecting structural price competition and spectrum amortisation costs.

Management guided for OpCo EBIT growth in the low-to-mid single digits in FY27, a step down from 10% in FY26.

Capex will also rise from S$2.5 billion to S$3.0 billion in FY27

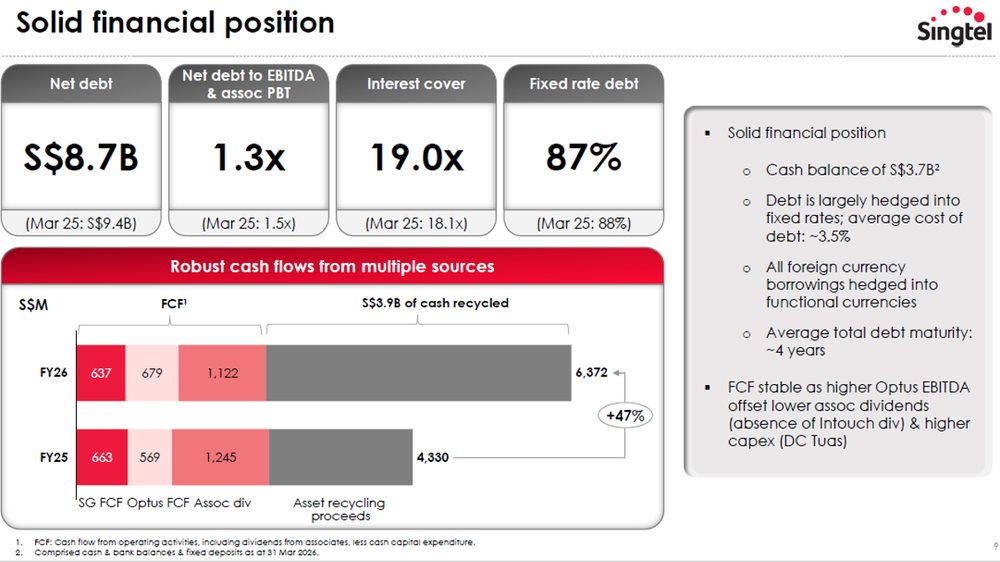

On the balance sheet, net debt fell from S$9.4 billion to S$8.7 billion, and interest cover stands at a comfortable 19 times.

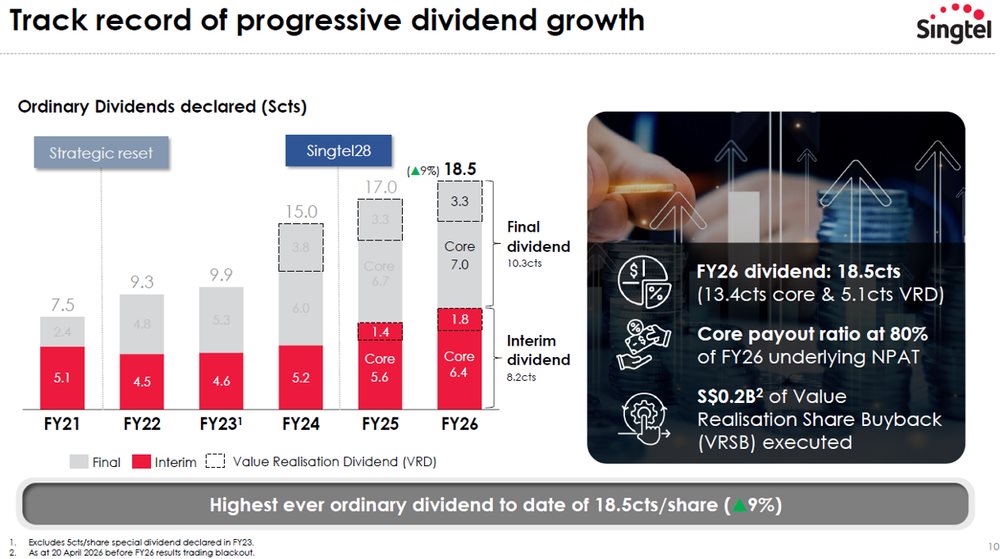

Singtel declared a final ordinary dividend of 10.3 cents per share. Together with the interim dividend of 8.2 cents, the total FY2026 payout is 18.5 cents per share is the highest ordinary dividend per share in Singtel's history.

The dividend has two components: a core dividend of 13.4 cents (representing an 80% payout ratio against underlying NPAT) and a Value Realisation Dividend (VRD) of 5.1 cents, funded by Singtel's asset recycling programme.

Based on the closing price of S$4.40 on 25 Jun 2026, Singtel is offering a dividend yield of 4.2%.

Source: Singtel FY26 Financial results

Find out how much dividends you would have received as a unitholder of Singtel in the past 12 months with the calculator below.

Related links:

#2 - SATS (SGX: S58)

SATS is one of Asia's leading aviation services and food solutions companies, spanning ground handling, cargo, inflight catering, and non-aviation food across more than 200 locations globally.

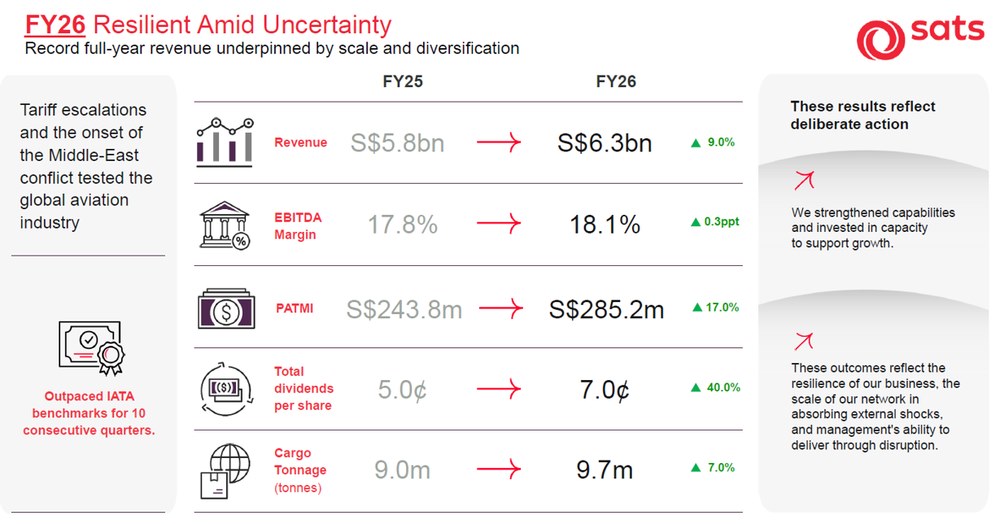

For the full year FY26 ended March 2026, revenue grew 9.0% year-on year to a record S$6.35 billion.

Net profit attributable to shareholders (PATMI) rose 17.0% year-on-year to S$285.2 million, a meaningful acceleration in profitability as the integration of Worldwide Flight Services continues to bear fruit.

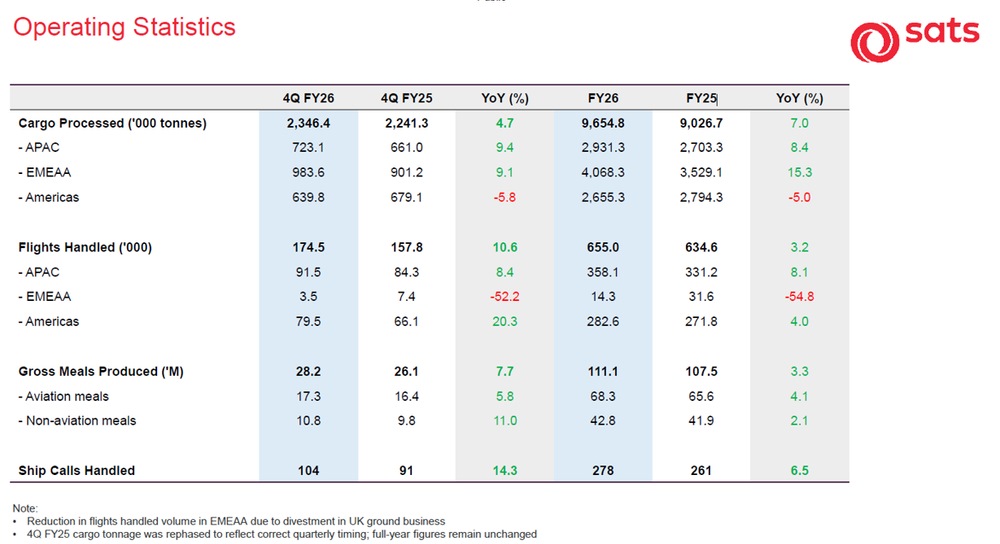

Volumes growth was resilient in FY26. Flights handled grew 3.2%, aviation meals rose 4.1%, and non-aviation meals grew 2.1%, when compared with the previous year.

SATS also completed the acquisition of Aviapartner Cargo NV at Brussels Airport during the quarter, adding a 33,000 square metre cargo terminal to its European network.

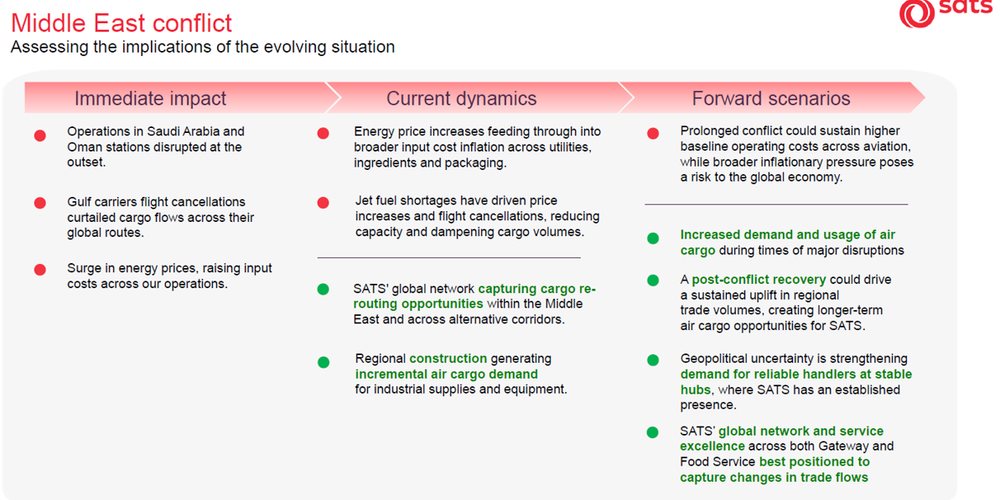

The Middle East conflict weighed on EBITDA through higher energy costs and Gulf carrier flight cancellations. SATS's diversified network allowed it to capture rerouting opportunities across alternative corridors.

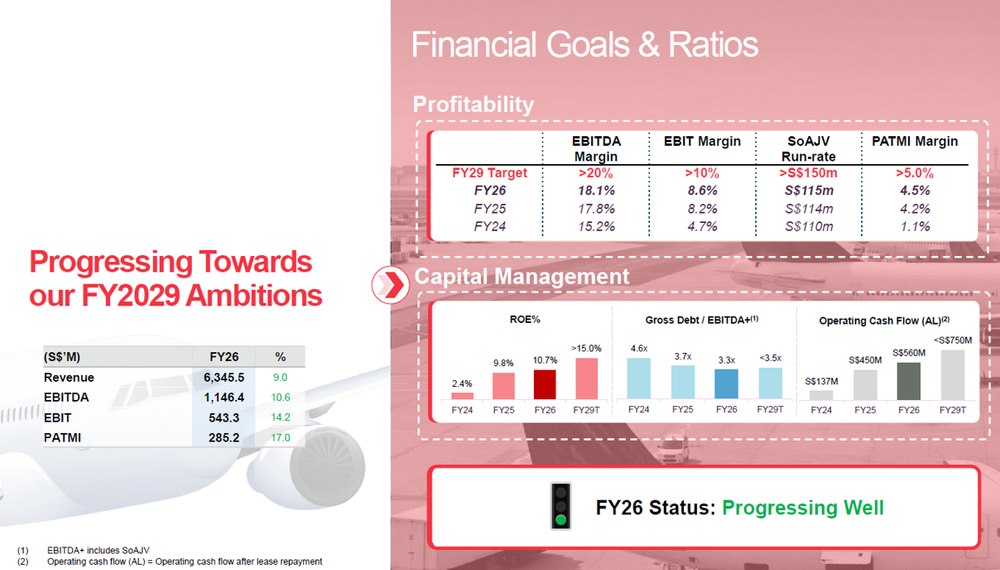

That said, SATS is on track against its FY2029 targets: EBITDA margin expanded to 18.1% (target: >20%), ROE improved to 10.7%, and gross debt fell 6.4% year-on-year.

SATS proposed a final dividend of 5.0 cents per share for FY2026, up 43% from 3.5 cents in the prior year. Together with the interim dividend of 2.0 cents, the total FY2026 dividend per share is 7.0 cents a share, up 40% year-on-year.

Based on the closing price of S$4.50 as of 25 Jun 2026, SATS provides a dividend yield of 1.56%. The yield is modest, but the payout ratio of around 29% of earnings is conservative and well-covered, with significant room to grow as profitability improves.

Find out how much dividends you would have received as a unitholder of SATS in the past 12 months with the calculator below.

Related links:

#3 - SIA Engineering (SGX: S59)

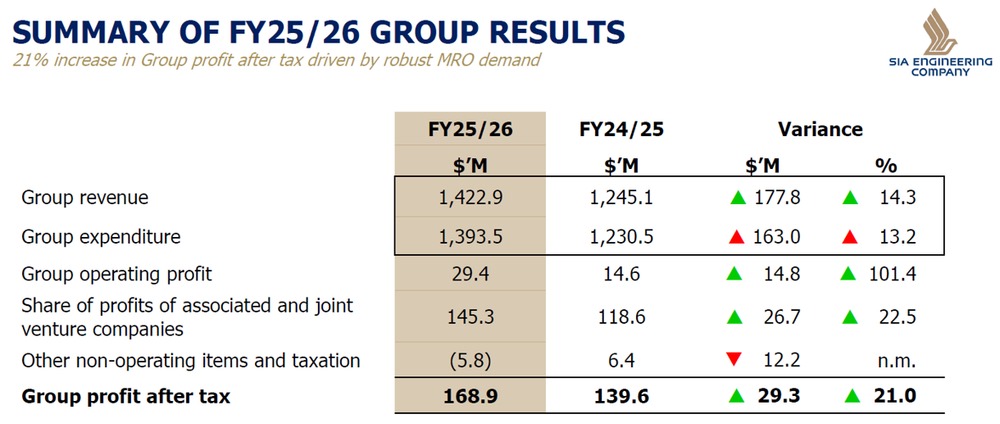

SIA Engineering Company (SIAEC) is Singapore's leading aircraft maintenance, repair, and overhaul (MRO) provider. The Group operates across 39 airports in 9 countries, with total revenue of S$11.2 billion in FY2026 ended March.

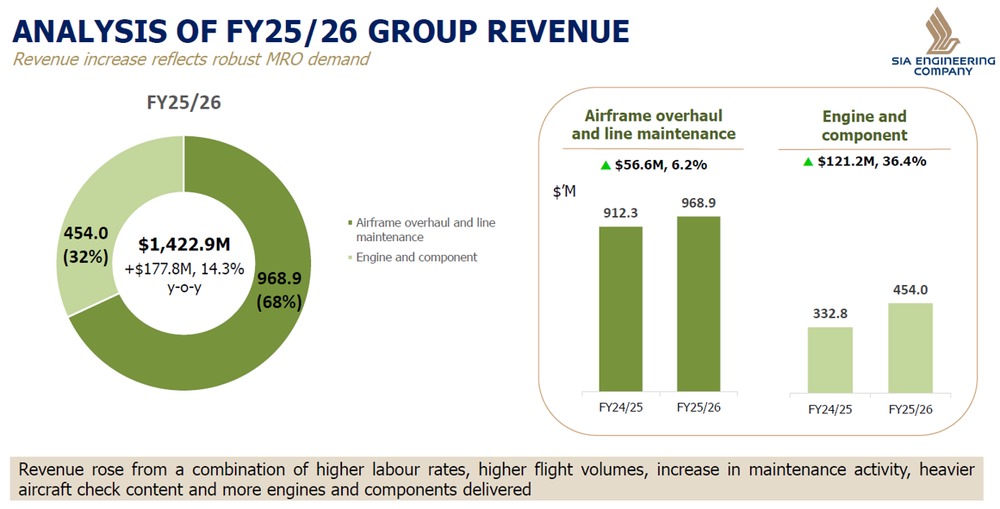

For FY2026 ended March, SIAEC delivered a strong set of results. Revenue rose 14.3% year-on-year to S$1.42 billion, driven by robust MRO demand as air travel continued to recover.

Operating profit more than doubled to S$29.4 million, as core segments achieved higher pricing.

Share of profits from associates and joint ventures rose 22.5% year-on-year to S$145.3 million. This JV network is anchored by engine overhaul partnerships with Pratt & Whitney, Rolls-Royce, and GE. This partnership is the backbone of SIAEC's profitability and provides a recurring, relatively stable income stream.

Net profit climbed 21% year-on-year to S$168.9 million.

Core segments continue to chart a healthy path of organic growth. Flights handled at Changi Airport grew 3.3% year-on-year to 162,608.

Engine and component revenue was the standout, rising 36.4% to S$454 million on higher engine inductions and component work volumes.

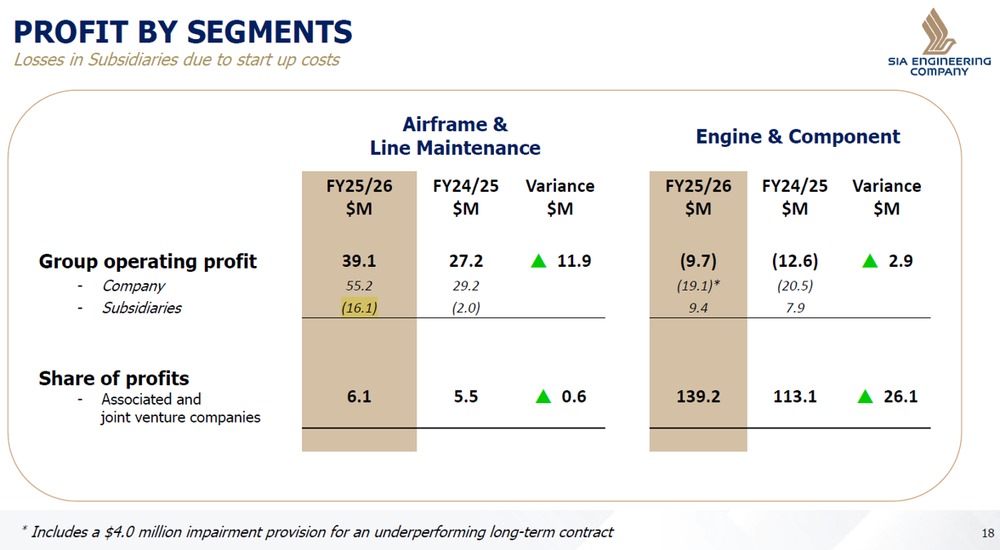

Subsidiaries in the Airframe & Line Maintenance segment reported operating losses of S$16.1 million.

This reflects start-up costs at new overseas operations, including the new Subang base in Malaysia and new line maintenance stations in Cambodia, Indonesia, Japan, and the Philippines.

These are one-off and represent investments in growth. We do not view this as a sign of structural weakness.

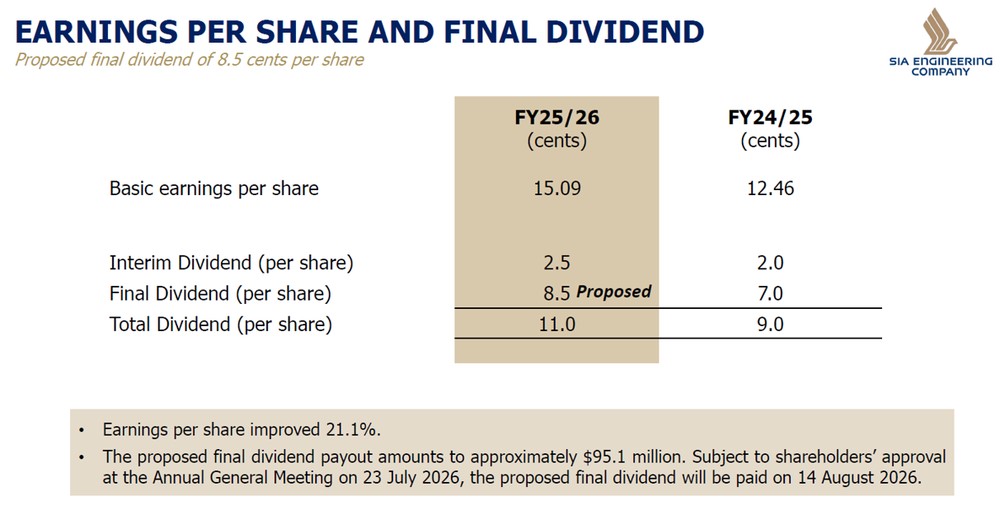

Basic earnings per share reached 15.09 cents, up 21.1% year-on-year.

SIAEC declared total FY2025/26 dividends of 11 cents per share, comprising interim dividend of 2.5 cents and final dividend of 8.5 cents.

Based on the closing price of S$3.53 as of 25 Jun 2026, SIAEC provides a dividend yield of 3.12%.

EPS is expected to grow approximately 30% over the next three years, which should provide further support to the dividend.

Return on equity improved to 9.7% from 8.2% a year earlier.

Cash and bank balances stood at S$564.8 million as at 31 March 2026.

The final dividend payout of approximately S$95.1 million is subject to shareholders' approval at the AGM on 23 July 2026.

The payout ratio is around 73%, well-covered by reported earnings.

EPS is expected to grow approximately 30% over the next three years, which should provide further support to the dividend.

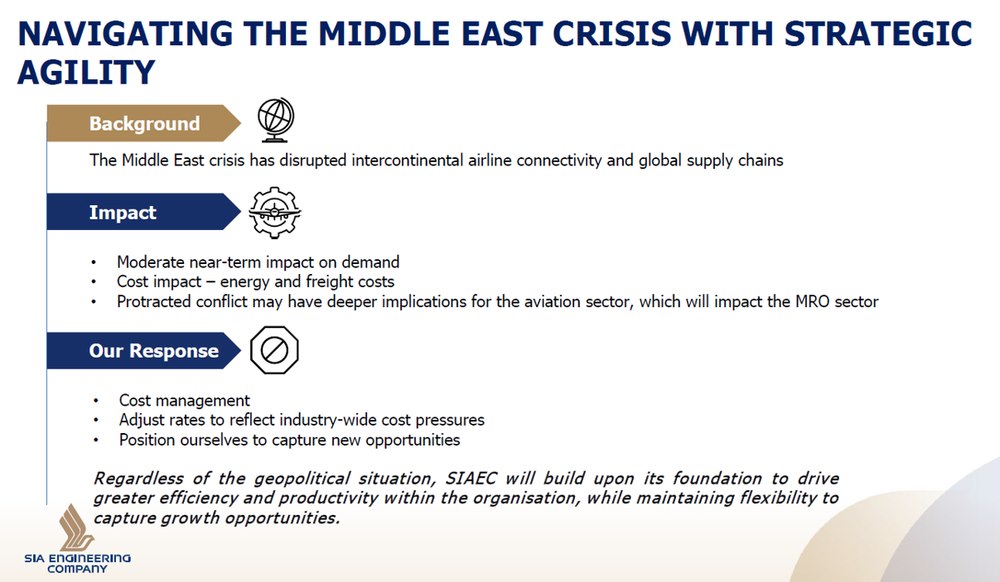

On the Middle East conflict, SIAEC acknowledged a moderate near-term impact on demand and cost pressures from higher energy and freight costs, while noting that a protracted conflict could have deeper implications for the aviation sector.

Its response has been cost management, rate adjustments, and positioning to capture new opportunities.

Find out how much dividends you would have received as a unitholder of SIA Engineering in the past 12 months with the calculator below.

Related links:

What should Beansprout do?

Singtel, SATS and SIA Engineering are paying dividends in July 2026.

As market conditions stay uncertain, I would not just look at which stock offers the highest dividend yield when evaluating these stocks for my income pot as part of Beansprout's four pots of wealth.

Following our income pot evaluation framework, I would look at what is supporting the payout, whether it is backed by recurring earnings, and whether the business has enough balance sheet strength to withstand tougher periods.

Singtel offers the highest yield among the three at 4.2%. Its core dividend is supported by underlying earnings, while the Value Realisation Dividend (VRD) depends on continued asset recycling. For now, the management has shown its capability to meet the target asset divestment plan, and the company has S$3.2 billion of remaining recycling headroom in the medium term. Learn more about Singtel latest valuation and dividend analysis here.

SATS has the lowest dividend yield at 1.6%, but arguably the strongest underlying business momentum. The payout ratio is conservative at 36%, with upside potential. Earnings are growing and the company is tracking well against its FY2029 Ambitions. For now, SATS looks more like a dividend growth story than a high-yield income stock. . Learn more about SATS latest valuation and dividend analysis here.

SIA Engineering offers the cleanest dividend recovery story among the three with a 3.1% dividend yield. Its dividend is supported by stronger MRO demand, higher associate and joint venture profits, and a payout ratio of around 73%. . The main caveat is near-term negative free cash flow as capacity investment ramps up. Learn more on SIA engineering latest valuation and dividend analysis here.

| Stock | Dividend yield | Key strength | Key risks |

| SIA Engineering | 3.1% |

|

|

| SATS | 1.6% |

|

|

| Singtel | 4.2% |

|

|

Overall, the dividend payouts of these Singapore blue chip stocks is aligned with our view on why Singapore stocks are still worth looking at in 2026.

Earlier, we shared that we would consider looking beyond Singapore REITs to Singapore blue chip stocks for more diversified dividend income, especially when the dividends are supported by earnings growth, strong balance sheets and sustainable payout ratios.

By combining different sources of dividends, investors may be able to build a more resilient income portfolio over time. Learn how to build a more dependable stream of income that can hold up across cycles here.

Which Singapore dividend blue chip stocks are you watching as the STI reaches new highs? Share your thoughts in the comments below or join the discussion in our Telegram group!

Planning to invest in Singapore stocks? Compare the best Singapore brokers to find the right trading platform, and see the latest promotions and sign-up rewards available.

Follow Beansprout on YouTube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

1 comments

- jane • 29 Jun 2026 11:59 PM